Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

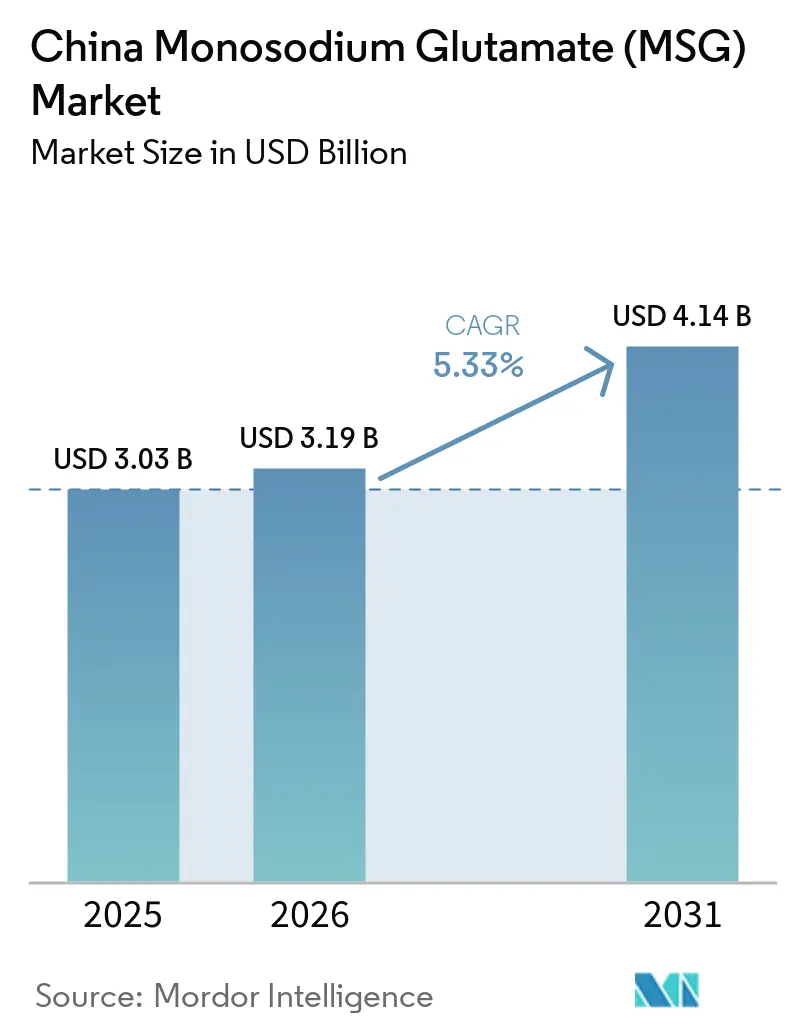

| Base Year Market Size (2025) | USD 3.03 Billion |

| Market Size (2026) | USD 3.19 Billion |

| Market Size (2031) | USD 4.14 Billion |

| Growth Rate (2026 - 2031) | 5.33% CAGR |

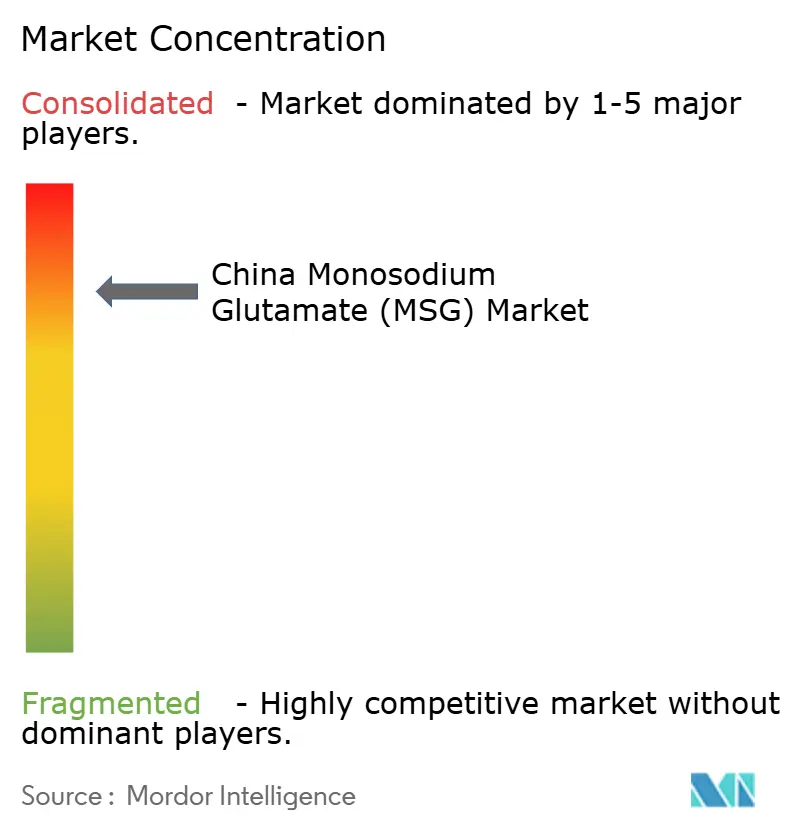

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

China Monosodium Glutamate (MSG) Market Analysis by Mordor Intelligence

The Monosodium Glutamate market size in China was valued at USD 3.03 billion in 2025 and estimated to grow from USD 3.19 billion in 2026 to reach USD 4.14 billion by 2031, at a CAGR of 5.33% during the forecast period (2026-2031). This growth is primarily driven by China's dominant role as the largest global producer and consumer of monosodium glutamate. Despite growing health concerns around food additives, the demand for monosodium glutamate remains strong. Food manufacturers rely on it to deliver a consistent umami flavor, which is highly sought after in the food industry, while also helping to reduce sodium content in products at a relatively low cost. This dual functionality makes it an indispensable ingredient for many processed foods. The market is heavily influenced by raw material availability, with corn starch being the dominant input, although cassava is emerging as a potential alternative. Natural fermentation processes continue to dominate production methods, ensuring high-quality output. In terms of applications, traditional uses of monosodium glutamate in processed foods drive the majority of demand, but innovation is expanding its reach into new product categories. China's monosodium glutamate market is highly concentrated, with an oligopolistic structure where the top five suppliers control over 80% of the country's production capacity.

Key Report Takeaways

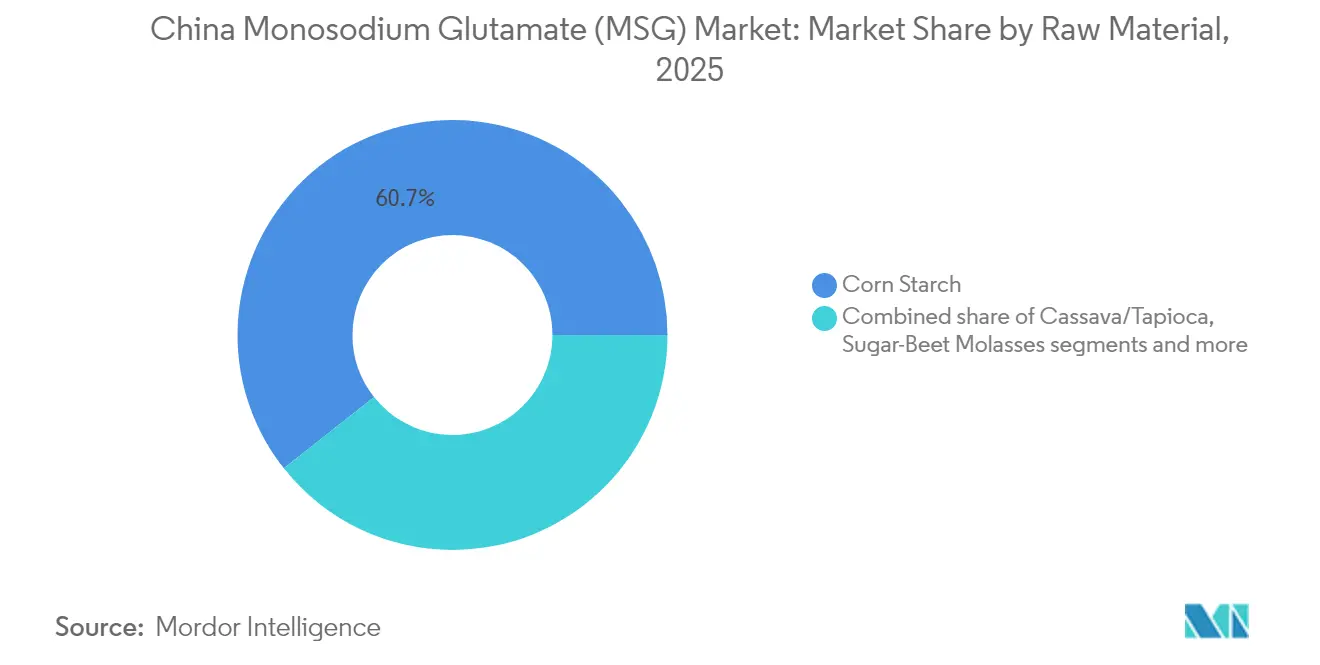

- By raw material, corn starch led with 60.65% monosodium glutamate market share in 2025, whereas cassava/tapioca is projected to expand at a 6.35% CAGR through 2031.

- By source, natural fermentation accounted for 95.72% of the monosodium glutamate market share in 2025, while synthetic production is poised for the quickest climb at a 5.79% CAGR through 2031.

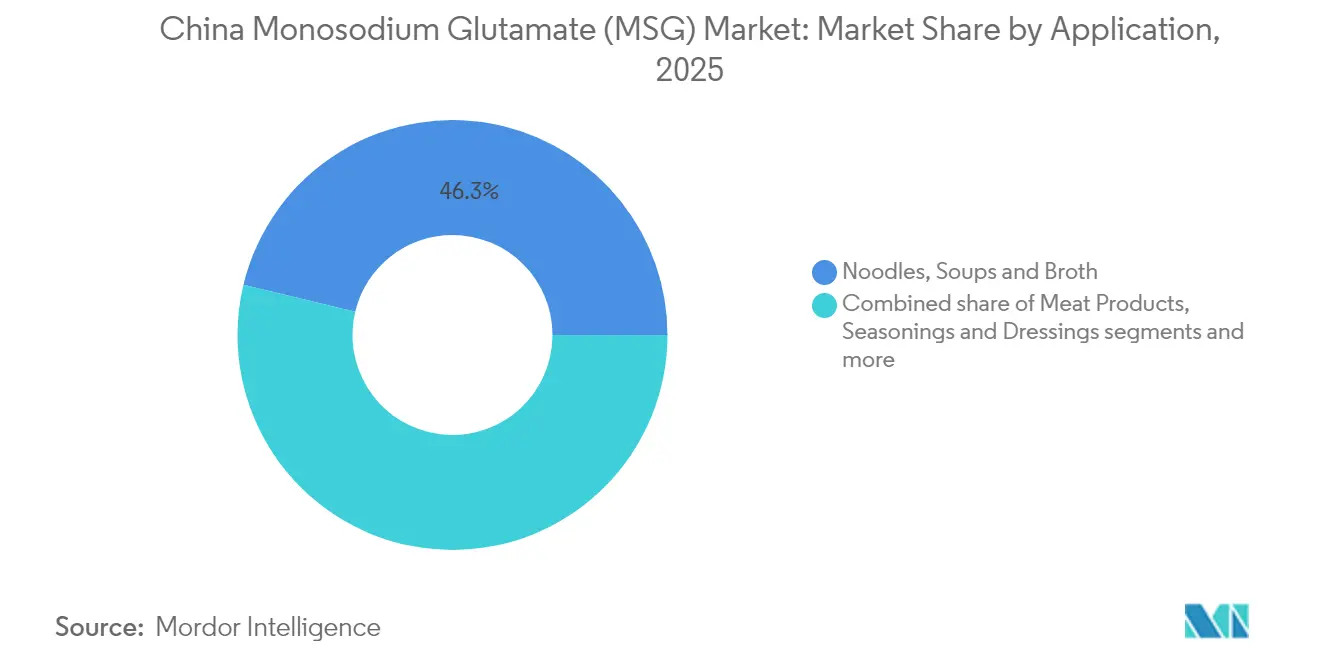

- By application, noodles, soups, and broth held 46.25% of the monosodium glutamate market size in 2025, and seasonings and dressings are advancing at a 6.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Monosodium Glutamate (MSG) Market Trends and Insights

Drivers Impact Table*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Growing demand for flavor enhancers in packaged foods | +1.2% | National, with concentration in eastern manufacturing hubs | Medium term (2-4 years) |

| Monosodium glutamate offers cost-effective taste enhancement for manufacturers | +0.8% | National, particularly in food processing clusters | Short term (≤ 2 years) |

| Expansion of foodservice and quick-service restaurant chains | +1.0% | Urban centers, tier-1 and tier-2 cities | Medium term (2-4 years) |

| Abundant raw material supply supports local monosodium glutamate production | +0.6% | Corn belt regions and cassava-growing provinces | Long term (≥ 4 years) |

| Rising consumption of instant noodles and other processed food items | +0.9% | National, with higher penetration in urban areas | Short term (≤ 2 years) |

| Technological advancements improve yield and production efficiency | +0.7% | Industrial clusters in Shandong, Inner Mongolia, Xinjiang | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing demand for flavor enhancers in packaged foods

The growing demand for flavor enhancers in China’s packaged food industry is playing a key role in driving the monosodium glutamate (MSG) market. According to the National Bureau of Statistics of China, the total retail sales of consumer goods in May reached 3,921.1 billion yuan, highlighting the expanding market potential [1]Source: National Bureau of Statistics of China, "Total Retail Sales of Consumer Goods in May 2024," stats.gov.cn. Manufacturers are increasingly relying on monosodium glutamate due to its ability to enhance the umami flavor while reducing sodium content by up to 40%, aligning with health-conscious reformulation goals. Unlike table salt, which contains 39% sodium, monosodium glutamate has only 12%, as reported by the Center for Food Safety, making it an effective solution for sodium reduction. New formulations now feature fermentation-derived monosodium glutamate, which caters to clean-label preferences and meets the growing consumer demand for natural ingredients. Advances in synthetic biology have further enabled the production of purer, “naturally fermented” monosodium glutamate variants, allowing food brands to position their products as premium offerings.

Rising consumption of instant noodles and other processed food items

The growing popularity of instant noodles and other processed foods is significantly driving the demand for monosodium glutamate in China. This is largely due to its ability to maintain flavor stability during high-temperature processing and its compatibility with long-shelf-life products. According to the World Instant Noodles Association, China and Hong Kong recorded the highest global consumption of instant noodles in 2024, with 43,802 million servings [2]Source: World Instant Noodles Association, "Demand Rankings," instantnoodles.org. This highlights the essential role of monosodium glutamate in preserving flavor and ensuring product durability. Rapid urbanization and the increasing preference for convenient, on-the-go meals among younger professionals are further boosting monosodium glutamate usage. Manufacturers aiming to expand in export markets rely on monosodium glutamate's cost-effectiveness to stay competitive, especially amid rising freight costs and trade restrictions. Monosodium Glutamate helps deliver consistent taste across a variety of dehydrated and shelf-stable food categories.

Abundant raw-material supply supports local monosodium glutamate production

China’s abundant supply of raw materials plays a crucial role in supporting its strong Monosodium Glutamate production capabilities. The northeastern regions, such as Heilongjiang and Jilin, consistently provide a reliable supply of corn starch, while cassava farming is rapidly growing in Guangxi and Yunnan provinces, aided by government subsidies aimed at promoting crop diversification. As of 2024, the Food and Agricultural Organization estimates China’s maize production at a record 295 million tonnes, driven by increased sowing and strong demand from the feed industry [3]Source: Food and Agriculture Organization, "Favourable production prospects for 2025 wheat crop," fao.org. This ensures a steady supply of raw materials for fermentation-based industries like monosodium glutamate production. Companies such as Thai Wah are investing in cassava-processing facilities, enabling a dual-feedstock approach that helps mitigate the impact of global grain price fluctuations. Leading manufacturers, including Fufeng Group, have implemented vertical integration strategies, managing operations from corn farming to glutamic acid fermentation.

Monosodium Glutamate offers cost-effective taste enhancement for manufacturers

Monosodium Glutamate remains a highly popular and cost-effective flavor enhancer for food manufacturers, particularly as they face increasing production costs. Its ability to deliver a strong umami flavor in small quantities helps producers reduce formulation expenses while maintaining consistent taste across large-scale production. Compared to alternatives like yeast extracts and protein hydrolysates, monosodium glutamate is simpler to use and offers greater stability in preserving flavor quality. Leading Chinese manufacturers are leveraging advancements in synthetic biology and precision fermentation to enhance production efficiency, further lowering costs. These innovations have reinforced monosodium glutamate's position as a preferred ingredient in widely consumed products such as instant noodles, savory snacks, and processed foods. Its affordability and reliability make it indispensable for both domestic consumption and export-oriented food products, ensuring its continued demand in the global market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health concerns related to excessive monosodium glutamate consumption | -0.7% | Urban centers with higher health awareness | Medium term (2-4 years) |

| Rising popularity of natural and clean label foods | -0.5% | Tier-1 cities and affluent consumer segments | Long term (≥ 4 years) |

| Regulatory restrictions on monosodium glutamate in certain applications | -0.3% | National, with stricter enforcement in export markets | Short term (≤ 2 years) |

| Competition from natural umami sources like yeast extract | -0.4% | Premium food segments and health-conscious demographics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Health concerns related to excessive monosodium glutamate consumption

Concerns about excessive monosodium glutamate consumption continue to limit market growth, particularly among urban and health-conscious consumers. Although global regulatory bodies like the FAO/WHO Joint Expert Committee on Food Additives have confirmed monosodium glutamate's safety within acceptable intake limits, many consumers remain skeptical. Studies, such as intake modeling from ScienceDirect, show that children aged 3–6 years in high-exposure groups may consume up to 97.2% of the Acceptable Daily Intake (ADI), raising concerns among parents and public health advocates. Outdated myths like “Chinese Restaurant Syndrome” persist, fueled by misinformation on social media, despite being scientifically debunked. In response to these challenges, premium food brands, especially in tier-1 Chinese cities, are introducing monosodium glutamate-free or “all-natural umami” product lines. These cleaner-label alternatives are gaining traction, redirecting some market value away from traditional monosodium glutamate products and pushing manufacturers to innovate and meet evolving consumer preferences.

Rising popularity of natural and clean-label foods

The growing demand for natural and clean-label foods is challenging Monosodium Glutamate's market presence, particularly in China’s urban and affluent regions. Consumers, especially those in higher-income households, are increasingly scrutinizing ingredient lists and favoring products labeled as “additive-free” or “no added monosodium glutamate.” The USDA GAIN Report highlights that China’s updated GB 7718-2025 food labeling regulation will require clearer disclosure of food additives, including Monosodium Glutamate, starting in March 2027 [4]Source: United States Department of Agriculture, "Prepackaged Food Labeling Standards Finalized," apps.fas.usda.gov. This change is expected to make monosodium glutamate more noticeable to health-conscious buyers. In response, food manufacturers are reformulating premium product lines with alternatives like yeast extracts, tomato concentrates, or mushroom-based seasonings to align with clean-label trends. This shift is particularly evident in tier-1 cities such as Beijing, Shanghai, and Shenzhen, where consumers are more inclined toward natural and healthier options.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material: Corn Starch Dominance Faces Cassava Challenge

Corn-starch formulations captured 60.65% of the China Monosodium Glutamate market share in 2025 because well-established wet-milling hubs in Heilongjiang and Jilin deliver steady, low-cost feedstock to adjacent fermentation plants. The same logistics networks channel finished monosodium glutamate into coastal seasoning factories, reinforcing corn’s position at the heart of domestic supply chains. Cassava-based monosodium glutamate remained smaller but benefited from Guangxi’s expanding crop base and Thai-linked import routes that secure year-round material flow. Sugar-beet molasses and other niche substrates held marginal shares, serving regional plants that capitalize on local by-product streams.

Looking ahead to 2031, cassava/tapioca-based monosodium glutamate is expected to grow at a faster rate, with a projected CAGR of 6.35%, outpacing other substrates. This growth is driven by advancements in fermentation technology, which are reducing detoxification costs, and by Guangxi’s increasing cassava acreage to meet rising demand. Corn-starch-based monosodium glutamate will continue to expand, albeit at a slower pace, as large integrated producers focus on balancing capacity utilization with environmental regulations. Meanwhile, sugar-beet and other specialty feedstocks are likely to see modest growth, primarily supporting research and development efforts and catering to niche markets that require differentiated texture or higher purity grades.

By Source: Natural Fermentation Maintains Overwhelming Dominance

Natural fermentation accounted for 95.72% of the total monosodium glutamate production in China in 2025, driven by consumer preference for products labeled as “naturally fermented” and the long-standing efficiency of Corynebacterium glutamicum cultures. This method is favored for its lower environmental impact, aligning with regulatory requirements and the growing demand for cleaner supply chains. Producers have optimized this process over the years, making it the dominant production method. On the other hand, chemically synthesized monosodium glutamate holds a smaller market share, catering to industries that require ultra-high purity, specific crystal shapes, or low-dust formulations for specialized applications.

In the coming years, synthetic production is projected to grow at a 5.79% CAGR by 2031. This growth will primarily be driven by niche applications in the pharmaceutical sector and specialized seasoning products that demand precise particle morphology, which fermentation cannot achieve. However, advancements in synthetic biology are likely to further improve fermentation yields and reduce refining costs, ensuring its continued prevalence in the market. While chemical synthesis will see incremental growth, natural fermentation will remain the preferred method due to its scalability and alignment with sustainability goals.

By Application: Traditional Uses Drive Growth While Innovation Expands Reach

In 2025, noodles, soups, and broths accounted for 46.25% of the monosodium glutamate market, highlighting their integral role in Chinese cuisine and the reliance on monosodium glutamate to enhance flavors in instant noodle seasoning packets. Other segments, such as processed meats, snacks, and dairy products, consumed smaller quantities but remained important contributors, where monosodium glutamate is used to amplify savory profiles. The seasonings and dressings segment, though smaller in market share, is steadily expanding due to the growing availability of compound condiments in retail stores and online platforms, catering to evolving consumer preferences.

The seasonings and dressings segment is projected to grow at a 6.31% CAGR through 2031, making it the fastest-growing application area. This growth is fueled by increasing demand for products like hot-pot bases, marinades, and dipping sauces, which align with the rising trend of home-based entertainment in China. While the use of monosodium glutamate in instant noodles and soups is expected to grow at a slower rate, it will still contribute significantly to the market due to the ongoing urbanization and the demand for convenient meal options. Emerging applications in innovative areas such as 3D-printed foods and sports nutrition gels are anticipated to provide additional high-margin opportunities toward the end of the forecast period.

Geography Analysis

China’s monosodium glutamate production is deeply influenced by the availability of raw materials and government policies aimed at industrial development. The northeastern provinces of Heilongjiang, Jilin, and Liaoning, known for their abundant corn supply, host large biorefineries that support nearby monosodium glutamate fermentation plants. Shandong province, with its strategic coastal location, plays a crucial role in downstream blending and export packaging, acting as a key logistics hub for food processors in the Yangtze River Delta. Fufeng Group, which holds a dominant 57% share of the domestic market, exemplifies this model with its Shandong facility, efficiently combining coastal access and corn shipments from the Northeast to maintain a cost-effective supply chain.

Inland regions such as Inner Mongolia and Xinjiang are rapidly becoming important centers for monosodium glutamate production. These areas offer advantages like low-cost land, renewable energy projects, and strong rail connections to Central Asia, attracting significant investments in new production facilities. Cities like Ulanqab and Korla are emerging as key production hubs, helping to diversify monosodium glutamate supply away from coastal regions that are more vulnerable to environmental restrictions and typhoons. These inland facilities cater to domestic food manufacturers and serve export routes through the China–Europe rail corridor, although European Union anti-dumping measures continue to limit the volume of exports.

Southern provinces like Guangdong and Fujian present a unique scenario, as they are major consumers of monosodium glutamate used in Cantonese sauces, dried seafood seasonings, and instant soup bases, which are widely exported. These provinces rely on cassava sourced from Guangxi as an alternative to corn, reflecting a growing trend toward feedstock diversification. Meanwhile, rising incomes and increased tourism in Hainan are driving demand for premium condiments, particularly those marketed with “non-additive” claims. While this shift poses challenges for monosodium glutamate penetration, it also opens opportunities for innovation, such as the development of lower-sodium and fermented monosodium glutamate variants to cater to changing consumer preferences.

Competitive Landscape

China’s monosodium glutamate market is highly consolidated, dominated by a few major players, with the top five suppliers accounting for over 80% of the country’s production capacity. Leading the market is Fufeng Group, which operates an integrated corn-processing system that spans from raw material storage to finished seasoning blends. The company’s focus on advanced fermentation technology and automated crystallization processes has significantly reduced energy costs, solidifying its position as a cost leader. Meihua Holdings, the second-largest player, utilizes proprietary synthetic biology strains to enhance productivity, which highlights the scale required to compete effectively in this market.

Mid-sized companies like Vedan International are adapting to stricter environmental regulations by upgrading wastewater treatment facilities and collaborating with local governments to secure tax incentives. However, some smaller players are losing market share to larger, better-funded competitors. International companies like Ajinomoto maintain a niche presence in the premium segment, offering high-purity monosodium glutamate and specialty nucleotides for applications in infant formula and pharmaceuticals. Despite this, intense price competition in the domestic market limits their ability to expand into the mass-market segment.

Merger and acquisition activity in the monosodium glutamate market is increasing. For instance, the February 2025 bidding war for CJ CheilJedang’s USD 4.1 billion bio division highlights private equity interest in consolidating amino acid assets, including monosodium glutamate, lysine, and tryptophan. At the same time, Chinese producers are focusing on developing specialty monosodium glutamate grades, such as dust-free granules for seasoning cube production, to differentiate themselves beyond cost advantages. Export strategies remain challenging due to anti-dumping tariffs in the European Union. As a result, Chinese companies are shifting their focus to emerging markets in Africa and Latin America to drive growth.

China Monosodium Glutamate (MSG) Industry Leaders

-

Fufeng Group Limited

-

COFCO Corporation

-

Meihua Holdings Group Co. Ltd

-

Ningxia Eppen Biotech

-

Vedan International Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: China's Fufeng Group, which specializes in the deep processing of corn, has begun constructing an industrial park. The project will also manufacture lysine, monosodium glutamate, xanthan gum, and feed amino acids.

- December 2024: Tongliao Meihua monosodium glutamate products passed the carbon footprint and water footprint certification. This demonstrated the company's unremitting efforts and firm commitment to green manufacturing.

China Monosodium Glutamate (MSG) Market Report Scope

The China monosodium glutamate (MSG) market is segmented by application. On the basis of application, the market is segmented into noodles, soups and broth, meat products, seasonings and dressings, and other applications.

By Raw Material

| Corn Starch |

| Sugar-beet Molasses |

| Cassava/Tapioca |

| Other Substrates |

By Source

| Natural Fermentation-Based |

| Synthetic/Chemically Derived |

By Application

| Noodles, Soups, and Broth |

| Meat Products |

| Seasonings and Dressings |

| Other Applications |

| By Raw Material | Corn Starch |

| Sugar-beet Molasses | |

| Cassava/Tapioca | |

| Other Substrates | |

| By Source | Natural Fermentation-Based |

| Synthetic/Chemically Derived | |

| By Application | Noodles, Soups, and Broth |

| Meat Products | |

| Seasonings and Dressings | |

| Other Applications |

Key Questions Answered in the Report

How big is China’s Monosodium Glutamate market today, and how fast will it grow?

The Monosodium Glutamate market in China is estimated at USD 3.19 billion in 2026 and is projected to climb to USD 4.14 billion by 2031, marking a 5.33% CAGR.

Which source dominates Monosodium Glutamate market in China?

Natural fermentation accounted for 95.72% of the monosodium glutamate market share in 2025.

What raw material dominates Monosodium Glutamate production in China?

Corn starch remains the primary feedstock with 60.65% share in 2025, though cassava-based production is the fastest-growing at a 6.35% CAGR through 2031.

How do new Chinese labeling rules affect Monosodium Glutamate manufacturers?

GB 7718-2025, effective March 2027, requires clearer additive disclosure, which could shift consumer perception and prompt reformulation in premium products.

Page last updated on: