Crepe Makers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 158.56 Billion |

| Market Size (2031) | USD 224.12 Billion |

| Growth Rate (2026 - 2031) | 7.17% CAGR |

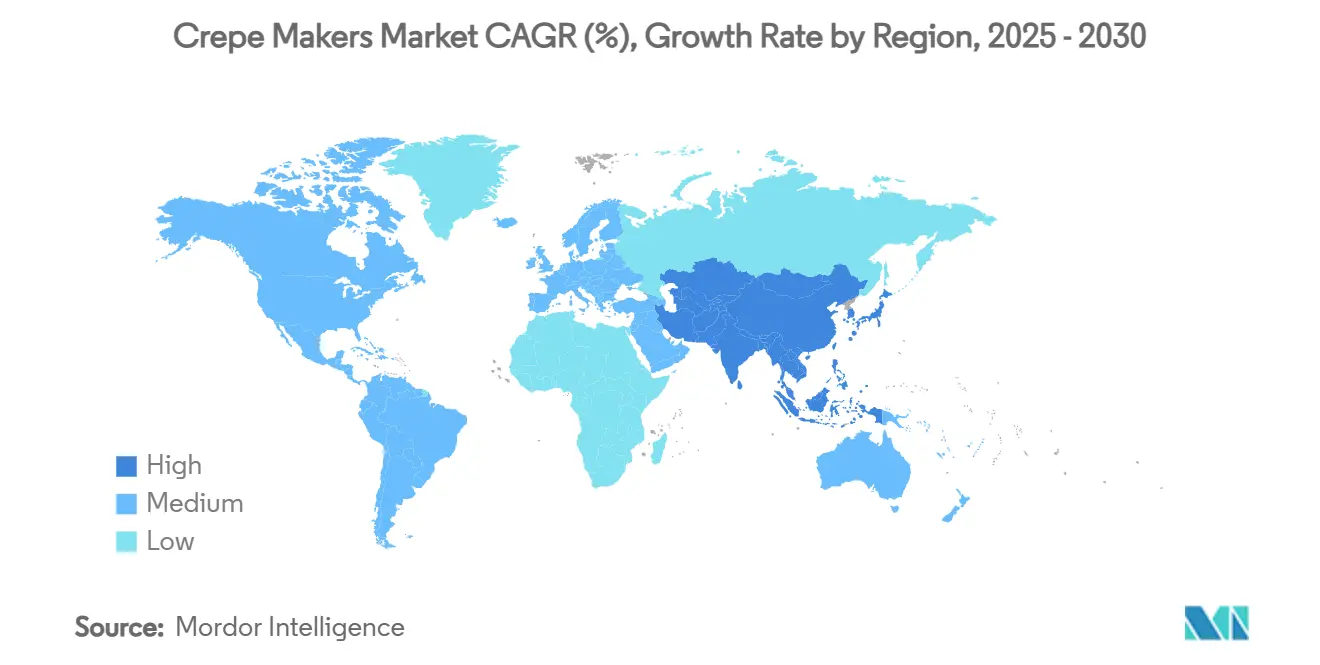

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Crepe Makers Market Analysis by Mordor Intelligence

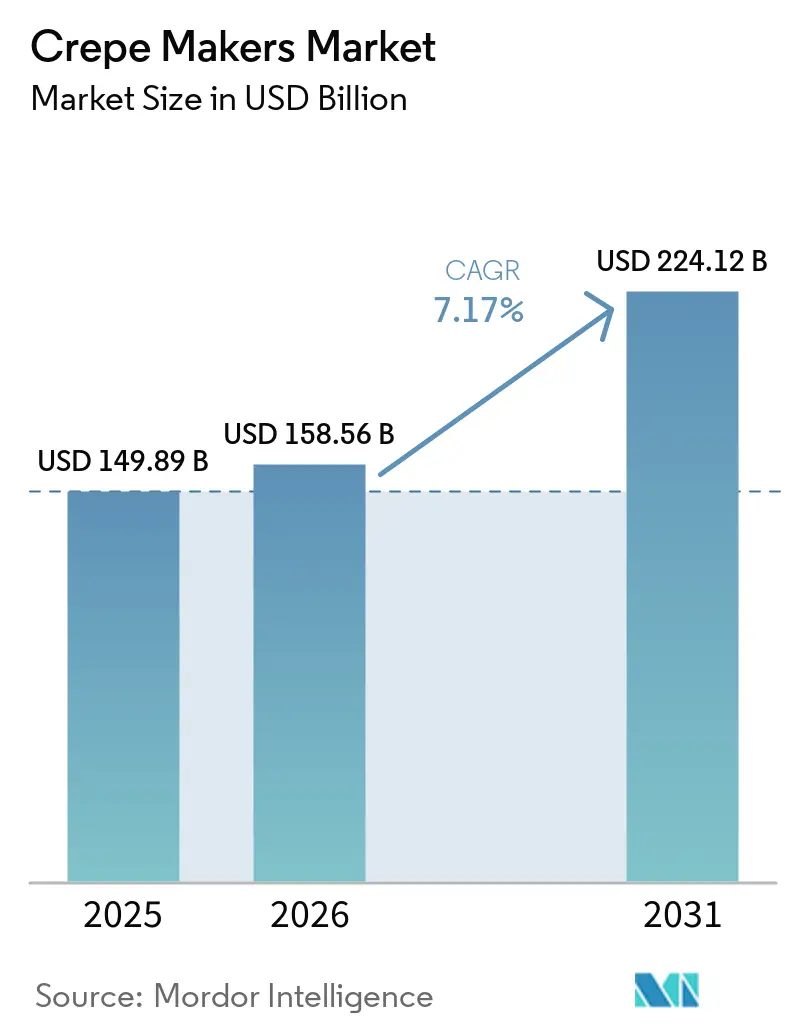

The crepe makers market size is projected to be USD 149.89 million in 2025, USD 158.56 million in 2026, and reach USD 224.12 million by 2031, growing at a CAGR of 7.17% from 2026 to 2031. Demand in the crepe makers market is benefiting from stronger out-of-home dining and a tourism-led rebound in hospitality spending across high-traffic corridors in Asia-Pacific and North America. Policy-driven electrification is also reshaping specifications, with all-electric construction mandates and incentives for induction platforms promoting a shift toward efficient, compliant equipment. Parallel regulatory pressure on PFAS in cookware is compressing product lifecycles and driving adoption of PFAS-free plates and coatings, steering product development and procurement priorities. Finally, digital procurement and embedded financing are expanding the assortment and accelerating purchase decisions, thereby increasing online contribution to the crepe makers market.

Key Report Takeaways

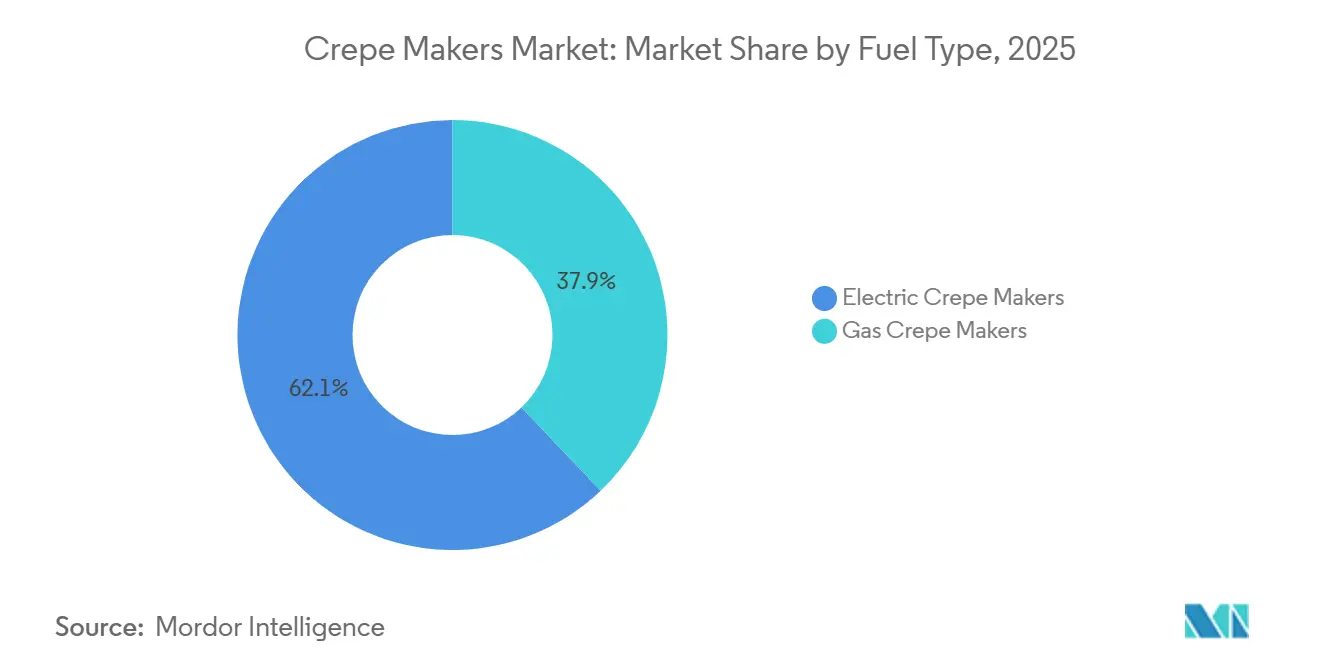

- By fuel type, electric led with 62.11% of the crepe makers market share in 2025 in the crepe makers market, and it is the fastest growing at a 7.56% CAGR through 2031.

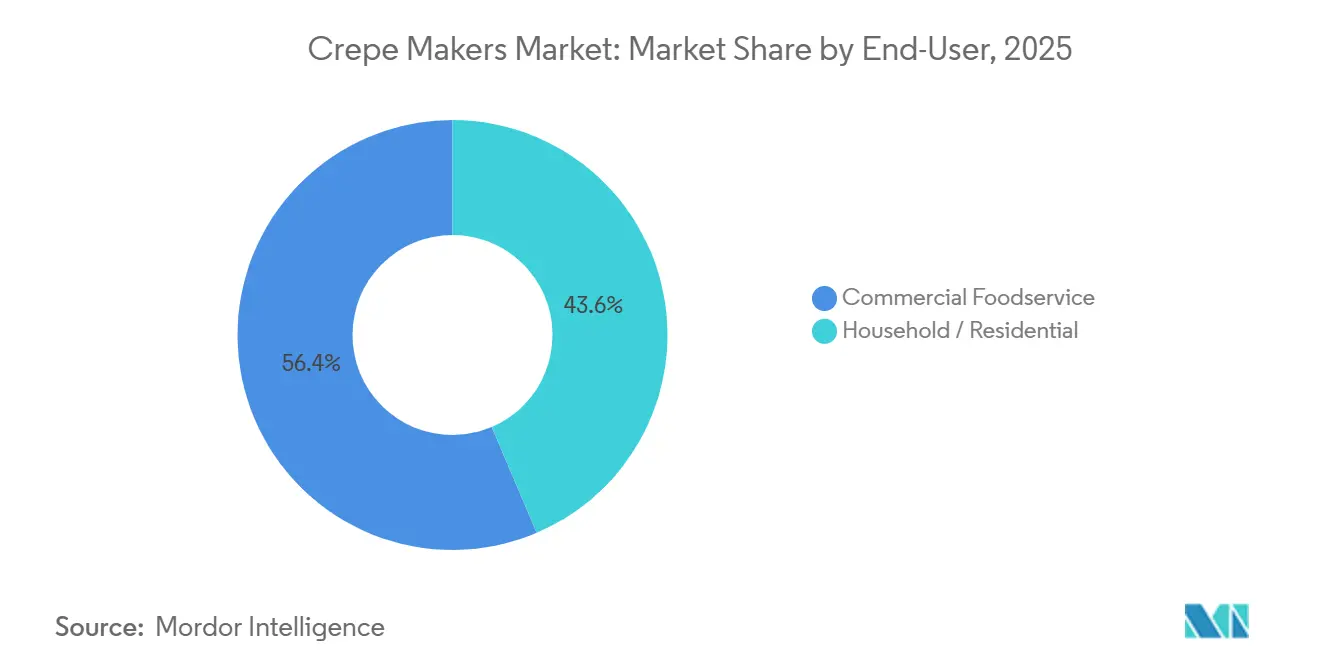

- By end-user, commercial foodservice held 56.41% share in 2025 in the crepe makers market, while household and residential is projected to expand at a 7.94% CAGR through 2031.

- By plate diameter, the 14–16-inch category captured 44.32% share in 2025 and is expected to grow at a 7.29% CAGR to 2031 in the crepe makers market.

- By automation level, manual countertop units dominated with 61.11% share in 2025 in the crepe makers market, while fully-automatic continuous lines are advancing at a 7.83% CAGR through 2031.

- By distribution channel, offline retail accounted for 55.43% share in 2025 in the crepe makers market, while online channels are growing the fastest at a 9.44% CAGR through 2031.

- By geography, North America accounted for 38.81% of 2025 revenue in the crepe makers market, and Asia-Pacific is projected to be the fastest-growing region at a 7.69% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Crepe Makers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Out-of-home dining and restaurant sales expansion | +1.8% | Global, strongest in Asia-Pacific and North America urban corridors | Medium term (2-4 years) |

| Tourism recovery is boosting cafés, street kiosks, and event catering | +1.2% | Global, most pronounced in Southeast Asia, the Mediterranean, and North America, resort markets | Short term (≤ 2 years) |

| Shift toward energy-efficient, connected commercial cooking equipment | +1.5% | North America and the European Union regulatory zones, spillover to the Asia-Pacific metro areas | Medium term (2-4 years) |

| E-commerce penetration in small kitchen appliances | +0.9% | Global, led by North America and Asia-Pacific digital-first markets | Short term (≤ 2 years) |

| Building-electrification policies nudging operators toward electric models | +1.3% | National in NY and CA, selected European Union markets, and city-level mandates are expanding. | Long term (≥ 4 years) |

| PFAS scrutiny is accelerating the shift to cast iron and ceramic plates | +0.5% | United States state-level regimes, Denmark, and parts of the European Union are in scope. | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Out-Of-Home Dining and Restaurant Sales Expansion

Restaurant sales growth and chain expansion are driving increased demand for back-of-house equipment that directly supports batter-based dessert and snack formats. Southeast Asia foodservice market revenue is projected to increase from USD 223.8 billion in 2025 to USD 416.37 billion by 2030, at a 13.2% CAGR, which is a strong backdrop for new café openings and kiosk rollouts that depend on compact, quick-heating equipment[1]QSR Magazine Staff, “Global Expansion Plans at Leading QSR Chains,” QSR Magazine, qsrmagazine.com . McDonald’s plans to add about 10,000 locations globally by 2027, with over one-third in China, which signals sustained kitchen buildouts and replacements that extend to specialty appliances. Starbucks added hundreds of net new stores in fiscal 2025 and is guiding continued unit growth in 2026, reinforcing the pipeline for equipment procurement aligned to breakfast and snack dayparts. As operators standardize menus and drive throughput, they adopt dedicated platforms that deliver consistent output at speed, supporting upgrades in the crepe maker market. Unit growth and menu innovation, especially in urban corridors with high footfall, are translating into multi-station purchases and fleet refreshes as part of broader kitchen optimization strategies.

Tourism Recovery Boosting Cafés, Street Kiosks, and Event Catering Equipment Purchases

Tourism recovery has improved hotel food and beverage performance and boosted street-kiosk activity, adding momentum to equipment orders in hospitality micro-sites. In Southeast Asia, international visitor spending on food and beverages rose by 180% from 2022 to 2024, while hotels reported 40-50% increases in food and beverage revenue per available room, encouraging the procurement of compact, durable cooking platforms. Malaysia’s MyKiosk program formalized street vending, with strong adoption across successive waves, giving vendors access to standardized, power-ready footprints that fit portable induction-based cooking. Operators in these settings seek rapid setup and teardown cycles and consistent heating performance across long service windows, which directs attention to mid-sized, easy-to-clean units. The combination of tourism-led footfall and formalized micro-retail formats supports repeat procurement in the crepe makers market as concepts replicate across high-traffic sites. As hotel and event volumes normalize, equipment fleets are being refreshed to align with higher occupancy and diversified menu offerings in cafés and kiosks.

Shift Toward Energy-Efficient, Connected Commercial Cooking Equipment

Efficiency and connectivity are becoming central to purchasing decisions in professional kitchens. Induction platforms convert energy at about 90% efficiency, compared with 40% for gas, reducing energy costs by more than one-third while keeping kitchens cooler. Policy incentives provide a fiscal pull, including a 30% tax credit of up to USD 5,000 per induction unit under the Inflation Reduction Act’s Section 25C, which shortens payback periods for electric upgrades. Financial capacity is also supportive, as equipment financing volumes remained strong into 2026, with broad credit approval rates, making it easier for operators to fund technology-forward equipment. Approval rates for equipment lending vary by lender type and remain favorable for both specialty and online lenders, accelerating the adoption of energy-efficient and connected appliances. On the product side, Miele’s M Sense intelligent cookware uses embedded sensors to communicate with induction hobs. At the same time, Samsung’s SmartThings Energy can reduce power consumption when AI Energy Mode is activated, which shows how hardware and software are converging. These factors are shaping specifications for the crepe makers market, where electric and sensor-equipped models align with compliance and operational targets.

Building-Electrification Policies Nudging Operators Toward Electric Crepe Makers

Regulatory momentum in North America is moving commercial kitchens toward electric infrastructure, and operators are aligning procurement to future-proof against tightening codes. New York State’s All-Electric Buildings Act prohibits fossil-fuel systems in new commercial buildings under 7 stories beginning January 1, 2026, which directly affects cooking equipment choices in new builds. California’s energy code changes for 2025 take effect in 2026 and push for electric-ready kitchens, which increases the appeal of induction platforms in new projects and major renovations. At the local level, dozens of U.S. cities have enacted measures that restrict or phase out gas hookups in commercial buildings, raising the risk of stranded assets for gas-only appliances. In parallel, jurisdictions like Los Angeles and San Francisco tie restaurant emissions to compliance obligations and penalties, which strengthens the case for electric equipment upgrades. Operators also need to align with safety and code frameworks for ventless and recirculating systems, including UL 710B and NFPA 96, which favor compliant electric models with certified filtration. These requirements are tilting the total cost of ownership in favor of electric units in the crepe makers market as operators plan long-lived equipment investments.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront CAPEX and financing hurdles for SMB operators | -1.4% | Global, acute in emerging Asia-Pacific and Latin America | Medium term (2-4 years) |

| Nonstick and PFAS transition increasing BOM and compliance costs | -0.7% | United States state-level regimes and European Union-influenced markets | Medium term (2-4 years) |

| Heat uniformity and serviceability pain points in lower-tier models | -0.3% | Global, concentrated in budget equipment tiers | Short term (≤ 2 years) |

| Competition from multifunction griddles and flat-tops | -0.5% | Global, strongest in North America commercial kitchens, and the emerging Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX And Financing Hurdles for SMB Operators

Capital intensity and lender selectivity can slow replacement cycles for specialized cooking platforms. Many small firms reported seeking financing in 2025, but fewer than half received full approval, which constrained the ability to purchase non-essential appliances on short timelines[2]GoFoodservice, “Restaurant Financing and Profitability Benchmarks,” GoFoodservice, gofoodservice.com . Approval rates vary across lender types, with online and captive finance channels typically more accommodating. Yet underwriting remains tighter than before, pushing some operators toward leasing rather than buying. Restaurants operate on thin pre-tax margins, and equipment purchases must align with revenue cycles and cash availability, which elongates decision windows for single-purpose units. Where approvals are clear, interest costs and required equity injections influence the choice between manual and automated models, as operators optimize for near-term cash flow. These financing dynamics moderate the pace of upgrades in the crepe maker market, despite strong product interest driven by energy savings and regulatory compliance.

Competition From Multifunction Griddles, Flat-Tops, And Pans

Multi-use griddles and flat-tops deliver high utilization across dayparts, which competes for the same counter space and budgets as dedicated crepe makers. A 36-inch gas flat-top griddle can cost USD 1,500 to USD 3,500, and it supports breakfast and lunch volumes across several menu items within a compact footprint. As smart cookware gains features such as sensor feedback and automated power regulation, the performance gap with dedicated appliances narrows in lower-volume contexts, which raises substitution pressure. Delivery-led formats and small kitchens often favor modular platforms that pivot between concepts without reconfiguration, which strengthens the value proposition of multifunction surfaces. Dedicated crepe makers retain an advantage in consistency and speed at high volumes. Yet, the budget-sensitive end of the market will continue to evaluate griddles and pans that fulfill multiple tasks with a single purchase. This substitution effect persists across both commercial and residential buyers and steadily drags on the crepe makers' market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fuel Type: Electric Dominance Accelerates Amid Policy Tailwinds

Electric crepe makers captured 62.11% of the crepe maker market share in 2025 and are projected to expand at a 7.56% CAGR through 2031, the fastest growth among fuel segments. Electrification codes in North America and select European markets are nudging new builds toward induction-ready installations, which raises the long-term risk of stranded gas-only assets. City-level measures to limit new gas hookups and municipal emissions targets add to the structural shift toward electric equipment. Operators also see labor benefits from cooler kitchens and precise temperature control, which are additional advantages of induction platforms. Incentives like a 30% tax credit of up to USD 5,000 per induction unit under Section 25C further improve the payback math for electric models in the crepe maker market.

Gas units still serve operators who value familiarity and instant heat or who operate in regions with established gas infrastructure and fewer near-term policy constraints. That said, more localities are curbing gas supply to commercial buildings, compressing the future addressable base for gas-only platforms over new-construction cycles. Where local energy prices remain stable and policy risk is low, gas equipment may persist until replacement windows align with broader electrification plans. Over the forecast, momentum remains with electric as the compliance, efficiency, and financing vectors align on a single trajectory, which supports higher attachment of connected features as well.

By Plate Diameter: Mid-Size Range Balances Output And Footprint

The 14–16-inch segment captured 44.32% of the crepe maker market in 2025 and is projected to grow at a 7.29% CAGR through 2031, reflecting a balance of throughput and counter space for cafés and kiosks. Mid-diameter platforms can exceed 60 crepes per hour in compact footprints, as seen with new dual-surface designs featuring embedded heating elements and programmable controls. These units also align with standardized kiosk formats and small kitchens that prioritize speed, consistency, and simple cleaning routines. As self-service front-of-house technologies scale, operators often mirror that efficiency with mid-sized, high-output equipment behind the counter. This segment is well-positioned for replacement and new-unit demand in the crepe maker market as urban footprints tighten.

Plates of ≤13 inches skew toward residential use and micro-operators that value portability over maximum throughput. They integrate well with portable induction hobs and smaller power budgets, which suits pop-ups and seasonal stands. At the other end, ≥ 17-inch plates and double or industrial models target high-volume settings, including commissaries and catering fleets. These units often pair with automation features and battery dispensing to stabilize yields, though higher CAPEX confines adoption to well-capitalized operators. Over time, chain standardization and commissary models should increase demand for larger formats where labor and consistency are the binding constraints.

By Automation Level: Manual Units Prevail, Automation Gains As Labor Costs Escalate

Manual countertop units dominated with a 61.11% share in 2025, as buyers value low acquisition costs, straightforward operation, and minimal training requirements. Their price points align with those of small cafés and mobile vendors, and they fit power and space constraints without complex installations. Financing approvals for lower-ticket units remain favorable across specialty and online lending channels, supporting steady replacement cycles. Semi-automatic systems reduce operator fatigue and increase portion consistency for mid-volume sites, and they bridge the gap between manual craft and full automation. These dynamics sustain a large installed base of manual units in the crepe makers market, even as automation gains traction.

Fully-automatic continuous lines, while holding a smaller base today, are projected to grow at a 7.83% CAGR through 2031 as robotics and AI reach commercial readiness. Miso Robotics’ automated frying systems show how back-of-house robotics can double human throughput, compress installation time, and deliver multi-shift reliability. Robotics-as-a-Service models that price automation monthly rather than through upfront CAPEX are also widening access for chain operators and high-throughput sites. CES showcases and field pilots suggest sensor-rich, connected systems are transitioning from trials to scaled deployment in specific prep tasks. As labor costs continue to rise in 2026, automated production lines become increasingly compelling for commissaries and delivery-led operations seeking 24/7 uptime.

By End-User: Commercial Segment Dominant, Residential Surging Post-Pandemic

Commercial foodservice accounted for 56.41% of the crepe maker market in 2025, supported by chain expansion, café density, and event-driven volumes in hospitality corridors. Southeast Asia’s foodservice market is on a double-digit growth path through 2030, and large chains continue to invest in new stores, which is positive for back-of-house procurement. McDonald’s has outlined plans to add around 10,000 locations globally by 2027, with a major push in China’s lower-tier cities, which drives standardized equipment rollouts. Starbucks maintained net new openings in fiscal 2025 and plans continued expansion in 2026, which sustains steady demand for compact, high-output platforms. Tourism and hotel F&B recovery also adds to the purchasing base for kiosks and cafés that rely on fast-heating, durable units.

Household and residential buyers held 43.59% share in 2025 and are projected to grow at a 7.94% CAGR through 2031, the fastest among end users. E-commerce and embedded financing expand access, including BNPL and online equipment loans that reduce entry barriers for specialty appliances. Smart kitchen adoption is rising, with Miele’s sensor-integrated cookware and Samsung’s AI-enabled appliances showing how software improves temperature control and energy profiles at home. Consumer interest in PFAS-free cookware is influencing material choices, and brands communicate testing protocols to lower perceived risk. Residential buyers favor easy-to-store manual units with clean aesthetics and predictable heat, which supports steady attachment to countertop appliance ecosystems in the crepe makers market.

By Distribution Channel: Offline Prevails, Online Surges in Digital Procurement and Financing

Offline retail and dealer networks captured 55.43% share in 2025, supported by hands-on product evaluation, installation support, and the ability to negotiate service. Physical stores also enable demonstrations that showcase heat uniformity and non-stick performance, which remain critical differentiators. Dealers add layout and utility planning and coordinate training, which helps smaller operators who lack in-house technical expertise.

Online channels held 44.57% share in 2025 and are advancing at a 9.44% CAGR through 2031, the fastest among channels in the crepe makers market. Embedded financing and BNPL expand affordability, while high approval rates in online lending reduce friction at checkout. Marketplaces aggregate inventory, improve price transparency, and speed up procurement cycles, which suits younger, digital-first operators. Delivery-led formats and ghost kitchens often source equipment online to compress opening timelines and compare multi-vendor offers in a single session. Online B2B portals also support larger ticket orders for front-of-house technologies like self-service kiosks, which are increasingly paired with streamlined back-of-house equipment.

Geography Analysis

North America accounted for 38.81% of the crepe maker market in 2025, supported by a mature foodservice infrastructure, regulatory support for electrification, and high consumer spending on dining. New York’s All-Electric Buildings Act compels a shift to electric in new projects starting in 2026, which elevates the case for induction-based cooking platforms [3]. City-level measures further restrict new gas connections and push operators toward electric-ready kitchens over new build cycles. PFAS regulations at the state level, including disclosure and labeling mandates, are compressing timelines for cookware transitions and driving the adoption of PFAS-free materials. Financing conditions remained constructive into 2026, though underwriting discipline has increased, which extends closing times for some borrowers. Operators expect labor costs to continue rising in 2026, which boosts interest in automation and energy-efficient equipment to protect margins. These factors support steady procurement in the crepe makers market, with a tilt toward electric and connected models that align with compliance and cost goals.

Asia-Pacific is projected to be the fastest-growing region, with a 7.69% CAGR through 2031, driven by QSR proliferation, café density, and expanding middle-class spending. Southeast Asia’s foodservice market is set to grow from USD 223.8 billion in 2025 to USD 416.37 billion in 2030 at a 13.2% CAGR, which signals a multi-year pipeline for compact, high-output cooking equipment in cafés and kiosks. McDonald’s expansion plans through 2027, with a strong China focus, will support steady back-of-house investment in standardized equipment. Starbucks continues to invest across Asia, which sustains demand for breakfast and snack formats that fit crepe maker use cases. Malaysia’s MyKiosk program saw strong take-up across successive rounds, reinforcing the role of formalized micro-retail in equipment demand. As digital payments and delivery platforms remain embedded across Asia-Pacific metro areas, equipment needs align with the rapid service and compact footprints of the crepe maker market.

Europe shows steady growth, supported by premium manufacturing clusters, energy-efficiency priorities, and café culture in urban centers and tourism corridors. European suppliers emphasize durable construction and connected features, which align with higher energy prices and sustainability targets. Product stewardship and recycling initiatives are expanding, as seen in cookware recycling programs that can extend to adjacent categories over time. Mediterranean tourism supports café and dessert formats, while Northern Europe’s sustainability focus encourages the adoption of energy-efficient, PFAS-free models. Beyond Europe, South America, the Middle East, and Africa, smaller bases exist with room for growth as formalized foodservice and tourism infrastructure expand. However, supply chains and financing conditions vary widely by market. Overall, the crepe makers market benefits from policy, product, and channel shifts that favor efficient, compliant platforms across regions.

Competitive Landscape

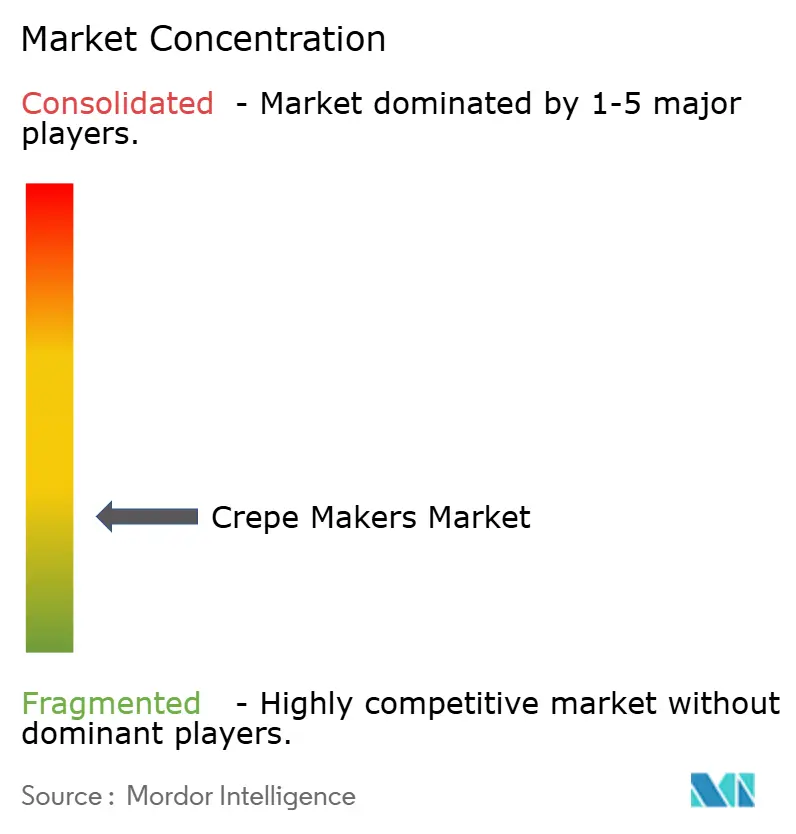

The crepe maker market remains fragmented, with the top five suppliers accounting for less than half the market share in 2025, reflecting diverse use cases from residential countertop appliances to industrial continuous lines. Tier-one foodservice groups are refining their portfolios to focus on commercial domains, as shown by Ali Group’s March 2026 acquisition of Bunn Commercial LP, which broadened their beverage equipment capabilities[4]Ali Group Press Office, “Ali Group Acquires Bunn Commercial LP,” Ali Group, aligroup.com . Middleby’s sale of a 51% stake in its Residential Kitchen business in February 2026 highlighted a pivot toward pure-play commercial foodservice. Groupe SEB, parent of Krampouz and Tefal, reported 2025 revenue of EUR 8,169 million and continued investing in sustainability programs and reconditioning capacity that can influence product roadmaps. These strategic shifts indicate that scale players are realigning resources toward automation, IoT, and circular-economy initiatives that can shape specialty categories over time.

Product differentiation centers on PFAS-free plates, induction heat distribution, and connectivity for predictive maintenance. Waring’s XPress multipurpose platform demonstrated high output in compact form factors and won an industry innovation award, signaling ongoing improvements in cycle times and consistency. Robotics innovators secured funding to scale production and deployment across airports, hospitals, and institutional settings, which aligns with kitchens where uniformity and uptime are critical. These developments raise performance expectations across the crepe makers market, including mid-diameter and manual units that form the core of demand. Niche suppliers are also finding white space in mobile foodservice and modular kiosk solutions, where durable, plug-and-play induction designs meet power and space constraints.

Technology is now a strategic lever for competitive advantage. Miele’s sensor-integrated cookware and Samsung’s AI-driven energy features show how vendors are turning hardware into data-rich systems that support quality control and cost management. Portfolio moves, including Groupe SEB's equipment brand acquisitions and facility investments, support the cross-pollination of design, materials, and service models. As operators seek turnkey bundles that package hardware with financing and service, suppliers that combine connected platforms, credible sustainability claims, and responsive support are better positioned to win share in the crepe makers market.

Crepe Makers Industry Leaders

Krampouz

Roller Grill / Equipex (Sodir)

Bartscher

Tefal (Groupe SEB)

Waring Commercial

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Ali Group completed the acquisition of Bunn Commercial LP to strengthen leadership in dispensed beverage systems across North America and other core regions.

- February 2026: Middleby Corporation sold a 51% stake in its Residential Kitchen business to 26North Partners, shifting strategic focus toward commercial foodservice.

- November 2025: Appetronix closed more than USD 10 million in seed funding to scale robotic kitchens for airports, hospitals, entertainment venues, universities, and offices with a Robotics-as-a-Service model.

- March 2025: Chef Robotics announced USD 43.1 million in Series A funding to expand AI-enabled meal assembly and accelerate RaaS deployments.

Global Crepe Makers Market Report Scope

Crepe makers are specialized appliances designed to spread batter evenly and cook thin, delicate crepes efficiently. Unlike standard pans, these devices provide a dedicated, flat cooking surface optimized for consistent heat distribution to meet both everyday and high-volume culinary demands. The crepe maker market is segmented by fuel type, plate diameter, automation level, end-user, distribution channel, and geography. By fuel type, the market is segmented into electric crepe makers and gas crepe makers. By plate diameter, the market is segmented into ≤ 13 inch, 14 – 16 inch, and ≥ 17 inch (double & industrial). By automation level, the market is segmented into manual countertop units, semi-automatic rotary machines, and fully-automatic continuous lines. By end-user, the market is segmented into commercial foodservice and household / residential. By distribution channel, the market is segmented into offline retail (specialty stores, hypermarkets, dealer networks) and online retail (brand e-stores, marketplaces, B2B portals). By geography, the market is segmented into North America, South America, Asia-Pacific, Europe, the Middle East, and Africa. The report offers the market size in value terms in USD for all the above-mentioned segments.

| Electric Crepe Makers |

| Gas Crepe Makers |

| ≤ 13 inch |

| 14 – 16 inch |

| ≥ 17 inch (Double & Industrial) |

| Manual Countertop Units |

| Semi-automatic Rotary Machines |

| Fully-automatic Continuous Lines |

| Commercial Foodservice |

| Household / Residential |

| Offline Retail (Specialty Stores, Hypermarkets, Dealer Networks) |

| Online Retail (Brand E-stores, Marketplaces, B2B Portals) |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia Pacific | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Fuel Type | Electric Crepe Makers | |

| Gas Crepe Makers | ||

| By Plate Diameter | ≤ 13 inch | |

| 14 – 16 inch | ||

| ≥ 17 inch (Double & Industrial) | ||

| By Automation Level | Manual Countertop Units | |

| Semi-automatic Rotary Machines | ||

| Fully-automatic Continuous Lines | ||

| By End-User | Commercial Foodservice | |

| Household / Residential | ||

| By Distribution Channel | Offline Retail (Specialty Stores, Hypermarkets, Dealer Networks) | |

| Online Retail (Brand E-stores, Marketplaces, B2B Portals) | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | ||

| Rest of Asia Pacific | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the crepe maker market growth outlook to 2031?

The crepe makers market size is expected to rise from USD 158.56 million in 2026 to USD 224.12 million by 2031, reflecting a 7.17% CAGR over 2026-2031.

Which fuel type leads demand in the crepe makers market?

Electric crepe makers lead with 62.11% share in 2025 and post the fastest growth at a 7.56% CAGR through 2031, supported by electrification policies and energy savings.

Which end-user is growing the fastest in the crepe makers market?

Household and residential buyers show the fastest growth at a 7.94% CAGR to 2031, while commercial foodservice remains the largest base with 56.41% share in 2025.

What plate diameter is most preferred by operators?

The 14–16-inch category captured 44.32% share in 2025 and is growing at a 7.29% CAGR, balancing output with counter space for cafés and kiosks.

Which region will expand the fastest in the crepe makers market?

Asia-Pacific is projected to grow at a 7.69% CAGR through 2031, driven by QSR expansion, café density, and rising middle-class spending.

How will online channels affect equipment buying behavior?

Online channels are advancing at a 9.44% CAGR through 2031 as embedded financing, faster approvals, and a broad assortment simplify procurement for both SMBs and chains.

Page last updated on: