Drainage Bottles Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

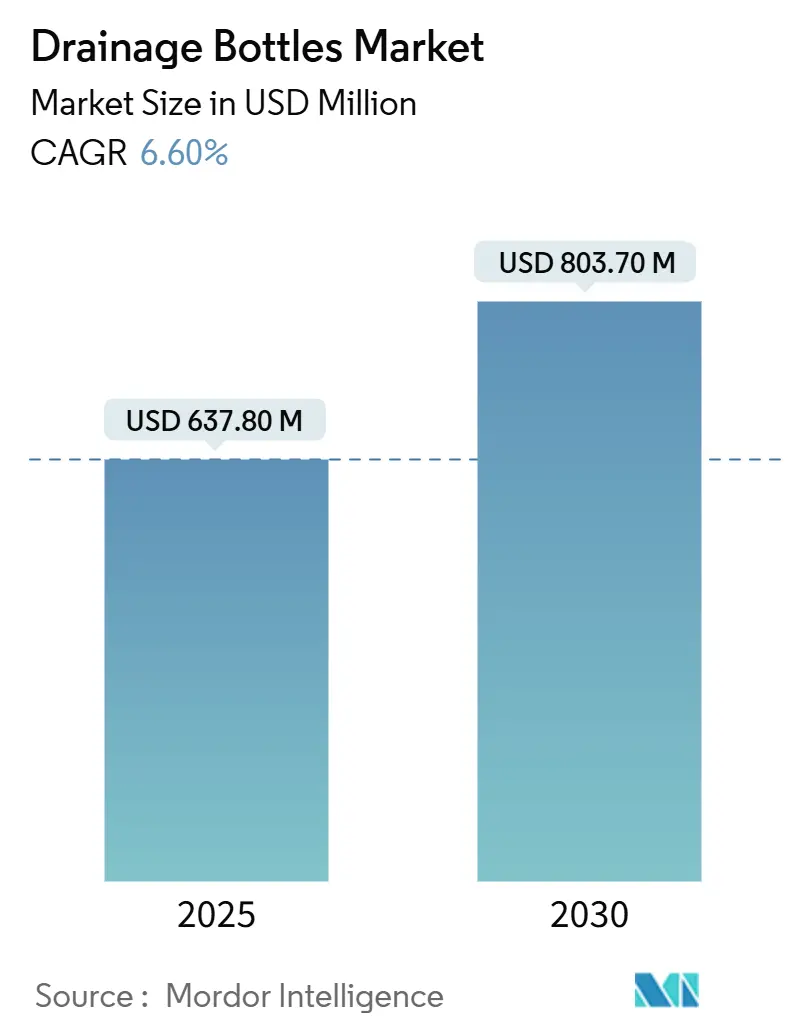

| Market Size (2025) | USD 637.80 Million |

| Market Size (2030) | USD 803.70 Million |

| Growth Rate (2025 - 2030) | 6.60% CAGR |

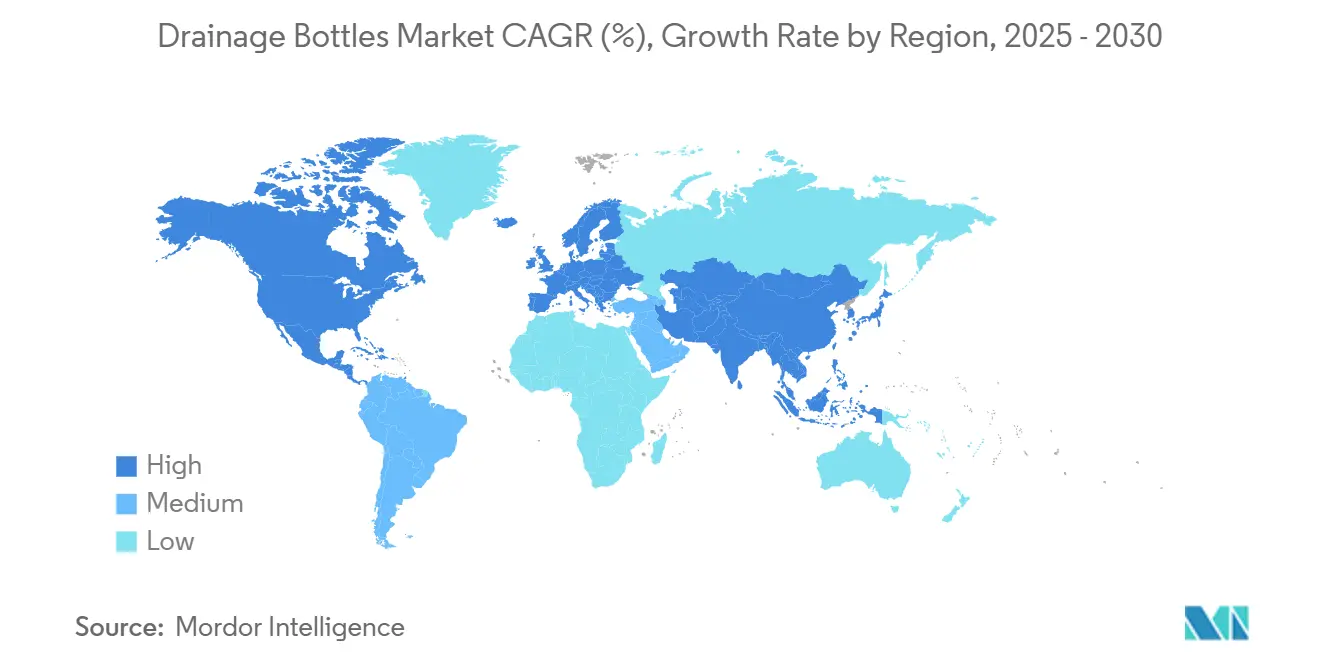

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Drainage Bottles Market Analysis by Mordor Intelligence

The drainage bottles market size stands at USD 637.8 million in 2025 and is forecast to reach USD 803.7 million by 2030, expanding at a 6.6% CAGR. Rising surgical volumes underpin this healthy trajectory, stricter infection-control rules that favor closed, single-use systems, and the accelerating shift of post-operative care into decentralized settings. Growing adoption of smart, digitally monitored drainage platforms is improving clinical decision-making and shortening length of stay, encouraging procurement by top-tier hospitals and ambulatory centers alike. Material innovation—particularly the migration from PVC toward silicone and other phthalate-free polymers—is reshaping supplier strategies as regulators tighten safety rules. Together, these forces are positioning the drainage bottles market for steady, innovation-driven growth into the next decade.

Key Report Takeaways

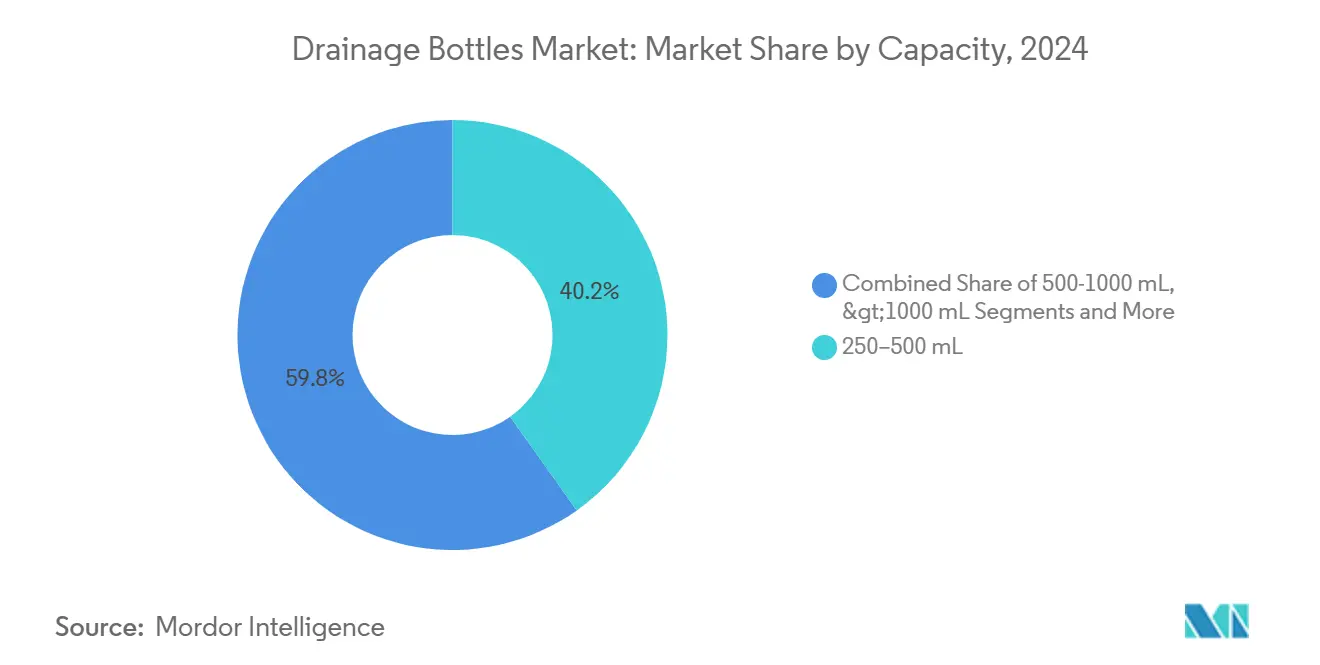

- By capacity, the 250-500 mL segment led with 40.2% of the drainage bottles market share in 2024; >1,000 mL systems are projected to log the fastest 8.6% CAGR through 2030.

- By material, polypropylene commanded 42.4% share of the drainage bottles market size in 2024, while silicone is advancing at a 7.2% CAGR to 2030.

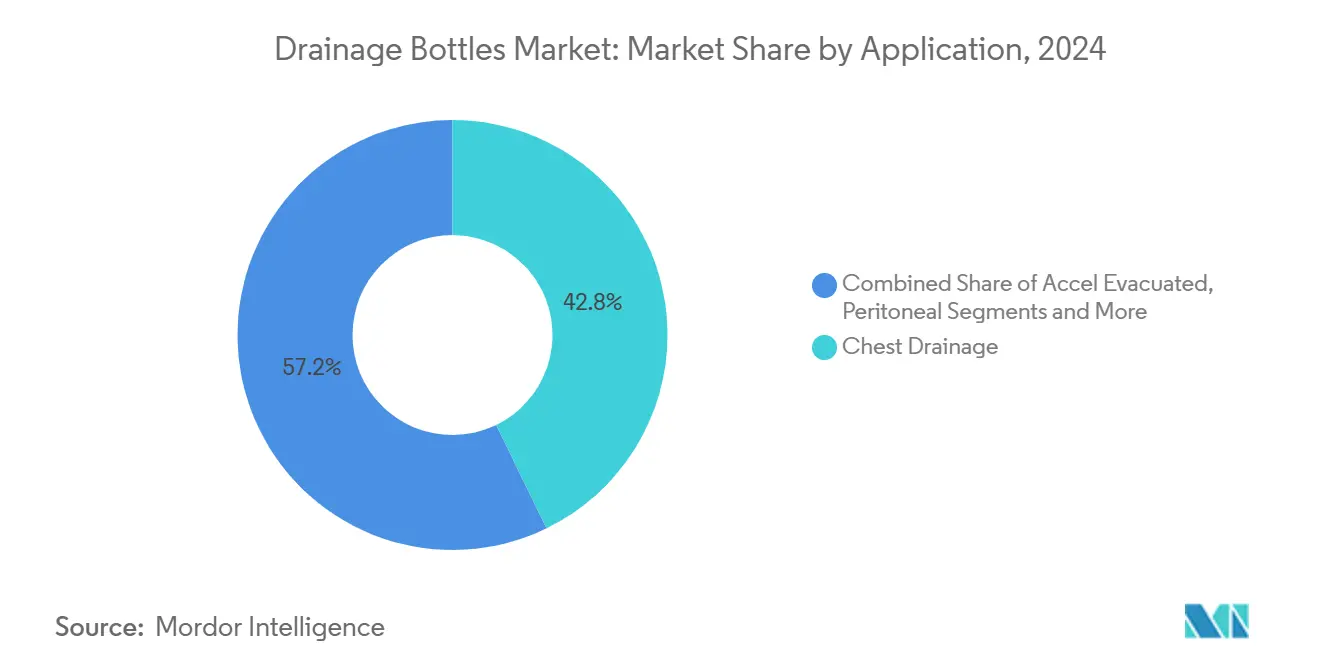

- By application, chest drainage accounted for 42.8% share in 2024 and wound drainage is progressing at a 9.2% CAGR through 2030.

- By end-user, hospitals held a 52.5% share in 2024, whereas home-care settings are forecast to expand at an 8.1% CAGR over the same horizon.

- By geography, North America captured a 34.6% share in 2024; Asia Pacific is poised for the quickest 7.6% CAGR to 2030.

Global Drainage Bottles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of Chronic & Oncological Surgeries | +1.80% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Expansion of Aged Population & Elective Procedures | +1.50% | Global, particularly developed markets | Long term (≥ 4 years) |

| Regulatory Push for Closed-System, Single-Use Devices | +1.20% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Integration with Digital Vacuum Monitoring | +0.90% | North America, Europe, select APAC markets | Medium term (2-4 years) |

| Veterinary Surgical Adoption in Emerging Nations | +0.80% | APAC core, spill-over to Latin America | Long term (≥ 4 years) |

| Shift Toward Ambulatory/Day-Care Surgery Settings | +0.60% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Chronic & Oncological Surgeries

Cancer and other chronic illnesses are driving higher surgical caseloads that frequently require meticulous fluid evacuation. Thoracic oncology procedures now rely on digital chest drainage to detect air leaks early, enabling faster tube removal and discharge.[1]S. Kumar et al., “Reduction of drainage-associated complications in cardiac surgery with a digital drainage system,” PubMed Central, pmc.ncbi.nlm.nih.gov Minimally invasive techniques, while reducing incision size, still necessitate precise drainage monitoring because internal visualization is limited. Hospitals are standardizing smart bottle systems that log hourly output and trigger alerts when thresholds are exceeded. This data-centric approach aligns with value-based reimbursement, which rewards shorter stays and lower complication rates. As chronic disease prevalence rises in aging societies, the drainage bottles market will benefit from sustained procedural demand.

Expansion of Aged Population & Elective Procedures

People aged ≥ 65 now account for a growing share of elective orthopedic, cardiac, and cosmetic surgeries. Older patients experience slower healing and higher exudate volumes, necessitating reliable drainage. Ambulatory centers—projected to conduct 44 million procedures by 2034—favor portable bottles that can transition home with minimal care-giver support. Remote-readout models that transmit data to clinicians reduce unnecessary readmissions and support reimbursement for chronic-care management. Consequently, suppliers integrating Bluetooth modules and cloud dashboards are gaining traction across developed markets.

Regulatory Push for Closed-System, Single-Use Devices

Post-pandemic infection-prevention protocols prioritize disposable, sealed drainage units that limit caregiver exposure and cross-contamination. Updated FDA guidance on quality systems underscores the role of single-use technology in curbing healthcare-associated infections. Cardiac and thoracic surgeons, sensitive to embolism risk, have become early adopters of molded, valve-equipped bottles that eliminate manual venting. Manufacturers are redesigning portfolios to phase out multi-patient systems while maintaining price parity, creating both compliance and differentiation advantages.

Integration with Digital Vacuum Monitoring

Pairing IoT sensors with vacuum regulators lets clinicians track pressure, volume, and fluid color in real time. Platforms such as Thopaz+ provide visual dashboards that assist in early bleeding detection after cardiothoracic surgery. Continuous data flow supports evidence-based protocols for tube removal, translating into shorter ICU stays. Hospitals adding 5G infrastructure in North America and Western Europe see digital drainage as a quick win for smart-ward initiatives. Suppliers able to interface their bottles with electronic medical record systems are winning procurement bids.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Infection Risks from Improper Handling | -0.80% | Global, particularly in resource-constrained settings | Short term (≤ 2 years) |

| Preference for Drainless or Negative-Pressure Dressings | -1.10% | Developed markets, expanding globally | Medium term (2-4 years) |

| Tightening Bans on PVC & Phthalates | -0.70% | North America & EU, with California leading | Short term (≤ 2 years) |

| Petrochemical Resin Price Volatility | -0.50% | Global, with higher impact in cost-sensitive markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Infection Risks from Improper Handling

Even the most advanced bottle can become a vector for pathogens if staff lack training in placement and removal. Observational studies link suboptimal drain positioning to pulmonary complications after cardiac bypass.[2]A. Kumar et al., “Impact of drains positioning on pulmonary function after CABG,” PubMed Central, pmc.ncbi.nlm.nih.govResource-limited hospitals often lack standardized protocols, leading to variable outcomes. Vendors are countering with color-coded connectors and tamper-evident seals to simplify workflows. Broader adoption of closed, single-use kits depends on affordable pricing for low-income regions and on-site education programs.

Preference for Drainless or Negative-Pressure Dressings

Surgeons in plastics, orthopedics, and general surgery are experimenting with drainless techniques and single-use negative-pressure dressings that obviate traditional bottles. NICE endorsement of the PICO system validated this approach for high-risk wounds. As enhanced-recovery protocols prioritize patient comfort and early mobilization, bottle suppliers must prove superior outcomes to retain share. Development of ultra-light, wearable drains and integration of antimicrobial liners are strategies to mitigate this restraint.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Capacity: Large-Volume Systems Drive Innovation

In 2024, 250-500 mL bottles retained a 40.2% share of the drainage bottles market, serving routine abdominal and orthopedic cases. The >1,000 mL category, while smaller, is forecast to post an 8.6% CAGR, reflecting demand in complex cardiothoracic surgeries where large fluid volumes and air evacuation are critical. Automated line-clearing systems tailored for these high-capacity bottles reduce clot formation and nursing labor.[3]Y. Huang et al., “Automated Line-Clearing Chest Tube System,” pmc.ncbi.nlm.nih.gov Hospitals seeking workflow efficiency are therefore upgrading to intelligent, large-volume kits. The 0-250 mL segment caters to pediatric and minimally invasive niches, whereas 500-1,000 mL bottles remain the workhorse for general surgery.

Digital functionality is moving fastest in the >1,000 mL class, where precise monitoring can prevent cardiac tamponade and expedite chest-tube removal. Cloud-connected models send automated alerts when drainage exceeds preset limits, enhancing post-op vigilance during staffing shortages. As procedure complexity rises, large-volume bottles embed RFID tags for inventory tracking, easing compliance with quality-system requirements. Collectively, these advancements anchor the drainage bottles market in value-added innovation rather than price competition.

By Material: Silicone Gains Ground Amid Safety Regulations

Polypropylene led the drainage bottles market size by value in 2024, but silicone-based devices are surging at a 7.2% CAGR as healthcare systems phase out DEHP and other phthalates. California’s statutory ban on DEHP in medical devices by 2030 is a clear catalyst for adopting silicone, TPE, and PVC-free blends. Silicone offers superior biocompatibility, temperature resilience, and transparency, attributes prized in neonatal and immunocompromised care. Suppliers are scaling peroxide-cured formulations that resist yellowing during sterilization, reinforcing product durability.

Price remains silicone’s chief hurdle, sustaining polypropylene’s foothold in cost-sensitive hospitals. Developers are narrowing the gap through lean manufacturing and by bundling silicone bottles with digital sensors that justify premium pricing via outcome improvements. Polyethylene and advanced PVC-free blends occupy a middle ground, offering incremental safety gains at marginal cost increases. As regulators worldwide harmonize material-safety frameworks, the drainage bottles market is expected to gravitate further toward silicone and other high-purity polymers.

By Application: Wound Drainage Accelerates Growth

Chest procedures still represented 42.8% of the drainage bottles market share in 2024 because thoracic and cardiac surgeries mandate stringent air-leak management. Yet wound drainage is the fastest-rising application at a 9.2% CAGR to 2030, propelled by minimally invasive orthopedic and plastic surgeries that require localized exudate control. Advanced wound bottles now feature graduated compression and antimicrobial impregnation, lowering infection risk in compromised tissues. Surgeons prioritize transparent chambers that allow quick visual checks without disconnecting the system.

Smart wound drains equipped with pressure sensors provide real-time feedback that can flag hematoma formation earlier than manual observation. Researchers are already trialing electronic sutures with inflammation detectors that might eventually replace traditional drainage. Until such platforms mature, hybrid solutions combining suction bottles with wireless monitoring are expected to dominate. Peritoneal, urostomy, and specialty trauma applications remain smaller niches but present upside for custom-volume bottles and infection-prevention coatings.

By End-User: Home-Care Transformation Accelerates

Hospitals remained the largest buyers with 52.5% of 2024 revenue, but reimbursement reforms are pushing complex wound and chest-tube management into outpatient and home-care settings. The drainage bottles market expects home-based use to rise at an 8.1% CAGR, aided by Medicare provisions that reimburse disposable negative-pressure devices starting 2025. Portable, lightweight bottles with quick-connect tubing and digital readouts allow caregivers to track output without specialist intervention. Ambulatory surgical centers adopt similar systems to support rapid discharge protocols.

Veterinary clinics represent an emerging micro-segment as pet owners demand advanced surgical after-care. Bottle makers are customizing smaller-volume, flexible chambers that conform to animal anatomy. Across human healthcare, success hinges on user-friendly designs with clear labeling and instructional media, minimizing misuse outside the acute-care setting. Partnerships with tele-health providers that integrate drainage data into remote monitoring dashboards will further entrench suppliers in home-care workflows.

Geography Analysis

North America led the drainage bottles market with 34.6% share in 2024 on the back of robust surgical volumes and early adoption of smart, closed-system technology. U.S. hospitals benefit from Medicare coverage of advanced wound care and negative-pressure therapy, bolstering premium unit sales. FDA initiatives that emphasize single-use safety strengthen demand for polypropylene-free devices, while 5G-enabled data platforms accelerate hospital IoT rollouts. Canada and Mexico provide incremental growth through surgical infrastructure expansion, though average selling prices remain lower than in the United States.

Asia Pacific is the fastest-growing region, poised for a 7.6% CAGR through 2030. China’s capital investment in private hospitals and high-end surgical equipment is reshaping regional procurement. Japan’s rapidly aging population is driving use of large-volume chest drains in cardiac and orthopedic surgery, while India’s expanding middle class fuels both budget and mid-tier bottle demand. Medical tourism hubs such as Thailand and Singapore invest in smart drainage to attract overseas patients seeking top-quality care. Device registration processes are becoming more stringent across ASEAN, nudging suppliers toward material-safe, digitally capable platforms.

Europe remains a mature yet opportunity-rich arena where regulatory rigor shapes buying decisions. The EU’s phased DEHP restrictions sustain momentum toward silicone bottles, though implementation delays to 2030 give manufacturers transition leeway. Germany, France, and the Nordics spearhead adoption of digital vacuum monitoring, reflecting well-funded hospital IT strategies. In the Middle East, oil-funded infrastructure projects are expanding tertiary care capacity and attracting premium device vendors. Africa’s growth stays modest but steady, with non-government organizations often procuring simplified drains for trauma care. South America, led by Brazil, is upgrading surgical suites despite currency volatility, focusing on cost-effective polypropylene bottles while gradually testing smart systems in flagship hospitals.

Competitive Landscape

The drainage bottles market is moderately fragmented, with innovators harnessing digitalization to outpace commodity rivals. Teleflex, Medtronic, and Cardinal Health deploy IoT-enabled bottles that integrate seamlessly into electronic medical records, reducing manual charting and positioning products as workflow solutions rather than consumables. Medline’s USD 950 million acquisition of Ecolab’s surgical business added high-margin infection-prevention lines that complement its drainage portfolio. Smith+Nephew’s 2024 revenue performance showed that products launched within five years—many in negative-pressure wound therapy—drove 60% of growth.

Start-ups are carving niches with disruptive smart-drain technology. SOMAVAC’s SVS wearable device earned FDA clearance and leverages machine-learning algorithms to predict seroma formation, targeting outpatient breast surgery. Material suppliers such as Teknor Apex and ConvaTec are vying to supply DEHP-free resins and antimicrobial linings, respectively, strengthening vertical partnerships with device OEMs. Competitive emphasis is shifting from unit pricing toward bundled service models that include data analytics, demand-positioning training, and infection-control certification.

Regulatory compliance represents both a barrier and a lever. Firms with in-house toxicology labs accelerate silicone migration, satisfying California’s 2030 DEHP prohibition ahead of lagging competitors. Meanwhile, procurement teams increasingly demand post-market surveillance data demonstrating reduced infection incidence, favoring players with robust clinical-evidence pipelines. As a result, the drainage bottles market rewards balanced portfolios that blend proven mechanical designs with cutting-edge digital augmentation.

Drainage Bottles Industry Leaders

Teleflex Incorporated

Medtronic plc

Cardinal Health Inc.

Becton Dickinson & Co.

Smith & Nephew plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: B. Braun issued guidance for removing DEHP-laden devices from hospitals, aiding the transition to safer materials.

- August 2024: Medline completed the acquisition of Ecolab’s surgical solutions business for USD 950 million, reinforcing its drainage and infection-prevention portfolio.

- August 2024: Sungkyunkwan University-developed electronic suture technology is now being combined with drainage systems to create smarter wound care solutions. These high-tech bandages can monitor inflammation and healing in real time, sending data to connected drainage bottles that automatically adjust suction pressure based on the wound's progress.

Global Drainage Bottles Market Report Scope

| 0-250 mL |

| 250-500 mL |

| 500-1 000 mL |

| >1 000 mL |

| Polypropylene (PP) |

| Polyethylene (PE) |

| Polyvinyl Chloride (PVC-free) |

| Silicone/Elastomers |

| Chest Drainage |

| Accel Evacuated |

| Peritoneal Drainage |

| Urostomy/Urinary |

| Wound Drainage |

| Others |

| Hospitals |

| Ambulatory Surgical Centers |

| Home-Care / Post-Acute Settings |

| Veterinary Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Capacity | 0-250 mL | |

| 250-500 mL | ||

| 500-1 000 mL | ||

| >1 000 mL | ||

| By Material | Polypropylene (PP) | |

| Polyethylene (PE) | ||

| Polyvinyl Chloride (PVC-free) | ||

| Silicone/Elastomers | ||

| By Application | Chest Drainage | |

| Accel Evacuated | ||

| Peritoneal Drainage | ||

| Urostomy/Urinary | ||

| Wound Drainage | ||

| Others | ||

| By End-User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Home-Care / Post-Acute Settings | ||

| Veterinary Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the drainage bottles market?

The drainage bottles market size is USD 637.8 million in 2025.

How fast is the market expected to grow?

It is projected to expand at a 6.6% CAGR to reach USD 803.7 million by 2030.

Which capacity segment is growing the quickest?

>1,000 mL drainage bottles are posting the fastest 8.6% CAGR through 2030.

Why are silicone drainage bottles gaining popularity?

Silicone is phthalate-free, highly biocompatible, and aligns with emerging DEHP bans, driving a 7.2% CAGR for this material.

Which region shows the highest growth potential?

Asia Pacific leads in growth with a forecast 7.6% CAGR owing to rising surgical volumes and healthcare investment.

How is digital technology influencing market demand?

IoT-enabled drainage bottles that provide real-time pressure and volume data are shortening hospital stays and supporting decentralized care, making them a key driver of adoption.

Page last updated on: