Digital Education Publishing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

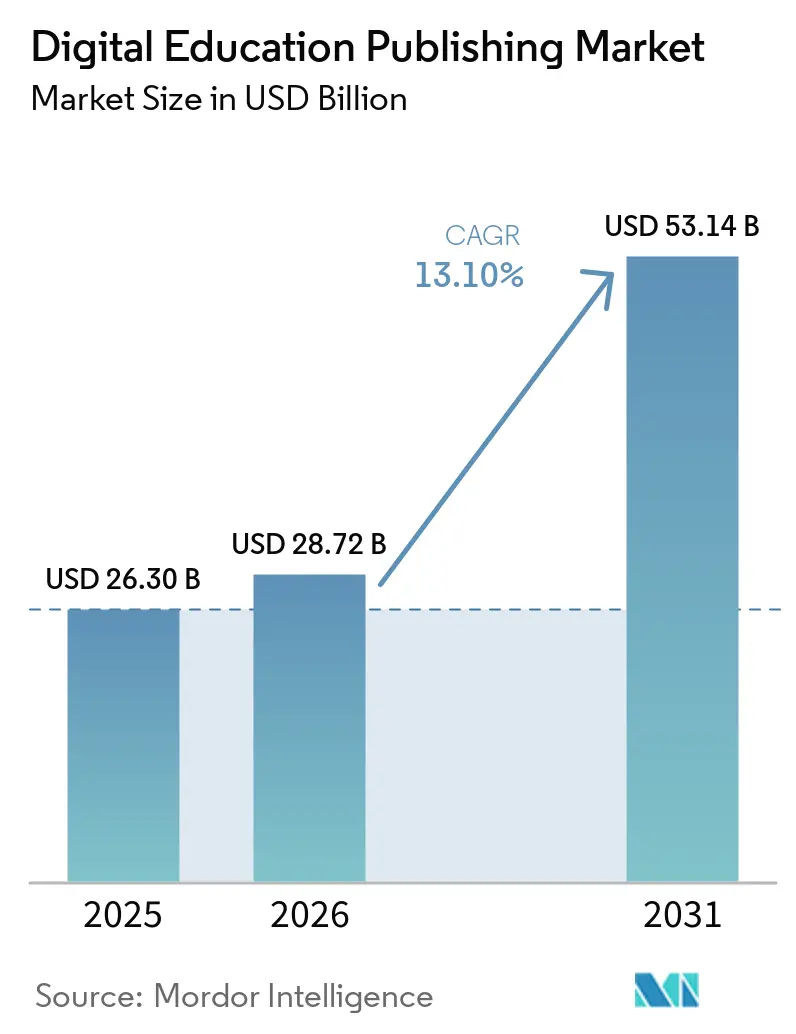

| Market Size (2026) | USD 28.72 Billion |

| Market Size (2031) | USD 53.14 Billion |

| Growth Rate (2026 - 2031) | 13.10% CAGR |

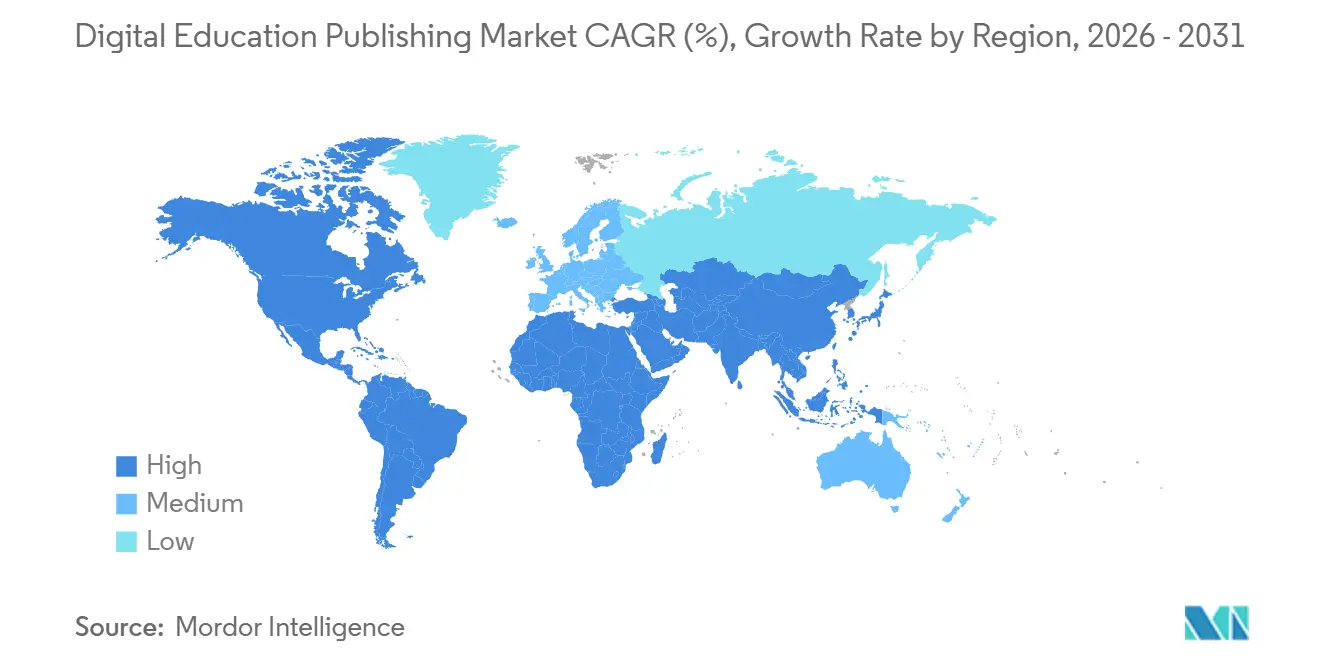

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Digital Education Publishing Market Analysis by Mordor Intelligence

The Digital Education Publishing Market size was valued at USD 26.30 billion in 2025 and is estimated to grow from USD 28.72 billion in 2026 to reach USD 53.14 billion by 2031, at a CAGR of 13.10% during the forecast period (2026-2031).

The expansion reflects a pivot to platform-native models where value accrues from integrated learning experiences that blend adaptive assessment, AI tutoring, and LMS-embedded subscriptions into persistent ecosystems. Procurement is shifting toward multi-year institutional licenses that anchor renewals to interoperability, accessibility, and data safeguards, thereby increasing switching costs and rewarding vendors that meet LTI 1.3, WCAG 2.2, and Section 508 requirements. Government-backed national platforms add momentum by formalizing digital delivery, as seen with India’s DIKSHA and PM e-VIDYA initiatives, and China’s “AI + Education” action plan, which guides content standards and deployment timelines across public systems. The digital education publishing market benefits when ministries tie budgets to broadband-to-school infrastructure and smart learning platforms that normalize digital-first content in everyday instruction. At the same time, OER repositories and regional procurement rules sustain fragmentation, which encourages publishers to differentiate on interoperability, accessibility, and language support aligned with public targets for digital skills and classroom inclusivity.

Key Report Takeaways

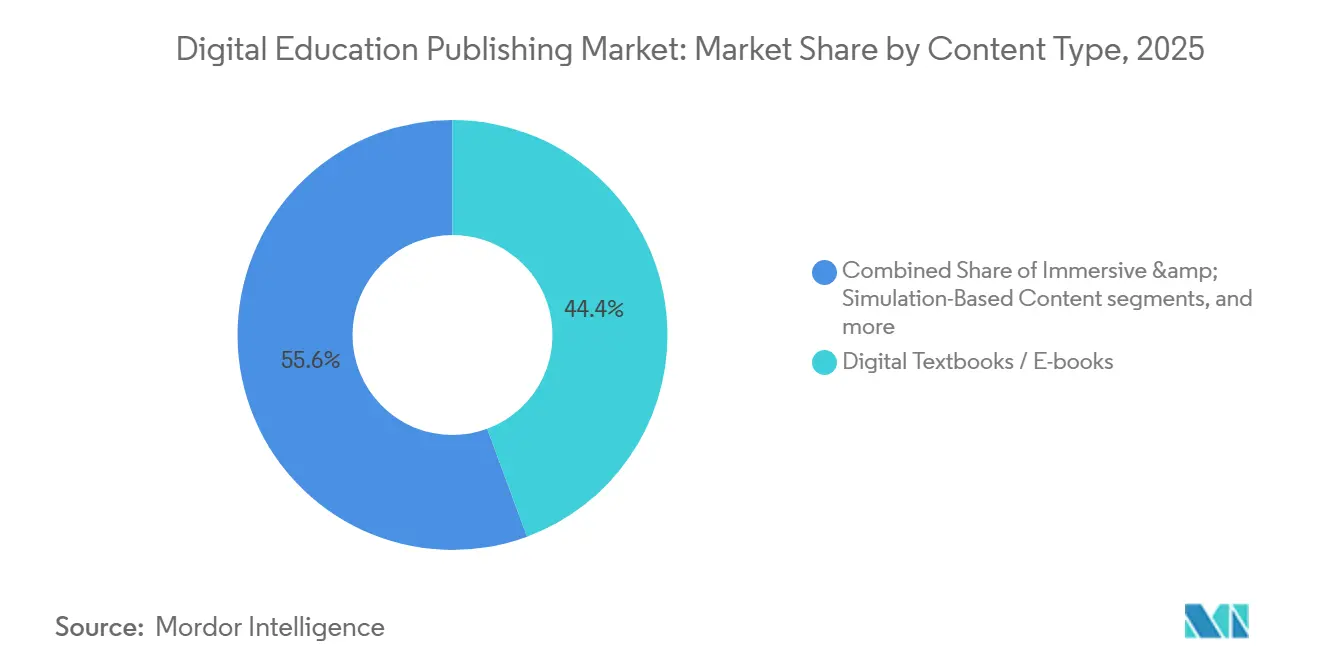

- By content type, digital textbooks held 44.36% of the digital education publishing market share in 2025, while immersive & simulation-based content is projected to expand at a 21.87% CAGR through 2031.

- By end user, K-12 and higher education institutions collectively accounted for 37.75% share in 2025, while corporate & professional learners are set to grow at a 19.39% CAGR through 2031.

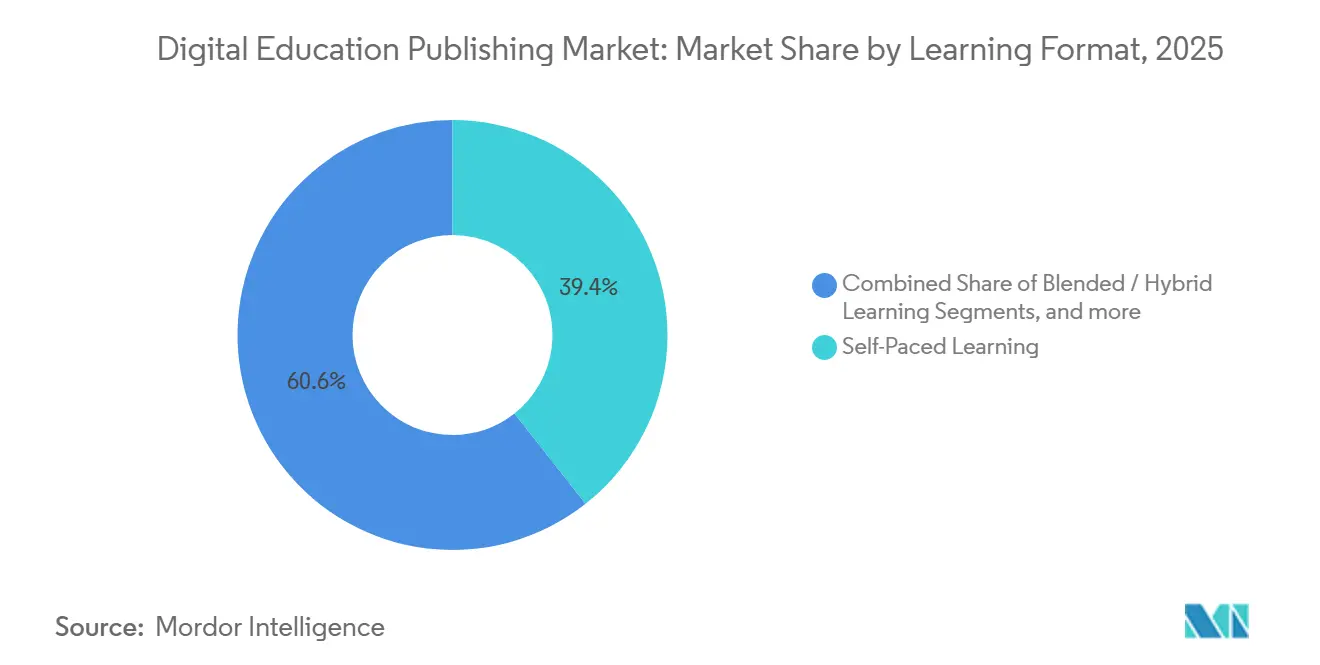

- By learning format, self-paced learning captured 39.38% share in 2025, while blended/hybrid learning is forecast at an 11.38% CAGR through 2031.

- By delivery channel, web-based platforms & portals accounted for 42.38% of the market in 2025, while mobile learning applications are projected to expand at a 15.49% CAGR through 2031.

- By geography, North America held 31.74% share in 2025, while Asia-Pacific is expected to post a 15.99% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Digital Education Publishing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Institutionalized hybrid learning procurement cycles | +2.8% | Global, spill-over strongest in North America & Western Europe | Medium term (2-4 years) |

| Curriculum-aligned digital assessment mandates | +2.1% | North America core, expanding to APAC (India, China national frameworks) | Long term (≥ 4 years) |

| LMS-native content bundles scaling adoption | +1.9% | Global, with North America & APAC leading penetration | Medium term (2-4 years) |

| Mobile-first access expands consumption | +1.7% | APAC, MEA, Latin America, rural and underserved geographies | Short term (≤ 2 years) |

| Interoperability certifications increasingly drive purchasing | +1.3% | North America, Europe with LTI 1.3, SCORM, xAPI compliance requirements | Long term (≥ 4 years) |

| GenAI item banks speed test-prep | +1.6% | Global, early gains in North America and APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Institutionalized Hybrid Learning Procurement Cycles Lock Multi-Year Revenue Streams

District- and system-level hybrid learning mandates channel spending into three-to-five-year licenses, turning one-off transactions into renewals anchored to LMS integration, content accessibility, and vendor certification trajectories. Where textbook adoption is centralized across 19 U.S. states plus Washington, D.C., formal RFPs elevate LTI 1.3, WCAG 2.2, and Section 508 compliance from nice-to-have attributes to eligibility gates for state-level approvals, stabilizing the digital education publishing market by rewarding compliant vendors during multi-year adoption cycles [1]Kitaboo, “K12 Digital Textbooks State Adoption,” kitaboo.com . Government platforms place greater weight on digital-first content, as illustrated by India’s PM e-VIDYA and DIKSHA, which support national-scale distribution; when ministries standardize repositories and content metadata, publishers adapt product roadmaps to align with public workflows and multilingual needs. China’s “AI + Education” action plan spans primary through higher education, with a 2030 horizon for full AI course integration, reinforcing demand for digital courseware and localized AI-aligned content that can connect to provincial platforms. In Europe, the Digital Education Action Plan frames interoperability and teacher capacity-building, pushing content providers toward standards participation and accessible-by-design production processes to remain relevant in cross-border programs, which sustains renewal potential across the digital education publishing market. As procurement focuses on durable integrations rather than discrete titles, the digital education publishing market faces higher switching costs, favoring vendors entrenched in district workflows and data systems.

Curriculum-Aligned Digital Assessment Mandates Restructure Content Development Economics

Mandated formative assessment and progress monitoring shift publishers from content shipments to ongoing diagnostic and analytics partners that feed lesson planning and intervention at the classroom scale. The framework effect is clearest where ministries outline explicit digital skills targets, as seen in the EU’s policy track to raise computer and information literacy while directing investment into interoperable platforms that can host and share assessment outcomes across schools, thereby reshaping demand in the digital education publishing market [2]European Commission, “Digital Education Action Plan 2021–2027,” European Commission, education.ec.europa.eu . China’s “AI + Education” direction produces content localization and AI-supported assessment needs across languages and scripts, with provincial smart platforms serving large installed bases that can use embedded diagnostics to close learning gaps. Human-in-the-loop workflows remain essential even as AI accelerates item creation, as evidenced by peer-reviewed research on AI-assisted test generation that documents scalability alongside the persistent need for expert review to ensure quality and fairness. The net effect is that content, assessment, and analytics converge into continuous services tied to institutional licenses rather than discrete textbook cycles, which reinforces recurring revenue for the digital education publishing market.

LMS-Native Content Bundles Compress Publisher Margins Through Platform Revenue Shares

Institutions favor LMS-integrated content and inclusive-access models that simplify provisioning and ensure day-one availability, thereby increasing reliance on platform connectors and catalog placement. As digital enrolment grows and course access integrates through campus systems, publishers lean on product differentiation, such as adaptive engines and analytics, rather than static content alone, which aligns the digital education publishing market to bundled licenses and long-term institutional deals. Data privacy frameworks in the EU and public-sector expectations for secure data processing drive anonymization and data-minimization practices that can limit event-level insights in some deployments, requiring content providers to fine-tune analytics without breaching policy constraints. At the same time, national MOOC platforms such as SWAYAM exert downward pricing pressure on undifferentiated content, so publishers emphasize proprietary adaptivity, assessment validity, and support services to justify enterprise pricing in the digital education publishing market. These dynamics pull revenue into subscription bundles and institutional data partnerships rather than into transactional print equivalents, reshaping product roadmaps across the digital education publishing market.

Mobile-First Access Expands Addressable Markets in Connectivity-Constrained Geographies

Smartphone-first usage is the default in many emerging markets, so app performance on 3G and 4G networks, offline caching, and data-light delivery become gating features. Affordability constraints persist in several regions where mobile broadband as a share of GNI per capita sits above the UN Broadband Commission target, which influences pricing models for course access and micro-credentials that feed the digital education publishing market [3]International Telecommunication Union, “The State of Broadband: Our Digital World,” itu.int . The ASEAN region shows wide variance in access and speeds, requiring publishers to maintain parallel, offline-capable SKUs for lower-bandwidth markets and cloud-synchronized experiences in markets with mature infrastructure. National policy shifts on device usage and screen time in schools affect assumptions about persistent mobile engagement patterns. They can recalibrate publisher investment in native apps versus desktop parity within the digital education publishing market. Over time, hybrid connectivity programs and school network upgrades bring new cohorts online, expanding the reach of digital-first content and supporting the broader growth of the digital education publishing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Piracy and weak DRM leakage | -1.4% | Global, acute in APAC, MEA, Latin America | Short term (≤ 2 years) |

| Uneven broadband and device access | -2.3% | MEA, rural APAC, Latin America, select North America rural zones | Medium term (2-4 years) |

| LMS revenue share compresses margins | -0.9% | North America, Europe, APAC higher education | Long term (≥ 4 years) |

| Accessibility retrofits inflate production costs | -0.7% | North America, Europe with WCAG 2.2 and Section 508 mandates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Piracy and Weak DRM Erode Revenue Capture in Emerging Markets

Low-connectivity environments influence delivery choices and can raise exposure to unauthorized redistribution when materials need to be accessible offline for extended periods. In markets where mobile and fixed broadband affordability exceeds benchmark targets, user reliance on cached or sideloaded content increases the risk surface for leakage, complicating ROI on premium titles in the digital education publishing market. Regions with school networks still in early deployment phases often lack persistent identity and license checks, which reduces the effectiveness of cloud-based DRM verification workflows and forces content providers to consider alternative controls suited to intermittent connectivity. When national platforms set open-access defaults for baseline materials, publishers respond by segmenting premium features such as adaptivity and analytics to defend value, which shapes product strategy across the digital education publishing market. This environment sustains a continuous need for packaging models and distribution safeguards aligned with local connectivity profiles and school device policies, which can change the calculus of DRM architectures.

Uneven Broadband and Device Access Fragments Addressable TAM

A large share of the global population remains offline, and many school sites still lack robust connectivity, which limits demand for cloud-only courseware and suppresses utilization of advanced multimedia. National budgets are now channeling funds into labs and broadband-to-school buildouts, including India’s recent education allocations that push digital resources and teacher support into government schools through multi-year execution windows, which will expand reach for the digital education publishing market as deployments progress. In Europe, Digitalpakt 2.0 financing targets WLAN expansion and device procurement from 2026 to 2030, supporting school-level readiness for digital content at scale once local co-funding is secured and implementation ramps up. These public programs gradually lift constraints on synchronous features and rich media that depend on reliable bandwidth, and they drive requirements for standards alignment and accessibility in procurement criteria across the digital education publishing market. As device ratios improve and network upgrades reach rural and underserved areas, addressable demand for adaptive, analytics-rich content that benefits both instruction and assessment grows.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Content Type: Digital Textbooks Anchor Revenue While Immersive Formats Redefine Engagement Models

Digital Textbooks commanded 44.36% of the digital education publishing market share in 2025, reflecting the persistence of state adoption cycles and the embedded role of core curricula in formal procurement. Immersive and simulation-based formats are projected to grow fastest at a 21.87% CAGR through 2031 as institutions and employers seek experiential learning that mimics clinical, engineering, and safety-critical environments, broadening the scope of the digital education publishing market. Europe’s investment in national digital platforms and school networks supports multimedia-first pedagogy. It raises the bar for content packaging and accessibility that textbooks alone cannot meet, thereby influencing publishers' portfolio balance between static and interactive assets. The digital education publishing industry is also prioritizing analytics-ready assets that can align with policy objectives such as skill tracking and inclusive access, putting adaptive and assessment-ready content at the center of renewal strategies in formal education. Where national repositories provide baseline materials, publishers focus on premium layers like adaptive feedback, progress dashboards, and secure proctoring to create a moat beyond open content and retain institutional contracts across the digital education publishing market.

Interactive Courseware and Assessment Materials continue to gain adoption as AI-assisted authoring compresses development timelines. At the same time, human validation maintains psychometric quality, as documented in peer-reviewed research on AI-generated test items with expert oversight. Multimedia Content adoption rises where broadband and device availability enable richer formats, with data integration partnerships that connect assessments and curricula to personalize sequencing in classrooms and districts. The digital education publishing market for immersive and simulation content is projected to expand at a 21.87% CAGR through 2031, as institutions procure scenario-based learning that can be measured through embedded tasks and analytics. Reference and supplemental content see more OER competition, which pushes differentiation toward adaptivity, accessibility, and evidence of learning impact that meets public-sector expectations. Together, these shifts move portfolios from static PDFs toward dynamic modules with assessment hooks that align with emerging standards and policy goals across the digital education publishing market.

By End User: Corporate Learners Outpace Academic Segments as Credentialing Displaces Degrees

K-12 and Higher Education Institutions collectively held 37.75% share in 2025, while Corporate and Professional Learners are set to grow at a 19.39% CAGR through 2031 as organizations fund targeted upskilling and verifiable credentials that can be tracked across HR systems. Enterprise demand focuses on skill diagnostics, continuous assessment, and role-based content paths that drive workforce productivity, steering a larger share of the digital education publishing market toward subscription delivery and analytics integrations. University-linked platforms and publishers are forming technology partnerships to bring AI-supported search, content discovery, and verification into institutional workflows, which sustains premium pricing for authenticated usage and citation inside the digital education publishing market. The digital education publishing industry also benefits when institutional buyers require accessible-by-design components that integrate into LMS catalogs in line with data protection rules, which encourages investment in platform reliability and customer support aligned with public expectations. Over time, outcome-linked content and credential networks become competitive moats as employers equate verified competencies with job readiness, which elevates the value of embedded assessment across the digital education publishing market.

Technical and vocational training providers benefit from national goals that expand access to labs, connectivity, and teacher development, thereby increasing the adoption of modular, stackable content aligned with local employment paths in the digital education publishing market. Corporate programs seek content that integrates with internal systems and supports role-based analytics without breaching regional data expectations, aligning with evolving standards agendas across the EU and other regions. Meanwhile, the K-12 and higher education segments continue to prioritize aligned assessments, teacher guidance, and compliance with accessibility mandates, which help stabilize renewals even as budgets fluctuate at the district and campus levels. These patterns point to a durable demand base for analytics-rich content that verifies skill gains and supports compliance across diverse user types inside the digital education publishing market.

By Learning Format: Blended Models, Institutionalize Hybrid Infrastructure Spend

Self-Paced Learning captured 39.38% of the market share in 2025 due to the mainstream acceptance of asynchronous modules and adaptive platforms that accommodate varied schedules and bandwidth profiles. Blended and Hybrid Learning is projected to grow at a 11.38% CAGR through 2031 as institutions embed LMS provisioning and device programs into long-term budgets, which channels sustained demand into the digital education publishing market. National MOOC and e-learning initiatives reinforce self-paced modalities at scale, including programs that offer course discovery, enrolment tracking, and certification through public platforms that complement formal curricula. The digital education publishing market for blended formats is expected to expand at a 11.38% CAGR through 2031, as connectivity upgrades and classroom devices enable real-time progress checks and analytics-supported lesson sequencing. In Europe, strategic funding for school networks and teacher development raises the baseline capabilities for hybrid delivery and accessible-by-design content, sustaining investment in workflow integrations that raise renewal rates across the digital education publishing market.

Synchronous Virtual Classrooms and instructor-led modes persist in high-stakes credentialing and regulated fields where live interaction and identity assurance are central to outcomes. Changes in school device policies and screen-time guidance can temper assumptions about continuous live engagement on mobile, leading publishers to maintain desktop parity and flexible delivery that suits policy environments in the digital education publishing market. Partnerships that connect assessment data with curricula help personalize pacing inside blended classrooms, and these integrations support timely intervention without requiring fully synchronous instruction for every learner. Collectively, these delivery modes reflect institutional demand for flexible combinations of asynchronous content, periodic synchronous touchpoints, and analytics-based supports that can run on school networks and meet public accessibility standards across the digital education publishing market.

By Delivery Channel: Mobile Apps Surge as Connectivity Gaps Close, Yet LMS Platforms Retain Institutional Lock-In

Web-Based Platforms and Portals held 42.38% share in 2025, since institutions favor browser-based deployment that reduces device management overhead, supports accessibility tooling, and standardizes authentication flows. Mobile Learning Applications are forecast at a 15.49% CAGR through 2031 as smartphone access deepens, especially in markets where laptops are less common and mobile bandwidth drives usage patterns in the digital education publishing market. App designs that work well on 3G and 4G, minimize data usage, and cache content for offline use increase adoption in bandwidth-constrained areas, which improves reach for the digital education publishing market. LMS channels remain central for institutions due to roster syncing, grading, analytics integration, and procurement workflows that prefer single sign-on and catalog curation, which continues to shape long-term relationships across the digital education publishing market.

New channels such as AI chat-based tutoring tools and voice interfaces are emerging, with early institutional pilots integrating question banks and class links to reduce teacher workload and streamline assignment workflows. AI models that adapt textbook materials by grade level and interest profiles also show learning gains in controlled experiments, signaling future demand for more adaptive delivery surfaces in the digital education publishing market. Data-localization trends encourage regional hosting strategies for recordings and analytics to meet public expectations and procurement criteria, which in turn influence cloud architectures and operating costs that publishers factor into their multiregional delivery plans. These delivery pathways demonstrate how app performance, privacy safeguards, and integration depth now drive channel selection for institutions and shape how content is packaged across the digital education publishing market.

Geography Analysis

North America secured 31.74% share in 2025, supported by well-funded K-12 districts and campus programs that favor inclusive-access licenses tied to LMS provisioning and analytics. Centralized textbook adoption across 19 states of the United States and Washington, D.C. underscores the importance of LTI 1.3, WCAG 2.2, and Section 508 compliance, which guide product design and bidding eligibility across the digital education publishing market. Institutions also maintain a preference for browser-based access that aligns with accessibility tooling and identity management, which sustains web-first portfolios. At the same time, mobile apps fill specific use cases and underserved contexts. The region’s shift toward diagnostic and analytics-infused curricula strengthens recurring revenue models for vendors that can evidence learning impact and policy alignment across the digital education publishing market. Over time, these features add to switching costs and favor vendors with proven integrations and compatibility with district data flows that span instruction and assessment.

Asia-Pacific is the fastest-growing region with a projected 15.99% CAGR to 2031, supported by large-scale public investments in connectivity, devices, and smart education platforms. India’s recent budgetary allocations continue to support digital resources and infrastructure for schools, thereby increasing platform usage and teacher adoption in government systems aligned with national initiatives like PM e-VIDYA and DIKSHA, which boost discovery and distribution at scale across the digital education publishing market. China’s “AI + Education” action plan sets expectations for AI course coverage through 2030 and leverages provincial platforms that support massive enrollments, accelerating the development of localized content and assessment features in the digital education publishing market. ASEAN markets show wide variation in internet access and speeds, which pushes publishers to tailor SKUs to bandwidth realities while preparing for growth as national programs advance digital-economy ambitions. As national clouds and data-residency rules evolve, vendors adopt region-specific hosting and privacy practices that enable public procurement and long-term institution partnerships in the digital education publishing market.

Europe posts steady gains as EU-level programs set direction for interoperable solutions and skills outcomes while member states manage procurement and co-funding. The Digital Education Action Plan 2021-2027 prioritizes teacher capacity, platform interoperability, and measurable progress in student digital skills, thereby shaping vendor priorities in accessibility, standards, and analytics across the digital education publishing market. Germany’s Digitalpakt 2.0 allocates funding from 2026 through 2030 for WLAN, devices, and training, which will expand capacity for rich media and hybrid instruction at scale once local match funding is arranged. EU data protection expectations guide hosting and analytics models that support institutional use without compromising privacy, which further aligns content packaging and assessment design with public-sector requirements in the digital education publishing market. Select markets in the Middle East and Africa and in Latin America continue to expand connectivity and school networks under national digital masterplans, which will progressively widen the addressable user base for digital-first content delivery at school and in the workplace.

Competitive Landscape

The digital education publishing market remains fragmented as regional procurement regimes, OER availability, and national platforms prevent any single provider from consolidating dominance. Public platforms such as DIKSHA demonstrate how governments can deliver large-scale content distribution and teacher support, which compels publishers to differentiate through adaptivity, analytics, and services that complement open repositories. Standards initiatives and EU policy frameworks continue to raise expectations for accessibility and interoperability, which reward vendors that shape specifications and deliver compliance proofs in procurement bids across the digital education publishing market. Data partnerships that link assessment and curriculum at the classroom scale have become strategic, as shown by collaborations that integrate benchmark assessments with core programs to personalize student pathways.

Strategic moves span AI enablement, platform partnerships, and content discoverability. University and publisher collaborations are embedding generative AI search and authenticated access into campus workflows, streamlining discovery and citation, and helping institutions manage knowledge assets more effectively in the digital education publishing market. Technology partnerships focused on cloud modernization and AI-enabled platforms indicate a push to scale infrastructure and accelerate feature delivery for institutional clients. Publishers and edtech firms are also piloting AI assistants that generate standards-aligned content and simplify assignment creation via direct class links, reducing instructor workload and supporting adoption across the digital education publishing market. At the same time, experiments in adaptive content generation show measurable gains in recall, signaling long-term advantages for AI-personalized pathways and multimodal study aids.

M&A and product innovation focus on AI-native feedback, data integrations, and accessibility-by-design production. Acquisitions and incubation programs that build writing assessment and feedback tools reflect a broader shift from static content toward workload-saving teacher assistants, aligning commercial models with institutional interest in measurable outcomes across the digital education publishing market. As public funders push for learning impact and digital skills, vendors invest in integrations that surface real-time progress and adapt materials to student needs while preserving privacy safeguards required for large-scale use. These strategic directions suggest continued fragmentation, with performance advantages accruing to providers that combine compliance, adaptivity, and analytics at an institutional scale across the digital education publishing market.

Digital Education Publishing Industry Leaders

Pearson

McGraw Hill

Houghton Mifflin Harcourt

Scholastic

Cengage Learning

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: McGraw-Hill and Renaissance launched a nationwide data integration partnership for back-to-school 2026, connecting Renaissance Star Assessment data with McGraw-Hill's math and literacy curricula to enable real-time student progress tracking and personalized learning pathways within Renaissance Intelligence℠.

- February 2026: Virtusa Corporation and Wiley formed a multi-year managed services partnership whereby Virtusa assumed ownership of Wiley's Sri Lanka technology operation to accelerate Wiley's technology transformation, infrastructure modernization, and AI-powered platform development.

- October 2024: McGraw-Hill's Evergreen model started offering perpetual digital updates, replacing the traditional fixed edition cycles. It ensures that users have access to the most current and relevant content without waiting for periodic updates, enhancing the overall learning experience.

- September 2025: Google launched Learn Your Way, a research experiment powered by LearnLM and Gemini 2.5 Pro, which adapts textbook materials based on student grade level and interests, generating mind maps, audio lessons, and interactive quizzes; efficacy studies showed students scored 11 percentage points higher on long-term recall tests.

- August 2025: Wiley and Perplexity announced a partnership, making Wiley the first education partner for Perplexity's generative AI search platform, enabling Perplexity Enterprise Pro users at institutions like Texas A&M and Texas State University to access Wiley's educational collections with proper attribution and citation.

Global Digital Education Publishing Market Report Scope

| Digital Textbooks |

| Interactive Courseware |

| Assessment & Test-Prep Materials |

| Reference & Supplemental Materials |

| Multimedia Content |

| Immersive & Simulation-Based Content |

| K-12 Educational Institutions |

| Higher Education Institutions |

| Corporate & Professional Learners |

| Technical & Vocational Training Providers |

| Independent Learners |

| Self-Paced Learning |

| Instructor-Led Learning |

| Blended / Hybrid Learning |

| Synchronous Virtual Classrooms |

| Web-Based Platforms & Portals |

| Mobile Learning Applications |

| Learning Management Systems (LMS) |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| Benelux (Belgium, Netherlands, and Luxembourg) | |

| Nordics (Sweden, Norway, Denmark, Finland, and Iceland) | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Content Type | Digital Textbooks | |

| Interactive Courseware | ||

| Assessment & Test-Prep Materials | ||

| Reference & Supplemental Materials | ||

| Multimedia Content | ||

| Immersive & Simulation-Based Content | ||

| By End User | K-12 Educational Institutions | |

| Higher Education Institutions | ||

| Corporate & Professional Learners | ||

| Technical & Vocational Training Providers | ||

| Independent Learners | ||

| By Learning Format | Self-Paced Learning | |

| Instructor-Led Learning | ||

| Blended / Hybrid Learning | ||

| Synchronous Virtual Classrooms | ||

| By Delivery Channel | Web-Based Platforms & Portals | |

| Mobile Learning Applications | ||

| Learning Management Systems (LMS) | ||

| Others | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Benelux (Belgium, Netherlands, and Luxembourg) | ||

| Nordics (Sweden, Norway, Denmark, Finland, and Iceland) | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the size of the digital education publishing market today, and where is it headed by 2031?

The digital education publishing market size is USD 28.72 billion in 2026 and is expected to reach USD 53.14 billion by 2031 at a 13.10% CAGR.

Which segment is growing fastest within the digital education publishing market?

Immersive and simulation-based content is the fastest-growing content type with a 21.87% CAGR to 2031, supported by experiential learning needs in academic and workforce settings.

Which region leads, and which region grows fastest in the digital education publishing market?

North America leads with 31.74% share in 2025, while Asia-Pacific is the fastest-growing region at a projected 15.99% CAGR through 2031.

How are policy and standards shaping the digital education publishing market?

Procurement emphasizes LTI 1.3, WCAG 2.2, and accessibility-compliant content, while EU and national initiatives guide interoperability and digital skills targets that shape vendor roadmaps.

What delivery channels and formats are most important right now in the digital education publishing market?

Web-based platforms hold the largest share, while mobile apps and blended learning formats are growing as institutions balance offline-capable access and analytics-rich hybrid instruction.

How are AI and assessment trends influencing the digital education publishing market?

AI-assisted assessment authoring and curriculum-integrated diagnostics increase scalability while human review ensures quality, and data integrations enable personalized pathways tied to outcomes.

Page last updated on: