Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

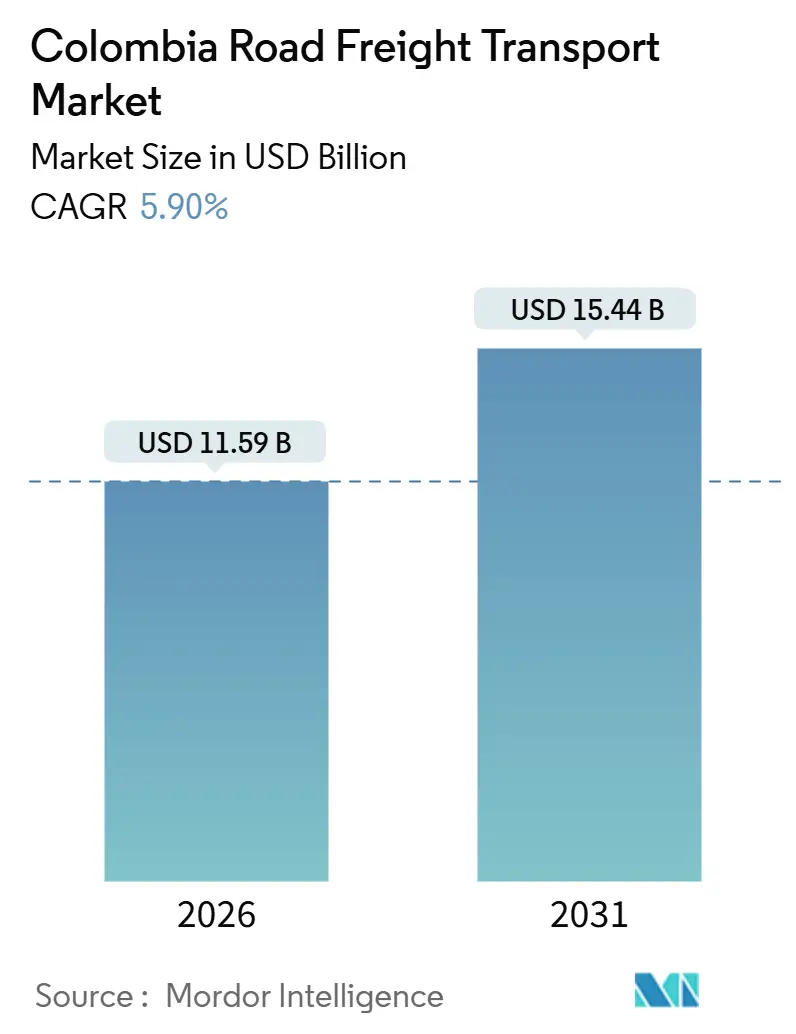

| Market Size (2026) | USD 11.59 Billion |

| Market Size (2031) | USD 15.44 Billion |

| Growth Rate (2026 - 2031) | 5.90% CAGR |

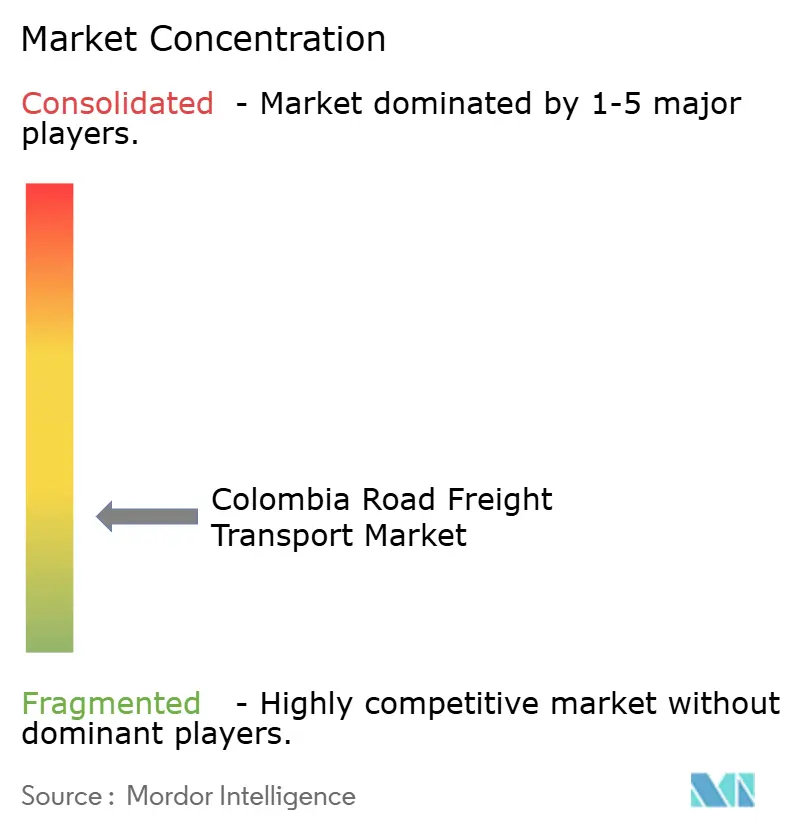

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Colombia Road Freight Transport Market Analysis by Mordor Intelligence

The Colombia Road Freight Transport Market size is estimated at USD 11.59 billion in 2026, and is expected to reach USD 15.44 billion by 2031, at a CAGR of 5.90% during the forecast period (2026-2031).

The trajectory captures Colombia’s role as a logistics bridge between Pacific and Caribbean trade lanes, while chronic cost friction, 18% of shipment value versus the 8% OECD benchmark, continues to erode margins. Capacity upgrades under the 4G highway program have trimmed trunk-route travel times, yet unpaved rural roads, high diesel prices, and an aging truck fleet keep operating costs elevated. Growth catalysts include nearshoring-led manufacturing relocation, a more than 10-fold rise in parcel volumes since 2010, which is reshaping the less-than-truckload (LTL) arena, and a wave of foreign direct investment in free-trade-zone (FTZ) warehousing. Competitive differentiation now hinges on digital control towers, electric-truck pilots, and bonded storage footprints, even as policy uncertainty and cargo theft constrain short-term confidence. Despite these headwinds, sustained export demand for coal, crude, and perishables keeps long-haul lanes busy, underpinning the revenue outlook of the Colombia road freight transport market.

Key Report Takeaways

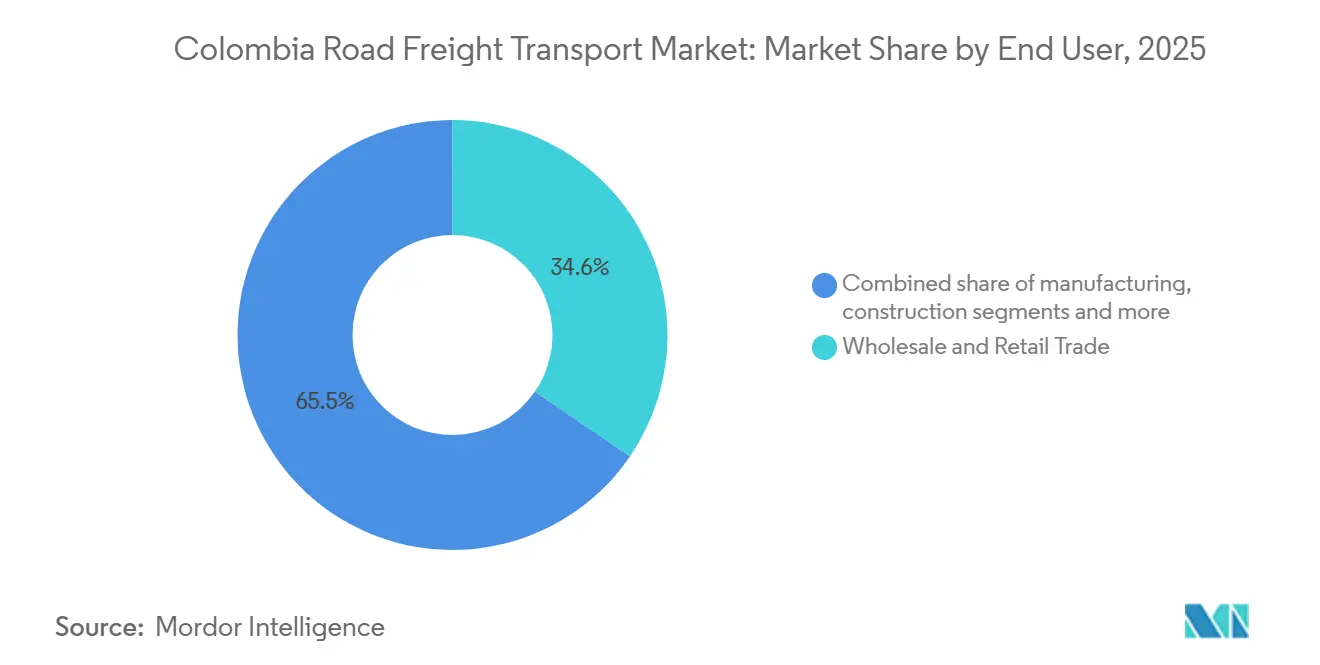

- By end user, wholesale & retail trade led with a 34.55% share of Colombia's road freight transport market in 2025, while also delivering the fastest growth of 6.34% CAGR through 2031.

- By destination, domestic freight controlled 63.57% of tonnage in 2025; international flows are on track for the highest 6.87% CAGR to 2031.

- By truckload specification, full truckload captured 77.65% of Colombia road freight transport market share in 2025, whereas less-than-truckload is forecast to expand at a 6.65% CAGR to 2031.

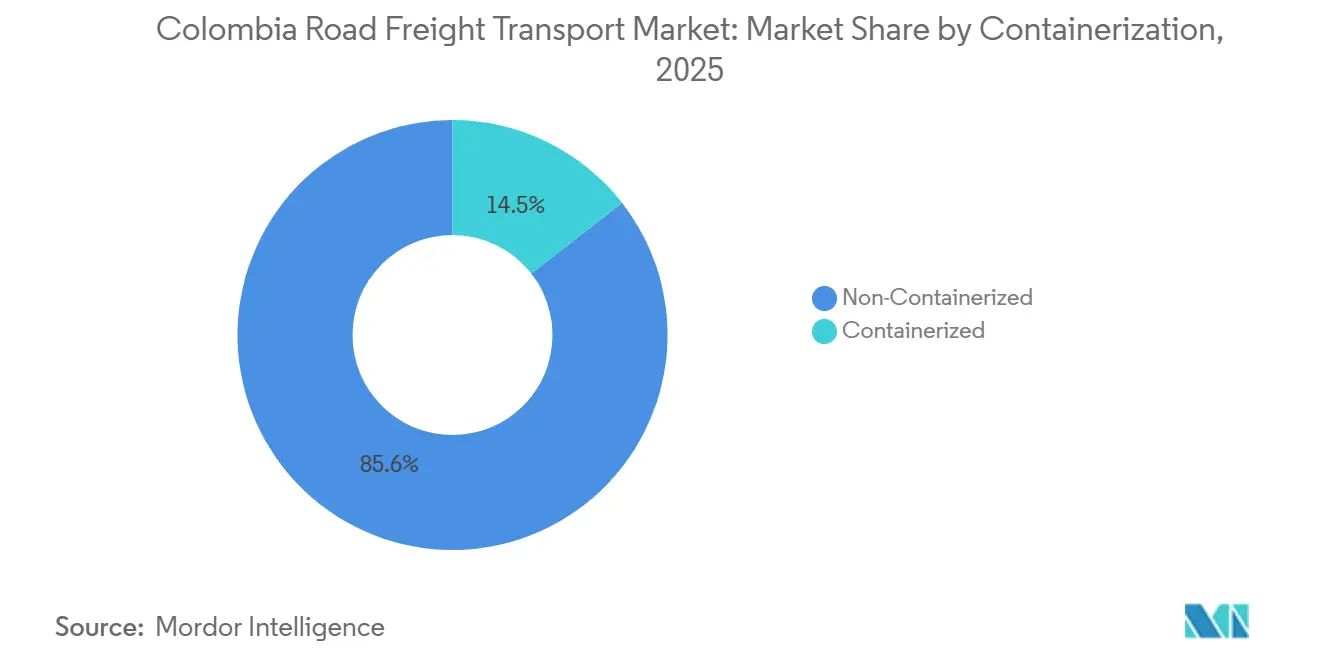

- By containerization, non-containerized cargo dominated with 85.55% of 2025 volume, while Colombia road freight transport market size for containerized freight is projected to grow at 6.03% CAGR between 2026 and 2031.

- By distance, long-haul moves held 74.62% of tonne-kilometers and are set to post a 6.21% CAGR, outpacing short-haul expansion.

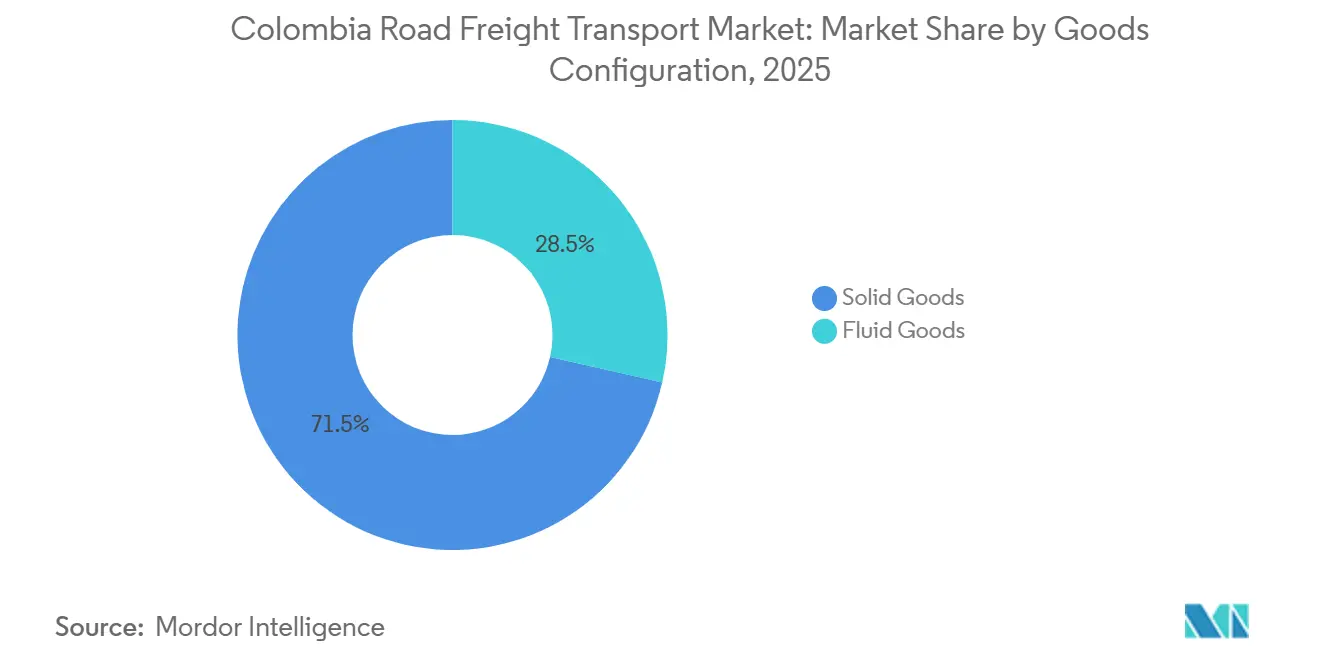

- By goods configuration, solid goods accounted for 71.46% of freight in 2025, but fluid-goods volumes will grow at a 6.37% pace as domestic refinery output climbs.

- By temperature control, non-temperature freight made up 94.55% of loads in 2025; temperature-controlled logistics is projected to advance at a 6.52% CAGR, led by pharmaceuticals and floriculture.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Colombia Road Freight Transport Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated 4G/5G Highway Programme | +1.2% | National, with early gains in Bogotá-Buenaventura, Magdalena corridors | Medium term (2-4 years) |

| E-commerce Boom Raises LTL Demand | +1.4% | Urban centers - Bogotá, Medellín, Cali, Barranquilla | Short term (≤ 2 years) |

| Manufacturing-sector Output Expansion | +0.9% | Andean industrial belt, Caribbean coastal zones | Medium term (2-4 years) |

| Truck-fleet Modernisation Incentives | +0.8% | National, prioritizing Bogotá, Antioquia fleets | Long term (≥ 4 years) |

| Automatic Axle-load Enforcement (e-scales) | +0.6% | Toll plazas on 4G corridors, gradual rural rollout | Medium term (2-4 years) |

| Free-trade-zone Warehousing Surge | +1.1% | Bogotá (30 FTZs), Cartagena, Barranquilla, Cali | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerated 4G/5G Highway Programme

Nearly 90% completion of 4G concessions in 2025 delivered more than 5,000 km of dual-carriageways that halved transit times on Bogotá–Buenaventura and Magdalena routes[1]Inter-American Development Bank, “4G Highway Progress,” iadb.org. The USD 2 billion Magdalena Trunk project, now funded and due by 2027, will open direct export pathways for Tolima and Huila growers. Progress toward next-generation 5G concessions has stalled because land-acquisition disputes have frozen USD 4.6 billion in works, delaying critical feeder links. A 2023 toll freeze also left operators with a USD 203 million revenue gap, forcing contract renegotiations that push completion into 2028-2029. The outcome is a bifurcated network where modern highways funnel trucks into a handful of corridors, intensifying congestion at Buenaventura port during peak coffee season.

E-commerce Boom Raises LTL Demand

Online sales reached 18% of national retail turnover in 2024, multiplying parcel flows and dropping average parcel weight below 5 kg[2]World Bank, “E-commerce Indicators,” worldbank.org. Domestic leaders Coordinadora Mercantil and Servientrega invested in automated sortation hubs that enable same-day delivery inside major cities, while digital freight platforms reduce empty runs by up to 20%. Amazon’s 2024 entry into Medellín and Cali signals rising competition, yet service gaps persist in rural zones where unpaved roads raise last-mile costs by 40%. Urban consolidation centers, therefore, remain the backbone of LTL growth within the Colombia road freight transport market.

Manufacturing-Sector Output Expansion

Colombia’s PMI stayed above the 50-point threshold through late 2025 despite industrial volatility; forward orders for chemicals and plastics remain firm as firms reshore from Asia. FTZs offering a 15% corporate tax rate attract assemblers that cluster warehousing with production, shrinking drayage-to-port distances. Nevertheless, the 2026 fuel-tax plan could lift logistics costs by 8-10%, pressuring producers to lock in full-truckload contracts. Commitments by Bavaria to cut emissions 25% by 2030 also require expanded electric fleets and temperature-controlled capacity, spurring equipment upgrades across the Colombia road freight transport market.

Truck-Fleet Modernization Incentives

An average heavy-duty vehicle age of 18 years undermines fuel efficiency, yet Resolution 5304 and the NAMA program offer subsidies for Euro VI trucks[3]Ministry of Transport, “Fleet Modernization Resolution 5304,” mintransporte.gov.co. Only 4,200 units were scrapped in 2024 versus a 10,000-unit target, highlighting financing barriers for small carriers. Bogotá pilots with 22 electric rigs proved 35% cheaper per kilometer than diesel units, but scarce charging outside cities limits wider deployment. Large shippers increasingly reward compliant fleets with premium contracts, nudging market consolidation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 94% Rural Roads Unpaved | -1.30% | Rural municipalities, Orinoquía, Amazonía, Pacific coast | Long term (≥ 4 years) |

| Ageing Heavy-duty Vehicle Fleet | -0.90% | National, concentrated in small-operator fleets | Medium term (2-4 years) |

| High Cargo-theft Incidence on Trunk Roads | -0.70% | Cauca, Nariño, Norte de Santander, Arauca corridors | Short term (≤ 2 years) |

| PPP Build-out Delays (permits/land) | -1.00% | Meta, Casanare, Chocó, secondary-road networks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

94% Rural Roads Unpaved

Just 21% of Colombia’s 204,855 km network is paved, leaving producers in coffee-growing Caldas and Quindío to rely on small all-terrain trucks that carry 40% less payload and double per-kilometer costs. The logistics performance index ranks Colombia 86th worldwide, in part because rainy-season closures isolate farms for days. Although USD 1.2 billion is earmarked for rural upgrades, land-tenure disputes have postponed 60% of projects, perpetuating two-tier freight service inside the Colombia road freight transport market.

Ageing Heavy-Duty Vehicle Fleet

More than one-third of trucks predate 2005 emissions rules, burning 25% more fuel than Euro VI models. Mandatory scrappage by 2028 faces funding gaps for owner-operators, who already endure 12-15% downtime. Diesel subsidy removal slated for 2026 will widen cost disparities, accelerating the shift of premium cargo to better-capitalized carriers and reshaping competition in the Colombia road freight transport market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End User: Retail Drives Parcel Density

Wholesale & Retail Trade generated the largest 34.55% slice of the Colombia road freight transport market share in 2025, and this segment is forecast to grow at a 6.34% CAGR to 2031 as online retail prompts network densification. The Colombia road freight transport market size attributed to retail freight is poised to surpass USD 5 billion by 2031. Automation at city hubs has streamlined same-day delivery, though rural service still encounters infrastructure limits.

Agriculture, Fishing & Forestry remains critical, anchored by coffee that represented 7.3% of 2024 exports. Manufacturing volumes are volatile but gain support from FTZ incentives, while Oil & Gas logistics relies on heavy tanker fleets to move crude and refined products. Construction freight should rebound once PPP road sites restart, lifting cement and steel demand across the Colombia road freight transport market.

By Destination: Cross-Border Gains Outpace Domestic

Domestic lanes retained 63.57% of 2025 tonnage, yet international flows will advance at a 6.87% CAGR through 2031 as nearshoring accelerates north-bound supply chains. The Colombia road freight transport market size linked to cross-border moves is expected to approach USD 6 billion by 2031.

4G corridor upgrades slash Bogotá–Medellín transit to under five hours, but Pacific-coast congestion drives exporters toward Caribbean ports 400 km farther away. Diesel tax hikes could raise border-crossing costs 8-10%, pushing shippers to bundle volumes in full-truck contracts.

By Truckload Specification: LTL Gains from Digital Aggregation

Full Truckload operations accounted for 77.65% of Colombia road freight transport market share in 2025, fueled by bulk coal and oil traffic[4]DANE, “Foreign Trade Statistics 2024,” dane.gov.co. Less-than-Truckload, however, will grow fastest at 6.65% as platforms match fragmented parcels with available deck space.

Telematics systems cut empty kilometers by up to 20%, while electric vans ensure zero-emission compliance inside Bogotá’s low-emission zones. FTL operators face margin pressure once diesel subsidies vanish, although fleet digitalization can offset part of the impact.

By Containerization: Bulk Dominates, FTZ Boosts Boxes

Non-containerized cargo made up 85.55% of 2025 tonnage, reflecting robust flows of coal, coffee, and crude. Containerized freight, steered by FTZ value-added activities, is forecast to grow 6.03%, adding roughly USD 1 billion to the Colombia road freight transport market size by 2031.

FTZ operators enjoy duty deferment and a 15% corporate tax rate, attracting electronics and pharma firms that demand bonded storage and stable cold-chain links. Land scarcity near Bogotá is driving warehouse expansion toward outer municipalities with lower rents but longer drayage legs.

By Distance: Long Haul Anchored by Export Corridors

Long-haul routes held 74.62% of tonne-kilometers in 2025, buoyed by 500-km-plus hauls from inland mines to Caribbean ports. Coal and crude flows ensure a 6.21% CAGR, while short-haul growth hinges on e-commerce density inside megacities.

Electric-truck pilots remain city-bound owing to limited rapid chargers outside major hubs, yet consumer demand is compelling carriers to hybridize fleets, especially for cold-chain beverages and perishables in the Colombia road freight transport market.

By Goods Configuration: Solid Goods Lead, Fluids Accelerate

Solid goods such as coffee, cement, and steel captured 71.46% of the 2025 volume. Fluid goods, including petroleum derivatives, are set for a 6.37% CAGR on the back of refinery expansions at Cartagena and Barrancabermeja.

Energy shippers deploy Euro VI tanker units with spill-containment technology, but looming diesel price hikes could compress margins. Solid-goods carriers shoulder rural-road deficits that double unit costs versus paved arteries, sustaining the competitive gap within the Colombia road freight transport industry.

By Temperature Control: Cold Chain Expands for Pharma & Produce

Non-temperature freight dominated at 94.55% in 2025, yet temperature-controlled loads will grow 6.52%, powered by USD 1.5 billion in flower exports and stringent pharmaceutical GDP rules. Colombia road freight transport market size for cold chain is projected to top USD 1 billion by 2031.

DHL’s 39-facility network now offers GDP-compliant storage, while Bavaria’s carbon roadmap is driving uptake of electric reefers. Only 15% of rural areas have nearby cold stores, requiring mobile chill units that lift costs 10-15%.

Geography Analysis

Colombia’s Andean axis, Bogotá, Medellín, Cali, handled roughly 65% of domestic tonnage in 2025, leveraging dual-carriageway gains that trimmed trunk travel times. FTZ clusters in Bogotá and Cartagena processed 1.2 million TEUs in 2024, feeding electronics and pharma flows bound for North America.

The Caribbean coast hosts export-heavy lanes for coal and crude that generated 48.5% of 2024 export earnings. Buenaventura on the Pacific manages 60% of container imports, but week-long dwell times push shippers northward, adding cost and distance.

Orinoquía and Amazonía together account for under 10% of freight activity because 94% of roads there remain unpaved, forcing multimodal river or air solutions that inflate rates up to 300%. Rising security provisions along border corridors further complicate operations, yet nearshoring gains in the Andean interior keep the Colombia road freight transport market on an upward trajectory.

Competitive Landscape

Small owner-drivers control 60-65% of the truck fleet, while global integrators secure premium contracts. DHL Supply Chain operates 296,000 m² of GDP-grade cold stores and plans USD 1.3 million in solar and fleet upgrades for 2025[5]DHL Supply Chain, “DHL Colombia Operations,” dhl.com.

Local champion Coordinadora Mercantil leverages automated hubs for same-day delivery, and TCC introduced battery-electric trucks serving micro-fulfillment centers. Organización Corona’s SAP control tower raised filled round trips by 20% and cut demurrage 40%, demonstrating that data-driven routing can boost productivity even in aging fleets.

Security tech and ESG credentials now tip contract awards. Carriers offering GPS geofencing command a 10-15% rate premium on high-risk corridors, while shippers with Scope-3 emissions targets seek partners deploying Euro VI or electric trucks, reshaping the Colombia road freight transport market.

Colombia Road Freight Transport Industry Leaders

Operadores Logisticos De Carga S OPL Carga S.A.S.

Coordinadora Mercantil S.A.

TCC S.A.S.

Transportes Vigia Sociedad Por Acciones Simplificada S.A.S.

Transportes Sanchez Polo S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: DHL Supply Chain has committed USD 1.3 million to enhance point-of-sale infrastructure and install solar panels across its 39 warehouses in Colombia. This initiative aims to boost operational efficiency, reduce energy costs, and promote sustainable logistics in the road freight sector.

- February 2025: TCC recently unveiled an electric-truck fleet dedicated to zero-emission urban freight deliveries in key cities like Bogotá, Medellín, and Cali. This move addresses air quality concerns and supports Colombia's push toward sustainable mobility in densely populated areas.

- December 2024: Transtainer SAS achieved BASC (Business Alliance for Secure Commerce) certification following 3,000 successful operations and 50% year-on-year growth. This prestigious endorsement validates their robust security protocols, vital for international road freight handling of sensitive cargo.

- November 2024: The Inter-American Development Bank (IDB) reports that USD 4.6 billion in public-private partnership (PPP) road projects remain stalled due to permitting delays, pushing 5G highway deadlines to 2029. These bottlenecks hinder freight corridor expansions critical for Colombia's road transport network.

Colombia Road Freight Transport Market Report Scope

By End User

| Agriculture, Fishing & Forestry |

| Construction |

| Manufacturing |

| Oil & Gas, Minning & Quarrying |

| Wholesale & Retail Trade |

| Others |

By Destination

| Domestic |

| International |

By Truckload Specification

| Full Truckload (FTL) |

| Less-than-Truckload (LTL) |

By Containerization

| Containerized |

| Non-Containerized |

By Distance

| Long Haul |

| Short Haul |

By Goods Configuration

| Fluid Goods |

| Solid Goods |

By Temperature Control

| Non-Temperature Controlled |

| Temperature Controlled |

| By End User | Agriculture, Fishing & Forestry |

| Construction | |

| Manufacturing | |

| Oil & Gas, Minning & Quarrying | |

| Wholesale & Retail Trade | |

| Others | |

| By Destination | Domestic |

| International | |

| By Truckload Specification | Full Truckload (FTL) |

| Less-than-Truckload (LTL) | |

| By Containerization | Containerized |

| Non-Containerized | |

| By Distance | Long Haul |

| Short Haul | |

| By Goods Configuration | Fluid Goods |

| Solid Goods | |

| By Temperature Control | Non-Temperature Controlled |

| Temperature Controlled |

Key Questions Answered in the Report

How large will Colombia’s road freight sector be by 2031?

The Colombia road freight transport market size is forecast to reach USD 15.44 billion by 2031, expanding at a 5.9% CAGR.

Which customer group ships the most freight?

Wholesale & Retail Trade led with 34.55% of 2025 volumes and is also the fastest-growing end-user segment.

What share of traffic is less-than-truckload?

LTL held 22.35% of 2025 revenues and is projected to grow 6.65% annually through 2031 thanks to e-commerce parcelization.

Why are containerized loads growing faster than bulk?

FTZ warehouse incentives and value-added assembly drive a 6.03% CAGR for containerized freight, despite bulk cargo dominance.

How will diesel subsidy removal affect carriers?

Pump prices are expected to rise 8-10%, squeezing margins and accelerating adoption of Euro VI and electric trucks for efficiency.

Page last updated on: