Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

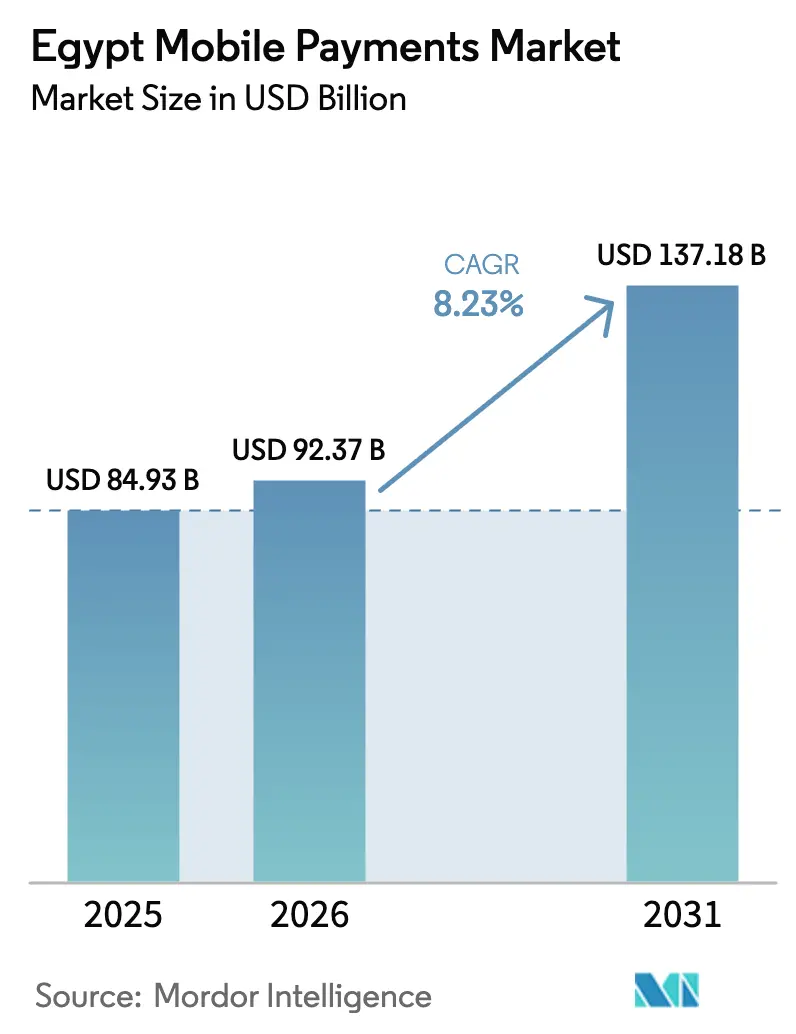

| Base Year Market Size (2025) | USD 84.93 Billion |

| Market Size (2026) | USD 92.37 Billion |

| Market Size (2031) | USD 137.18 Billion |

| Growth Rate (2026 - 2031) | 8.23% CAGR |

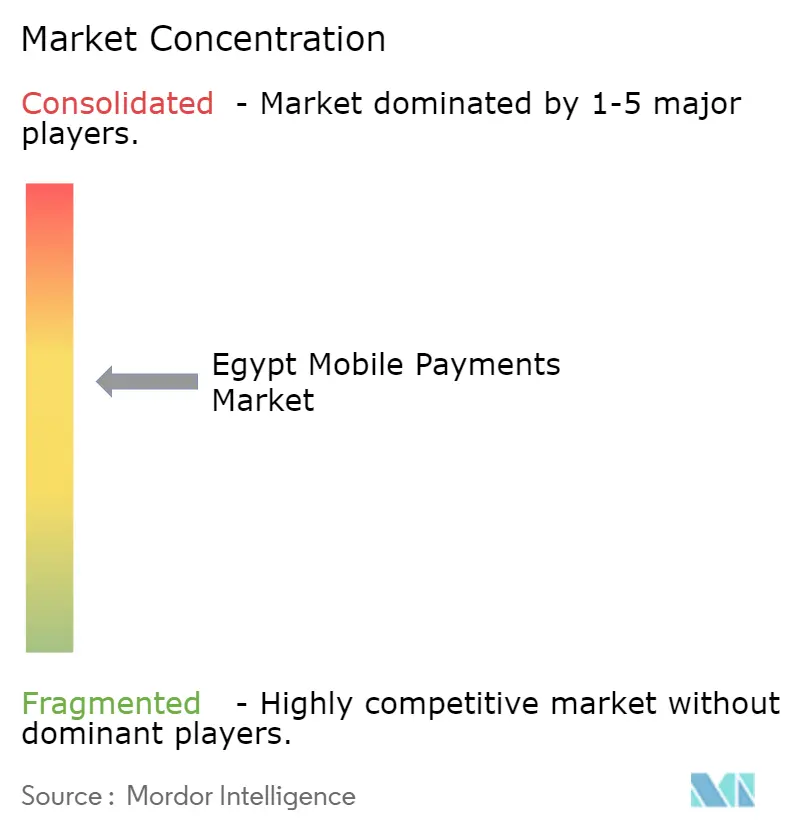

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Mobile Payments Market Analysis by Mordor Intelligence

The Egypt mobile payments market size is projected to be USD 84.93 billion in 2025, USD 92.37 billion in 2026, and reach USD 137.18 billion by 2031, growing at a CAGR of 8.23% from 2026 to 2031. A mandatory QR-code acceptance program, the tokenization of state-backed Meeza cards inside wallet apps, and the rapid scale-up of the InstaPay instant-payment rail are jointly accelerating cash-to-digital migration among consumers and micro-merchants. Wallet interoperability over InstaPay reduces switching frictions, while soft POS applications turn low-cost Android handsets into payment terminals that meet Central Bank of Egypt (CBE) compliance thresholds. Cross-border wallet-to-wallet remittances from the Gulf Cooperation Council (GCC) compress transfer fees below 3% and inject immediate liquidity into household budgets. Challenger fintechs layer buy-now-pay-later (BNPL) and value-added services on top of wallets, elevating average revenue per user and drawing venture investment despite margin compression from CBE fee caps.

Key Report Takeaways

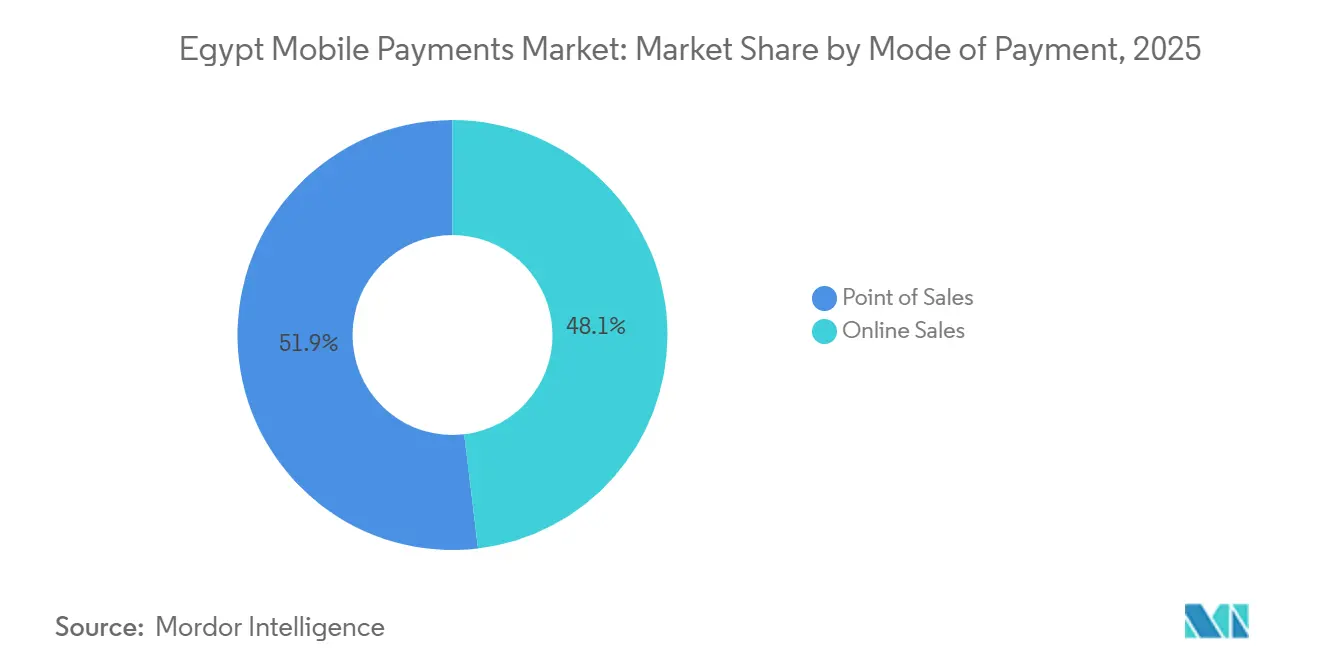

- By mode of payment, Online Sales led with 51.89% revenue share in 2025, while Point of Sales is forecast to expand at a 9.12% CAGR through 2031.

- By payment type, QR-based methods captured 48.67% of the Egypt mobile payments market share in 2025, yet NFC is poised to grow at a 10.24% CAGR as tokenization partnerships widen.

- By transaction type, Peer-to-Peer flows accounted for 53.92% of the Egypt mobile payments market size in 2025, whereas Person to Business transactions are set to advance at a 9.37% CAGR through 2031.

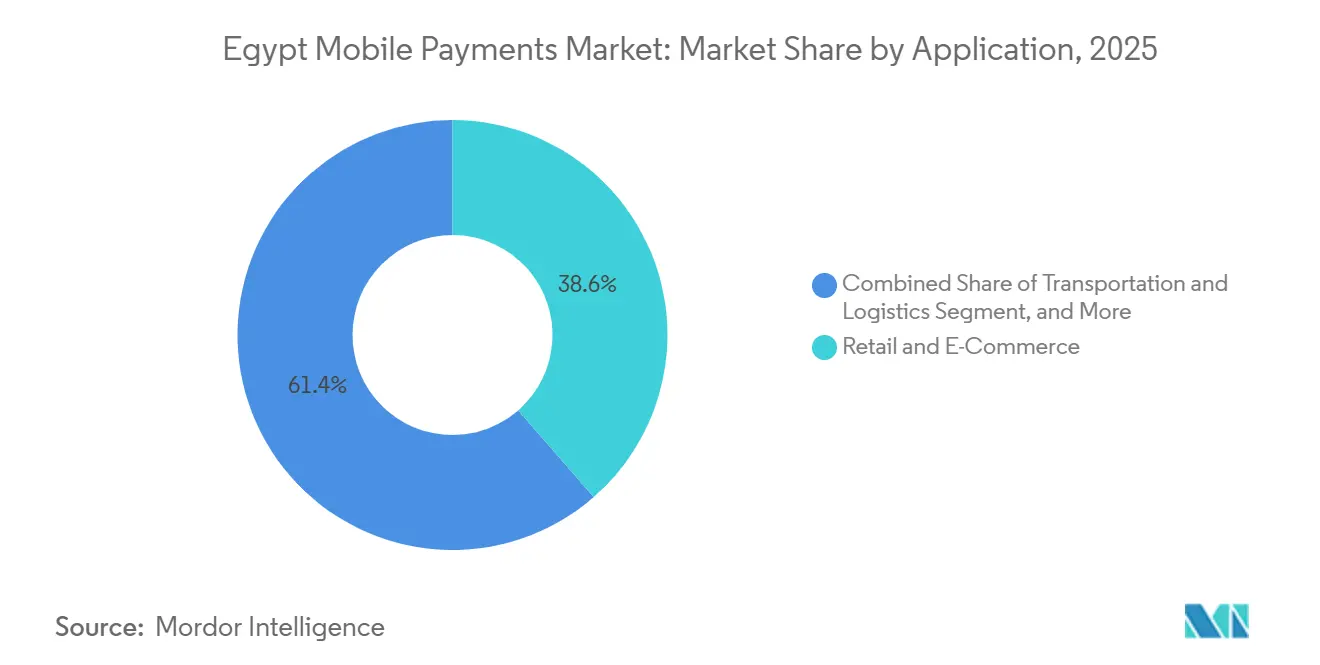

- By application, Retail and E-Commerce held 38.59% share of the Egypt mobile payments market size in 2025, while Transportation and Logistics is projected to accelerate at an 11.56% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Egypt Mobile Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Real-Time Payments via InstaPay Rails | +2.3% | National, strongest in Greater Cairo, Alexandria, Giza | Medium term (2-4 years) |

| State-Backed Meeza Cards Integration into Wallets | +1.8% | Urban centers and government-employee segments | Medium term (2-4 years) |

| Merchant Shift to QR-Based Acceptance Under CBE Mandate | +1.5% | Formal retail and hospitality sectors nationwide | Short term (≤ 2 years) |

| Cross-Border Remittance Corridor Digitization (GCC-Egypt) | +1.2% | Inflows from UAE, Saudi Arabia, Kuwait, Qatar | Medium term (2-4 years) |

| Buy-Now-Pay-Later Apps Embedding Wallet Checkout | +0.9% | Cairo, Alexandria, Giza | Short term (≤ 2 years) |

| Generative-AI Fraud Analytics Lowering Charge-Back Rates | +0.5% | Early adopters among tier-1 banks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Real-Time Payments Via InstaPay Rails

InstaPay’s instant-settlement design removes the multi-day clearing cycle that previously deterred micro-merchants from digital acceptance. By end-2024, 12.5 million users executed 1.5 billion transfers worth EGP 2.9 trillion (USD 62.2 billion), firmly positioning the rail as Egypt’s de facto interbank clearing layer.[1]Central Bank of Egypt, “Monthly Statistical Bulletin,” CBE.ORG.EG The CBE’s decision to layer QR-code functionality onto InstaPay lowers merchant onboarding costs to near zero because a smartphone and static sticker replace dedicated point-of-sale hardware. Network effects intensify as every licensed wallet plugs into the same rail, encouraging single-app usage for consumers and widening addressable merchant coverage. The December 2024 cross-border pilot extended InstaPay into GCC corridors, accelerating instant liquidity for remittance recipients and adding a high-margin revenue stream for wallet operators.

State-Backed Meeza Cards Integration Into Wallets

Meeza counted 43.5 million cards in circulation by June 2025, making it Egypt’s largest domestic scheme . Mandatory tokenization of these cards into every wallet channels public-sector payroll, pension, and subsidy disbursements directly into the digital ecosystem, boosting daily active usage. Integration sidesteps earlier siloed wallet programs because Meeza credentials interoperate across issuing banks and InstaPay. Security improves through device-level tokenization, a key lesson from Apple Pay’s 40 million-plus NFC transactions in six months. Wallet providers gain a captive user base for bill payments and micro-credit upsell, while government agencies cut cash-handling overheads.

Merchant Shift to QR-Based Acceptance Under CBE Mandate

A June 2024 CBE directive compels every merchant with annual turnover above EGP 500,000 (USD 10,726) to accept digital payments, igniting a national QR rollout. Compared with a conventional POS terminal costing EGP 2,000 (USD 43) or more, a printed QR code slashes capital outlay and eliminates maintenance. Paymob onboarded 390,000 merchants in 2025, with QR transactions dominating sign-ups.[2]Paymob Solutions, “About Paymob,” PAYMOB.COM Fawry and telecom wallets piggy-backed on their agent footprints, distributing QR stickers to kiosks, cafés, and ride-hailing fleets. Transaction fees average 1.5-2.0%, and InstaPay guarantees next-day settlement, enhancing cash-flow visibility for micro-retailers.

Cross-Border Remittance Corridor Digitization (GCC-Egypt)

The GCC supplied USD 19.5 billion of remittances to Egypt in 2023. InstaPay’s December 2024 pilot and Vodafone Cash’s April 2025 wallet-to-wallet service trimmed average fees below 3% and delivered funds in minutes, replacing cash-based money-transfer operators that once charged up to 8%. TerraPay’s February 2026 alliance with botim money broadens coverage across Africa.[3]TerraPay, “Cross-Border Payments,” TERRAPAY.COM Faster, cheaper flows increase disposable income in Upper Egypt and Nile Delta households, expanding merchant purchases and bill-payment volumes within wallets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cash-Centred Consumer Culture Outside Urban Centers | -1.1% | Rural governorates and peri-urban areas | Long term (≥ 4 years) |

| SIM-Swap and Social-Engineering Fraud Uptick | -0.7% | Nationwide, higher in dense cities | Short term (≤ 2 years) |

| Inconsistent KYC Enforcement Across Agents | -0.4% | Informal agent networks nationwide | Medium term (2-4 years) |

| Limited Merchant POS NFC Penetration | -0.3% | Small and micro-merchants nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cash-Centred Consumer Culture Outside Urban Centers

The Global Findex 2024 survey shows only 43.4% of adults hold a transaction account, and mobile-money usage is 13.8%, far below Egypt’s headline 76.3% inclusion rate. Informal merchants fear taxation, connectivity is unreliable, and older cohorts regard cash as safer, sustaining physical currency dominance in rural governorates. Because the CBE mandate targets merchants above a revenue floor, millions of micro-enterprises remain exempt, limiting network effects. Agent networks must continue expensive cash-in and cash-out operations, squeezing unit margins and slowing adoption curves beyond Greater Cairo and Alexandria.

SIM-Swap and Social-Engineering Fraud Uptick

SIM-swap attacks exploit loopholes in telecom verification processes, hijacking SMS one-time passwords and draining wallet balances. The GSMA’s 2024 report lists SIM-swap as a top threat in mobile-money markets.[4]GSMA, “State of the Industry Report on Mobile Money 2024,” GSMA.COM Egypt’s fragmented agent landscape and variable identity checks heighten vulnerability, prompting the CBE to tighten KYC rules and cap unverified-wallet limits. Fraud episodes erode consumer trust and push risk-averse users back to cash, forcing wallet operators to invest in biometric authentication and AI-driven anomaly detection. Elevated compliance costs weigh on profitability until fraud analytics mature and user education campaigns gain traction.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment: Point of Sales Momentum Accelerates With QR Adoption

Point of Sales channels accounted for 48.11% of the Egypt mobile payments market size in 2025 and are forecast to expand at a 9.12% CAGR through 2031. Merchant compliance with the CBE mandate, combined with near-zero onboarding costs for QR stickers, is converting cash-only counters into digital acceptance points at unprecedented speed. Soft POS applications that transform Android phones into terminals eliminate hardware expense and integrate seamlessly with InstaPay, delivering same-day settlement that rivals cash liquidity. Fawry distributed QR to 382,000 agents, while Paymob enabled 390,000 merchants across retail, transport, and hospitality, shrinking the dominance gap with Online Sales.

Online Sales, though still larger at 51.89% share in 2025, face logistics headwinds such as last-mile costs and cash-on-delivery preferences outside Cairo. Yet the line between channels is blurring: Careem Pay’s wallet-transfer launch lets consumers fund ride-hailing and food delivery in-app, exemplifying omnichannel commerce. The Egypt mobile payments market benefits when merchants offer unified checkout both online and in-store, deepening user stickiness and transaction frequency. As QR acceptance becomes ubiquitous, the competitive axis shifts from acceptance availability to value-added features such as BNPL and loyalty integration.

By Payment Type: NFC Set To Outpace QR From a Low Base

QR-based methods retained 48.67% share in 2025 due to effortless deployment across smartphones; nevertheless, NFC transactions are projected to grow at 10.24% CAGR, the fastest among payment types. Apple Pay’s December 2024 entry processed more than 40 million transactions inside six months, proving latent appetite for tap-to-pay convenience among affluent users. Google Wallet and Samsung Pay broaden device coverage, while First Abu Dhabi Bank Misr and Geidea are rolling out contactless-capable POS readers.

The choke point is merchant hardware: many existing terminals lack NFC and small retailers balk at upgrade costs. Mastercard’s Tap on Phone software may tilt economics by letting merchants accept NFC on unmodified Android devices, but pilots remain limited. QR enjoys full interoperability via InstaPay’s standardized spec, keeping switching costs low. Over time, dual-mode acceptance will prevail, giving consumers freedom to pick the fastest option and forcing acquirers to streamline settlement across both rails.

By Transaction Type: Person to Business Formalization Propels Growth

Peer-to-Peer flows seized 53.92% share in 2025 owing to zero-fee InstaPay transfers, yet Person to Business payments are forecast to rise at a 9.37% CAGR, eclipsing overall market growth. Mandatory merchant acceptance and accelerating QR deployments encourage consumers to channel everyday purchases through wallets. Fawry and Paymob collectively enrolled more than 770,000 merchants, while Orange Cash processed EGP 943.4 billion (USD 20.3 billion) in Q2 2025, up 72% year on year, indicating robust Person to Business velocity.

P2P remains the onboarding gateway for first-time users, but revenue upside lies in merchant payments that carry interchange and discount fees. Embedded BNPL further boosts ticket sizes: Valu logged EGP 10.56 billion (0.23 billion) gross merchandise value in H1 2025, with many transactions initiated via wallet checkout. As micro-enterprises formalize to access digital credit, the Egypt mobile payments industry derives compounding gains from transactional data leveraged for underwriting.

By Application: Transportation and Logistics Lead Sector-Specific CAGR

Retail and E-Commerce cornered 38.59% of the Egypt mobile payments market size in 2025, yet Transportation and Logistics are forecast to expand at an 11.56% CAGR to 2031. Cairo Metro activated contactless gates on Lines 1 and 2 in December 2025, and National Bank of Egypt allied with Mastercard and Mwasalat Misr to roll out tap-to-pay on intercity buses, catalyzing rapid ridership adoption. Ride-hailing super-apps such as Careem integrate wallet transfers, embedding payments deep into daily commutes.

Hospitality and food service gain from surging online ordering and a growing tourism pipeline that aims for 30 million visitors by 2028. Contactless and QR payment options reduce foreign-exchange hassles for travelers, stimulating merchant upgrades at Red Sea resorts. In healthcare, Valu’s partnership with Vezeeta and Geidea opens installment plans for medical consultations, expanding wallet relevance into essential services. Education, agriculture, and government disbursements round out a long tail of emerging verticals that will collectively push transaction diversity higher over the forecast horizon.

Geography Analysis

Wallet uptake concentrates in Greater Cairo, Alexandria, and Giza, where smartphone penetration tops 85%, merchant density is high, and soft POS coverage widens daily. Orange Cash reported 46.3 million active wallets by mid-2025 and EGP 943.4 billion (USD 20.3 billion) in quarterly throughput, attesting to urban scale. Fawry’s 382,000-strong agent network bridges physical-digital gaps, operating kiosks, post-office counters, and mobile vans in secondary cities and rural townships.

Remittance-heavy governorates in Upper Egypt receive immediate liquidity via GCC wallet-to-wallet transfers that now settle in minutes and cost under 3%, versus multi-hour cash pickups before digitization. World Bank pilots added 250,000 new accounts and lifted women’s remittance transactions by 13%, a material boost to inclusive finance. Tourism clusters along the Red Sea, Luxor, and Aswan adopt contactless acceptance to meet visitor expectations, and hotel lobby shops increasingly print bilingual QR codes linked to InstaPay.

Rural adoption trails due to patchy internet, limited digital literacy, and entrenched cash habits. Telecoms are extending 4G and 5G coverage, but electricity reliability and device affordability continue to hamper consistent wallet usage. Government plans for digital IDs and e-health cards promise new payment touchpoints that could catalyze uptake outside urban cores. Until then, agent networks will remain indispensable for cash-in and cash-out, albeit at higher operating cost.

Competitive Landscape

No single provider dominates the Egypt mobile payments market, reflecting CBE-mandated interoperability and diverse use-case coverage. Vodafone Cash, Orange Cash, and Etisalat Cash exploit subscriber scale and airtime distribution, yet none climb past a 15% transaction share. Bank-affiliated apps from Commercial International Bank, National Bank of Egypt, and Banque Misr protect deposit bases while partnering with tokenization platforms for NFC capability.

Fawry pivots from bill-payment aggregator to full-stack fintech, fielding BNPL, merchant acquiring, and remittance corridors, backed by 6 million daily transactions and 52.9 million monthly users. Fintech challengers attack niche pain points: Paymob furnishes 50-plus payment methods to 390,000 merchants, Telda issues customizable prepaid cards for Gen Z, and MoneyFellows scales a digital ROSCA model that accumulated USD 1.5 billion in circulation value.

Strategic moves focus on ecosystem depth rather than rail exclusivity. Vodafone Cash’s GCC remittance service, Orange Cash’s gold-trading in-app feature, and Fawry’s Apple Pay tie-up illustrate vertical expansion to entrench users. Generative-AI fraud analytics, such as Network International’s deployment with Abu Dhabi Commercial Bank Egypt, seek efficiency gains and trust enhancement. With margins compressed by capped fees, providers differentiate through credit, savings, and investment add-ons that monetize stored value and data exhaust.

Egypt Mobile Payments Industry Leaders

Paypal Holdings Inc.

Samsung Corporation

Apple Inc

Google LLC (Alphabet Inc.)

Amazon.com Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: botim money and TerraPay extended wallet-to-wallet transfers across Africa, including Egypt, lowering remittance fees and latency.

- January 2026: Careem Pay enabled wallet funding for ride-hailing and food delivery in Egypt, embedding payments inside its super-app.

- January 2026: First Abu Dhabi Bank Misr introduced NFC-enabled POS terminals to accelerate tap-to-pay adoption among merchants.

- December 2025: Cairo Metro activated contactless fare machines on Lines 1 and 2, cutting cash handling and queue times.

Egypt Mobile Payments Market Report Scope

A mobile payment is a cash payment made for a product or service using a portable electronic device such as a smartphone, and technology can also be used to send money to friends or family members, among other things.

The Egypt Mobile Payments Market Report is Segmented by Mode of Payment (Point of Sales, Online Sales), Payment Type (NFC, QR-Based, Other Payment Types), Transaction Type (Peer-to-Peer, Person to Business), Application (Retail and e-Commerce, Transportation and Logistics, Hospitality and Food-Service, Government and Public Sector, Other Applications), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

By Mode of Payment

| Point of Sales |

| Online Sales |

By Payment Type

| NFC |

| QR-Based |

| Other Payment Types |

By Transaction Type

| Peer-to-Peer (P2P) |

| Person to Business |

By Application

| Retail and e-Commerce |

| Transportation and Logistics |

| Hospitality and Food-Service |

| Government and Public Sector |

| Other Applications (Education, Healthcare) |

| By Mode of Payment | Point of Sales |

| Online Sales | |

| By Payment Type | NFC |

| QR-Based | |

| Other Payment Types | |

| By Transaction Type | Peer-to-Peer (P2P) |

| Person to Business | |

| By Application | Retail and e-Commerce |

| Transportation and Logistics | |

| Hospitality and Food-Service | |

| Government and Public Sector | |

| Other Applications (Education, Healthcare) |

Key Questions Answered in the Report

How large will the Egypt mobile payments market be by 2031?

It is forecast to reach USD 137.18 billion, expanding at an 8.23% CAGR from 2026 to 2031.

Which payment channel is growing fastest?

Point of Sales transactions are projected to rise at a 9.12% CAGR thanks to the nationwide QR-code mandate.

Why is NFC adoption still limited in Egypt?

Legacy terminals lack contactless readers, and many small merchants favor low-cost QR stickers over hardware upgrades.

What segments benefit most from BNPL integration?

Retail, e-commerce, and increasingly healthcare see larger basket sizes and higher conversion when BNPL appears inside wallet checkout.

How are remittances affecting mobile payment volumes?

GCC wallet-to-wallet transfers now settle instantly at fees below 3%, boosting liquidity for households and driving wallet activity in Upper Egypt.

Which firms stand out in fraud mitigation?

Abu Dhabi Commercial Bank Egypt and Network International are early adopters of generative-AI analytics that cut charge-back rates.

Page last updated on: