China LED Epitaxy MOCVD Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

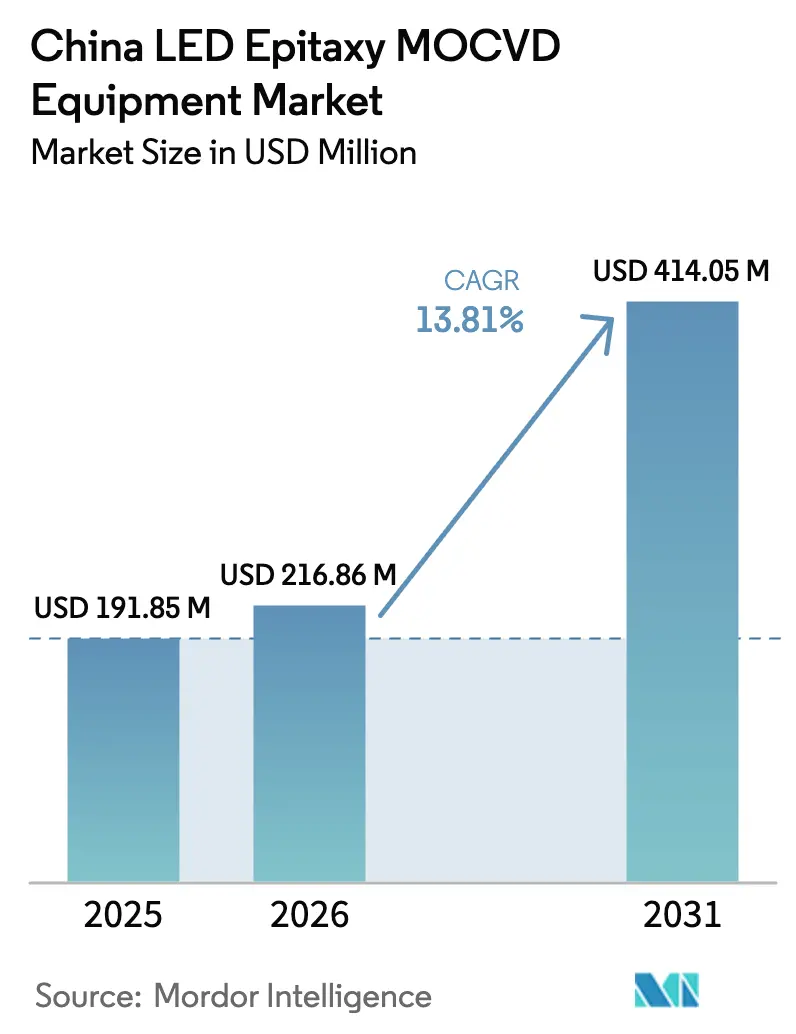

| Base Year Market Size (2025) | USD 191.85 Million |

| Market Size (2026) | USD 216.86 Million |

| Market Size (2031) | USD 414.05 Million |

| Growth Rate (2026 - 2031) | 13.81% CAGR |

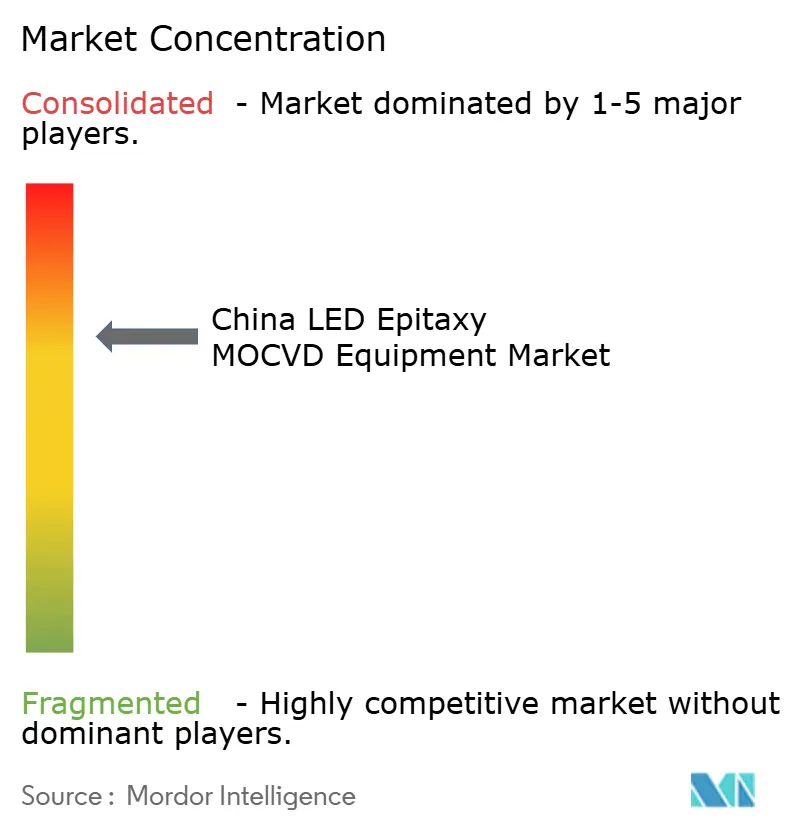

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China LED Epitaxy MOCVD Equipment Market Analysis by Mordor Intelligence

The China LED epitaxy MOCVD equipment market size is projected to be USD 191.85 million in 2025, USD 216.86 million in 2026, and reach USD 414.05 million by 2031, growing at a CAGR of 13.81% from 2026 to 2031. Solid policy support, rapid capacity expansion by vertically integrated device makers, and a steady pivot toward advanced display and automotive applications are steering capital toward domestic reactors. Strong localization rules that tie government incentives to local tool purchases have made Chinese suppliers the default choice for new lines, while a looming switch to 200 millimeter wafers promises a structural cost reset that keeps unit economics attractive even as general lighting demand plateaus. Large smart phone and panel makers are now underwriting pilot micro LED lines, tightening uniformity specifications that favor close coupled showerhead architectures. Meanwhile, persistent supply risk around gallium and aluminum precursors accelerates multi-year procurement contracts that lock in domestic chemical streams. Together, these factors sustain a robust outlook for the China LED epitaxy MOCVD equipment market despite cyclical softness in commodity devices.

Key Report Takeaways

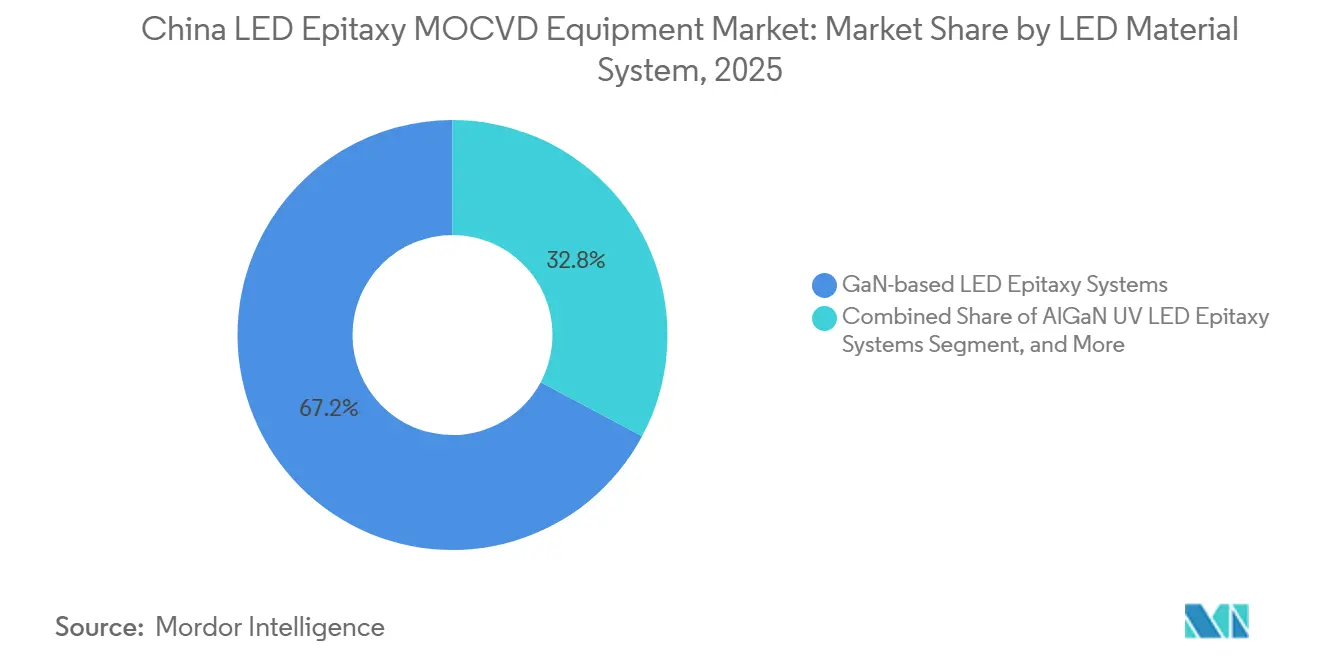

- By LED material system, GaN-based LED epitaxy systems held 67.19% of the China LED epitaxy MOCVD equipment market share in 2025, while the AlGaN UV LED epitaxy systems segment is projected to grow at a 14.53% CAGR through 2031.

- By wafer size capability, the 150 mm segment accounts for 45.24% of the China LED epitaxy MOCVD equipment market size in 2025, whereas the 200 mm and above segment is forecast to expand at a 14.14% CAGR between 2026 and 2031.

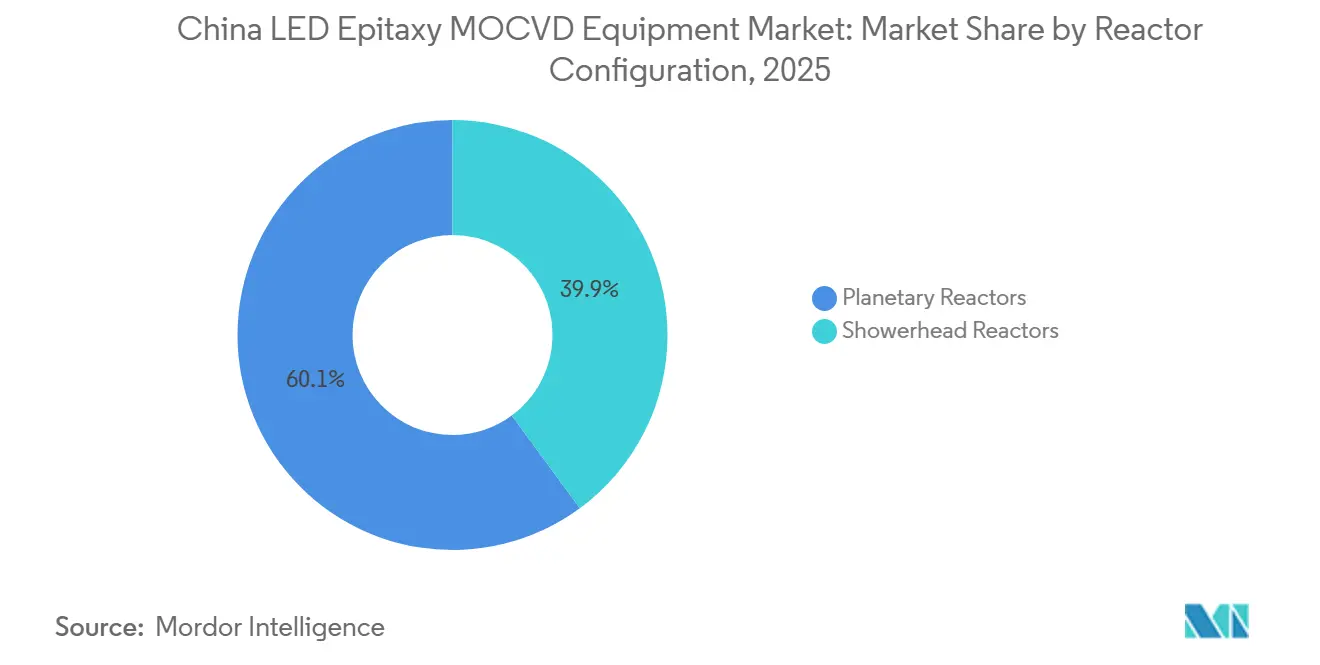

- By reactor configuration, the planetary reactors segment led with 60.09% share in 2025, but the showerhead reactors segment is expected to advance at a 14.48% CAGR during the forecast period.

- By end user, the integrated LED manufacturers segment commanded 71.64% of the market share in 2025, yet the epitaxy foundries and merchant Epi suppliers segment is set to post the fastest growth at a 14.62% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global valuation is built by aggregating outputs from multiple countries and regions, with China being one of the contributors. Our global led epitaxy mocvd equipment market size represents that cumulative total.

China LED Epitaxy MOCVD Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for High Brightness GaN-Based LEDs in Automotive Lighting | +3.2% | Nationwide clusters in Guangdong, Jiangsu, Zhejiang | Medium term (2-4 years) |

| Subsidy Reforms Accelerating Domestic MOCVD Adoption | +4.1% | Nationwide, tied to state backed semiconductor projects | Short term (≤ 2 years) |

| Capacity Expansion of Chinese IDM LED Manufacturers Post-2026 | +2.8% | Fujian, Hubei, Anhui corridors | Medium term (2-4 years) |

| Localization Initiatives for Semiconductor Equipment Supply Chains | +3.5% | Nationwide, spillover to Belt and Road partners | Long term (≥ 4 years) |

| Shift to 200 mm Sapphire Wafers Reducing Per Device Cost | +1.9% | Xiamen, Wuhan, Hefei pilot fabs | Medium term (2-4 years) |

| Emerging Micro LED Display Projects Backed by Smartphone OEMs | +2.4% | Xiamen, Mianyang, Shenzhen | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for High Brightness GaN Based LEDs in Automotive Lighting

Automakers are shifting from halogen or HID lamps to adaptive GaN arrays that deliver up to 200 lumens per watt, cutting power draw and boosting electric-vehicle range. Sanan Optoelectronics’ 2025 purchase of Lumileds secured a sizeable patent library and automotive-qualified GaN recipes, positioning local tier-one suppliers to capture higher value modules. New headlamp rules issued by MIIT mandate glare-free high beam patterns, effectively locking in pixel-addressable GaN as the compliant technology.[1]Ministry of Industry and Information Technology, “GB 25991-2020 Headlamp Photometric Requirements,” miit.gov.cn Higher raw material costs since 2025 further favor these efficient dies, because fewer chips now achieve the required brightness. Collectively, these forces lift equipment demand as headlamp makers convert entire production lines to high-power GaN.

Subsidy Reforms Accelerating Domestic MOCVD Adoption

A December 2025 directive links state subsidies to a 50% domestic tool quota, forcing fabs that rely on public funding to qualify Chinese reactors or lose access to RMB 81 billion (USD 11.4 billion) in aid. Advanced Micro-Fabrication Equipment Inc. China responded by shipping production batches of its newest six and eight-wafer tools with over 80% local content, easing licensing risk under United States export controls.[2]U.S. Department of Commerce, “Export Controls for Compound Semiconductor Equipment,” commerce.gov Early adopters report wavelength uniformity under 2% across 50 wafer runs, a level once attainable only on premium imports, supporting accelerated switch overs.

Capacity Expansion of Chinese IDM LED Manufacturers Post-2026

Integrated device makers are scaling aggressively to lock in margin across epitaxy, fabrication, and packaging. Sanan’s Hubei campus is slated to house 4,995 front end tools by 2027, including 120 reactors dedicated to red green blue micro displays. HC Semitek’s in-house wafers cut external procurement costs by 18%, enabling the firm to post 13.44% revenue growth in the first half of 2025. Vertical ownership allows real time recipe tuning that has already lifted die yield from 85% to 92%, underpinning a fresh purchasing cycle for mid decade lines.

Localization Initiatives for Semiconductor Equipment Supply Chains

Self-sufficiency targets call for 70% domestic tool coverage by 2027, up from 35% in 2025. Financing from the third phase of the National Integrated Circuit Industry Fund directs RMB 344 billion (USD 48.5 billion) toward front-end equipment, with epitaxy classed as a priority technology. AMEC and NAURA now source manifolds, quartzware, and vacuum sub-components from local vendors, cutting export exposure and shaving up to 20 weeks off lead times. Domestic chemical suppliers are also scaling trimethylgallium output to 50 metric tons per year, protecting fabs from international gallium price spikes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Slowdown in General Lighting LED Demand Saturation | -2.7% | Mature residential and commercial segments nationwide | Short term (≤ 2 years) |

| High Capital Intensity and Long Payback Periods for New Reactors | -1.8% | Small and medium sized epitaxy foundries nationwide | Medium term (2-4 years) |

| Supply Chain Volatility in High Purity Source Materials | -1.4% | Export oriented fabs nationwide | Short term (≤ 2 years) |

| Stringent Environmental Compliance Costs for Epitaxy Facilities | -0.9% | Jiangsu, Zhejiang, Guangdong coastal belts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Slowdown In General Lighting LED Demand Saturation

Urban households surpassed 75% LED penetration by 2024, elongating replacement cycles from three to roughly seven years. Combined with slower real estate starts, this dynamic reduced commodity GaN wafer pricing by 8 % in 2025 and cut merchant utilization into the high seventies.[3]U.S. Department of Energy, “LED Manufacturing Cost Analysis 2025,” energy.gov Suppliers are reallocating capital toward automotive, horticultural, and UVC segments, but the transition period weighs on near term orders for legacy 150 millimeter tools.

High Capital Intensity and Long Payback Periods for New Reactors

A 50-reactor line carries a USD 150-250 million price tag once cleanrooms and gas delivery are included, stretching payback beyond five years unless subsidy offsets apply. The mandatory domestic-tool quota softens equipment discounts but can lengthen ramp schedules, as new reactors often require more than one year of process tuning before matching imported yields. Smaller foundries, therefore, face balance sheet strain, which may slow tool adoption until wafer pricing for premium applications firmly outpaces depreciation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By LED Material System: GaN Leads While UV Gains Momentum

GaN platforms accounted for 67.19% of the China LED epitaxy MOCVD equipment market share in 2025, driven by their use in automotive headlamps, horticultural lamps, and pilot micro display lines. AlGaN ultraviolet tools are expected to grow at a 14.53% CAGR as municipal water and healthcare operators prefer mercury-free 265-275 nanometer emitters that meet disinfection standards without chemical byproducts. This growth is supported by advancements in aluminum nitride wafers, which enable higher current density compared to sapphire, reducing die counts per lamp and lowering fixture costs.

GaN producers are addressing flat general lighting demand by redirecting surplus capacity into high-brightness automotive arrays and early micro display qualification runs. These applications require tight binning but offer price premiums, ensuring healthy overall utilization. Sustained UV momentum relies on substrate breakthroughs, with aluminum nitride wafers playing a critical role in enhancing performance and cost efficiency.

By Wafer Size Capability: 200 mm Shift Drives Economies Of Scale

Legacy 150 millimeter reactors accounted for 45.24% of the China LED epitaxy MOCVD equipment market size in 2025. The demand for 200 millimeter and larger systems is expected to grow at a rate of 14.14% through 2031. This growth is driven by fabs achieving 35-40% per die cost savings through higher throughput and improved substrate utilization.

A surge of joint development projects, such as the 200 millimeter GaN on silicon program between ALLOS and Ennostar, underlines the migration. Reactor OEMs are enlarging platen diameters while refining gas flow to hold sub-2% wavelength variation across larger wafers, prerequisites for premium micro displays. Tool makers that master these parameters early will capture next wave orders once crystal growers clear current lead time bottlenecks.

By Reactor Configuration: Showerhead Adoption Quickens

Planetary tools accounted for 60.09% of the market share in 2025 due to their established reliability in commodity output, where 8-12 nanometer peak-to-peak uniformity is sufficient. Close-coupled showerhead systems are projected to grow at 14.48% as display and automotive customers increasingly demand below 5 nanometer variation. These systems are gaining traction due to their ability to meet stringent uniformity requirements.

Showerhead reactors, with perpendicular gas flow reducing boundary layer effects, achieve sub-1% uniformity over 200 millimeter wafers while maintaining low defect densities. Domestic suppliers now match foreign benchmarks with advanced technology. Integrated in situ monitoring has further tightened process windows, catering to the needs of high-resolution devices.

By End User: Outsourced Epitaxy Gains Traction

Integrated device makers accounted for 71.64% of the market share in 2025 due to the advantages of vertical control, which eliminates merchant markups. This approach also accelerates recipe optimization, making it highly efficient. Large IDMs like Sanan have significantly scaled micro LED lines, with its Hubei complex alone allocating 120 reactors for RGB die production.

Foundry and merchant epi houses are expected to experience the strongest growth at 14.62% through 2031, driven by the preference of smartphone, tablet, and wearable brands for asset-light strategies. Outsourcing advanced die production helps brands avoid fixed investments of USD 150-250 million. It also allows them to benefit from foundry learning curves, which distribute costs across multiple clients, making this model particularly appealing for micro LED production, where yields remain unpredictable.

Geography Analysis

Fujian hosts the single largest cluster, anchored by Sanan’s Xiamen headquarters and adjacent suppliers. Together, they may hold one-third of the national reactors. Guangdong follows closely due to Shenzhen’s dense downstream ecosystem of handset, panel, and automotive lighting firms, which are now running qualification lines that demand high-uniformity tools.

In the Yangtze River Delta, Jiangsu and Zhejiang benefit from proximity to sapphire growers, financial markets, and export logistics. These factors make them natural homes for medium-scale foundries. Hubei has emerged as a micro display hub, where provincial incentives and available land enabled Sanan to begin constructing a multibillion-dollar tool park that promises to develop a local skills base supporting the broader region.

These coastal and central provinces share strict green factory codes that require ammonia and fluorine abatement, increasing both upfront and recurring costs. However, compliance spending is partially offset by shorter chemical supply chains. Domestic precursor plants in Zhejiang and Jiangsu now deliver within 48 hours, avoiding the longer shipping cycles of imported materials.

Coverage of the led epitaxy mocvd equipment market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Asia, alongside detailed country-level intelligence for Taiwan and Japan, each shaped by local operating conditions.

Competitive Landscape

The China LED epitaxy MOCVD equipment market remains moderately concentrated. Advanced Micro-Fabrication Equipment Inc. China surpassed the 100-tool milestone for its flagship GaN reactors in 2025, firming domestic share above 80% for general lighting equipment. Veeco and Aixtron still command high-performance niches, particularly UVC and red die, under multiyear tool-of-record contracts, though their aggregate share has slipped to roughly one-sixth of shipments.

NAURA’s entry into the global top five in early 2026 highlights the rapid progress of local OEMs in achieving uniformity, throughput, and reliability. The firm’s Satur series consistently achieves sub-2% wavelength variation across 50-wafer batches. It matches imported benchmarks while providing shorter lead times through local supply chains.

Looking ahead, 200 millimeter and 300 millimeter GaN on silicon platforms represent the prime white space. United States export restrictions limit foreign deliveries of large diameter compound tools, giving Chinese makers a rare window to leapfrog into volume positions before global competitors can re-enter. Success will hinge on integrating advanced in situ metrology and maintaining chamber cleanliness at larger scales, both critical for micro display grade wafers.

China LED Epitaxy MOCVD Equipment Industry Leaders

Advanced Micro-Fabrication Equipment Inc. China

Veeco Instruments Inc.

Aixtron SE

NAURA Technology Group Co., Ltd.

Taiyo Nippon Sanso Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: NAURA Technology Group climbed to fifth in worldwide semiconductor equipment rankings after strong uptake of its Satur N800 and Satur V700 reactors.

- January 2026: ALLOS Semiconductors and Ennostar partnered to commercialize 200 millimeter GaN on silicon epi wafers targeting micro LED displays.

- January 2026: China’s LED supply chain enacted 3-15% price increases across wafers, packages, and modules following gallium driven precursor inflation and a 22% rise in sapphire costs.

- December 2025: Beijing enforced the 50% domestic equipment quota for all state backed semiconductor projects, linking subsidy access to local tool purchases.

China LED Epitaxy MOCVD Equipment Market Report Scope

The LED Epitaxy MOCVD Equipment Market refers to the segment of the semiconductor equipment industry focused on manufacturing Metal-Organic Chemical Vapor Deposition (MOCVD) systems used for the epitaxial growth of LED materials. These systems are critical for producing high-quality LED wafers, which serve as the foundation for LED devices used in various applications such as lighting, displays, and automotive technologies.

The China LED Epitaxy MOCVD Equipment Market Report is Segmented by LED Material System (GaN-based LED Epitaxy Systems, AlGaN UV LED Epitaxy Systems, and AlInGaP LED Epitaxy Systems), Wafer Size Capability (Up to 100mm, 150mm, and 200mm and Above), Reactor Configuration (Planetary Reactors, and Showerhead Reactors), and End User (Integrated LED Manufacturers, and Epitaxy Foundries and Merchant Epi Suppliers). The Market Forecasts are Provided in Terms of Value (USD).

| GaN-based LED Epitaxy Systems |

| AlGaN UV LED Epitaxy Systems |

| AlInGaP LED Epitaxy Systems |

| Upto 100 mm |

| 150 mm |

| 200 mm and Above |

| Planetary Reactors |

| Showerhead Reactors |

| Integrated LED Manufacturers (IDMs) |

| Epitaxy Foundries and Merchant Epi Suppliers |

| By LED Material System | GaN-based LED Epitaxy Systems |

| AlGaN UV LED Epitaxy Systems | |

| AlInGaP LED Epitaxy Systems | |

| By Wafer Size Capability | Upto 100 mm |

| 150 mm | |

| 200 mm and Above | |

| By Reactor Configuration | Planetary Reactors |

| Showerhead Reactors | |

| By End User | Integrated LED Manufacturers (IDMs) |

| Epitaxy Foundries and Merchant Epi Suppliers |

Key Questions Answered in the Report

What was the China LED epitaxy MOCVD equipment market size in 2026?

The market stood at USD 216.86 million in 2026, up from USD 191.85 million in 2025 and on track to reach USD 414.05 million by 2031.

How fast is equipment demand growing for GaN ultraviolet lines in China?

AlGaN UVC reactor demand is projected to expand at a 14.53% CAGR between 2026 and 2031, the quickest among all material systems.

Which wafer size is gaining traction among Chinese LED epitaxy fabs?

Lines capable of processing 200 millimeter wafers segment is expected to grow at a 14.14% CAGR, positioning them to overtake 150 millimeter tools by 2031.

Why are showerhead reactors becoming more popular than planetary designs?

Showerhead systems consistently deliver under 5 nanometer wavelength variation across 200 millimeter wafers, a metric required for micro-LED and advanced automotive arrays.

What policy most influences tool selection in Chinese LED fabs?

A December 2025 mandate ties government incentives to at least 50% domestic equipment content, steering most new purchases toward local reactor vendors.

What is driving the recent surge in epitaxy raw material costs?

China’s late-2024 gallium export controls and tighter global sapphire supply have pushed up trimethylgallium and substrate prices, leading to 3-15% industry-wide price increases in 2026.

Page last updated on: