Diesel Particulate Filter Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 24.15 Billion |

| Market Size (2031) | USD 29.25 Billion |

| Growth Rate (2026 - 2031) | 3.91% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Diesel Particulate Filter Market Analysis by Mordor Intelligence

The Diesel Particulate Filter Market size is projected to expand from USD 23.24 billion in 2025 and USD 24.15 billion in 2026 to USD 29.25 billion by 2031, registering a CAGR of 3.91% between 2026 and 2031. The regulatory push toward particulate-number limits as low as PN10, together with retrofit mandates for off-highway and marine engines, is reshaping revenue streams away from shrinking European passenger-car volumes toward Asia-Pacific heavy-duty and construction fleets. Silicon-carbide substrates are advancing on the back of Euro 7 and CARB Tier 5 thermal demands, while combined passive-active regeneration architectures are emerging as the preferred solution for stop-and-go urban logistics. Rising adoption of remanufacturing and AI-enabled predictive maintenance is lifting aftermarket profitability, and moderate supplier concentration is spurring vertical integration moves that secure platinum-group metal supply and catalytic-coating know-how.

Key Report Takeaways

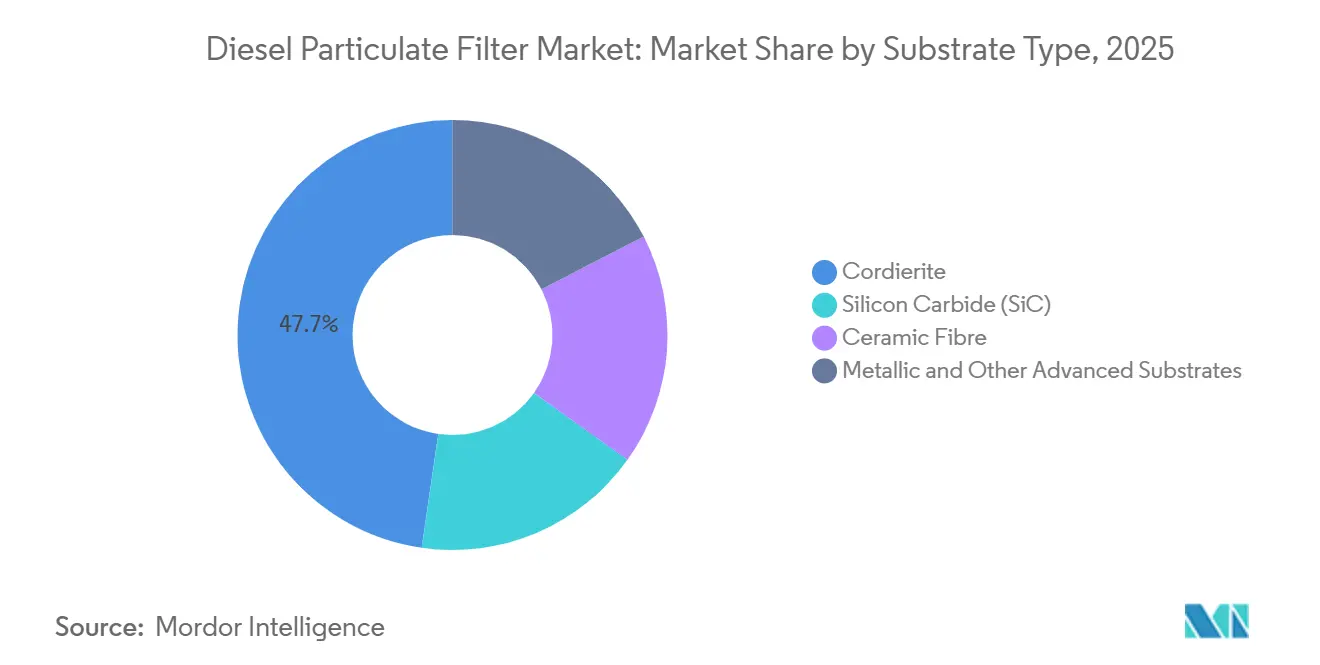

- By substrate technology, cordierite held 47.71% of the diesel particulate filter market size in 2025; silicon carbide is forecast to expand at a 4.32% CAGR by 2031.

- By regeneration process, passive systems maintained 50.33% diesel particulate filter market share in 2025, whereas combined passive-active concepts are set to grow at a 4.58% CAGR during the forecast period (2026-2031).

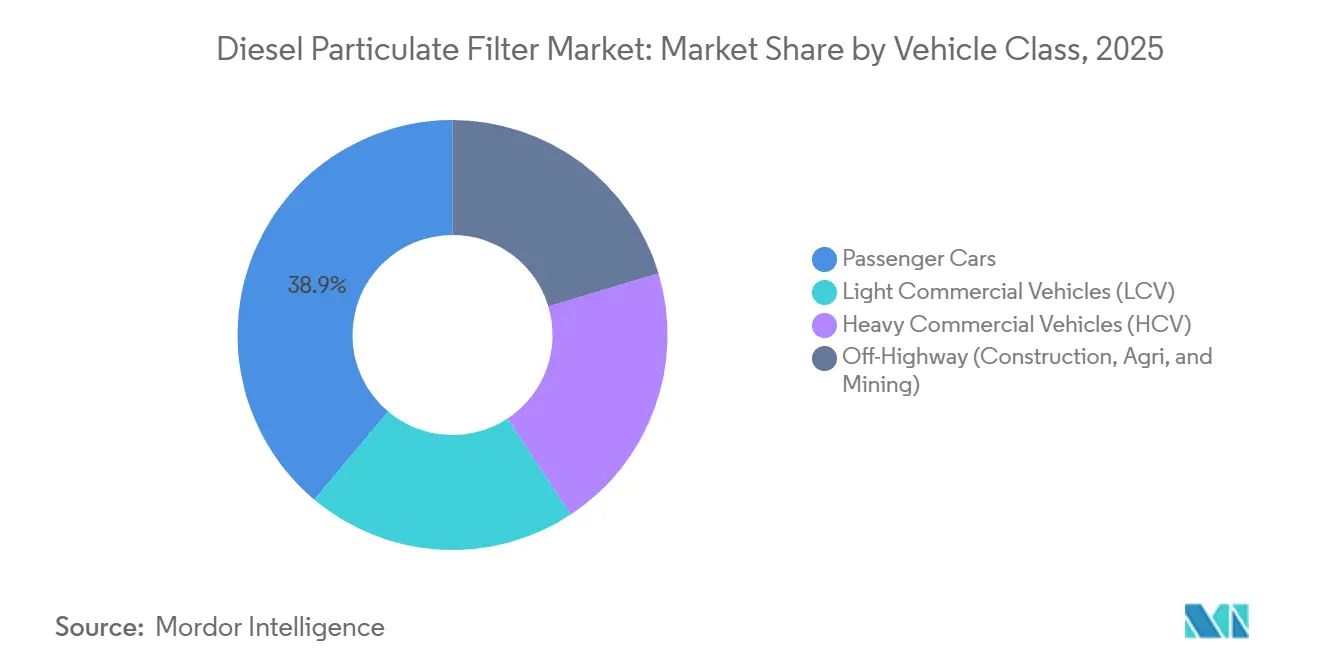

- By vehicle type, passenger cars captured 38.89% of the diesel particulate filter market size in 2025, but heavy commercial vehicles are projected to record a 4.12% CAGR throughout the outlook period (2026-2031).

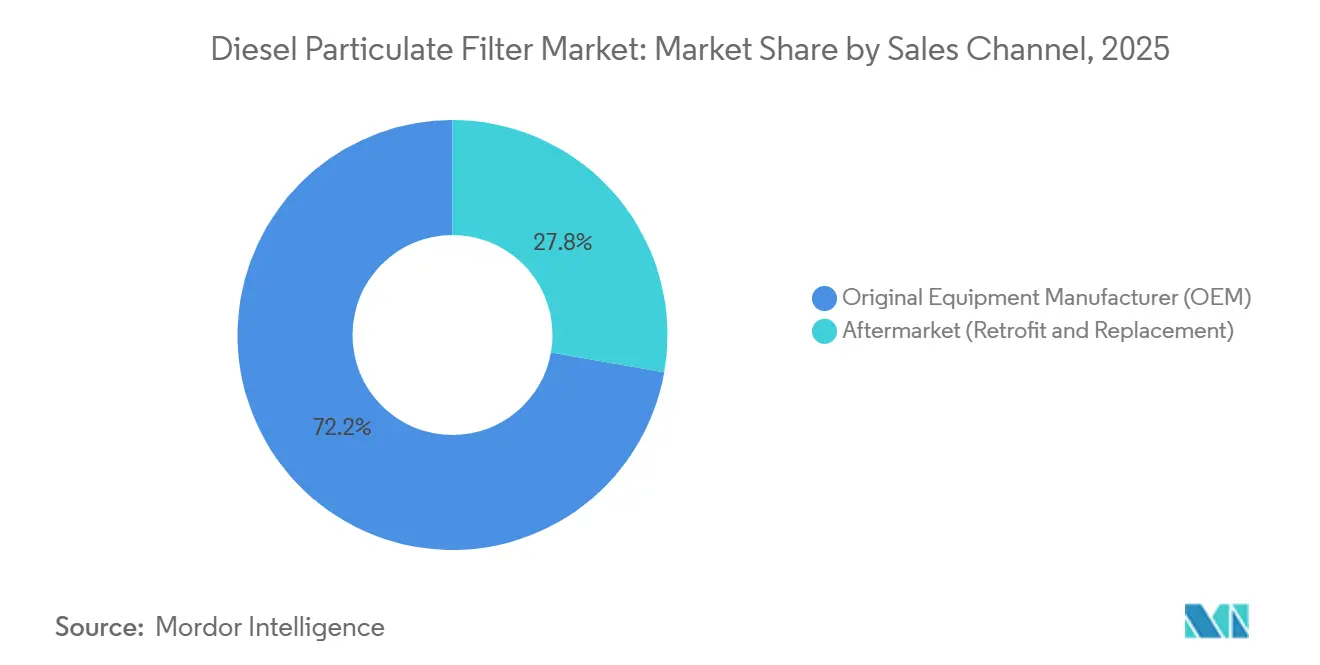

- By sales channel, OEM deliveries represented 72.22% of the diesel particulate filter market share in 2025, while aftermarket revenues are expected to climb at a 4.81% CAGR to 2031.

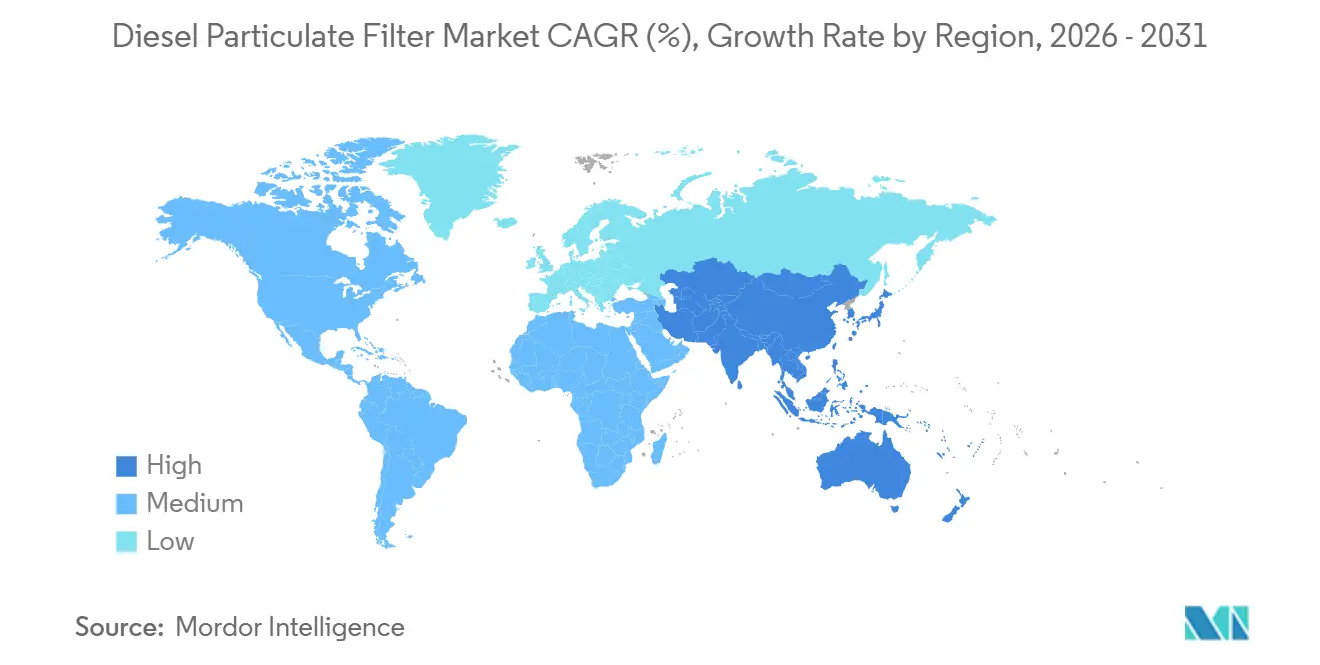

- By geography, Europe accounted for 42.23% of the diesel particulate filter market share in 2025, whereas Asia-Pacific is projected to post a 5.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Diesel Particulate Filter Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid diesel fleet growth in India, ASEAN and Africa | +1.2% | Asia-Pacific core, spillover to Middle East & Africa | Medium term (2-4 years) |

| Retrofit mandates for marine and off-road diesel equipment | +0.9% | Global, with concentration in North America, Europe, and coastal Asia | Medium term (2-4 years) |

| E-commerce last-mile boom lifting LCV mileage | +0.7% | Asia-Pacific, North America, Europe urban corridors | Short term (≤ 2 years) |

| Low-temperature, catalyst-coated filters for hybrid powertrains | +0.5% | Europe, Japan, South Korea | Long term (≥ 4 years) |

| AI-enabled predictive DPF maintenance unlocking fleet ROI | +0.6% | North America, Europe, India | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Diesel Fleet Growth in India, ASEAN and Africa

Commercial-vehicle sales in India rose 15% year-on-year to 107,486 units in January 2026, and diesel retained an 81.97% share[1]Society of Indian Automobile Manufacturers, “Monthly Commercial Vehicle Sales," siam.in. Fleet age averaged 10 years in fiscal 2025, driving replacements as Bharat Stage VI Stage 2 rules require wall-flow filters. ASEAN’s commercial-vehicle market is forecast to reach USD 83.51 billion by 2030, a 6.97% CAGR, with Thailand and Indonesia enforcing Euro-equivalent norms ahead of infrastructure rollouts. African ports are adopting low-emission zones that open retrofit opportunities for imported used trucks. The momentum across these regions underpins sustained demand for the Diesel particulate filter market.

Retrofit Mandates for Marine and Off-Road Diesel Equipment

The Netherlands required operational filters on all construction and agricultural machinery from January 2025, subsidizing installs that cut particulate mass by more than 90%. California’s Commercial Harbor Craft rule covers about 3,159 vessels and phases in level-3 systems once product verification is achieved[2]California Air Resources Board, “Commercial Harbor Craft Rule,” arb.ca.gov. CARB’s draft Tier 5 off-road proposal, issued in February 2026, will mandate filters on engines previously exempt under Tier 4. International Maritime Organization emission-control areas coming into force in March 2026 further expand demand for combined SCR-DPF solutions. These converging policies lift medium-term growth prospects for the Diesel particulate filter market.

E-Commerce Last-Mile Boom Lifting LCV Mileage

Urban delivery fleets in India and ASEAN routinely exceed 40,000 kilometers per year, accelerating soot buildup and shortening passive-regeneration intervals. Intangles introduced a digital-twin monitoring platform that tracks real-time soot levels across 200,000 trucks and cuts unplanned downtime by up to 75%. Higher mileage and data-driven maintenance raise replacement frequency, pushing active-regeneration and combined systems deeper into the Diesel particulate filter industry.

Low-Temperature, Catalyst-Coated Filters for Hybrid Powertrains

Hybrid diesel engines operate at lower exhaust temperatures, making soot oxidation harder. Umicore’s catalyzed filters enable passive regeneration below 300°C by converting NO to NO₂ inside the substrate. BASF unveiled a dual-layer catalyst-on-filter design at the 2026 SAE World Congress that simultaneously reduces NOₓ and oxidizes hydrogen for hybrid diesel-hydrogen concepts. Japan and South Korea are early adopters as hybrid commercial vehicles gain share, setting the stage for long-run uptake of advanced coatings in the Diesel particulate filter market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fast BEV and fuel-cell uptake in urban buses and cars | -0.8% | Europe, North America, China urban centers | Medium term (2-4 years) |

| Post-COVID delays to Euro-7 weaken 2025-26 demand | -0.5% | Europe | Short term (≤ 2 years) |

| HVO/Synthetic-diesel adoption lowers PM and filter demand | -0.3% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fast BEV and Fuel-Cell Uptake in Urban Buses and Cars

Electric penetration in Indian commercial segments was 1.92% in January 2026 but is projected to reach up to 30% of buses by 2030, mostly in metropolitan corridors. The United States hydrogen truck fleet could rise from 5,000 units in 2024 to 75,000 by 2030, eliminating filter servicing on those vehicles. European low-emission zones incentivize zero-emission buses, eroding light-duty diesel volumes, yet long-haul and off-highway sectors remain diesel-reliant. This urban–rural split tempers overall Diesel particulate filter market expansion.

Post-COVID Delays to Euro 7 Weaken 2025-26 Demand

The European Commission shifted Euro 7 start dates to late 2026 for light-duty and to 2027-2028 for heavy-duty vehicles. OEMs paused tooling for next-generation filters, generating a temporary ordering trough. Euro 7 will ultimately impose PN10 particle counting and 200,000-kilometer durability, demanding silicon-carbide substrates and advanced coatings. Near-term softness in Europe, therefore, contrasts with resilience in Asia-Pacific, moderating the Diesel particulate filter market trajectory through 2026.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Substrate Type: Silicon Carbide Addresses Higher Thermal Loads

Cordierite retained 47.71% market share in 2025 on cost advantages but faces thermal limits at 1,400°C, whereas silicon carbide tolerates more than 2,000°C, accelerates regeneration, and achieves filtration efficiency above 99%. Silicon-carbide components accounted for a rising slice of the Diesel particulate filter market size and are set to grow at a 4.32% CAGR during the forecast period (2026-2031) as Euro 7 and CARB Tier 5 tighten PN thresholds.

OEMs such as NGK, Corning, and IBIDEN have released porous structures that cut backpressure without sacrificing ash capacity. Faurecia Service remanufactures silicon-carbide filters via a six-step process that lowers costs by 30% and extends service life, reinforcing aftermarket uptake. Higher price sensitivity in passenger cars constrains penetration, yet heavy-duty and hybrid applications will continue shifting volumes toward silicon carbide through 2031.

By Regeneration Process: Combined Systems Suit Urban Duty Cycles

Passive regeneration dominated installations with 50.33% share in 2025, but combined passive-active architectures are projected to rise at 4.58% CAGR during the forecast period (2026-2031) as stop-and-go duty cycles prevail in last-mile fleets. Cummins introduced the Twin Module system with twin 5 kW heaters powered by a 48-V alternator, enabling rapid soot burn-off without diesel dosing.

SAE studies demonstrate that high-pressure dosing and thermal-management strategies improve regeneration efficiency by up to 20% and lower HC and CO by 95%. While active events consume extra fuel, predictive scheduling reduces occurrences, balancing cost and compliance. Emerging plasma and electric-only heaters are under trial for stationary and marine sets, indicating an innovation runway in the Diesel particulate filter market.

By Vehicle Type: Heavy Commercial Vehicles Sustain Growth

Passenger cars supplied 38.89% of the 2025 volume, yet heavy commercial vehicles will expand at a 4.12% CAGR during the forecast period (2026-2031) on the back of Bharat Stage VI upgrades and ASEAN infrastructure spending. India’s average truck age hit 10 years in fiscal 2025, triggering a replacement cycle that embeds wall-flow filters into every new diesel.

Off-highway machinery is also in focus as the Netherlands, CARB, and the International Maritime Organization impose retrofit requirements on construction, agriculture, and marine engines. Electrification timelines in these segments extend beyond 2031, underpinning steady demand for the Diesel particulate filter industry across high-load applications.

By Sales Channel: Aftermarket Benefits From Aging Fleets

Original Equipment Manufacturer (OEM) deliveries held 72.22% revenue share in 2025, but the aftermarket (retrofit and replacement) is forecast to outpace at a 4.81% CAGR through 2031. Replacement units cost USD 3,000-10,000, and downtime averages 8-12 hours per failure, incentivizing proactive ash cleaning and predictive maintenance.

Platforms from Intangles and others cut forced regenerations by up to 75%, lengthening service intervals and lifting parts sales for sensors and gaskets. Retrofit programs in marine and off-road sectors, plus extended life cycles in developing regions, further widen the aftermarket’s addressable base within the Diesel particulate filter market.

Geography Analysis

Europe generated 42.23% of 2025 revenue on the strength of Euro 6 saturation and robust remanufacturing networks. The Euro 7 delay moderates 2025-26 demand, yet future PN10 limits and 200,000-kilometer durability will pivot fleets to silicon-carbide substrates and advanced coatings, especially in Germany, France, and the United Kingdom. Circular-economy moves by BASF, which recycles platinum-group metals with 97% lower CO₂ than primary refining, align with looming sustainability guidelines.

Asia-Pacific is set to post the fastest 5.12% CAGR during the forecast period (2026-2031), anchored by India’s 81.97% diesel share in commercial vehicles, ASEAN’s growth in fleet spending, and China's 7 implementation timelines. The Diesel particulate filter market size across the region will accelerate as older trucks are scrapped and new Bharat Stage VII and China 7 engines adopt high-efficiency substrates. Early hybrid uptake in Japan and South Korea drives demand for catalyst-coated filters that regenerate below 300°C.

North America remains a sizable market where EPA Tier 4 Final keeps off-road equipment filtered. CARB Tier 5, proposed for 2031-36, will widen adoption to engines previously exempt, while hydrogen truck pilots reduce urban demand. California’s R99 or R100 renewable-diesel mandate cuts PM but does not eliminate filtration needs, preserving aftermarket volumes for silicon-carbide units that withstand extended service intervals.

Competitive Landscape

The diesel particulate filter market is moderately concentrated. Remanufacturing players such as Faurecia Service deliver 30% cost savings through renewed silicon-carbide filters, aligning with circular-economy mandates and fleet budget constraints. Technology leadership now hinges on high-thermal-conductivity substrates, below-300°C catalyst coatings, and integrated sensors that support Euro 7 and EPA (Environmental Protection Agency) on-board diagnostics, all of which shape the Diesel particulate filter market’s competitive dynamics.

Diesel Particulate Filter Industry Leaders

-

Tenneco Inc.

-

FORVIA

-

Corning Incorporated

-

Johnson Matthey

-

Cummins Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Johnson Matthey (JM) revealed that its DPFi electrically regenerating diesel particulate filter (DPF) received certification from the Canadian Standards Association (CSA), validating its safety and performance for underground mining and tunneling applications.

- September 2025: Power Service announced the launch of Diesel Injector and DPF Flush, the industry's first single-tank solution to clean the entire diesel fuel system, injectors, turbo, DPF, and more.

Global Diesel Particulate Filter Market Report Scope

A Diesel Particulate Filter (DPF) is an exhaust aftertreatment device that captures and stores exhaust soot, reducing emissions from diesel vehicles by up to 99%. It uses a honeycomb ceramic structure to trap particulates, which are periodically burned off through a self-cleaning "regeneration" process to prevent clogging.

The diesel particulate filter market is segmented by substrate type, regeneration process, vehicle type, sales channel, and geography. By substrate type, the market is segmented into cordierite, silicon carbide (SIC), ceramic fiber, and metallic and other advanced substrates. By regenration process, the market is segmented into passive, active (in-cylinder/in-exhaust), and combined passive-active. By vehicle type, the market is segmented into passenger cars, light commercial vehicles (LCV), heavy commercial vehicles (HCV), and off-highway (construction, agri, and mining). By sales channel, the market is segmented into original equipment manufacturer (OEM) and aftermarket (retrofit and replacement). The report also covers the market size and forecasts for diesel particulate filters in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Cordierite |

| Silicon Carbide (SiC) |

| Ceramic Fiber |

| Metallic and Other Advanced Substrates |

| Passive |

| Active (In-cylinder/In-exhaust) |

| Combined Passive-Active |

| Passenger Cars |

| Light Commercial Vehicles (LCV) |

| Heavy Commercial Vehicles (HCV) |

| Off-Highway (Construction, Agri, and Mining) |

| Original Equipment Manufacturer (OEM) |

| Aftermarket (Retrofit and Replacement) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Substrate Type | Cordierite | |

| Silicon Carbide (SiC) | ||

| Ceramic Fiber | ||

| Metallic and Other Advanced Substrates | ||

| By Regeneration Process | Passive | |

| Active (In-cylinder/In-exhaust) | ||

| Combined Passive-Active | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles (LCV) | ||

| Heavy Commercial Vehicles (HCV) | ||

| Off-Highway (Construction, Agri, and Mining) | ||

| By Sales Channel | Original Equipment Manufacturer (OEM) | |

| Aftermarket (Retrofit and Replacement) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

Which regions will drive the strongest growth in diesel particulate filters by 2031?

Asia-Pacific is projected to post the fastest 5.12% CAGR during the forecast period (2026-2031), led by India, ASEAN, and China.

Why are silicon-carbide filters gaining share over cordierite units?

Silicon carbide withstands higher temperatures, enables faster regeneration, and meets Euro 7 durability targets, driving a 4.32% CAGR during the forecast period (2026-2031).

How will Euro 7 affect demand for diesel particulate filters?

Stricter PN10 limits and 200,000-kilometer durability will boost adoption of advanced substrates and coatings after the regulation starts in late 2026-2028.

What role does predictive maintenance play in filter replacement cycles?

AI platforms like Intangles cut forced regenerations by up to 75%, lengthen service intervals, and support the aftermarket’s 4.81% CAGR during the forecast period (2026-2031).

What is the market size of diesel particulate filter market?

The Diesel Particulate Filter Market size is projected to expand from USD 23.24 billion in 2025 and USD 24.15 billion in 2026 to USD 29.25 billion by 2031, registering a CAGR of 3.91% between 2026 and 2031.

Page last updated on: