Asia-Pacific LED Epitaxy MOCVD Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

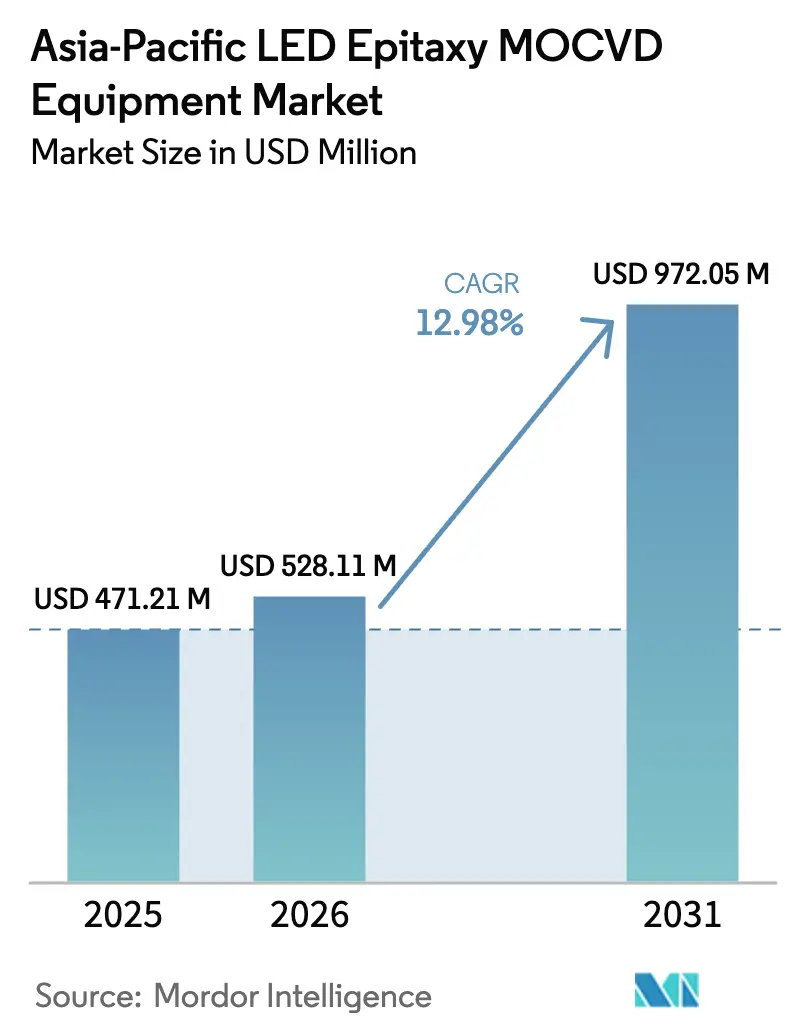

| Base Year Market Size (2025) | USD 471.21 Million |

| Market Size (2026) | USD 528.11 Million |

| Market Size (2031) | USD 972.05 Million |

| Growth Rate (2026 - 2031) | 12.98% CAGR |

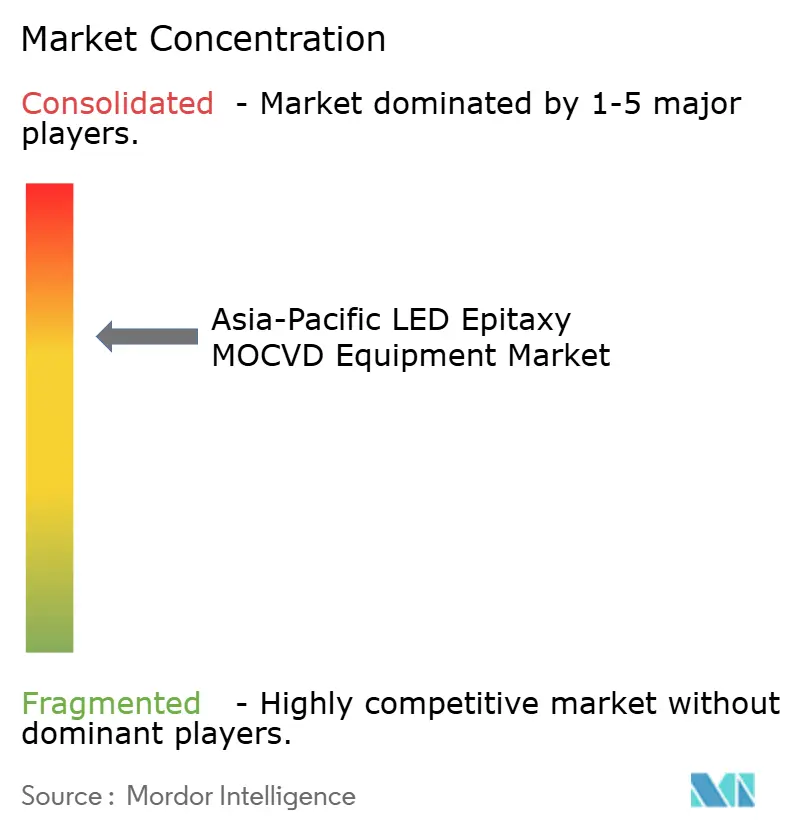

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific LED Epitaxy MOCVD Equipment Market Analysis by Mordor Intelligence

The Asia-Pacific LED epitaxy MOCVD equipment market size is projected to be USD 471.21 million in 2025, USD 528.11 million in 2026, and reach USD 972.05 million by 2031, growing at a CAGR of 12.98% from 2026 to 2031. Robust state incentives for domestic semiconductor tools, the pivot toward mini-LED and micro-LED displays, and the shift to larger GaN wafers are together accelerating capital spending across China, Taiwan, Japan, and South Korea. Local equipment vendors are capitalizing on Beijing’s mandate that at least half of new semiconductor tools come from domestic suppliers, while display makers are qualifying advanced showerhead reactors to meet tight wavelength-binning targets. Gallium export controls are reinforcing regional self-reliance, driving long-term supply-chain realignment, and expanding addressable demand for indigenous precursor purification. At the same time, AI-driven in-situ metrology is becoming standard on new tools, cutting defect density and shortening root-cause analysis cycles. Refurbishment programs are widening access to mature reactors for Tier-2 fabs, enabling incremental capacity additions without full capital outlays.

Key Report Takeaways

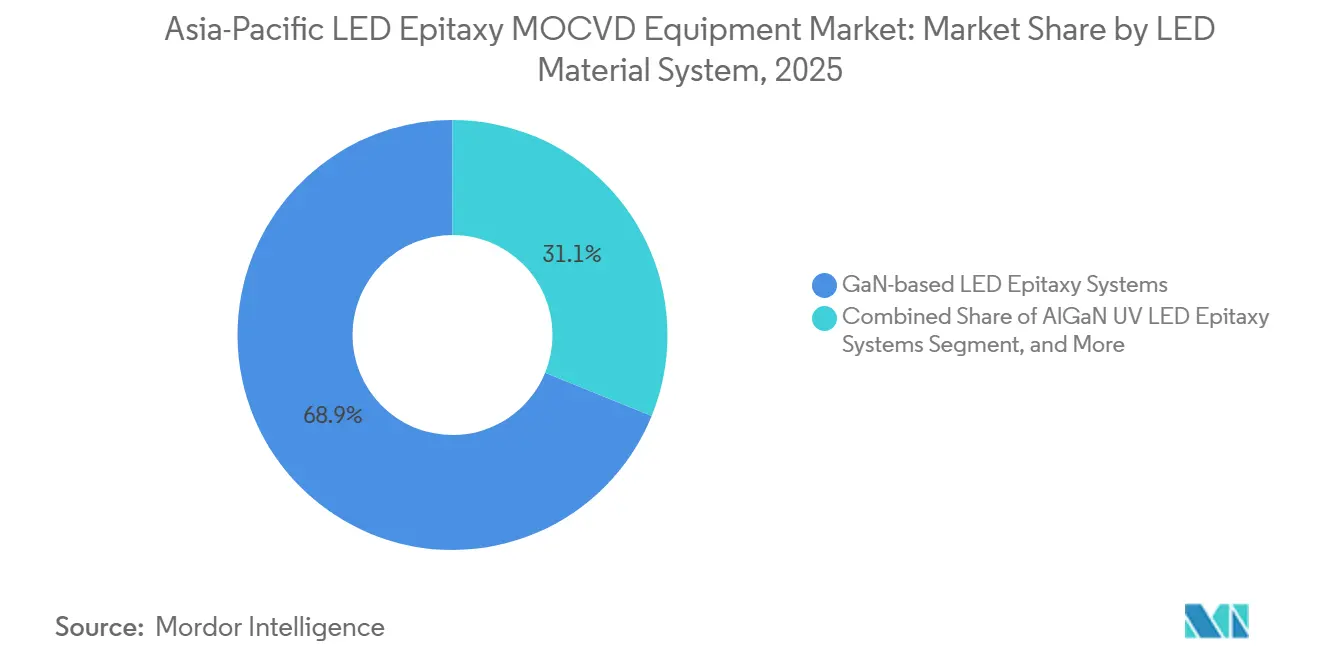

- By LED material system, GaN-based LED epitaxy systems segment held 68.86% of the market share in 2025, while the AlGaN UV LED epitaxy systems segment is forecast to advance at a 13.24% CAGR through 2031.

- By wafer size capability, the 150 mm segment accounted for 46.39% of the Asia-Pacific LED epitaxy MOCVD equipment market share in 2025, whereas the 200 mm and above segment is projected to expand at a 13.63% CAGR between 2026 and 2031.

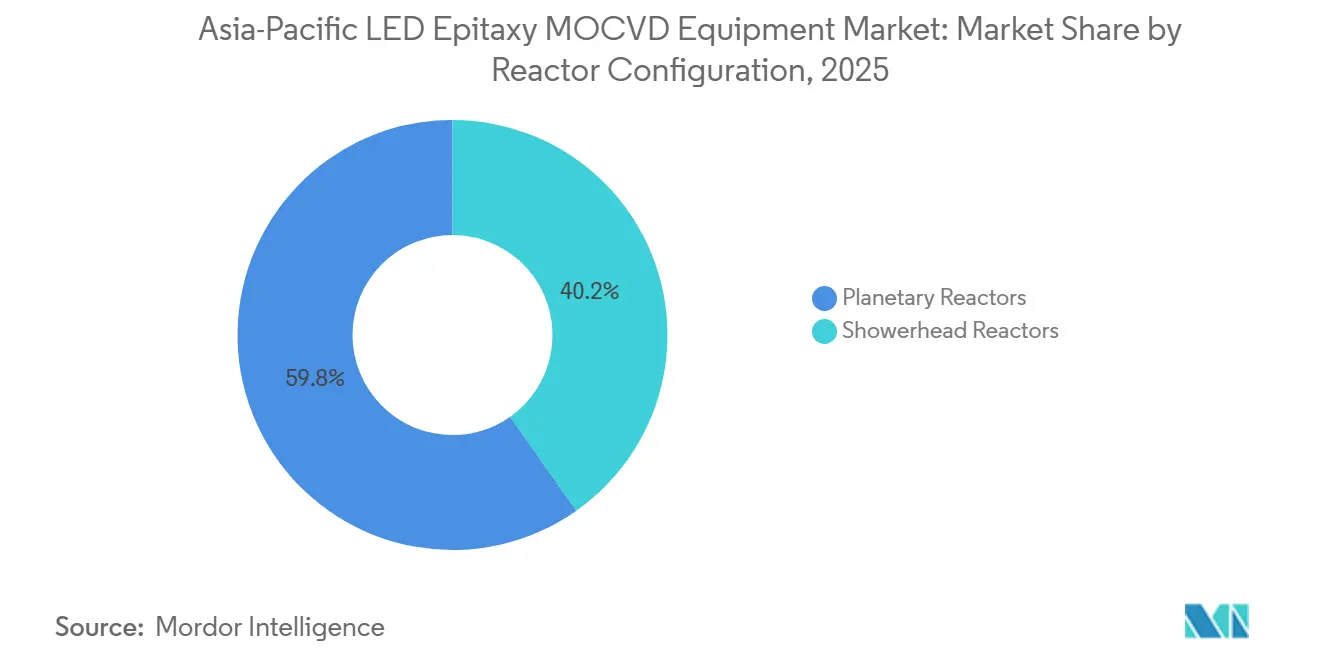

- By reactor configuration, planetary reactors captured 59.78% of the market share in 2025, while the showerhead reactors segment is set to grow at a 13.72% CAGR through 2031.

- By end user, integrated LED manufacturers held 69.64% share in 2025, yet the merchant foundries and merchant Epi suppliers segment is positioned to post a 13.47% CAGR during 2026-2031.

- By country, China accounted for 40.71% of the market share in 2025 and is forecast to post a 13.81% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia contributes to a system defined not by any single geography but by the interaction of many. The global led epitaxy mocvd equipment market data by Mordor Intelligence represents that combined structure.

Asia-Pacific LED Epitaxy MOCVD Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Subsidies for Compound-Semiconductor Fabs in China | +3.2% | China, spill-over to Southeast Asia | Medium term (2-4 years) |

| Surge in Demand for Mini and Micro-LED Displays | +2.8% | Global, APAC core (China, Taiwan, South Korea) | Short term (≤ 2 years) |

| Shift to 150 mm and 200 mm GaN Wafers for Cost Reduction | +2.1% | Global, early adoption in Taiwan and Japan | Medium term (2-4 years) |

| Increasing Adoption of UV-C LED Disinfection Systems | +1.6% | Global, accelerated in North America, Europe, APAC healthcare | Long term (≥ 4 years) |

| AI-Driven In-Situ Metrology Integration Reducing Yield Loss | +1.3% | Global, concentrated in advanced fabs | Short term (≤ 2 years) |

| Circular Reactor Refurbishment Programs Lowering CapEx | +0.9% | APAC Tier-2 cities, emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Subsidies for Compound-Semiconductor Fabs in China

China’s Big Fund Phase 3 set aside USD 47.5 billion to accelerate domestic tool adoption, with quotas stipulating that half of new equipment purchases come from local vendors. Domestic penetration rose from 25% in 2024 to 35% in 2025, directly lifting shipments for NAURA Technology Group and Advanced Micro-Fabrication Equipment Inc. Provincial tax holidays and subsidized industrial parks have cut effective fab capex by up to 30%, unlocking incremental orders for multi-wafer reactors. Gallium resource dominance further aligns state incentives with supply-chain localization. Neighboring Malaysian and Vietnamese LED makers are already sourcing Chinese tools to qualify for reduced-tariff trade corridors, reinforcing the driver’s regional spill-over effect.

Surge in Demand for Mini and Micro-LED Displays

Omdia projects global micro-LED display revenue to double between 2025 and 2026, then scale to USD 6.8 billion by 2032.[1]Omdia Research Team, “Micro-LED Display Revenue to Reach USD 6.8 Billion by 2032,” Omdia, omdia.tech.informa.com Mini-LED TV shipments climbed 100% year-over-year to 8.2 million units in 2024, lifting demand for narrow-binning epitaxial wafers. Display suppliers now require ±2.5 nm wavelength tolerance, prompting migration from planetary to showerhead reactors. Veeco’s Lumina series logged repeat orders in 2026 for indium-phosphide lasers that support AI-server optical links, highlighting cross-market synergies. Although chip-on-board backlighting faces oversupply risk, adoption in automotive dashboards and augmented-reality headsets is absorbing idle epi capacity.

Shift to 150 mm and 200 mm GaN Wafers for Cost Reduction

Moving from 100 mm to larger GaN wafers cuts die cost by up to 40% and improves material utilization. Imec and Azzurro demonstrated 200 mm GaN-on-silicon epi in 2024, validating the path toward high-volume adoption.[2]Imec Press Office, “Imec and Azzurro Demonstrate 200 mm GaN-on-Si Epitaxy,” Imec, imec-int.com Veeco secured orders for its Propel 300 mm system in 2025, showing rising interest in even broader diameters.[3]Veeco Investor Relations, “Veeco Receives Order for Propel 300 mm GaN-on-Si System,” Veeco, ir.veeco.com Larger substrates also lower edge-exclusion losses, an advantage for dense mini-LED arrays. Planetary platforms can be retrofitted for 150 mm, yet 200 mm migration generally favors showerhead architectures designed for tighter thermal envelopes. While capital budgets stretch, the wafer-size transition remains integral to long-run cost curves across lighting, display, and power-device lines.

Increasing Adoption of UV-C LED Disinfection Systems

Rapid efficiency gains have positioned UV-C LEDs to replace mercury lamps in residential point-of-use purifiers and municipal treatment plants, with wall-plug efficiency now triple the 2015 baseline. Module suppliers such as MASSPHOTON are building AlGaN epi stacks in Taiwanese and Chinese foundries for export to North American and European hygiene markets. Healthcare retrofits and automotive cabin-air systems extend the demand horizon well into the next decade. Technical hurdles remain, because threading-dislocation density and quantum-efficiency droop below 270 nm call for high-temperature reactors with strict III-V ratio control. This complexity supports equipment differentiation and keeps unit pricing resilient despite rising volumes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost of Multi-Wafer MOCVD Tools | -2.4% | Global, acute in emerging markets and Tier-2 cities | Short term (≤ 2 years) |

| Oversupply Risk in LED Backlighting Market | -1.8% | APAC core (China, Taiwan, South Korea) | Short term (≤ 2 years) |

| Volatile Trimethylgallium and Ammonia Supply Chains | -1.2% | Global, concentrated impact in China and Taiwan | Medium term (2-4 years) |

| Shortage of Experienced Epitaxy Engineers in Tier-2 Cities | -0.7% | China Tier-2 cities, Southeast Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Multi-Wafer MOCVD Tools

State-of-the-art 200 mm batch reactors carry USD 3-5 million price tags, a hurdle for fabs with annual sales below USD 50 million. Although Alliance MOCVD and Heraeus Covantics offer 30-40% discounts on refurbished 100 mm equipment, availability of newer 150 mm or 200 mm tools in the secondary market is limited. Long four-to-six-year payback periods discourage greenfield investment when demand visibility narrows. Leasing structures are emerging in Taiwan and Japan, yet mainland China lenders remain cautious, keeping financing channels constrained. The capex burden therefore delays technology transitions and tempers short-term shipment spikes for the Asia-Pacific LED epitaxy MOCVD equipment market.

Oversupply Risk in LED Backlighting Market

Excess chip-on-board capacity, estimated at over 50,000 m² per month in 2024, has already compressed commodity LED prices. AIXTRON’s revenue slipped 12% year-over-year to EUR 556.6 million (USD 628.9 million) in 2025, as LED tool orders softened after the 2023-2024 build-out. OLED substitution in premium mobile screens further erodes backlight demand, prompting LED houses to pivot toward micro-LED and automotive lighting. Re-qualification of existing reactors for tighter micro-LED specs entails downtime and incremental spending, pressuring margins. This oversupply drag remains a tangible headwind for near-term growth across the Asia-Pacific LED epitaxy MOCVD equipment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By LED Material System: GaN Dominance Meets AlGaN Acceleration

GaN platforms anchored 68.86% of the market share in 2025, thanks to entrenched use in general lighting, backlighting, and automotive headlamps. Mature precursor ecosystems and substrate optionality keep GaN die costs competitive, reinforcing the Asia-Pacific LED epitaxy MOCVD equipment market’s installed base advantage. Taiwan Semiconductor Manufacturing Company’s USD 2 billion gallium recycling program is further insulating GaN supply from export volatility. AlGaN UV-C devices sit at a smaller baseline yet carry a 13.24% forecast CAGR, buoyed by stringent hygiene mandates in water-treatment and healthcare facilities. Tight emission regulations in Europe and North America are already spurring municipal retrofit projects, translating into firm tool orders for high-temperature reactors that can sustain >1,100 °C growth windows.

Supply-chain specialization is deepening. Chinese and Taiwanese foundries are ramping AlGaN epi pilot lines, leveraging AI-driven in-situ metrology to tackle high threading-dislocation density. Western vendors, meanwhile, are redirecting arsenide-phosphide reactor roadmaps toward power electronics and solar concentrator markets, allowing domestic APAC players to consolidate GaN LED share. The Asia-Pacific LED epitaxy MOCVD equipment industry therefore expects GaN to remain the revenue anchor, while AlGaN provides the incremental growth zest that lifts blended margins.

By Wafer Size Capability: 200 mm Migration Reshapes Economics

In 2025, the 150 mm segment accounted for 46.39% of the market share, reflecting its long-standing role in volume LED manufacturing. Yet the 200 mm and above category is charted to post a 13.63% CAGR, as larger substrates lower per-die cost and align with mainstream silicon fab logistics. Utilization improvements stem from smaller edge exclusion zones, which drop from near 20% on 100 mm wafers to roughly 8-10% on 200 mm lots, enhancing effective capital-per-square-centimeter economics. Veeco’s Propel platform, capable of seamless 300 mm transitions, illustrates equipment makers’ push to future-proof customer roadmaps.

The transition, however, is uneven. Japanese and Taiwanese IDMs have re-purposed legacy DRAM cleanrooms for GaN epi, minimizing incremental infrastructure spend, whereas many mainland Chinese fabs must finance entirely new bulk-gas and abatement systems for 200 mm readiness. Sapphire cost and defectivity currently limit some UV-C and laser applications to 150 mm, preserving a multi-diameter ecosystem. Overall, migration dynamics underscore how wafer-size shifts can swing capex timing for the Asia-Pacific LED epitaxy MOCVD equipment market.

By Reactor Configuration: Showerhead Gains on Uniformity Demands

Planetary reactors accounted for 59.78% of the market share in 2025 because batch processing delivers attractive cost-per-wafer metrics for commodity LEDs. They remain the workhorse for general lighting nodes that tolerate ±5 nm wavelength spread. Showerhead architectures, nevertheless, are forecast to grow 13.72% a year through 2031 as mini-LED, micro-LED, and power-device customers demand sub-±2.5 nm uniformity. Showerhead designs also push trimethylgallium utilization above 40%, a key hedge against gallium price spikes.

Adoption further benefits from AI-enhanced optical monitors that allow real-time doping corrections, reducing tool downtime linked to off-spec lots. The premium price delta between designs narrows when yield-driven rework costs are factored in, accelerating crossover in advanced fabs. Over time, expert consensus anticipates a dual-framework landscape; planetary reactors servicing high-volume, lower-spec lighting, and showerhead tools anchoring differentiated display and power segments within the Asia-Pacific LED epitaxy MOCVD equipment market.

By End User: Foundry Model Gains Traction

Integrated device makers held 69.64% of the market share in 2025 as vertical control of epi, chip, and package lines safeguarded intellectual property and ensured supply certainty. Yet fabless design houses focusing on AR glasses, horticulture, and UV-C niches increasingly outsource epitaxy to merchant foundries, propelling a 13.47% CAGR for the foundry cohort through 2031. The Asia-Pacific LED epitaxy MOCVD equipment market, therefore, mirrors the silicon logic playbook, where scale foundries drive capital efficiency through multi-customer load balancing.

Ennostar, formed by the 2025 merger of Epistar and Lextar, has repositioned itself as a pure-play epi-and-chip foundry, underpinning Taiwan’s ecosystem depth. Mainland champions Sanan Optoelectronics and Silan Azure are likewise building 200 mm lines that court foreign fabless entrants drawn by local subsidies. Equipment adoption skews toward showerhead tools when foundries target micro-LED or UV-C verticals, reinforcing how customer mix steers reactor selection patterns across the Asia-Pacific LED epitaxy MOCVD equipment market.

Geography Analysis

China generated 40.71% of regional revenue in 2025 and is projected to register a 13.81% CAGR to 2031. Big Fund Phase 3 incentives, combined with Beijing’s 50% local-equipment mandate, continue to push domestic reactor suppliers up the learning curve. NAURA Technology Group, now the fifth-largest global MOCVD vendor, is shipping multi-wafer tools into both LED and power GaN fabs, leveraging China’s 98% hold over refined gallium to lock in precursor security. Nevertheless, backlight oversupply weighs on several coastal provinces where subsidies had spurred over-aggressive 2023-2024 build-outs. Authorities are responding by steering credit lines toward micro-LED and power electronics, keeping the Asia-Pacific LED epitaxy MOCVD equipment market aligned with next-generation demand profiles.

Taiwan remains the region’s precision epi nucleus. Ennostar’s USD 780 million 2024 revenue underscores continued leadership in mini-LED and micro-LED wafers for premium TVs, automotive dashboards, and AR devices. Island foundries benefit from co-location with backend OSATs, trimming cycle times for display integrators. Taiwan Semiconductor Manufacturing Company’s USD 2 billion gallium-recycling investment also underwrites GaN supply security, damping raw-material volatility that complicates mainland procurement. These strengths collectively position Taiwan as the highest-value epi service locale within the Asia-Pacific LED epitaxy MOCVD equipment industry.

Japan, South Korea, and the remainder of Southeast Asia contribute the balance of regional spending. Tokyo Electron logged JPY 1,731,715 million (USD 12.1 billion) net sales for the nine months ended December 2025, though LED-specific MOCVD remains a niche side business. Japanese incumbents Nichia and Toyoda Gosei sustain in-house epi mainly for automotive and UV-C LED programs. South Korea’s Samsung and LG Display channel most display capex into OLED, yet exploratory micro-LED pilots proceed in collaboration with Taiwanese epi partners. In Southeast Asia, refurbished tool availability lowers entry barriers for Vietnamese and Malaysian fabs eager to capture ASEAN smart-lighting demand. Local expansion rounds out the geographically diversified base that now supports the broader Asia-Pacific LED epitaxy MOCVD equipment market.

The led epitaxy mocvd equipment market is analyzed by Mordor Intelligence across multiple other geographies. This is complemented by country-specific insights for Taiwan, China, and Japan, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The Asia-Pacific LED epitaxy MOCVD equipment market remains moderately consolidated. AIXTRON and Veeco together dominate Western supply, splitting planetary and showerhead segments, respectively. AIXTRON booked EUR 556.6 million (USD 628.9 million) revenue in 2025, down 12% year-over-year, attributing weakness to cyclical LED backlighting cuts. Veeco reported USD 664.3 million 2025 revenue, with compound-semiconductor systems contributing USD 60 million and projected to rise by one-third in 2026 on micro-LED tailwinds. Chinese entrants NAURA and AMEC leverage state funding to undercut Western pricing, driving rapid share gains across commodity GaN lines and cementing local tool preference under import-substitution policies.

Strategic focus is diverging. Western vendors are prioritizing high-margin micro-LED, InP laser, and power GaN nodes that reward uniformity and advanced metrology integration. Veeco’s Lumina+ launch in 2025 and subsequent Rocket Lab order underscore that repositioning toward arsenide-phosphide solar and space-grade applications. Chinese suppliers concentrate on high-volume mid-power LEDs where cost per wafer remains paramount, using government procurement quotas and interest-free loans to scale. Across both camps, AI-enabled in-situ sensors from providers such as LayTec and Nanotronics are fast becoming standard, embedding switching costs and creating an ancillary ecosystem around process analytics.

Refurbishment specialists like Alliance MOCVD and Heraeus Covantics are emerging disruptors, offering circular-economy business models that shave 30-40% off list prices for certified pre-owned tools. Their model taps latent demand among Tier-2 fabs unable to justify new-tool purchases amid price pressure. At the same time, ISO 19694-7:2024 greenhouse-gas metrics are now embedded in buyer RFQs, tilting preference toward reactors with lower per-wafer CO₂e footprints. This sustainability filter reinforces the competitive gap between vendors with advanced abatement integration and firms still dependent on legacy exhaust architectures, shaping long-term positioning inside the Asia-Pacific LED epitaxy MOCVD equipment market.

Asia-Pacific LED Epitaxy MOCVD Equipment Industry Leaders

AIXTRON SE

Veeco Instruments Inc.

Advanced Micro-Fabrication Equipment Inc. (AMEC)

NAURA Technology Group Co. Ltd.

Taiyo Nippon Sanso Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Veeco Instruments booked multiple Lumina reactors and Spector ion-beam systems from a global optical-communications laser maker to scale indium-phosphide transceiver volumes.

- November 2025: Veeco received a Propel 300 mm GaN-on-silicon reactor order for micro-LED and power applications, expanding its large-wafer footprint.

- October 2025: Veeco introduced the Lumina+ batch MOCVD tool and secured a multi-system order from Rocket Lab to double space-grade solar-cell output under the CHIPS and Science Act.

- October 2025: Ennostar finalized the merger of Epistar and Lextar, creating a vertically integrated LED supplier with 2024 revenue of NTD 24.387 billion (USD 780 million).

Asia-Pacific LED Epitaxy MOCVD Equipment Market Report Scope

The LED Epitaxy MOCVD Equipment Market refers to the segment of the semiconductor equipment industry focused on manufacturing Metal-Organic Chemical Vapor Deposition (MOCVD) systems used for the epitaxial growth of LED materials. These systems are critical for producing high-quality LED wafers, which serve as the foundation for LED devices used in various applications such as lighting, displays, and automotive technologies.

The Asia-Pacific LED Epitaxy MOCVD Equipment Market Report is Segmented by LED Material System (GaN-based LED Epitaxy Systems, AlGaN UV LED Epitaxy Systems, and AlInGaP LED Epitaxy Systems), Wafer Size Capability (Up to 100mm, 150mm, and 200mm and Above), Reactor Configuration (Planetary Reactors, and Showerhead Reactors), End User (Integrated LED Manufacturers, and Epitaxy Foundries and Merchant Epi Suppliers), and Country (China, Taiwan, Japan, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

| GaN-based LED Epitaxy Systems |

| AlGaN UV LED Epitaxy Systems |

| AlInGaP LED Epitaxy Systems |

| Upto 100 mm |

| 150 mm |

| 200 mm and Above |

| Planetary Reactors |

| Showerhead Reactors |

| Integrated LED Manufacturers (IDMs) |

| Epitaxy Foundries and Merchant Epi Suppliers |

| China |

| Japan |

| Taiwan |

| Rest of Asia-Pacific |

| By LED Material System | GaN-based LED Epitaxy Systems |

| AlGaN UV LED Epitaxy Systems | |

| AlInGaP LED Epitaxy Systems | |

| By Wafer Size Capability | Upto 100 mm |

| 150 mm | |

| 200 mm and Above | |

| By Reactor Configuration | Planetary Reactors |

| Showerhead Reactors | |

| By End User | Integrated LED Manufacturers (IDMs) |

| Epitaxy Foundries and Merchant Epi Suppliers | |

| By Country | China |

| Japan | |

| Taiwan | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the expected value of the Asia-Pacific LED epitaxy MOCVD equipment market by 2031?

The market is forecast to reach USD 972.05 million by 2031.

Which wafer size is growing fastest in new reactor purchases?

200 mm and above segment is projected to grow at a 13.63% CAGR over 2026-2031.

Why are showerhead reactors gaining share against planetary designs?

Showerhead platforms deliver tighter wavelength uniformity and higher precursor utilization, which are essential for mini-LED and micro-LED production.

How is China influencing regional equipment demand?

Beijing’s Big Fund Phase 3 subsidies and a 50% domestic-equipment mandate are accelerating orders for mainland MOCVD suppliers.

Which material system shows the highest growth potential beyond GaN?

AlGaN UV-C LED epitaxy is projected to register a 13.24% CAGR due to rising disinfection applications.

How do refurbished reactors impact smaller fabs?

Certified refurbishment can cut capital outlays by up to 40%, enabling Tier-2 manufacturers to enter the market with lower financial risk.

Page last updated on: