Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

| Market Size (2026) | USD 3.58 Billion |

| Market Size (2031) | USD 5.67 Billion |

| Growth Rate (2026 - 2031) | 9.63% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China High-Voltage Direct Current (HVDC) Transmission Systems Market Analysis by Mordor Intelligence

The China High-Voltage Direct Current Transmission Systems Market size is estimated at USD 3.58 billion in 2026, and is expected to reach USD 5.67 billion by 2031, at a CAGR of 9.63% during the forecast period (2026-2031).

Rapid build-out of ultra-high-voltage (UHV) corridors, rising offshore-wind connections, and sustained policy support under the 14th Five-Year Plan are steering the market toward double-digit expansion.[1]State Grid Corporation of China, “Annual Investment Plan 2026,” SGCC.COM.CN Converter-station investments dominate capital outlays because valve-hall, transformer, and cooling assemblies account for almost half of project costs, while submarine-cable demand is accelerating as coastal provinces integrate far-from-shore wind farms.[2]Jiangsu Zhongtian Technology, “Offshore HVDC Cable Portfolio,” CHINAZTT.COM Beijing’s decision to guarantee cost recovery through distance-indexed transmission tariffs has trimmed financing risk and encouraged provincial grid companies to lock in long-term loans at concessional rates.[3]National Development and Reform Commission, “Grid Tariff Adjustment Notice No. 27 (2025),” NDRC.GOV.CN Foreign vendors such as Hitachi Energy still supply niche components at ±800 kV and above, yet the value chain is steadily localizing as domestic suppliers ramp press-pack IGBT and XLPE-cable capacity.

Key Report Takeaways

- By transmission type, overhead links led with 64.8% of the China high-voltage direct current transmission systems market share in 2025; submarine systems are forecast to post the fastest 12.0% CAGR through 2031.

- By component, converter stations held 54.5% revenue share in 2025, while transmission-medium cables are poised to expand at a 10.8% CAGR to 2031.

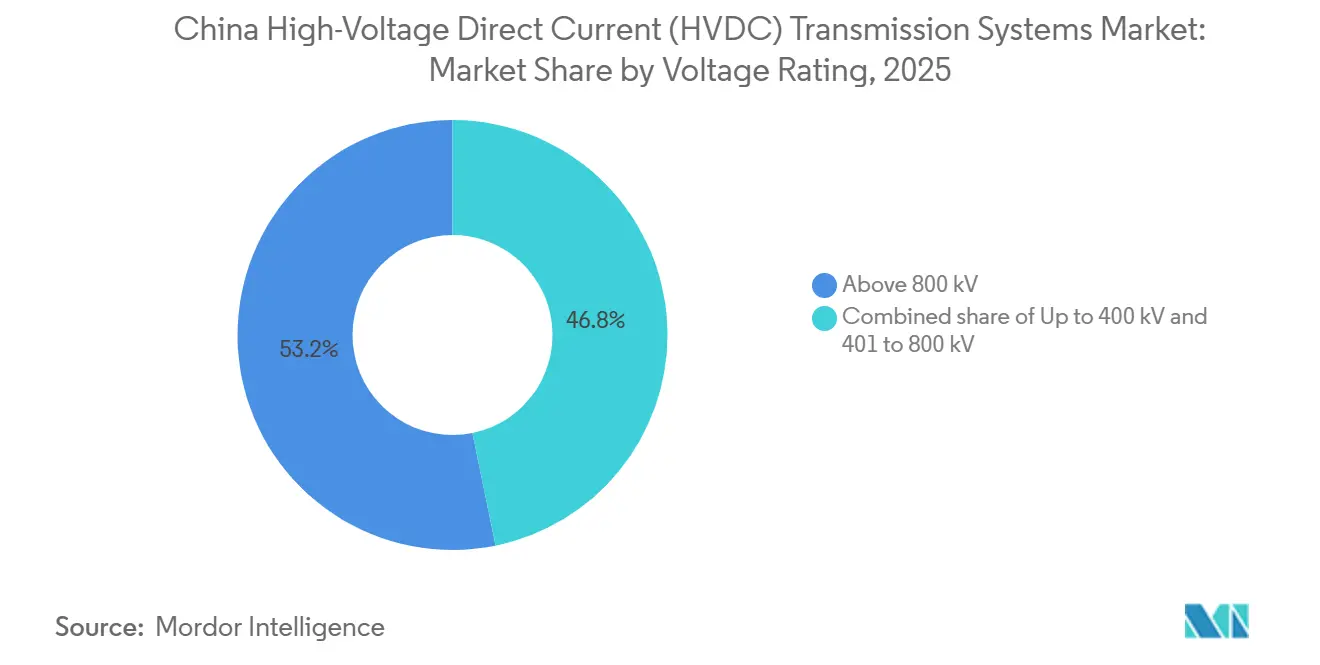

- By voltage rating, above-800 kV corridors commanded 53.2% of the China high-voltage direct current transmission systems market size in 2025 and are projected to grow at a 10.1% CAGR during the period.

- State Grid Corporation and China Southern Power Grid awarded 94% of engineering-procurement-construction contracts in 2025, underscoring concentrated buyer power within the Chinese high-voltage direct current transmission systems market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

China High-Voltage Direct Current (HVDC) Transmission Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Policy push under 14th Five-Year Plan | 2.80% | Xinjiang, Qinghai, Gansu, Sichuan | Medium term (2-4 years) |

| Accelerating West-to-East renewable power transfer | 2.50% | Western generation hubs to Eastern load centers | Long term (≥4 years) |

| Surge in large-scale offshore wind HVDC links | 1.90% | Jiangsu, Guangdong, Fujian | Medium term (2-4 years) |

| Flexible VSC-HVDC demand from hyperscale data centers | 1.20% | Beijing-Tianjin-Hebei, Yangtze River Delta, Pearl River Delta | Short term (≤2 years) |

| Semiconductor and EV-battery clusters’ high-quality-power needs | 0.90% | Jiangsu, Guangdong, Sichuan, Shaanxi | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Policy Push Under 14th Five-Year Plan

Twelve new UHV corridors received central approval, turning HVDC investment from discretionary to mandatory for provincial operators. State Grid earmarked CNY 600 billion (USD 83 billion) for grid capex in 2026, 45% of which targets HVDC converter stations and ±800 kV lines.[4]State Grid Corporation of China, “Annual Investment Plan 2026,” SGCC.COM.CN Tariff guarantees indexed to distance allow sponsors to close 15-year policy-bank loans at 3.2% interest, widening the spread versus commercial funding and shortening breakeven timelines. The mechanism has already de-risked the Xizang-Guangdong project despite its 23-year nominal payback horizon. Renewable-integration mandates that call for 150 GW of wind and solar to flow eastward by 2030 further lock in demand for flexible VSC-HVDC topologies with black-start and frequency-support capability.

Accelerating West-to-East Renewable Power Transfer

Xinjiang recorded double-digit curtailment when the existing Hami-Chongqing link hit 85% loading. The upcoming Gansu-Zhejiang ±800 kV VSC corridor will shift 8 GW across 2,370 km and enable reverse flow during photovoltaic peaks, easing thermal limits on the AC grid. Qinghai’s solar base shows why extra transfer capacity matters: by 2025, the province’s peak load of 9.2 GW absorbed barely one-quarter of its installed capacity, making sub-3% HVDC losses decisive for revenue preservation. Every percentage-point loss above 3% wipes USD 28 million from annual earnings on an 8 GW line operating 6,000 full-load hours.

Surge in Large-Scale Offshore Wind HVDC Links

Beyond 50 km from shore, AC cables require costly reactive-compensation platforms. Jiangsu’s Rudong project proved that a ±400 kV VSC link can remove two-thirds of these platforms and shrink total installed cost by 18%. Guangdong faces typhoon forces that raise armored-cable prices to USD 2.8 million per km, yet developers accept the premium because 40-year design life and lower upkeep outweigh the upfront outlay. Domestic suppliers commanded 68% of submarine-cable orders in 2025 thanks to 9-month delivery cycles that undercut European imports constrained by trans-Pacific logistics.

Flexible VSC-HVDC Demand from Hyperscale Data Centers

China’s East-West Computing Resource initiative pushes 30% of new data-hall capacity toward western regions, where weak AC grids threaten voltage stability. VSC-HVDC feeders modulate active and reactive power in 10 ms, meeting 99.99% uptime guarantees without static VAR compensators. The Zhangbei four-terminal DC grid removed 12 such compensators and freed 18 ha of substation land, cutting auxiliary spend by USD 340 million. Operators like Alibaba Cloud now co-finance dedicated DC feeders to avoid 4-6 annual voltage events that breach service-level agreements.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Very high upfront CAPEX and extended payback | -1.4% | Nationwide, acute in western provinces | Long term (≥4 years) |

| Grid-code complexity for multi-terminal HVDC meshing | -0.8% | Pilot sites in Xizang, Sichuan, Guangdong, Hebei | Medium term (2-4 years) |

| Domestic supply bottleneck for ≥±800 kV valves | -0.6% | Hunan, Shaanxi, Jiangsu | Short term (≤2 years) |

| Environmental approvals for new corridors | -0.5% | Qinghai, Gansu, Xizang, Sichuan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Very High Upfront CAPEX and Extended Payback

The Gansu-Zhejiang ±800 kV VSC project costs USD 612,500 per MW, 28% above a comparable 1,000 kV AC route. Provinces must co-fund converter stations, yet face tariff caps of CNY 0.05 per kWh that jeopardize debt coverage ratios below 1.2×. Xizang-Guangdong assumes 6,800 operating hours, but hydropower seasonality could stretch payback to 28 years if utilization falls. Each unplanned outage day erodes project NPV by USD 4.2 million, making predictive maintenance on cooling loops and DC filters central to investment returns.

Grid-Code Complexity for Multi-Terminal HVDC Meshing

The three-terminal Xizang-Guangdong corridor must stabilize DC voltage across AC networks with dissimilar short-circuit ratios, a scenario not fully addressed by IEC 61975. The smaller Zhangbei ±500 kV grid logged three DC-bus excursions in its first 18 months and had to de-rate transfer 12% for stability. At ±800 kV, hybrid mechanical-semiconductor DC breakers cost USD 10 million apiece, and only NR Electric and Xuji Group hold type-test certification, creating a two-vendor bottleneck that can raise procurement prices by 35%.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Transmission Type: Offshore Wind Propels Submarine Surge

Overhead corridors held 64.8% of the Chinese high-voltage direct current transmission systems market in 2025, led by projects such as the 915 km Longdong-Shandong line, whose per-kilometer cost of CNY 1.5-2 million remains 60% below submarine alternatives. Submarine links, however, are forecast to post a 12.0% CAGR to 2031 as Jiangsu and Guangdong fast-track far-from-shore wind farms that demand ±400 kV VSC technology.

The China high-voltage direct current transmission systems market size for submarine links benefits from cost savings achieved by eliminating multiple AC platforms. The Rudong project, operational since 2024, removed three intermediate stations and cut the total bill by 18%. Offshore adoption is further bolstered by domestic cable makers that offer 9-month lead times and renminbi pricing, a 4-6% cost edge over European peers. Underground HVDC remains a niche option for short urban segments where overhead routes face right-of-way hurdles, as seen in Beijing’s 12 km section priced at CNY 8.2 million per km.

By Component: Converter Complexity Sustains Station Dominance

Converter stations accounted for 54.5% of the Chinese high-voltage direct current transmission systems market share in 2025. A single ±800 kV VSC station demands 480 high-rating IGBT modules, converter transformers with ±15% tap range, and sophisticated cooling, pushing electrical procurement alone above USD 680 million. Transmission-medium cables are projected to grow at a 10.8% CAGR through 2031 on the back of offshore-wind tie-ins and conductor uprating of aging ±500 kV corridors.

Domestic firms control 68% of medium-voltage content, yet valve-grade 8-inch wafer fabs remain scarce, forcing 60% import content at the VSC top tier. Still, suppliers able to bundle civil works, HVAC, and fire suppression alongside electrical scope can capture more than half of converter-station value, cementing a competitive moat for integrated players inside the China high-voltage direct current transmission systems market.

By Voltage Rating: Ultra-High Voltage Cements Efficiency Lead

Links above 800 kV captured 53.2% of 2025 revenue and will grow at a 10.1% CAGR. The ±1 100 kV Changji-Guquan and Zhundong-Wannan lines ship 12 GW each over 3,200 km with losses under 2.8%, outperforming lower-voltage corridors by 70 bps. The China high-voltage direct current transmission systems market size attached to above-800 kV projects is buoyed by fuel savings: trimming losses from 3.5% to 2.6% on a 10 GW path saves USD 72 million a year.

The 401-800 kV bracket suits medium-range corridors up to 1,500 km, while up-to-400 kV ratings dominate offshore wind and point-to-point data-center feeders where compact stations are valued. Only two global vendors can deliver 8.5 kV thyristors needed for ±1 100 kV valves, a constraint that prolongs lead times to 18 months and reinforces foreign participation in the ultra-high-voltage tier.

Geography Analysis

Generation in the western provinces of Xinjiang, Qinghai, Gansu, and Xizang totaled 118 GW of wind and solar in 2025, yet these regions house limited local demand. They exported 87 TWh over HVDC links to Jiangsu, Zhejiang, Guangdong, and Shandong, which together consumed 62% of transmitted power. Transmission bottlenecks surfaced when curtailment in Xinjiang topped 12% during shoulder months, underscoring the lag between renewable build-out and corridor approvals.

Coastal provinces are mitigating import dependence by bankrolling local offshore wind. Jiangsu committed CNY 18 billion in 2025 for submarine HVDC cables that will connect 27.3 GW of turbines planned through 2030. Guangdong is adopting armored XLPE designs to survive typhoon loading, accepting USD 2.8 million per-km cable costs in exchange for a 40-year life that cuts operating spend.

Sichuan operates as a hydropower swing producer inside the emerging Xizang-Guangdong three-terminal network. It injects 2 GW in the monsoon season and withdraws energy during dry months, effectively using the DC corridor as a long-distance storage asset. The model illustrates how multi-terminal projects can balance regional supply diversity once grid-code challenges are resolved.

Regulatory Landscape

China's HVDC transmission regulatory environment is primarily shaped by the National Energy Administration (NEA) and the National Development and Reform Commission (NDRC), with implementation at the utility level led by State Grid Corporation of China and China Southern Power Grid. For long-distance HVDC corridors, tariff and cost-recovery mechanisms remain a key bankability lever, including NDRC's distance-indexed transmission tariff approach referenced in the report context (Grid Tariff Adjustment Notice No. 27 (2025)), which supports long-tenor financing for cross-provincial links.

Technical compliance is also moving toward tighter standardization for VSC-HVDC equipment and lifecycle assurance. GB/T 30553-2023 for VSC-HVDC power transmission entered implementation in June 2024, and DL/T 1793-2025 (manufacturing supervision requirements for VSC-HVDC transmission equipment) was issued in December 2025 and implemented in June 2026, reinforcing expectations around factory inspection, traceability, and acceptance testing for converter valves and related station equipment.

Competitive Landscape

State Grid and China Southern Power Grid dominated 94% of EPC awards in 2025, establishing a regulated duopoly that defines technical standards and procurement cycles. In equipment, Hitachi Energy, Siemens Energy, and ABB collectively supplied 42% of converter transformers and semiconductors for projects at ±800 kV and above. Domestic challengers, TBEA, NR Electric, Xuji Group, and China XD, captured 68% in the ±500 kV space by offering 25-30% price concessions and 9-month lead times.

White-space opportunities lie in VSC systems, where 62% of valve content still relies on imports. Firms capable of localizing 8-inch wafer production could unlock a USD 1.8 billion addressable market by 2031. Procurement data also show a rising share for Shenzhen Sieyuan Electric, which won 12% of protection-and-control lots in the March 2025 tender by pricing 18% below incumbents.

Technology strategies are diverging. State Grid pilots hybrid-commutated converters that cut valve count by 30% and could save USD 85 million on an 8 GW link, though commercialization awaits IEC-62501 certification expected in 2028. China Southern Power Grid pursues meshed DC grids, aiming to translate its record with flexible ±160 kV demos into large-scale ±800 kV networks once grid-code revisions mature.

China High-Voltage Direct Current (HVDC) Transmission Systems Industry Leaders

State Grid Corporation of China

Hitachi Energy

NR Electric

TBEA

Siemens Energy

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The 15th Five-Year Plan (2026-2030) grid build-out creates near-term whitespace for UHVDC execution and equipment supply, especially for converter stations and VSC-based architectures on weak-grid and renewable-heavy sending ends. State Grid's 4 trillion yuan fixed-asset investment plan for 2026-2030, paired with visible 2026 project activity (including advancing multiple UHVAC/UHVDC projects with combined investments above 200 billion yuan), supports a sustained pipeline for valves, converter transformers, control and protection systems, and station auxiliaries, consistent with converter stations as the largest component pool in this market.

The 2026 commissioning and new starts also point to execution opportunities across both inland corridors and coastal integration. The Shaanbei-Anhui +/-800 kV UHVDC project entered operation in June 2026 (8 million kW rated capacity, 1,055 km), while construction milestones on the Xizang-Guangdong UHVDC link (2,681 km, 10 million kW) reinforce demand for high-altitude construction capability, long-span line hardware, and reliability-focused station designs. Alongside these trunk projects, the shift toward VSC and hybrid LCC/VSC solutions increases the focus on domestic localization of high-end valve content and supports suppliers that can tighten lead times for submarine and land cable systems, as delivery cycles and project schedules become more differentiating.

Recent Industry Developments

- June 2026: State Grid Corporation of China put the Shaanbei-Anhui +/-800 kV UHVDC project into operation, a 1,055 km link rated at 8 million kW. As the first UHVDC project commissioned under the 15th Five-Year Plan (2026-2030), it reinforces the near-term build cycle for converter stations and UHV-class equipment across inland corridors.

- September 2025: Construction began on the +/-800 kV Xizang-Guangdong HVDC transmission line to deliver power to the Guangdong-Hong Kong-Macao Greater Bay Area. The 2,681 km project carries a reported investment of 53.2 billion yuan and adds a marquee UHVDC corridor that elevates demand for high-reliability station packages, line hardware, and controls suited to complex terrain.

- July 2024: State media reported on the Gansu-to-Zhejiang UHVDC project, which is planned to transmit more than 36 billion kWh annually across multiple provinces from western generation to eastern load centers. The scale of annual energy transfer underscores why ultra-long-distance HVDC corridors remain central to West-to-East power delivery, supporting continued procurement of UHVDC converters and associated transmission assets.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue generated from HVDC transmission systems deployed in China, including converter stations and the transmission medium used to move bulk electricity over long distances or for grid interconnections.

Scope exclusions: Routine operation and maintenance services, general AC grid equipment, and power generation assets are not counted unless they are part of an HVDC system package.

Segmentation Overview

- By Transmission Type

- Submarine HVDC Transmission System

- Overhead HVDC Transmission System

- Underground HVDC Transmission System

- By Component

- Converter Stations

- Transmission Medium (Cables)

- Others (Control & Protection Systems, Reactive Power Equipment, Accessories)

- By Voltage Rating

- Up to 400 kV

- 401 to 800 kV

- Above 800 kV

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by mapping the China HVDC project environment and the demand signals that can be checked year by year. We used public sources such as National Energy Administration releases, National Bureau of Statistics data series, State Grid and other grid-operator publications, China Electricity Council updates, and China customs trade statistics for electrical equipment to understand investment cycles and equipment movement.

To convert these signals into a workable market model, we also reviewed company annual reports, investor presentations, tender announcements, and reputable press coverage tied to major UHVDC corridors. A paid subscription for company financials and news was used to cross-check supplier exposure, and a patent database was referenced to track active technology focus areas, such as converter and control improvements. These examples are not exhaustive, and additional sources were used to compile the dataset, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work focused on confirming how much of grid investment turns into HVDC system revenue in China, and when that revenue is recognized across the project cycle. We spoke with system suppliers, EPC-facing contacts, component specialists, and utility or project-side experts to confirm the typical voltage-rating mix, the converter station scope included in system packages, and pricing movement for cables and power electronics.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 13% | |

| Mid tier: 49% | Functional/Unit leaders: 40% | |

| Smaller Players: 17% | Managers: 47% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where China grid capex direction, publicly announced UHVDC corridor additions, and project pipeline timing are translated into an addressable HVDC system revenue pool, then converted using factors reflecting equipment intensity and commissioning schedules. The totals were checked with selective bottom-up approximations, such as sampled project-level equipment packages, typical converter station bill-of-material splits, and reasonableness checks on implied pricing for converter stations and the transmission medium.

A few inputs that matter in this market were tracked closely, including the number of HVDC links under development, voltage rating split (up to 400 kV, 401 to 800 kV, and above 800 kV), the share of overhead versus underground or submarine routes, and the relative weight of converter stations versus transmission medium in delivered system value. Where project details were incomplete, gaps were handled by using ranges discussed in interviews and then applying conservative mid-points that align with observed public project patterns.

For the forecast, scenario analysis was used to reflect different outcomes for approval timing, construction pace, and cost inflation, and the final line was selected after aligning with expert views on grid buildout cadence, renewable integration urgency, and supply chain constraints.

Data Validation & Update Cycle

Outputs were validated by comparing implied spend levels against independent signals such as grid investment trends, project commissioning news flow, and the expected mix shift between voltage classes and route types. When large variances showed up, we reviewed assumptions again and checked whether the change came from scope, timing, or pricing.

Before sign-off, the model is reviewed in multiple steps so calculation logic, units, and year alignment remain consistent across inputs. The report is refreshed annually, and interim updates are triggered when material policy moves, major project approvals, or sudden cost swings can change the near-term demand picture. Right before delivery, a final pass is done to ensure the view reflects the latest available public and expert information.

Mordor Intelligence's China High Voltage Direct Current Hvdc Transmission Systems Market Market Sizing Compared With Other Published Estimates

Published market sizes for China HVDC transmission systems can differ more than expected because the counted scope is not always the same, and the timing of when project value is recorded can shift the current-year number. Differences also come from how firms treat ultra-high voltage projects, whether they count only equipment or include EPC and services, and how currency conversion dates are handled.

The main gap drivers in this market are usually whether revenue is limited to HVDC system supply (converter stations plus transmission medium) versus broader grid buildout spend, and whether the study focuses on a narrower segment like very high capacity links. Another frequent issue is refresh cadence, since new corridor approvals and commissioning slippages can quickly change the near-term size. The model therefore uses project timing checks and grid investment context before the final number is locked in by Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.58 B (2026) | |

| Industry Research Publisher A | USD 6.80 B (2026) | Uses a broader definition that appears to include additional components and adjacent electrical equipment beyond delivered HVDC system packages, which inflates the same-year value when compared on a like-for-like basis. |

| Trade Research Outlet B | USD 2.12 B (2025) | Reports China value only for a high-capacity segment (above 2001 MW) rather than the full HVDC transmission systems market, so the figure is structurally smaller even before year differences are considered. |

Taken together, the spread is mostly explained by scope and segment coverage, and only partly by different years. Using clear inclusion rules, project timing logic, and cross-checks against public buildout signals keeps the estimate traceable to repeatable steps, which helps users reconcile why two numbers can both be reasonable but still not comparable.

Key Questions Answered in the Report

What is the current value of the China high-voltage direct current transmission systems market?

The market was valued at USD 3.58 billion in 2026 and is on track to hit USD 5.67 billion by 2031.

Which segment holds the largest China high-voltage direct current transmission systems market share?

Overhead transmission accounted for 64.8% of revenue in 2025, reflecting lower per-kilometer costs on long inland routes.

How fast will submarine HVDC links grow through 2031?

Submarine systems tied to offshore wind are expected to register a 12.0% CAGR, the fastest among transmission types.

Why are converter stations so dominant in project budgets?

Valve halls, transformers and cooling assemblies together absorb more than half of total costs, giving converter stations a 54.5% revenue share in 2025.

Which voltage class is expanding quickest?

Corridors rated above 800 kV, including the world-leading ±1 100 kV lines, are projected to grow at a 10.1% CAGR as developers seek lower line losses over 2 000 km-plus distances.

Who are the major players in equipment supply?

Hitachi Energy, Siemens Energy and ABB lead in ultra-high-voltage components, while domestic firms such as TBEA, NR Electric and Xuji Group dominate the mid-voltage tier.

Page last updated on: