CyberKnife Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

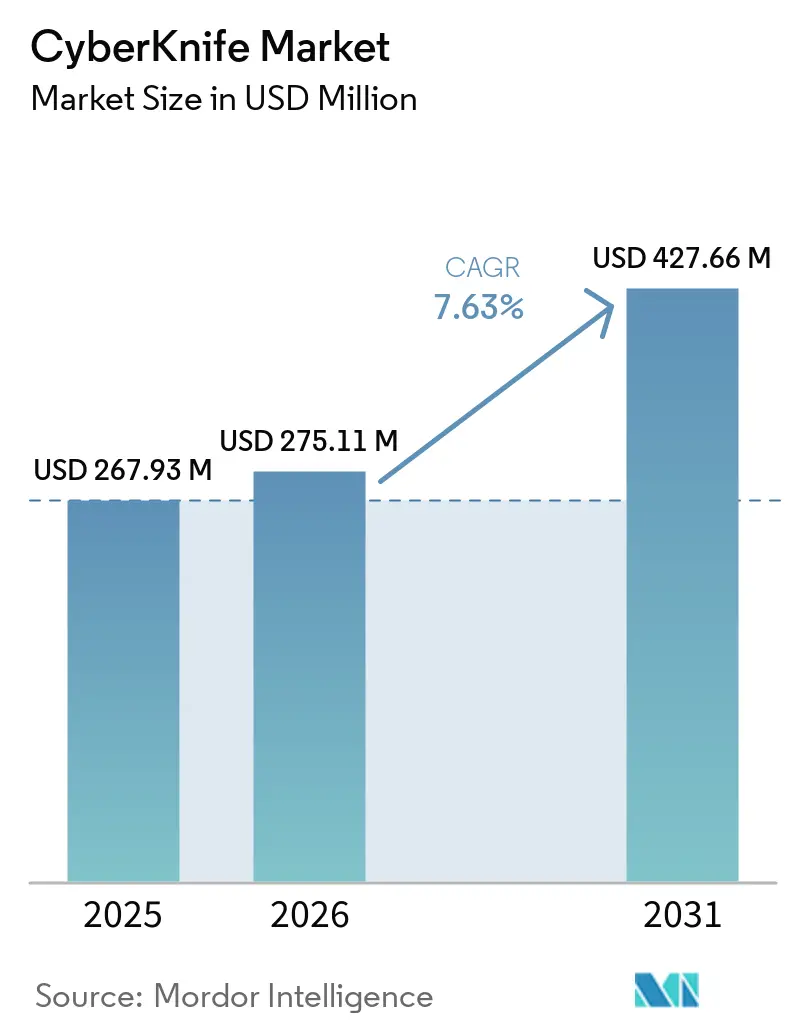

| Market Size (2026) | USD 275.11 Million |

| Market Size (2031) | USD 427.66 Million |

| Growth Rate (2026 - 2031) | 7.63% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

CyberKnife Market Analysis by Mordor Intelligence

The CyberKnife Market size is projected to expand from USD 267.93 million in 2025 and USD 275.11 million in 2026 to USD 427.66 million by 2031, registering a CAGR of 7.63% between 2026 to 2031.

The market is expanding because cancer care providers are placing more value on sub-millimeter accuracy, real-time tracking, and shorter treatment schedules as routine clinical needs rather than premium differentiators. The CyberKnife market is also supported by the rising global cancer burden, with the World Health Organization stating that annual cancer cases are expected to exceed 35 million by 2050, which keeps demand firm for high-precision radiation systems that can handle larger caseloads without matching growth in physical infrastructure. The CyberKnife market benefits from the system’s ability to treat intracranial and extracranial targets in 1 to 5 outpatient sessions, which aligns with provider efforts to improve ambulatory efficiency and patient throughput. The CyberKnife market is also being shaped by a revenue mix that is moving toward software and service layers, while greenfield installations in Asia-Pacific are widening the platform’s geographic base. The CyberKnife market remains highly concentrated around a single vendor, which supports pricing discipline and ecosystem control, but it also leaves yearly revenue exposed to delays in a limited pool of high-value capital decisions and to geopolitical disruption.

Key Report Takeaways

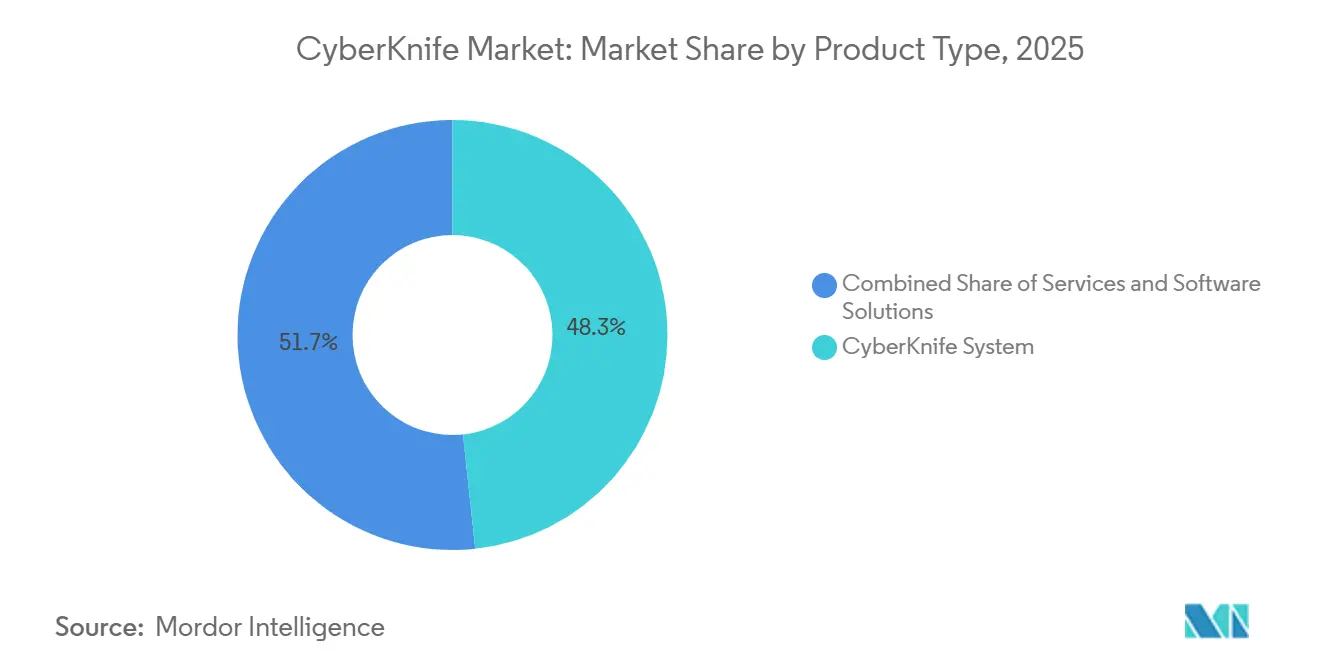

- By product type, CyberKnife System hardware held 48.31% revenue share in 2025, while services are projected to grow at an 8.38% CAGR through 2031.

- By indication, tumor and cancer treatment accounted for 85.24% share in 2025, while vascular malformation is forecast to expand at an 8.52% CAGR through 2031.

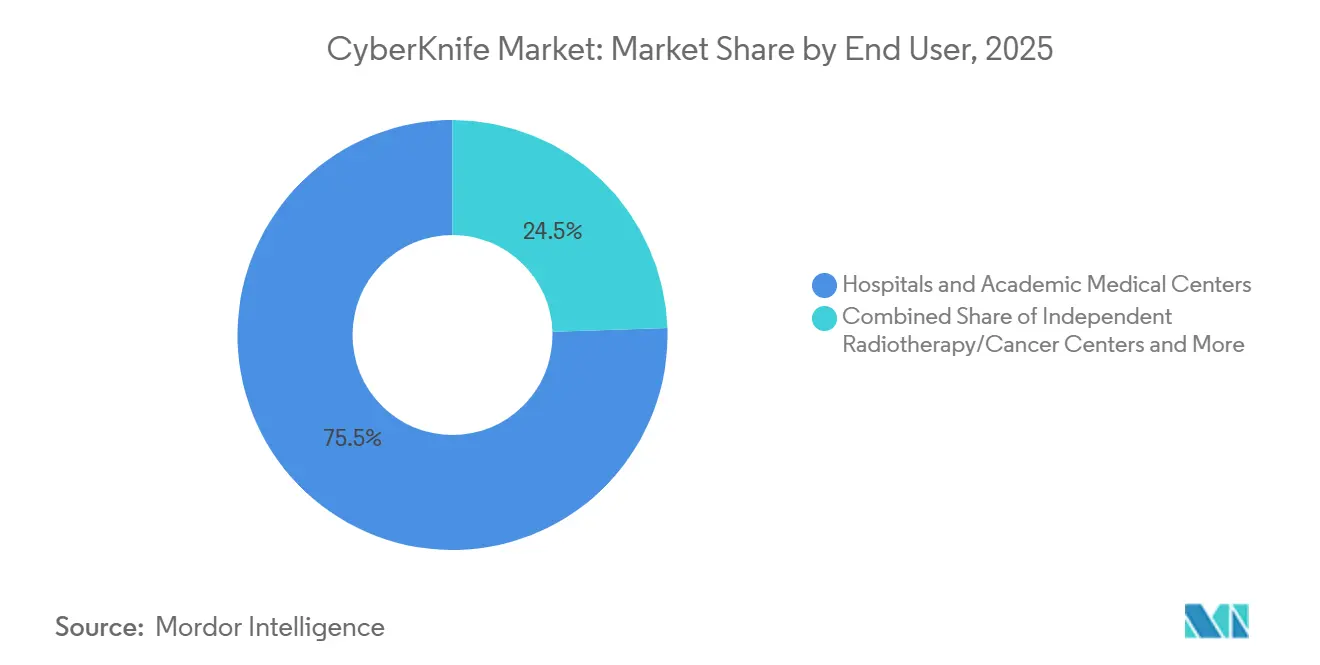

- By end user, hospitals and academic medical centers held 75.52% share in 2025, while ambulatory and outpatient radiosurgery centers are expected to grow at a 9.25% CAGR through 2031.

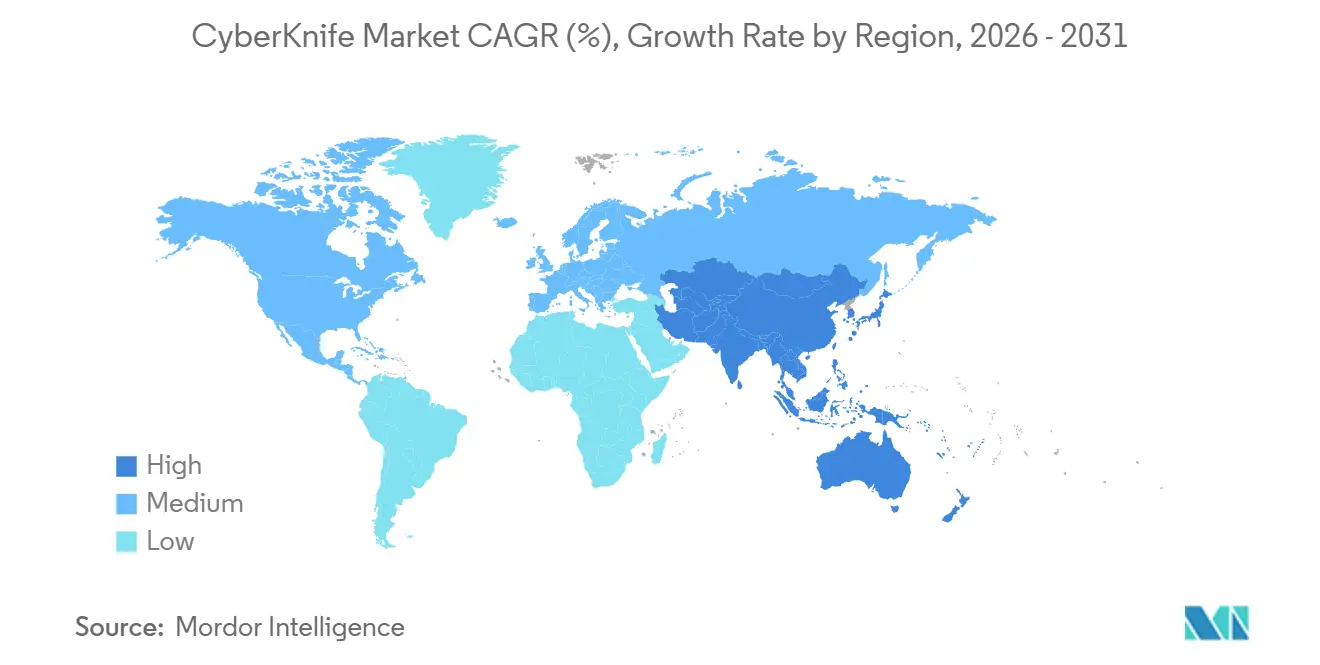

- By geography, North America held 45.22% share in 2025, while Asia-Pacific is projected to record the fastest regional growth at a 9.65% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global CyberKnife Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Cancer Burden And Treatment Demand | +2.1% | Global, with elevated intensity in APAC and MEA as incidence growth outpaces infrastructure | Long term (≥ 4 years) |

| Preference For Non-Invasive And Organ-Sparing Treatment | +1.5% | Global, strongest in North America and Western Europe where patient-reported outcomes shape referrals | Medium term (2-4 years) |

| Expansion Of Outpatient And Ambulatory Radiosurgery Delivery | +1.2% | North America and APAC core, with spillover to Latin America and MEA | Medium term (2-4 years) |

| Faster Adoption Of Hypofractionated Treatment Pathways | +1.0% | North America, Europe, Australia | Medium term (2-4 years) |

| Reimbursement Optimization For Complex High-Cost Procedures | +0.8% | North America and EU, with selective gains in APAC under national insurance schemes | Short term (≤ 2 years) |

| Movement-Tracking And Real-Time Imaging Differentiation | +0.6% | Global, with early adoption in academic centers across North America and East Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Cancer Burden and Treatment Demand

The CyberKnife market is gaining support from the steady rise in cancer volume and case complexity across major care systems. The World Health Organization said annual global cancer cases are expected to exceed 35 million by 2050, which keeps long-term demand strong for precise radiation platforms that can absorb more patients without a matching increase in treatment infrastructure[1]World Health Organization, “Global Cancer Burden Growing, Amidst Mounting Need for Services,” WHO, who.int. This demand is especially relevant for brain metastases, vertebral metastases, and prostate cancer, where longer survival in primary oncology is increasing the number of patients who need focused local treatment. Australia’s cancer diagnoses are projected to rise from 212,332 cases to 318,285 by 2045, which supports the business case for expanding access to high-precision treatment networks. Austria also remains under-supplied in radiotherapy equipment, with availability 27% below the EU average and 34% below economic peers, which creates room for new CyberKnife market installations in under-served regions. As these supply gaps persist, the CyberKnife market is likely to benefit most in locations where cancer demand is rising faster than radiotherapy capacity.

Preference for Non-Invasive and Organ-Sparing Treatment

The CyberKnife market is also benefiting from the broader preference for non-invasive care that avoids surgery when clinical outcomes are comparable. CyberKnife’s Synchrony real-time motion-tracking capability helps clinicians treat thoracic, hepatic, and spinal targets with continuous adjustment for patient movement, which broadens its use beyond frame-based intracranial treatment. A 2025 long-term study of vestibular schwannoma patients reported 89.3% local control and 97.1% overall survival at 25 years after CyberKnife treatment, which reinforces confidence in durable organ-sparing management. A 2025 clinical study from Peking Union Medical College Hospital also found highly accurate dose delivery with minimal damage to surrounding tissue in pituitary adenoma and lung adenocarcinoma vertebral metastasis cases, which supports broader extracranial use. As a result, the CyberKnife market is gaining from a treatment preference that values precision, tissue preservation, and recovery outside the operating room.

Expansion of Outpatient and Ambulatory Radiosurgery Delivery

The CyberKnife market is moving closer to outpatient care models as hospitals and physician groups look for more efficient ways to deliver high-value oncology services. Bundled payment models and value-based reimbursement create pressure to reduce inpatient use, which makes ambulatory treatment settings more attractive for eligible radiation cases. CyberKnife fits this shift because its 1 to 5 session treatment profile allows faster scheduling and removes the long multi-week treatment pattern associated with conventional radiotherapy. In July 2025, Asian Hospital in the Philippines installed the country’s first CyberKnife S7 system, and in October 2025 Unio Specialty Care launched community-based CyberKnife S7 treatment in San Diego, showing that deployment is moving beyond major academic hubs. Vietnam’s social health insurance now covers CyberKnife S7 treatment, which lowers the affordability barrier and improves the case for broader utilization beyond elite private settings. This shift is important because the CyberKnife market can expand faster when treatment access is no longer limited to large tertiary campuses.

Faster Adoption of Hypofractionated Treatment Pathways

The CyberKnife market is also supported by the wider use of hypofractionated treatment plans that shorten therapy timelines without giving up local control. A 2026 peer-reviewed cohort study in Radiation Oncology reported durable local control in brain metastases treated with CyberKnife fractionated stereotactic radiotherapy, while also identifying tumor volume and prior surgery as important predictors of outcome. The platform’s ability to deliver prostate treatment in 5 sessions instead of 40 conventional sessions improves treatment vault productivity and strengthens the return profile of each installed system. This matters more in emerging markets where capital outlays of USD 5 million to USD 7 million need strong utilization to be justified. Post-surgical resection cavity treatment is also gaining ground, with a 2025 study reporting 1-year local control rates of 93% for stereotactic radiosurgery after brain metastasis resection. As these shorter-course protocols become more accepted, the CyberKnife market stands to benefit from higher throughput and a broader set of clinically validated use cases.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost And Service Intensity | -2.2% | Global, most acute in low- and middle-income markets across APAC, MEA, and Latin America | Long term (≥ 4 years) |

| Prior Authorization And Reimbursement Friction | -1.5% | North America, with emerging policy pressure in EU and select APAC markets | Short term (≤ 2 years) |

| Site-Of-Care Concentration In Specialized Centers | -1.0% | Global, pronounced outside North America and Western Europe | Medium term (2-4 years) |

| Installed Base Dependence And Slow Conversion Cycles | -0.8% | Global, with concentration in mature markets such as North America, Germany, and Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost and Service Intensity

The CyberKnife market still faces a major barrier from the high upfront cost of system acquisition and the ongoing cost of support after installation. A typical system costs USD 5 million to USD 7 million before shielding construction and commissioning, which limits new projects to well-capitalized academic and tertiary providers. This burden becomes even more important after installation because service contracts, upgrades, and maintenance add recurring obligations over the asset life. Accuray reported that service revenue rose 3% year over year to USD 169.1 million in the first 9 months of fiscal 2026, while product revenue fell 21%, which shows how a slower capital cycle and a maturing installed base can weigh on fresh placements while raising service dependence. In Mexico, IMSS spent USD 8.7 million, to commission its first CyberKnife system in December 2025, which underlines how large these projects are even for public institutions. Because of this, the CyberKnife market remains concentrated in health systems that can absorb both capital and long-term service intensity.

Prior Authorization and Reimbursement Friction

The CyberKnife market is also constrained by reimbursement delays and payer scrutiny, especially in North America. An ASTRO survey published in June 2025 found that 92% of radiation oncologists said prior authorization delayed treatment initiation, while 68% said those delays extended beyond 1 week. CyberKnife procedures face an additional layer of review because CMS uses dedicated HCPCS codes G0339 and G0340 for robotic image-guided radiosurgery, and some Medicare Advantage plans have reportedly denied these claims at elevated rates compared with other radiation therapy services. A 2024 peer-reviewed review in Advances in Radiation Oncology also found that radiation oncology carried the highest prior authorization burden across medical specialties, with stereotactic body radiation therapy seeing a disproportionate impact[2]“The Burden of Insurance Prior Authorization on Cancer Care, A Review of Evidence From Radiation Oncology,” Advances in Radiation Oncology, advancesradonc.com. CMS then finalized further valuation changes for radiation therapy delivery codes in the CY 2026 Physician Fee Schedule, which added more administrative recalibration during the current operating cycle. Until approval timelines improve, the CyberKnife market will continue to face revenue timing pressure even in clinically established settings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Services Growth Reshapes the Revenue Architecture

The CyberKnife System segment held 48.31% of the CyberKnife market share in 2025, which kept hardware as the largest product category in the CyberKnife market. Services, however, are projected to grow at an 8.38% CAGR through 2031, making them the fastest-rising layer of the CyberKnife market by product type. This change matters because installed systems generate recurring revenue through preventive maintenance, remote diagnostics, training, and software upgrades even when new hardware orders slow. Accuray reported service revenue of USD 169.1 million in the first 9 months of fiscal 2026, up 3% year over year, while product revenue declined, which supports the view that the installed base is becoming more important to the CyberKnife market than single equipment sales[3]Accuray Incorporated, “Accuray Reports Fiscal 2026 Third Quarter Financial Results,” Accuray Investor Relations, accuray.com.

Software is still the most dynamic layer inside the broader platform stack because it supports planning, adaptive delivery, and faster commissioning. Accuray received NMPA approval in China for the Accuray Precision Treatment Planning System in June 2024, and in September 2025 launched the Stellar solution, which brought adaptive radiotherapy capabilities together with CyberComm commissioning tools. That launch shows how the CyberKnife industry is moving toward a model where software, service, and workflow integration deepen customer retention after the initial sale. It also means procurement teams are placing more weight on lifetime ownership cost than on unit price alone. In practical terms, the CyberKnife market size for services is projected to expand at 8.38% CAGR through 2031, which signals that recurring post-sale revenue is becoming central to vendor economics.

By Indication: Vascular Malformation Emerges as a High-Value Growth Corridor

Tumor and cancer treatment accounted for 85.24% share in 2025, which made oncology the clear foundation of the CyberKnife market by indication. Prostate cancer, lung cancer, brain metastases, and spinal tumors remain the highest-volume use cases because they fit the platform’s need for accurate dose delivery around critical structures. Long-term clinical data continue to support that position, with reported 10-year disease-free survival of 93.7% in localized prostate cancer treated with CyberKnife. This strong oncology base gives the CyberKnife market a broad demand floor across both intracranial and extracranial treatment settings.

Vascular malformation remains smaller in absolute revenue but is forecast to grow at an 8.52% CAGR through 2031, which makes it the fastest-growing indication in the CyberKnife market. A 2025 study in Strahlentherapie und Onkologie reported 5-year obliteration rates of 85.2% for Spetzler-Martin grade I and II cerebral arteriovenous malformations, which supports radiosurgery as a strong treatment option in selected cases. A 2025 meta-analysis in the Journal of Clinical Neuroscience also found that stereotactic radiosurgery alone delivered higher AVM obliteration rates than combined embolization plus radiosurgery, which lowers some of the procedural friction that previously shaped treatment sequencing. Other uses such as trigeminal neuralgia, functional neurosurgery, and cardiac arrhythmias remain smaller today but are strategically important for future volume. FV Hospital’s May 2025 deployment in Vietnam included positioning for cardiac arrhythmia treatment as well as vascular malformations, which shows how the CyberKnife industry is testing expansion beyond its core oncology base.

By End User: Ambulatory Centers Redefine the Access Frontier

Hospitals and academic medical centers held 75.52% share in 2025, which kept them as the leading end-user group in the CyberKnife market. Their lead reflects the need for high capital investment, shielded vaults, and multidisciplinary clinical teams that large institutions are better able to organize and fund. This concentration has been reinforced by the fact that many early deployments were made in tertiary settings where complex oncology volumes were already established. Even so, the center of gravity inside the CyberKnife market is starting to shift as other care settings become operationally viable.

Ambulatory and outpatient radiosurgery centers are projected to grow at a 9.25% CAGR through 2031, which makes them the fastest-growing end-user group in the CyberKnife market. This shift is tied to shorter treatment schedules, improved commissioning speed through CyberComm, and the ability of community-based providers to raise vault utilization with hypofractionated treatment patterns. Unio Specialty Care’s October 2025 installation in San Diego shows that physician-led and private-equity-backed platforms are now willing to place CyberKnife outside quaternary academic centers. Independent radiotherapy centers also sit in an important middle tier, especially where oncology delivery is partly privatized or regionally dispersed. Mexico’s IMSS expected a daily schedule of 30 to 35 radiosurgery sessions after launch, which shows how throughput assumptions now shape adoption decisions at the institutional level.

Geography Analysis

North America held 45.22% share in 2025, which gave the region the largest position in the CyberKnife market and the most established operating environment. The United States remained the anchor because of its large installed base, established CMS reimbursement codes for robotic image-guided radiosurgery, and long history of high-technology oncology procurement. Even in this mature setting, access is still expanding into community care, as shown by the October 2025 San Diego CyberKnife S7 launch, which was described as one of only 2 sites in California and the only one in Southern California. Mexico remained a smaller market, but its December 2025 public-sector installation through IMSS marked a meaningful regional step because it showed that government-backed procurement can support CyberKnife market development outside high-income systems.

Europe remains more concentrated by country and by site type, with academic centers playing a leading role in the CyberKnife market. Germany continued to be the region’s most established base, and Charité Berlin remained a prominent university hospital site for CyberKnife treatment. Austria added a fresh point of expansion in May 2025 when the CyberKnife Center Salzburg started SRS and SBRT patient treatments using the CyberKnife S7 system. That project also highlighted a structural supply gap, since Austria’s radiotherapy equipment availability remained 27% below the EU average, which supports room for further CyberKnife market growth in under-equipped systems. Across the region, compliance under EU medical device rules continues to add cost and operating discipline for both vendors and center operators.

Asia-Pacific is projected to grow at a 9.65% CAGR through 2031, which makes it the fastest-expanding regional block in the CyberKnife market. China’s January 2025 NMPA approval of the CyberKnife S7 system opened a much larger hospital base to next-generation deployment and improved the platform’s access to one of the world’s largest cancer care systems. In India, installations in Lucknow and Western Uttar Pradesh show that adoption is moving beyond top-tier metro centers, although regulatory approvals still shape commissioning timelines. Australia also became a visible growth market after the October 2025 Melbourne launch through a joint venture between 5D Clinics and Icon Group, with plans to expand across the East Coast. In the Middle East and Africa, Tawam Hospital introduced the first CyberKnife S7 deployment in Abu Dhabi and Kenya commissioned the first CyberKnife in sub-Saharan Africa, while South America remained early stage with Brazil and Colombia already active and Mexico joining the regional installed base in 2025.

Competitive Landscape

The CyberKnife market operates under a very unusual structure because Accuray Incorporated is the only manufacturer and developer of the CyberKnife platform. That gives Accuray full control over hardware, software, upgrades, and service for the installed base, which makes the CyberKnife market a single-vendor platform business rather than a multi-vendor equipment category. As a result, competition comes from substitute technologies rather than direct CyberKnife rivals. The main alternatives remain Elekta’s Gamma Knife for intracranial applications, linear accelerator-based SBRT systems from Varian Medical Systems for extracranial treatment, and proton therapy for selected complex cases.

Accuray’s differentiation still rests on Synchrony real-time motion tracking and on the fact that CyberKnife is the only dedicated robotic radiosurgery platform designed to treat tumors throughout the body in one system architecture. The company’s December 2025 transformation plan targeted USD 25 million in annualized profitability improvement through cost rightsizing, commercial simplification, and service margin recovery. That move signaled a clear shift in the CyberKnife market from volume-led expectations to stronger monetization of the installed base. The same pressure was visible in product orders, with gross product orders falling to USD 48.5 million in Q3 FY2026 from USD 71.2 million in the prior-year period.

Growth opportunities in the CyberKnife market now center on underpenetrated geographies, deeper software and service attachment, and expansion into adjacent clinical uses. Accuray’s September 2025 launch of the Stellar all-in-one radiotherapy solution was one important strategic step because it connected adaptive radiotherapy capability with faster commissioning and tighter workflow integration. A second major step came in May 2026, when Accuray signed a 10-year Master Research Agreement with the University of Wisconsin School of Medicine and Public Health to advance personalized cancer treatment through the Stellar platform. A third example was the October 2025 Melbourne deployment through the 5D Clinics and Icon Group joint venture, which showed how private capital can help extend the CyberKnife market into multi-center regional networks. The main technology risk is that AI-enabled adaptive delivery on competing LINAC platforms could narrow the premium clinical distinction that currently supports CyberKnife use in extracranial radiosurgery.

CyberKnife Industry Leaders

Accuray Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: The Board of Investments (BOI) celebrated a significant milestone in Philippine healthcare as Asian Hospital and Medical Center (AHMC), a BOI-registered enterprise, marked the treatment of its first 100 cancer patients using the country’s first CyberKnife robotic radiosurgery system.

- October 2025: Accuray announced first CyberKnife S7 patient treatments in Melbourne, Australia, delivered through a joint venture between 5D Clinics and Icon Group with alphaXRT as the exclusive Australasian distributor and trainer. The JV plans to expand CyberKnife centers across Australia's East Coast, reducing patient travel burdens.

Global CyberKnife Market Report Scope

As per the scope of the report, CyberKnife is a brand of advanced, non-invasive robotic radiotherapy system used to treat cancer and other medical conditions. It delivers highly precise, targeted radiation beams to destroy tumors while minimizing damage to surrounding healthy tissue.

The CyberKnife market is segmented by product type, indication, end user, and geography. By product type, the market includes CyberKnife systems, software solutions, and services. By indication, it covers tumors and cancer, vascular malformations, and other conditions. By end user, the segmentation includes hospitals and academic medical centers, independent radiotherapy/cancer centers, and ambulatory/outpatient radiosurgery centers. Geographically, the market is divided into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| CyberKnife System |

| Software Solutions |

| Services |

| Tumor and Cancer |

| Vascular Malformation |

| Other Indications |

| Hospitals & Academic Medical Centers |

| Independent Radiotherapy/Cancer Centers |

| Ambulatory/Outpatient Radiosurgery Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | CyberKnife System | |

| Software Solutions | ||

| Services | ||

| By Indication | Tumor and Cancer | |

| Vascular Malformation | ||

| Other Indications | ||

| By End User | Hospitals & Academic Medical Centers | |

| Independent Radiotherapy/Cancer Centers | ||

| Ambulatory/Outpatient Radiosurgery Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving growth in CyberKnife demand through 2031?

Growth is being supported by rising cancer incidence, stronger demand for non-invasive organ-sparing treatment, more outpatient deployment, and wider use of hypofractionated care pathways.

How large will the CyberKnife business become by 2031?

The CyberKnife market size is projected to reach USD 427.66 million by 2031, rising from USD 275.11 million in 2026 at a 7.63% CAGR.

Which product area is growing fastest in this space?

Services are the fastest-growing product type, with an 8.38% CAGR through 2031, while hardware remained the largest category with 48.31% share in 2025.

Which clinical use accounts for the largest revenue base?

Tumor and cancer treatment led with 85.24% share in 2025, while vascular malformation is the fastest-growing indication at an 8.52% CAGR through 2031.

Which end users are expanding fastest?

Ambulatory and outpatient radiosurgery centers are growing fastest at a 9.25% CAGR through 2031, even though hospitals and academic medical centers still held 75.52% share in 2025.

Which region offers the strongest near-term expansion potential?

Asia-Pacific shows the strongest growth outlook with a 9.65% CAGR through 2031, supported by new installations in China, India, the Philippines, Vietnam, and Australia.

Page last updated on: