Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

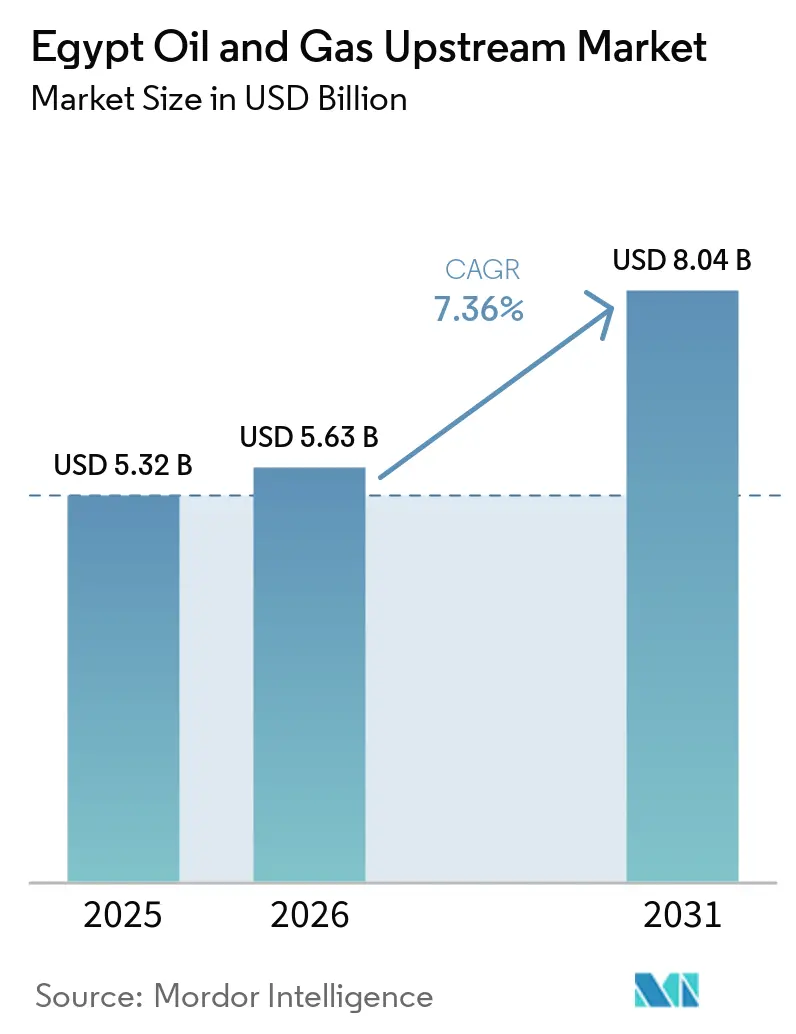

| Base Year Market Size (2025) | USD 5.32 Billion |

| Market Size (2026) | USD 5.63 Billion |

| Market Size (2031) | USD 8.04 Billion |

| Growth Rate (2026 - 2031) | 7.36% CAGR |

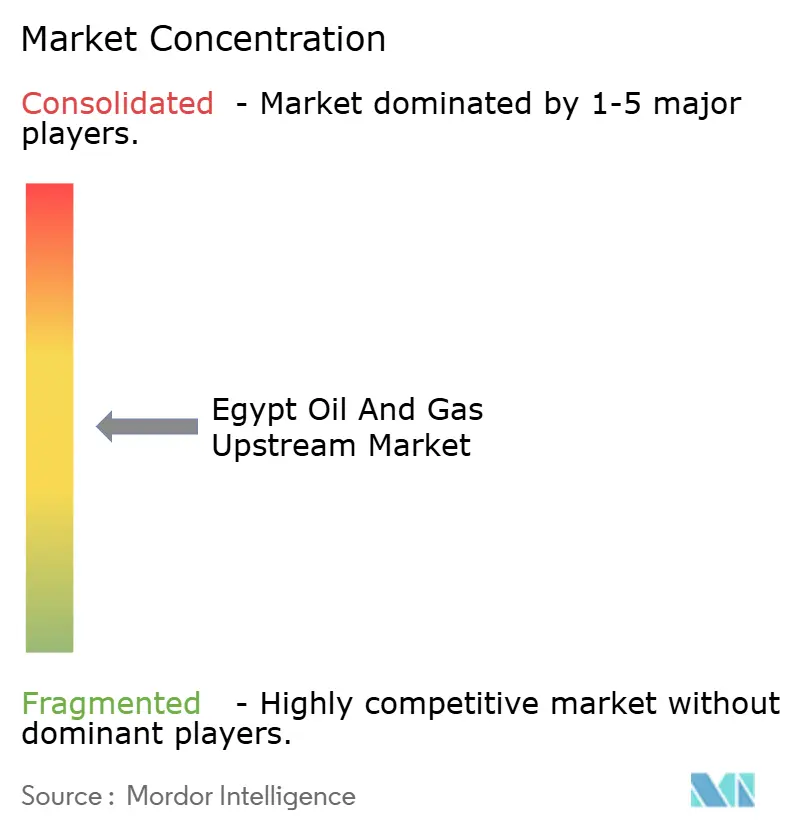

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Oil And Gas Upstream Market Analysis by Mordor Intelligence

The Egypt Oil And Gas Upstream Market size is projected to expand from USD 5.32 billion in 2025 and USD 5.63 billion in 2026 to USD 8.04 billion by 2031, registering a CAGR of 7.36% between 2026 to 2031.

Recent performance reflects a paradox: gas output slipped 14% in 2025 to a nine-year low, yet international oil companies (IOCs) collectively earmarked USD 1.1 billion for 21 new agreements after the government unveiled production-linked fiscal incentives in August 2024. Operators are channeling capital toward deep-water Mediterranean prospects where decline rates are lower, and export routes to Idku and Damietta liquefied-natural-gas (LNG) plants support pricing power. Faster clearance of Egyptian General Petroleum Corporation (EGPC) arrears, down 77.8% over seven months in 2025, has lifted confidence that cash flows will be repatriated on time. At the same time, diesel prices climbed from EGP 13.50 to EGP 15.50 per liter in April 2025 as Egypt advances toward full subsidy removal, compressing domestic netbacks for high-opex onshore fields.

Key Report Takeaways

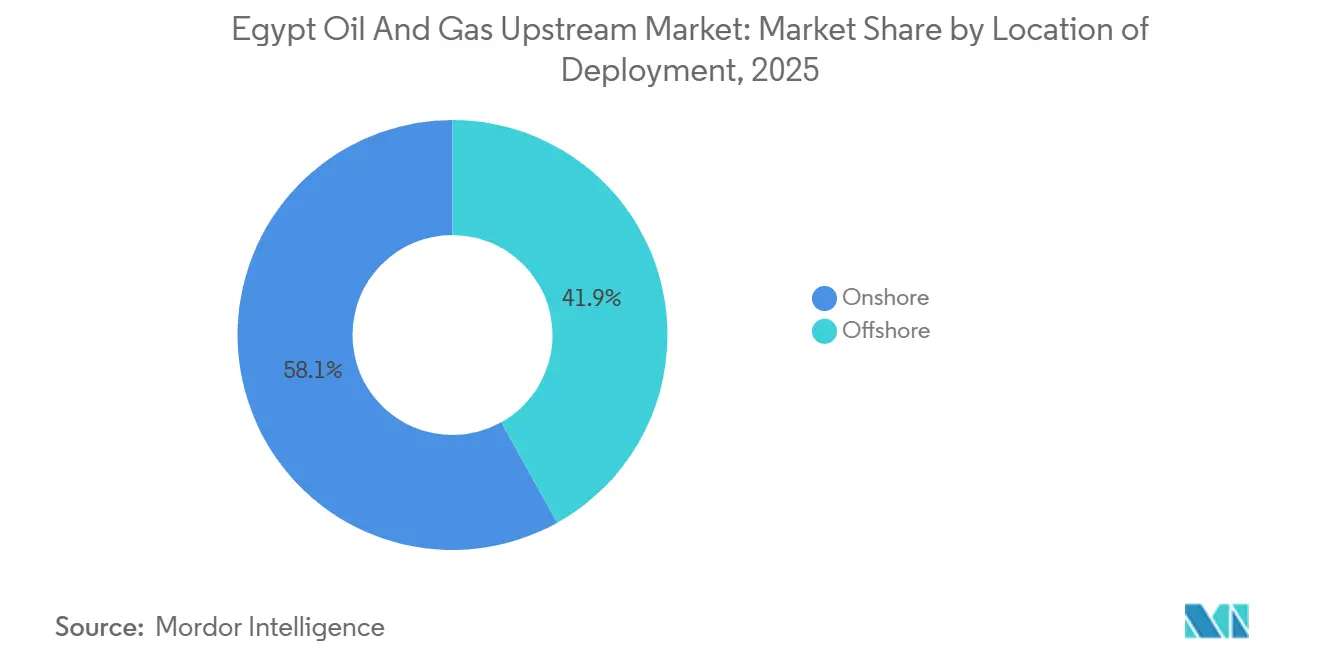

- By location of deployment, onshore operations led with 58.1% Egypt's oil and gas upstream market share in 2025, while offshore is expected to grow at 8.1% through 2031.

- By resource type, crude oil accounted for 60.9% Egypt's oil and gas upstream market size in 2025, and natural gas is expected to expand at a 7.7% CAGR to 2031.

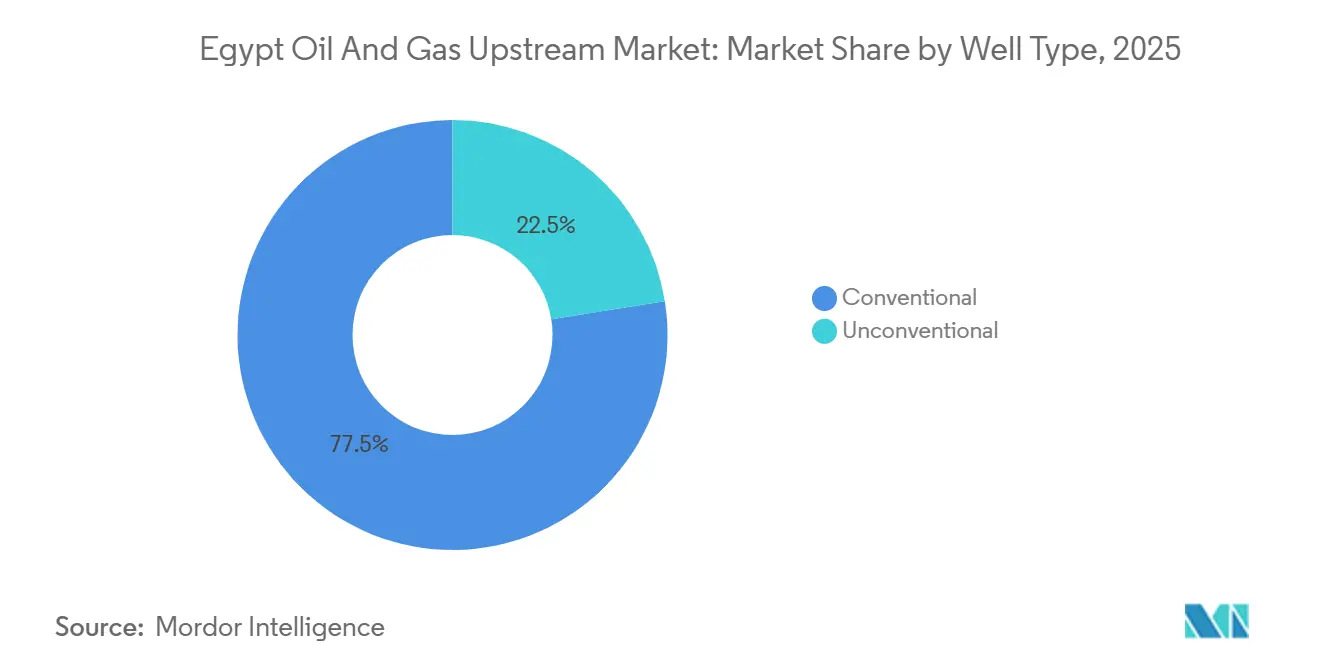

- By well type, conventional completions commanded 77.5% of Egypt's oil and gas upstream market share in 2025; unconventional wells are expected to grow at an 8.3% CAGR during 2026-2031.

- By service, development and production captured 61.7% share of Egypt's oil and gas upstream market size in 2025, whereas decommissioning is projected to grow at a 7.9% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Egypt Oil And Gas Upstream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated development of deep-water Mediterranean gas plays | +1.8% | Mediterranean offshore blocks | Medium term (2-4 years) |

| Entry of new IOCs leveraging production-linked fiscal incentives | +1.2% | National, Western Desert & offshore | Short term (≤ 2 years) |

| Reinforced regional demand pull via East-Med Gas Forum export routes | +1.0% | Damietta & Idku LNG corridors | Long term (≥ 4 years) |

| Revival of mature Western Desert fields through EOR pilots | +0.9% | Western Desert basins | Medium term (2-4 years) |

| Digital oil-field roll-outs lowering lifting costs | +0.7% | West Nile Delta pilot assets | Short term (≤ 2 years) |

| Egypt–Israeli pipeline reversals expanding spare capacity | +0.5% | Eastern Mediterranean corridor | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Development of Deep-Water Mediterranean Gas Plays

Mediterranean wells between 300 m and 1,500 m water depth are now the centerpiece of Egypt’s growth pipeline, supported by BP’s five-well campaign starting 2026 and Eni’s USD 80 million Noor tie-in that will add 100 MMcf/d by mid-2026.[1]BP plc, “BP Signs 5-Well Mediterranean Exploration MoU,” bp.com Shell’s West Mina cluster should supply 160 MMcf/d by end-2026 after a USD 300 million commitment. Viridien and SLB launched a large-scale ocean-bottom-node seismic survey in Q1-2026, confirming sustained exploration appetite. Although offshore capex is high, deep-water wells can cost more than USD 50 million, government clearance of EGPC arrears has strengthened fiscal visibility.

Entry of New IOCs Leveraging Production-Linked Fiscal Incentives

An R-factor production-sharing model introduced in August 2024 allows contractor take a rise in early cost-recovery phases, spurring QatarEnergy to farm into three Mediterranean blocks during 2024-2025. Chevron redirected funds from the Red Sea to the Nargis prospect, while EGAS awarded six new blocks in June 2025, underpinning a 480-well drilling roadmap through 2030. The framework’s credibility hinges on continued arrears discipline; any backsliding would undercut marginal economics.

Reinforced Regional Demand Pull via East-Med Gas Forum Export Routes

Egypt’s Damietta and Idku LNG terminals anchor regional monetization. Agreements signed with Cyprus in February 2025 for Cronos and Aphrodite tie-backs, and a USD 35 billion Leviathan-to-Egypt outline announced in August 2025, extend the transport grid. Yet actual flows fell to 730 MMcf/d in November 2025 due to pipeline bottlenecks, and Chevron’s 600 MMcf/d Nitzana spur has slipped to a 2028 start-up. The export architecture, therefore, both amplifies upside and embeds geopolitical risk.

Revival of Mature Western Desert Fields Through Enhanced-Oil-Recovery Pilots

Carbon-dioxide miscible flooding could lift Horus recovery factors from 23.7% to 37.3%, while the Morgan field is testing low-salinity sweeps. IPR Energy’s Alamein-Yidma discovery and TAG Oil’s 3.2 billion-barrel SERQ concession underscore remaining potential. Success depends on reliable CO₂ supply chains and stable fiscal terms amid foreign-exchange shortages.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Subsidy phase-out elevating domestic breakevens | -1.3% | National, with acute impact on onshore oil producers | Short term (≤ 2 years) |

| Above-ground security risks in Sinai & frontier concessions | -0.6% | Sinai Peninsula, Gulf of Suez frontier blocks | Medium term (2-4 years) |

| Heightened water-stress limiting frac-water availability | -0.4% | Western Desert unconventional plays | Long term (≥ 4 years) |

| Rising ESG-linked financing costs for greenfield oil projects | -0.5% | National, particularly new crude-oil developments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Subsidy Phase-Out Elevating Domestic Breakevens

Diesel increased to EGP 15.50 per liter in April 2025, continuing a stair-step path to full cost-recovery pricing by December 2025 under the IMF program.[2]International Monetary Fund, “Extended Fund Facility Review,” imf.org Monthly subsidy spending fell from EGP 40 billion in early 2024 to EGP 10 billion by late 2025. Higher fuel and electricity tariffs inflate service costs and squeeze high-opex onshore wells, forcing operators either to export or deploy enhanced-oil-recovery to stay below USD 30 per-barrel breakevens.

Above-Ground Security Risks in Sinai & Frontier Concessions

Daesh Wilaya Sinai resumed infrastructure attacks near the Suez Canal in 2022, elevating insurance premiums by up to 10% for Sinai blocks. Chevron exited Red Sea Block 1 in April 2025, citing risk-adjusted economics, and other firms are favoring Western Desert or offshore acreage where military presence is stronger. Physical losses have been limited, but the perception of danger raises capital costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Location of Deployment: Offshore Gains Outpace Onshore Base

The offshore segment accounted for 41.9% of the Egyptian oil and gas upstream market size in 2025 and is projected to expand at an 8.1% CAGR over 2026-2031. Production from BP’s Harmattan (125 MMcf/d gas, 3,300 b/d condensate from Q1-2026) and Shell’s Merneith wells is emblematic of deep-water momentum.[3]Shell plc, “Shell Commits $300 Million to West Delta Deep Marine,” shell.com Onshore assets retain the larger installed base but confront higher water-handling costs and subsidy-driven margin compression. Mid-tier firms such as United Energy Group, which boosted output to 39,000 boe/d after acquiring Apex in February 2025, are consolidating these mature fields.

Offshore operators benefit from export optionality via LNG plants, insulating returns as domestic prices liberalize. However, the upfront spend on single wells can top USD 50 million, concentrating control among major IOCs and Gulf national oil companies. Onshore operators depend increasingly on low-cost infill and enhanced-oil-recovery programs to offset decline, reinforcing a two-speed market structure.

By Resource Type: Gas Ascendancy Driven by Regional Hub Strategy

Crude oil led with 60.9% Egypt's oil and gas upstream market share in 2025, yet natural gas is forecast to grow at 7.7% CAGR and narrow the gap. Eni's Noor and Shell's West Mina alone add 260 MMcf/d by end-2026, while BP targets Pliocene reservoirs across five new wells.[4]Eni SpA, “Eni Advances Noor Field Development,” eni.com Domestic gas output fell to 4.2 Bcf/d in 2025, forcing Egypt to sign a USD 3 billion LNG import deal covering 60 cargoes with TotalEnergies and Shell. The government's ambition to become the East-Med processing hub ensures policy support for gas projects, but arresting decline at Zohr remains pivotal.

Crude remains essential for hard-currency revenue, especially Western Desert light grades that fetch export premiums. Fields like North Safa (2,250 b/d from 2025) illustrate niche growth. The net resource split to 2031 will reflect success rates in Mediterranean infill drilling and scale-up of Western Desert EOR pilots.

By Well Type: Unconventional Surge from Low Base

Conventional wells dominated Egypt's oil and gas upstream market size in 2025, yet unconventional spuds are forecast to rise at 8.3% CAGR. TAG Oil's' BED-1 encountered 532 MMbbl in place and raised CAD 5 million in February 2026 to test multistage fracturing. Water scarcity, renewable supply is only 570 m³ per-capita per-year, which means scaling depends on produced-water recycling and desalination tie-ins. Conventional vertical wells, meanwhile, keep per-well costs near USD 8 million in the Western Desert, preserving their near-term dominance.

If pilot frac programs prove commercial, unconventional share could approach 25% by 2031. Service readiness remains a gating factor; only a handful of rigs and pressure-pumping spreads in Egypt can perform horizontal multistage completions, inflating lead times.

By Service: Decommissioning Emerges as Fastest-Growing Segment

Development and production services held 61.7% Egypt oil and gas upstream market share in 2025, but decommissioning is set to grow fastest at 7.9% CAGR. More than 400 Gulf of Suez wells exceed 90% water cut, and structural integrity issues demand plug-and-abandonment campaigns. Egypt lacks a clear cost-recovery framework analogous to the North Sea’s OSPAR convention, so early movers such as Eni are shaping standards through selective well abandonment in Belayim.[5]OSPAR Commission, “Guidelines for Decommissioning,” ospar.org

Exploration services also benefit from the government’s 480-well plan and the 2026 ocean-bottom-node seismic program. Diesel inflation from subsidy reforms lifted logistics costs by around 15% in 2025, squeezing service margins, yet digital solutions that trim drilling time partially offset cost pressure.

Geography Analysis

The Western Desert dominates onshore crude volumes, hosting enhanced-oil-recovery pilots and unconventional tight oil. IPR Energy’s new Alamein-Yidma well at 2,765 b/d and TAG Oil’s 3.2 billion-barrel SERQ contingent resource highlight remaining upside. However, lifting costs are rising with diesel prices, and frac-water availability is limited.

Mediterranean offshore blocks, stretching from the West Nile Delta to the Levantine extension, deliver the bulk of new gas investment. BP’s 2026 drilling, Eni’s Noor incremental, and Shell’s West Mina illustrate a pipeline that supports the offshore segment’s 8.1% CAGR. LNG terminals at Idku and Damietta permit cargo diversion into premium Atlantic Basin markets when economics justify.

The Gulf of Suez, Egypt’s oldest producing province, is shifting toward decommissioning and selective infill. Eni’s Belayim Offshore 133 well delivered 1,500 b/d in February 2026, but mainly offsets base decline. Security issues confine Sinai activity; Daesh’s sporadic attacks inflate insurance costs, steering capital away from Red Sea frontier acreage.

Competitive Landscape

Egypt features a middle-concentrated structure: BP and partners supply roughly 70% of gas, yet the top five firms do not reach 80% combined share, leaving room for mid-tiers. Arcius Energy, a BP-ADNOC joint venture, acquired the Harmattan development in November 2025, signaling consolidation around core gas hubs. QatarEnergy executed three farm-ins across 2024-2025, reflecting Gulf NOCs’ appetite for Mediterranean exposure.

Mid-tier consolidators such as United Energy Group are picking up Western Desert packages shed by cash-strapped independents, moving production to 39,000 boe/d after the Apex deal. Technology adoption differentiates leaders: real-time drilling analytics via Corva and the Egypt Upstream Gateway shorten cycle times and lower costs. Regulatory momentum around methane measurement favors IOCs with robust ESG systems as the IMF’s Resilience and Sustainability Facility mandates operator-level MRV by August 2026.

Egypt Oil And Gas Upstream Industry Leaders

BP Plc

Eni SpA

Shell Plc.

Apache Corp.

Chevron Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Shell launched a multi-well offshore drilling program in Egypt's Mediterranean region. The campaign targets West Mena development wells and frontier exploration in the Herodotus Basin. The expected output includes 160 million cubic feet per day (mcf/d) of gas and 1,900 barrels per day (bpd) of condensate. This initiative aims to bolster foreign investment confidence and accelerate upstream growth.

- November 2025: Egypt signed a three-year extension agreement with SLB to invest USD 44 million in upgrading the Egypt Upstream Gateway. The enhancements include advanced digital data access and a major ocean-bottom node (OBN) seismic survey covering 95,000 square kilometers. These upgrades are designed to attract upstream investment and mitigate exploration risks.

- November 2025: Egypt issued its first R-Factor-based production-sharing tender for four Red Sea blocks. This approach aligns investor rewards with associated risks to attract international exploration companies. The six-month bidding window is part of a broader plan to enhance reserves through a USD 5.7 billion, 480-well exploration program.

- March 2025: Egypt outlined significant upstream expansion plans, including new auctions, the development of a USD 7 billion petrochemical complex, and accelerated offshore exploration efforts to address declining gas output. The strategy emphasizes increased foreign participation through the Egypt Upstream Gateway, aiming to strengthen long-term production and energy security.

Egypt Oil And Gas Upstream Market Report Scope

The oil and gas upstream market encompasses the exploration and production (E&P) segment of the petroleum industry. This includes activities such as locating, drilling, and extracting crude oil and natural gas from underground or underwater reservoirs.

The Egypt oil and gas upstream market is segmented into location of deployment, resource type, well type, and service. By location of deployment, the market is segmented into onshore and offshore. By resource type, the market is divided into crude oil and natural gas. By well type, the market is segmented into conventional and unconventional. By service, the market is divided into exploration, development and production, and decommissioning. The market sizing and forecasts for all the above segments are given in terms of value (USD billion).

By Location of Deployment

| Onshore |

| Offshore |

By Resource Type

| Crude Oil |

| Natural Gas |

By Well Type

| Conventional |

| Unconventional |

By Service

| Exploration |

| Development and Production |

| Decomissioning |

| By Location of Deployment | Onshore |

| Offshore | |

| By Resource Type | Crude Oil |

| Natural Gas | |

| By Well Type | Conventional |

| Unconventional | |

| By Service | Exploration |

| Development and Production | |

| Decomissioning |

Key Questions Answered in the Report

How large is the Egyptian oil and gas upstream market in 2026?

It stands at USD 5.63 billion in 2026 and is on track to reach USD 8.04 billion in 2031.

How fast is Egyptian upstream spending shifting from onshore to offshore zones?

Offshore activity in the Egypt oil and gas upstream market is projected to grow at an 8.1% CAGR through 2031 while onshore grows slower, narrowing the share gap over the forecast period.

Which companies are leading new Mediterranean gas exploration?

BP, Eni, Shell and QatarEnergy are spearheading deep-water programs, supported by a five-well BP campaign, Eni's Noor tie-in and Shell's West Mina development.

Why is decommissioning the fastest-growing service segment?

An aging Gulf of Suez asset base and water cuts above 90% are driving 7.9% CAGR growth in decommissioning services through 2031 as operators plug and abandon idle wells.

How will Egypt meet frac-water needs for unconventional plays?

Operators plan produced-water recycling and, where economic, seawater desalination tie-ins to mitigate freshwater scarcity of only 570 m³ per-capita annually.

What impact will subsidy removal have on field economics?

Diesel reached EGP 15.50/L in 2025, lifting onshore lifting costs and raising breakevens, yet deep-water gas tied to LNG exports remains attractive despite subsidy reforms.

Page last updated on: