China EV Battery Pack Market Size and Share

Market Overview

| Study Period | 2017 - 2029 |

|---|---|

| Forecast Data Period | 2025 - 2029 |

| Historical Data Period | 2017 - 2023 |

| Market Size (2025) | USD 56.89 Billion |

| Market Size (2029) | USD 69.19 Billion |

| Growth Rate (2025 - 2029) | 5.02% CAGR |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China EV Battery Pack Market Analysis by Mordor Intelligence

The China EV Battery Pack Market size is estimated at 56.89 billion USD in 2025, and is expected to reach 69.19 billion USD by 2029, growing at a CAGR of 5.02% during the forecast period (2025-2029).

China's electric vehicle battery industry is undergoing a profound transformation driven by technological innovation and manufacturing scale. The market structure demonstrates a clear preference for electric vehicle battery pack solutions, with battery electric vehicles (BEVs) commanding approximately 70% of total electric vehicle sales in 2022, while plug-in hybrid electric vehicles (PHEVs) accounted for 28%. This distribution reflects the maturing ecosystem for pure electric vehicles, though PHEVs continue to gain traction, evidenced by their 32% growth in 2022. The industry's evolution is further characterized by the emergence of advanced battery management system technologies and sophisticated manufacturing processes that are reshaping the competitive landscape.

The battery technology landscape is dominated by specific chemistries and form factors that have proven most effective for the Chinese market. Lithium Iron Phosphate (LFP) batteries have emerged as the predominant chemistry, accounting for approximately 80% of total battery consumption in 2022, primarily due to their cost-effectiveness and safety characteristics. In terms of physical configuration, prismatic cells have established themselves as the industry standard, capturing an 87% market share among all battery forms in 2022, owing to their efficient space utilization and manufacturing scalability. The demand for electric car battery solutions continues to rise, driven by these technological advancements.

The manufacturing landscape continues to evolve with significant capacity expansions and technological advancements. Major manufacturers are investing heavily in new production facilities, exemplified by BMW's announcement in 2023 to invest USD 1.4 billion in a new battery manufacturing plant in China. Tesla China has also made strategic moves by applying for clearance to expand its Shanghai plant to include pouch battery cell production, demonstrating the industry's shift toward diversifying EV battery pack form factors and increasing domestic production capabilities.

Strategic developments in 2023 highlight the industry's focus on innovation and market expansion. Polestar's introduction of a new electric SUV with a 315-mile range demonstrates the industry's push toward extended-range vehicles. BYD's launch of the Qin Plus EV in both pure electric and plug-in hybrid variants showcases the industry's commitment to providing diverse powertrain options. The plug-in hybrid segment has shown particular momentum, with a 23% growth recorded in March 2023, indicating evolving consumer preferences and technological maturity in the hybrid space. The expansion of the automotive battery pack market is a testament to these strategic advancements.

China EV Battery Pack Market Trends and Insights

DRIVING THE ELECTRIC REVOLUTION, BYD LEADS THE CHINESE EV BATTERY PACK MARKET, FOLLOWED BY TESLA, WULING, TOYOTA GROUP, AND GAC AION

- The market for electric vehicles in China is huge and is operated by many sellers, but it is largely driven by five major companies, which held more than 50% of the market in 2022. These companies include BYD, Tesla, Wuling, Toyota Group, and GAC Aion. BYD was the largest seller of electric vehicles in China, accounting for around 25.27% of the share in EV sales. The company has strong R&D capabilities with good financial positioning. It is capturing customers through a great pricing strategy and a wide sales and service network across China.

- Tesla held a market share of around 9.72%, making it the second-largest seller of electric vehicles across China. The company focuses on cutting-edge innovations and has solid strategic alliances with producers of several EV parts, including batteries. The company also has a strong sales network across China. The Wuling recorded the third-highest market share, 8.47%, for the electric vehicle sales. The company operates as a subsidiary of Liuzhou Wuling Automobile Industry Co. Ltd. It has a strong hold on the customers of China due to its wide product portfolio offering EVs for various types of customers.

- The fourth-largest player in China EV sales was Toyota Group, accounting for around 7.06% of the market share. The company has a reliable brand image among its customers and sells its products in China through a well-established supply chain network. The fifth-largest player operating in the Chinese EV battery pack market was GAC Aion, maintaining its market share at around 3.71%. Other players selling EVs in China include Chery, Changan, Neta, Li-Auto, and Fengshen.

IN 2022, TESLA, BYD, AND WULING HAD MORE THAN 50% OF CHINA'S PASSENGER CAR MARKET, DRIVING THE MAJOR BATTERY PACK DEMAND

- China is one of the largest electric vehicle markets globally, and the demand for electric vehicles has grown significantly over the past few years. The country has a variety of buyers for electric vehicles, but hatchbacks and SUVs are some of the best-selling segments. Economical drive, affordable pricing, and easy parking are the major factors for the hatchback’s increasing demand, and large head and leg room, large seating capacity, and comfortable drive on various roads due to high ground clearance are some of the factors aiding the sales of the electric SUVs in the country.

- The country has witnessed good sales of the hatchback as people prefer affordability. Wuling Hongguang MINIEV registered significant sales growth in 2022, as it is one of the very affordable full electric cars with good range and limited top speed. It also offers a convertible version, which is attracting consumers. The population of China is showing a positive response to various brands, such as Tesla, owing to the good brand image and wide product offering of EVs. The company is operating as one of the prominent brands in China and registered good sales of models Y and 3 in 2022.

- Most of the electric vehicle market is captured by Chinese brands. Song has also been one of the best sellers of BYD among Chinese consumers, owing to its fully electric powertrain with a large seating capacity. The Chinese EV battery pack market also features a variety of electric SUVs and hatchbacks from various brands. One of the common cars is the BYD Dolphin and Yuan Plus, which registered good sales in 2022. Other cars in the Chinese EV battery pack market include Qin PLUS DM-I, Han DM, and Tang DM.

OTHER KEY INDUSTRY TRENDS COVERED IN THE REPORT

- Government Initiatives and Strong OEM Investments Drive Rapid Growth in Electric Vehicle Sales in China

- The Declining Cost of Lithium-Ion Batteries Drives Demand for Electric Vehicles in China

- Technological Advancements, Economies of Scale, and Supply Chain Efficiency to Lower China's Battery Chemistry Prices from 2023 to 2029, Enabling Electric Vehicle Adoption and Renewable Energy Integration

- New Chinese Electric Vehicle Launches Drive Battery Pack Demand

- There is a dominance of LFP batteries and rising demand for NMC batteries

- China's Rapid EV Growth Drives Demand for Battery Materials, with LFP Batteries Dominating the Market

- China Leads in Electric Vehicle Adoption and Battery Technology Advancements

Segment Analysis: Body Type

Passenger Car Segment in China EV Battery Pack Market

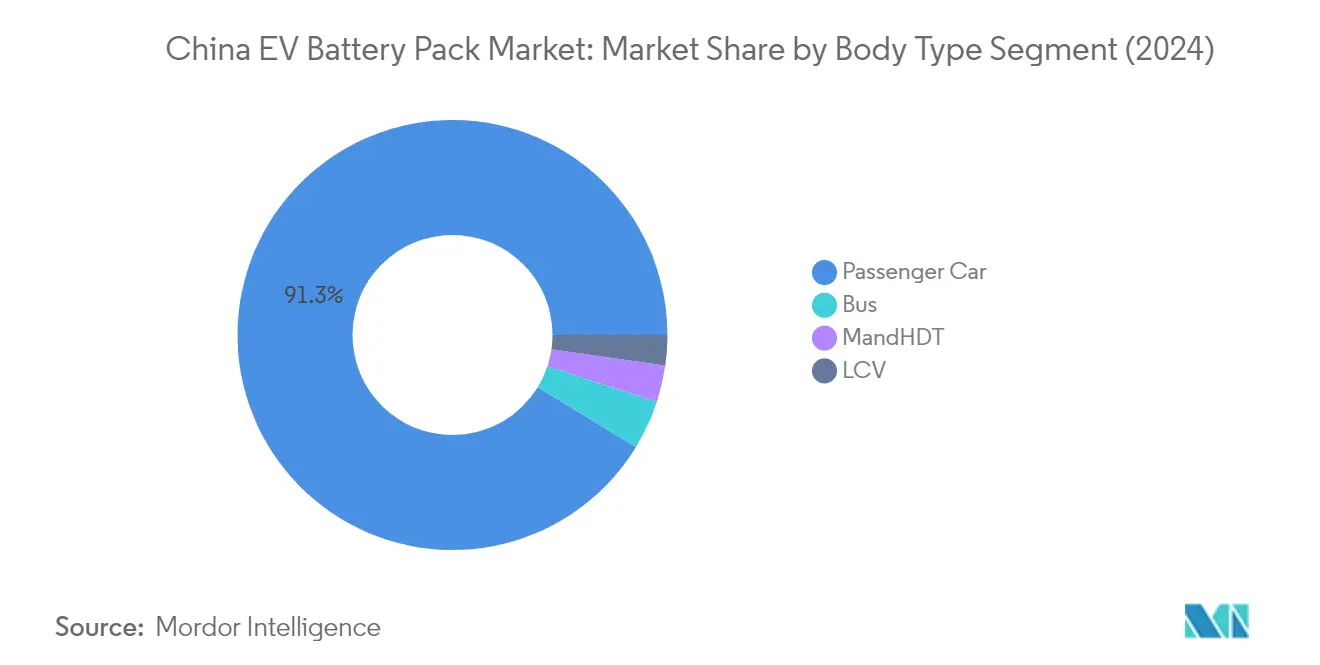

The passenger car segment continues to dominate the China EV battery pack market, commanding approximately 91% market share in 2024. This overwhelming dominance is driven by strong consumer adoption of electric passenger vehicles, extensive government support through subsidies and incentives, and a well-developed charging infrastructure network across major Chinese cities. The segment's growth is further supported by the increasing variety of electric passenger vehicle models offered by both domestic and international manufacturers, ranging from affordable city cars to premium luxury vehicles. Major Chinese automakers like BYD, Wuling, and international players like Tesla have significantly contributed to this segment's expansion through continuous product launches and technological innovations in EV battery cell technology.

Bus Segment in China EV Battery Pack Market

The bus segment is emerging as the fastest-growing segment in the China EV battery pack market, projected to experience remarkable growth of approximately 54% CAGR from 2024 to 2029. This exceptional growth trajectory is primarily driven by aggressive government initiatives to electrify public transportation systems across major Chinese cities. The segment's expansion is further supported by increasing environmental regulations, municipal commitments to reduce urban air pollution, and technological advancements in high-capacity traction battery pack systems specifically designed for electric buses. Chinese cities' ambitious targets for transitioning their entire public transport fleets to electric vehicles, coupled with supportive policies and infrastructure development, are creating a robust growth environment for this segment.

Remaining Segments in Body Type

The Light Commercial Vehicle (LCV) and Medium & Heavy-Duty Truck (M&HDT) segments represent important niches in the China EV battery pack market, each serving distinct commercial and industrial transportation needs. The LCV segment is gaining traction in urban logistics and last-mile delivery applications, driven by increasing e-commerce activities and urban emission regulations. Meanwhile, the M&HDT segment is showing promising development in specialized applications such as port operations, mining, and regional freight transport, with manufacturers focusing on developing high-capacity EV battery module solutions to meet the demanding requirements of heavy-duty applications. Both segments are benefiting from ongoing technological improvements in battery energy density and charging capabilities.

Segment Analysis: Propulsion Type

BEV Segment in China EV Battery Pack Market

Battery Electric Vehicles (BEV) dominate the China EV battery pack market, commanding approximately 97% of the total market share in 2024. This overwhelming dominance can be attributed to several factors, including the Chinese government's strong push for pure electric vehicles through subsidies and incentives, the expanding charging infrastructure network across the country, and increasing consumer confidence in BEV technology. Major automotive manufacturers in China are primarily focusing on BEV production, with companies like BYD and Tesla leading the market with their extensive BEV portfolios. The segment's growth is further supported by advancements in battery management system technology, resulting in improved range capabilities and reduced charging times, making BEVs increasingly attractive to consumers. Additionally, the decreasing costs of battery production and the growing emphasis on environmental sustainability have contributed to the strong market position of BEVs in China.

PHEV Segment in China EV Battery Pack Market

The Plug-in Hybrid Electric Vehicle (PHEV) segment is emerging as the fastest-growing segment in China's EV battery pack market, with a projected growth rate of approximately 15% from 2024 to 2029. This accelerated growth is driven by increasing consumer preference for vehicles that offer both electric and conventional fuel options, effectively addressing range anxiety concerns. The segment is witnessing significant technological advancements in battery thermal management and hybrid powertrain systems, making PHEVs more attractive to consumers seeking flexibility in their driving options. Chinese automotive manufacturers are expanding their PHEV offerings, introducing new models with improved electric ranges and enhanced fuel efficiency. The segment's growth is also supported by government policies promoting new energy vehicles and the increasing awareness among consumers about the benefits of hybrid technology, including lower emissions and reduced fuel consumption.

Segment Analysis: Battery Chemistry

LFP Segment in China EV Battery Pack Market

Lithium Iron Phosphate (LFP) batteries have emerged as the dominant chemistry in China's EV battery pack market, commanding approximately 72% of the market share in 2024. This substantial market leadership can be attributed to several key advantages that LFP batteries offer, including lower production costs, enhanced safety features, improved thermal stability, and longer lifecycle performance. The segment's growth is further bolstered by major Chinese EV manufacturers like BYD and Wuling predominantly using LFP batteries in their vehicle lineup. The increasing focus on cost-effective and reliable battery solutions, coupled with China's strong manufacturing capabilities in LFP technology, has solidified this segment's position. Additionally, the segment benefits from the extensive domestic supply chain for LFP battery materials and components within China, making it a preferred choice for both manufacturers and consumers.

NMC Segment in China EV Battery Pack Market

The Nickel Manganese Cobalt (NMC) battery segment is experiencing remarkable growth in China's EV battery pack market, with a projected growth rate of approximately 17% from 2024 to 2029. This accelerated growth is driven by the increasing demand for high-performance electric vehicles that require superior energy density and extended driving range. The segment's expansion is supported by continuous technological advancements in NMC chemistry, leading to improved battery performance and efficiency. Chinese battery manufacturers are investing heavily in NMC technology development and production capacity expansion to meet the growing demand from premium electric vehicle manufacturers. The segment is also benefiting from the broader industry trend toward higher energy density batteries, particularly in the luxury and performance vehicle segments where driving range and performance are critical factors.

Remaining Segments in Battery Chemistry

The remaining battery chemistry segments in China's EV battery pack market include NCA (Nickel Cobalt Aluminum) and other emerging chemistries. These segments play a specialized role in serving specific market niches and applications within the electric vehicle industry. NCA batteries are particularly valued for their high energy density and performance characteristics, making them suitable for premium electric vehicles and specialized applications. Other emerging battery chemistries are being developed and tested to address specific market needs, such as ultra-fast charging capabilities or extreme temperature performance. These segments continue to evolve through ongoing research and development efforts, contributing to the overall diversification of battery solutions in the Chinese market.

Segment Analysis: Battery Form

Prismatic Segment in China EV Battery Pack Market

The prismatic battery segment continues to dominate the China EV battery pack market, commanding approximately 87% market share in 2024. This significant market position can be attributed to several key advantages that prismatic batteries offer, including low production costs, ease of manufacturing, and enhanced safety features for battery cells. The large size of prismatic cells reduces the number of cells needed for battery formation, which simplifies the production process and improves overall efficiency. Chinese manufacturers prefer prismatic cells due to their higher energy density per volume and superior cost-effectiveness compared to other battery forms. The segment's growth is further supported by major investments in manufacturing capacity expansion and technological advancements by leading battery manufacturers in China.

Pouch Segment in China EV Battery Pack Market

The pouch battery segment is emerging as the fastest-growing segment in China's EV battery pack market, projected to grow at approximately 10% CAGR from 2024 to 2029. This remarkable growth trajectory is driven by several key advantages that pouch batteries offer, including efficient space utilization, excellent safety performance, and high ductility. The segment's expansion is further supported by increasing investments in pouch battery manufacturing capabilities across China. Major automotive manufacturers are showing growing interest in pouch batteries due to their flexibility in design and ability to maximize energy density within limited spaces. The segment is witnessing significant technological advancements, particularly in areas of thermal management and structural integrity, which are expected to further accelerate its adoption in the coming years.

Remaining Segments in Battery Form

The cylindrical battery form represents another significant segment in China's EV battery pack market, offering unique advantages in terms of manufacturing efficiency and thermal management. Cylindrical cells are particularly valued for their superior consistency and automated manufacturing process capabilities. These batteries have established a strong presence in specific applications where their form factor provides optimal performance benefits. The segment continues to evolve with ongoing innovations in cell design and manufacturing processes, contributing to the overall diversity and competitiveness of the battery market. The cylindrical format maintains its importance in certain vehicle applications where its specific characteristics align well with performance requirements.

Segment Analysis: Method

Laser Segment in China EV Battery Pack Market

The laser welding method has emerged as the dominant technology in China's EV battery pack market, commanding approximately 52% market share in 2024. This advanced technology has gained significant traction due to its superior precision, reliability, and ability to create high-quality connections between battery cells. Laser welding offers numerous advantages including improved joint strength, reduced electrical resistance, and enhanced thermal management capabilities, making it particularly suitable for high-power battery applications. The segment's prominence is further reinforced by its robust growth trajectory, with projections indicating an impressive growth rate of nearly 24% from 2024 to 2029. This substantial growth is driven by increasing adoption of electric vehicles, technological advancements in laser welding systems, and the method's ability to meet the demanding requirements of modern battery pack assembly manufacturing. The expansion is also supported by major Chinese battery manufacturers who are increasingly investing in laser welding equipment to enhance their production capabilities and meet the growing demand for high-quality battery packs.

Wire Segment in China EV Battery Pack Market

Wire bonding represents a traditional yet reliable method in China's EV battery pack manufacturing landscape, particularly favored in low to medium-power applications. This method continues to maintain its significance due to its cost-effectiveness, proven reliability, and flexibility in connecting various types of battery cells. Wire bonding's appeal lies in its straightforward implementation, adaptability to different wire types, and ability to create dependable connections through ultrasonic or thermocompression bonding techniques. The method's established presence in the market is supported by its widespread use in electric passenger vehicles, which constitute a significant portion of China's EV market. Manufacturers appreciate wire bonding for its lower equipment costs, simpler maintenance requirements, and ability to accommodate various production volumes. The technology's continued relevance is also attributed to its compatibility with existing manufacturing processes and its ability to meet the specific requirements of certain battery pack designs where laser welding might not be optimal.

Segment Analysis: Component

Cathode Segment in China EV Battery Pack Market

The cathode segment dominates the China EV battery pack component market, accounting for approximately 69% market share in 2024. Cathodes represent one of the most expensive battery materials, making up around 52% of all battery cell components. This significant market position is driven by cathodes being the main factor influencing battery performance, range, and thermal safety. Many automakers in China have increased their usage of cathodes due to their critical role in determining overall battery efficiency. The segment's dominance is further strengthened by ongoing technological advancements in cathode materials and manufacturing processes. Major manufacturers are investing heavily in cathode production facilities to meet the growing demand from electric vehicle manufacturers. The establishment of new production facilities and research centers focused on cathode development continues to support this segment's market leadership.

Separator Segment in China EV Battery Pack Market

The separator segment is emerging as the fastest-growing component in China's EV battery pack market, with a projected growth rate of approximately 5% from 2024 to 2029. This growth is primarily driven by the increasing demand for high-performance battery separators that enhance battery safety and efficiency. The segment is witnessing significant technological advancements in separator materials and manufacturing processes, leading to improved battery performance and reliability. Companies are investing in expanding their separator production capabilities to meet the rising demand from EV manufacturers. The growth is further supported by innovations in separator design that contribute to better thermal management and increased battery life. Various manufacturers are developing advanced separator technologies with enhanced properties such as improved porosity and mechanical strength. The segment's expansion is also bolstered by increasing investments in research and development activities focused on next-generation separator materials.

Remaining Segments in Component Market

The anode and electrolyte segments play crucial roles in the overall EV battery pack market in China. The anode segment is essential for determining battery charging speed and capacity, with manufacturers focusing on developing advanced anode materials to improve battery performance. Anodes typically comprise around 12% of the total battery cost and are crucial for quick charging capabilities and extended battery life. The electrolyte segment, while representing a smaller portion of the battery cost at approximately 4%, is vital for ion transport and overall battery functionality. Both segments continue to see technological advancements and innovations, with manufacturers exploring new materials and compositions to enhance battery efficiency and performance. These components work in conjunction with cathodes and separators to create high-performance battery systems that meet the evolving demands of the electric vehicle industry.

Segment Analysis: Material Type

Natural Graphite Segment in China EV Battery Pack Market

Natural graphite has emerged as the dominant material segment in China's EV battery pack market, commanding approximately 31% market share in 2024. This material's prominence can be attributed to its crucial role in manufacturing battery anodes, where it serves as a primary component across all battery types including LFP, NMC, NCM, and NCA. The material's superior properties, including high energy density and excellent conductivity, make it indispensable for EV battery production. Chinese manufacturers are increasingly favoring natural graphite due to its cost-effectiveness and reliable performance characteristics. The segment's growth is further supported by the country's robust supply chain infrastructure and significant domestic graphite processing capabilities. Major battery manufacturers in China are continuously expanding their production capacities and optimizing their graphite utilization to meet the rising demand from the EV sector.

Nickel Segment in China EV Battery Pack Market

The nickel segment is demonstrating remarkable growth potential in China's EV battery pack market, projected to grow at approximately 17% during 2024-2029. This exceptional growth trajectory is driven by the increasing adoption of nickel-rich cathode chemistries in EV batteries, particularly in high-performance electric vehicles. The segment's expansion is supported by technological advancements in nickel-based battery materials, which offer enhanced energy density and improved range capabilities. Chinese battery manufacturers are investing heavily in nickel-based battery technology development, recognizing its potential to meet the evolving demands of premium electric vehicle segments. The growth is further accelerated by the increasing focus on reducing cobalt content in batteries, making nickel an increasingly important component in next-generation battery formulations.

Remaining Segments in Material Type

The other significant materials in China's EV battery pack market include lithium, manganese, and various other materials such as aluminum and copper. Lithium continues to be a critical component across all battery chemistries, playing a vital role in both cathode and electrolyte formulations. Manganese serves as an essential element in various cathode chemistries, particularly in NMC batteries, offering a balance of cost and performance benefits. Other materials, including aluminum for thermal management and copper for current collectors, play crucial supporting roles in battery pack construction. Each of these materials contributes uniquely to the overall performance and efficiency of EV battery packs, with their demand closely tied to the evolving requirements of different battery chemistries and designs.

Competitive Landscape

Top Companies in China EV Battery Pack Market

The Chinese EV battery pack market is characterized by intense innovation and strategic expansion activities among key players like CATL, FinDreams Battery, EVE Energy, and CALB. Companies are heavily investing in research and development to enhance battery performance, energy density, and charging capabilities while simultaneously expanding their production capacities through new manufacturing facilities. Strategic partnerships with automotive manufacturers have become increasingly common, allowing battery makers to secure long-term supply agreements and collaborate on custom solutions. The industry has witnessed a strong focus on developing advanced battery chemistries, particularly in LFP and NCM technologies, while also investing in automated production lines and smart manufacturing capabilities to improve efficiency and quality control. Companies are also emphasizing vertical integration strategies, establishing control over raw material supply chains and recycling operations to ensure sustainable growth and competitive advantage in the automotive battery systems sector.

Domestic Players Dominate Chinese Battery Market

The Chinese EV battery pack market exhibits a relatively concentrated structure dominated by domestic manufacturers who have established strong positions through technological expertise and government support. These local players have leveraged their deep understanding of the domestic market, established relationships with Chinese automakers, and benefited from supportive government policies to maintain their market leadership. The industry has seen limited participation from international players, although some global automotive manufacturers have formed joint ventures with local battery makers to secure their supply chains and access the Chinese market.

The market has experienced significant consolidation as larger players acquire smaller competitors to expand their technological capabilities and production capacity. This consolidation trend has been driven by the need for economies of scale, access to advanced technologies, and the high capital requirements for establishing competitive battery manufacturing operations. While new entrants continue to emerge, particularly in specialized EV battery components chemistries or niche applications, the barriers to entry remain high due to the intensive capital requirements, technological expertise needed, and the importance of established relationships with automotive manufacturers.

Innovation and Scale Drive Future Success

Success in the Chinese EV battery pack market increasingly depends on companies' ability to balance technological innovation with cost-effective mass production capabilities. Market leaders are focusing on developing next-generation battery technologies while simultaneously optimizing their manufacturing processes to reduce costs and improve efficiency. The ability to secure stable raw material supplies, establish strategic partnerships with automotive manufacturers, and maintain high-quality standards while reducing production costs will be crucial for maintaining competitive advantage. Companies must also demonstrate strong environmental credentials and invest in sustainable practices to meet increasingly stringent regulatory requirements.

For new entrants and smaller players, success will depend on identifying and exploiting niche market segments or specialized applications where they can differentiate themselves from larger competitors. This could include focusing on specific battery chemistries, developing innovative battery management systems technologies, or targeting particular vehicle segments or applications. Building strong relationships with automotive manufacturers, particularly emerging EV brands, will be essential for securing market share. Additionally, companies must prepare for potential regulatory changes, particularly around battery safety standards and environmental requirements, while maintaining flexibility to adapt to evolving market demands and technological developments in the electric vehicle power systems industry.

China EV Battery Pack Industry Leaders

China Aviation Battery Co. Ltd. (CALB)

Contemporary Amperex Technology Co. Ltd. (CATL)

EVE Energy Co. Ltd.

FinDreams Battery Co. Ltd.

SVOLT Energy Technology Co. Ltd. (SVOLT)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2023: CATL announced the signing of a strategic cooperation framework agreement with the Shenzhen Municipal People’s Government. The two parties will focus on such key fields as New Energy Vehicle battery swapping, electric ships, new energy storage, green parks, financial services, and trade for all-round cooperation.

- May 2023: Changan Auto recently disclosed that the battery cell joint venture (JV) between it and CATL will complete registration in the first half of 2023. The JV will mainly be engaged in the production and manufacturing of power battery cells and is expected to be commissioned within 2023, with an annual capacity as high as 25 GWh.

- May 2023: CATL announced the holding of a bank-enterprise strategic cooperation agreement signing ceremony with the Agricultural Bank of China (ABC). With the agreement signed, the two parties will deepen cooperation to continuously innovate cooperation models in such fields as battery swapping business, overseas and domestic businesses, and green electricity and energy storage businesses.

China EV Battery Pack Market Report Scope

Bus, LCV, M&HDT, Passenger Car are covered as segments by Body Type. BEV, PHEV are covered as segments by Propulsion Type. LFP, NCA, NCM, NMC, Others are covered as segments by Battery Chemistry. 15 kWh to 40 kWh, 40 kWh to 80 kWh, Above 80 kWh, Less than 15 kWh are covered as segments by Capacity. Cylindrical, Pouch, Prismatic are covered as segments by Battery Form. Laser, Wire are covered as segments by Method. Anode, Cathode, Electrolyte, Separator are covered as segments by Component. Cobalt, Lithium, Manganese, Natural Graphite, Nickel are covered as segments by Material Type.| Bus |

| LCV |

| M&HDT |

| Passenger Car |

| BEV |

| PHEV |

| LFP |

| NCA |

| NCM |

| NMC |

| Others |

| 15 kWh to 40 kWh |

| 40 kWh to 80 kWh |

| Above 80 kWh |

| Less than 15 kWh |

| Cylindrical |

| Pouch |

| Prismatic |

| Laser |

| Wire |

| Anode |

| Cathode |

| Electrolyte |

| Separator |

| Cobalt |

| Lithium |

| Manganese |

| Natural Graphite |

| Nickel |

| Other Materials |

| Body Type | Bus |

| LCV | |

| M&HDT | |

| Passenger Car | |

| Propulsion Type | BEV |

| PHEV | |

| Battery Chemistry | LFP |

| NCA | |

| NCM | |

| NMC | |

| Others | |

| Capacity | 15 kWh to 40 kWh |

| 40 kWh to 80 kWh | |

| Above 80 kWh | |

| Less than 15 kWh | |

| Battery Form | Cylindrical |

| Pouch | |

| Prismatic | |

| Method | Laser |

| Wire | |

| Component | Anode |

| Cathode | |

| Electrolyte | |

| Separator | |

| Material Type | Cobalt |

| Lithium | |

| Manganese | |

| Natural Graphite | |

| Nickel | |

| Other Materials |

Market Definition

- Battery Chemistry - Various types of battery chemistry considred under this segment include LFP, NCA, NCM, NMC, Others.

- Battery Form - The types of battery forms offered under this segment include Cylindrical, Pouch and Prismatic.

- Body Type - Body types considered under this segment include, passenger cars, LCV (light commercial vehicle), M&HDT (medium & heavy duty trucks)and buses.

- Capacity - Various types of battery capacities inldude under theis segment are 15 kWH to 40 kWH, 40 kWh to 80 kWh, Above 80 kWh and Less than 15 kWh.

- Component - Various components covered under this segment include anode, cathode, electrolyte, separator.

- Material Type - Various material covered under this segment include cobalt, lithium, manganese, natural graphite, nickel, other material.

- Method - The types of method covered under this segment include laser and wire.

- Propulsion Type - Propulsion types considered under this segment include BEV (Battery electric vehicles), PHEV (plug-in hybrid electric vehicle).

- ToC Type - ToC 1

- Vehicle Type - Vehicle type considered under this segment include passenger vehicles, and commercial vehicles with various EV powertrains.

| Keyword | Definition |

|---|---|

| Electric vehicle (EV) | A vehicle which uses one or more electric motors for propulsion. Includes cars, buses, and trucks. This term includes all-electric vehicles or battery electric vehicles and plug-in hybrid electric vehicles. |

| PEV | A plug-in electric vehicle is an electric vehicle that can be externally charged and generally includes all electric vehicles as well as plug-electric vehicles as well as plug-in hybrids. |

| Battery-as-a-Service | A business model in which the battery of an EV can be rented from a service provider or swapped with another battery when it runs out of charge |

| Battery Cell | The basic unit of an electric vehicle's battery pack, typically a lithium-ion cell, that stores electrical energy. |

| Module | A subsection of an EV battery pack, consisting of several cells grouped together, often used to facilitate manufacturing and maintenance. |

| Battery Management System (BMS) | An electronic system that manages a rechargeable battery by protecting the battery from operating outside its safe operating area, monitoring its state, calculating secondary data, reporting data, controlling its environment, and balancing it. |

| Energy Density | A measure of how much energy a battery cell can store in a given volume, usually expressed in watt-hours per liter (Wh/L). |

| Power Density | The rate at which energy can be delivered by the battery, often measured in watts per kilogram (W/kg). |

| Cycle Life | The number of complete charge-discharge cycles a battery can perform before its capacity falls under a specified percentage of its original capacity. |

| State of Charge (SOC) | A measurement, expressed as a percentage, that represents the current level of charge in a battery compared to its capacity. |

| State of Health (SOH) | An indicator of the overall condition of a battery, reflecting its current performance compared to when it was new. |

| Thermal Management System | A system designed to maintain optimal operating temperatures for an EV's battery pack, often using cooling or heating methods. |

| Fast Charging | A method of charging an EV battery at a much faster rate than standard charging, typically requiring specialized charging equipment. |

| Regenerative Braking | A system in electric and hybrid vehicles that recovers energy normally lost during braking and stores it in the battery. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all its reports.

- Step-1: Identify Key Variables: To build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built based on these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. Market revenue is calculated by multiplying the volume demand with volume-weighted average battery pack price (per kWh). Battery pack price estimation and forecast takes into account various factors affecting ASP, such as inflation rates, market demand shifts, production costs, technological developments, and consumer preferences, providing estimations for both historical data and future trends.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms