China Electric Vehicle Battery Materials Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

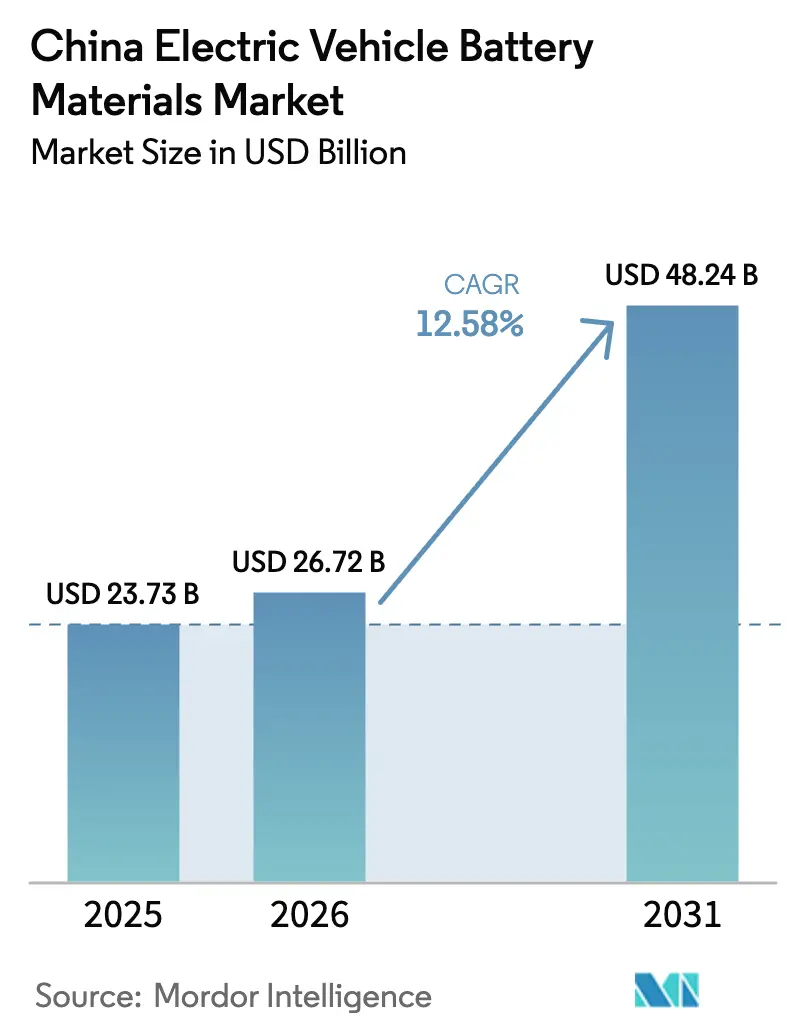

| Base Year Market Size (2025) | USD 23.73 Billion |

| Market Size (2026) | USD 26.72 Billion |

| Market Size (2031) | USD 48.24 Billion |

| Growth Rate (2026 - 2031) | 12.58% CAGR |

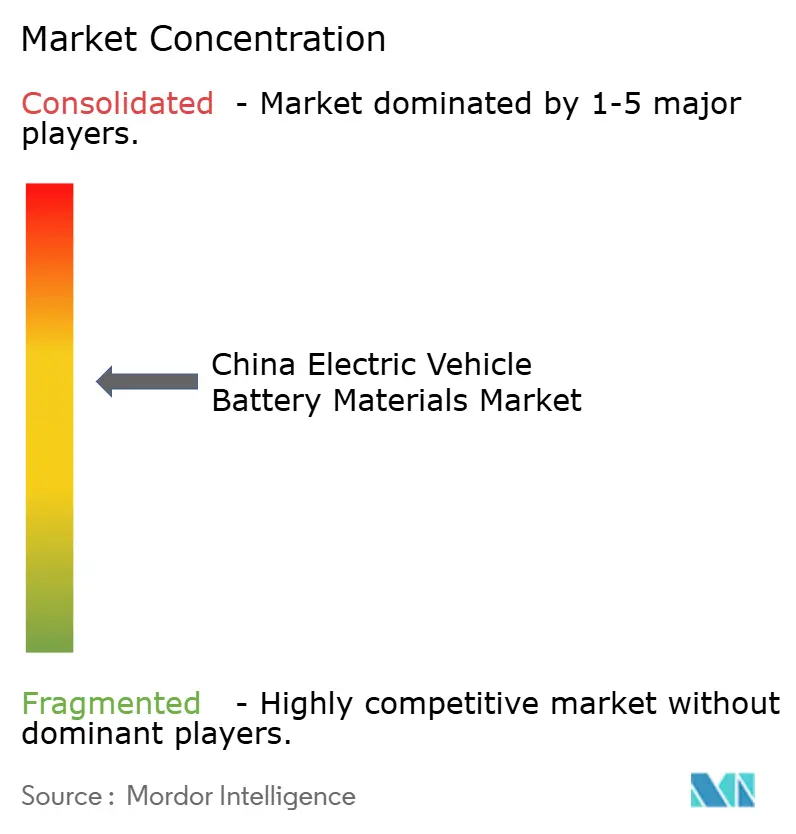

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Electric Vehicle Battery Materials Market Analysis by Mordor Intelligence

The China Electric Vehicle Battery Materials Market size is expected to grow from USD 23.73 billion in 2025 to USD 26.72 billion in 2026 and is forecast to reach USD 48.24 billion by 2031 at 12.58% CAGR over 2026-2031.

Strong policy support, led by the MIIT 2025 durability standards, accelerates investment in next-generation chemistries and secures domestic supply.[1]Ministry of Industry and Information Technology, “2025 Standardization Work Plan for Battery Industry,” MIIT.gov.cn Rapid electrification of passenger and commercial fleets keeps cathode, anode, and auxiliary material demand on an upward trajectory as vehicle makers race to localize critical inputs.[2]State Council of the People’s Republic of China, “Work Plan for Stabilizing Growth (2025-2026),” Gov.cn Capital continues to reallocate from nickel- and cobalt-intensive NMC cathodes to lithium iron phosphate (LFP) and lithium manganese iron phosphate (LMFP) variants as producers hedge against raw-material volatility. In parallel, Jiangxi, Sichuan, and Qinghai provinces are scaling spodumene-to-hydroxide and lepidolite processing to narrow the deficit in battery-grade lithium and phosphate supplies. Competitive dynamics remain intense: CATL and BYD maintain a cost advantage through vertical integration, while mid-tier firms pursue Indonesian nickel joint ventures to offset feedstock costs.

Key Report Takeaways

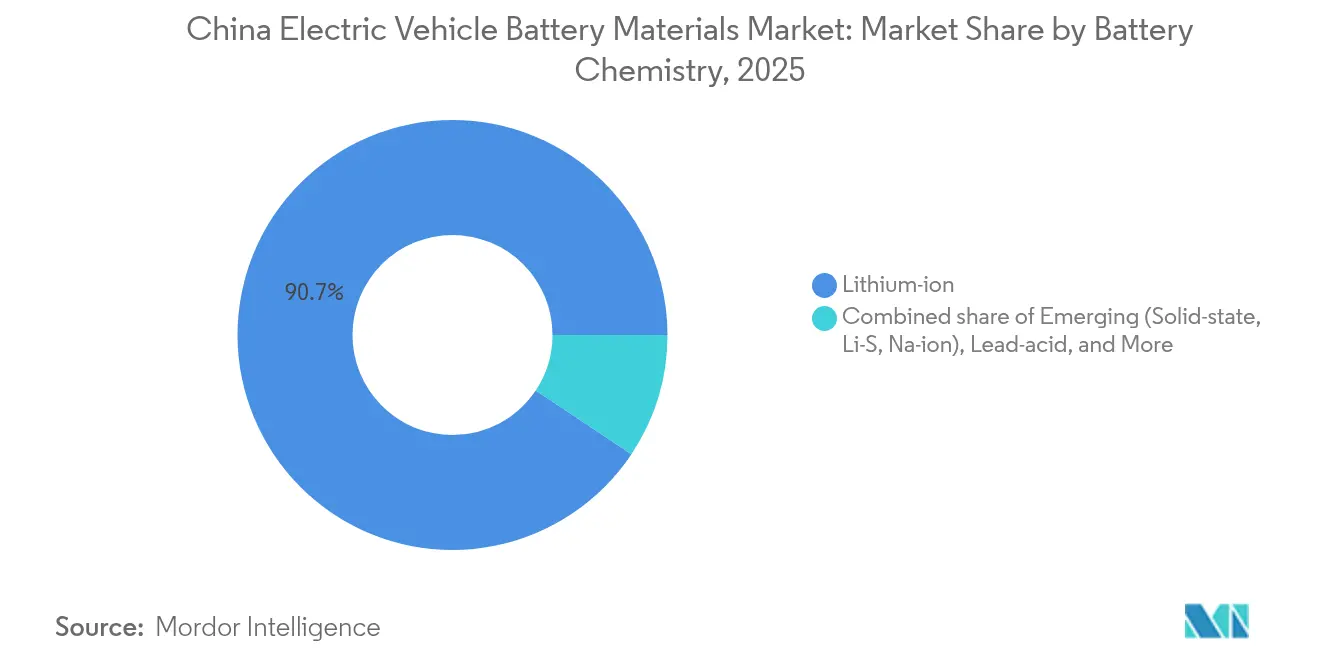

- By battery chemistry, lithium-ion captured 90.65% of the China Electric Vehicle Battery Materials market share in 2025, and emerging solid-state, lithium-sulfur, and sodium-ion alternatives are set to expand at a 35.62% CAGR through 2031.

- By material, cathode materials accounted for 61.78% of 2025 revenue, whereas the “Others” segment, binders, conductive additives, and thermal interface materials, will post the fastest 24.05% CAGR to 2031.

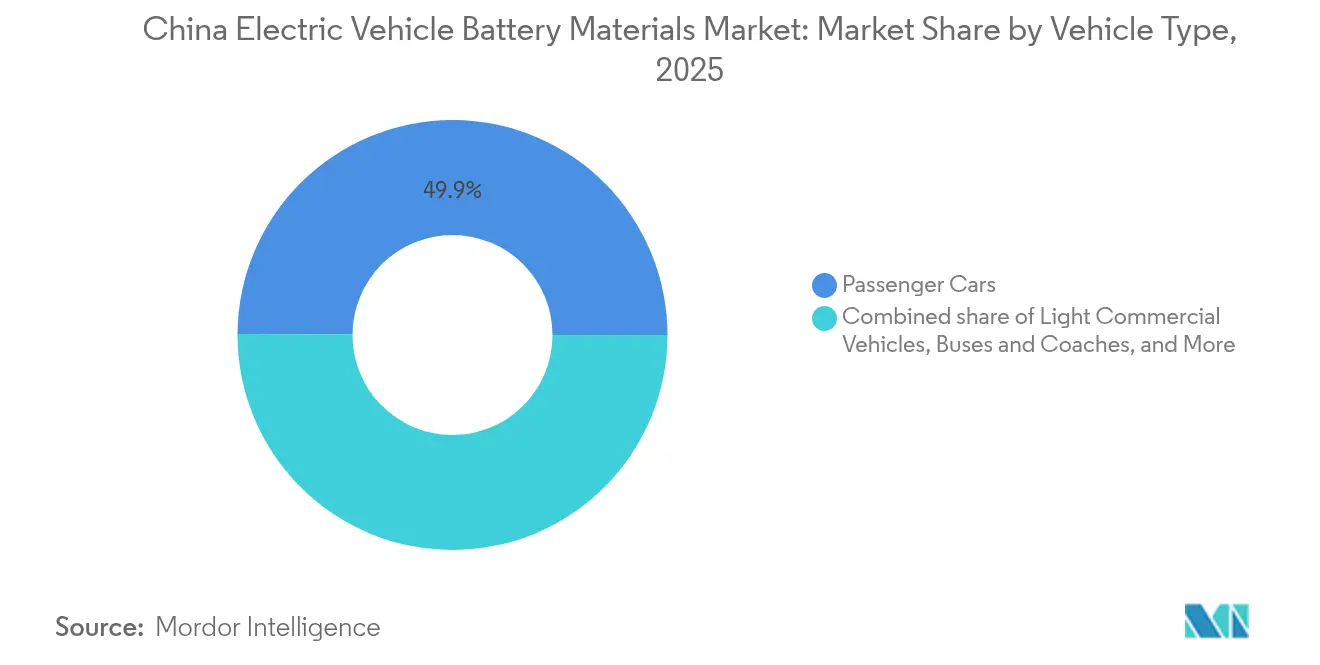

- By vehicle type, passenger cars held 49.92% of the 2025 value and are forecast to post the quickest 14.88% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Proportional positioning is established by comparing country level and regional contributions against the global total, including that of China. The electric vehicle battery materials market share in our global report expresses these relative weights.

China Electric Vehicle Battery Materials Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging domestic EV output post-2025 NEV 3.0 mandate | +3.2% | National, with concentration in Yangtze River Delta and Pearl River Delta | Short term (≤ 2 years) |

| Aggressive cathode-to-LFP substitution to contain nickel/cobalt exposure | +2.8% | National, particularly Fujian and Guangdong cathode clusters | Medium term (2-4 years) |

| Localization push for high-purity lithium carbonate and phosphate supply | +2.1% | Jiangxi, Sichuan, Qinghai lithium corridors | Medium term (2-4 years) |

| State-backed battery-swapping corridors for heavy trucks | +1.5% | National trunk routes, pilot zones in Fujian, Hebei, Inner Mongolia | Long term (≥ 4 years) |

| EU/US tariff walls accelerating export-of-batteries strategy | +1.3% | Global, with primary impact on Jiangsu and Fujian export-oriented manufacturers | Medium term (2-4 years) |

| Capital-market preference for low-carbon material chains (green-bonds quota) | +0.9% | National, favoring vertically integrated producers with ESG disclosure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Domestic EV Output Post-2025 NEV 3.0 Mandate

Policy targets lifting NEV penetration to 85% by 2040 are already influencing procurement forecasts, as each 1-percentage-point rise in penetration adds nearly 20,000 metric tons of cathode demand.[3]China Society of Automotive Engineers, “Technology Roadmap 3.0 for New Energy Vehicles,” Sae-china.org Provinces link automotive quotas to GDP goals, speeding approvals for new material plants even while regulators elevate environmental standards. Recycling requirements set at 65% for power batteries by 2025 are creating a closed-loop system that could trim primary lithium demand 12-15% annually by 2028. Regional responses differ: Guangdong accelerated vehicle targets to capture manufacturing, whereas Sichuan emphasized upstream refining. Suppliers able to serve both provinces secure long-term offtake contracts that stabilize revenue.

Aggressive Cathode-to-LFP Substitution to Contain Nickel/Cobalt Exposure

LFP packs cost USD 53 per kWh versus USD 75-80 for high-nickel NMC, pushing LFP’s share of passenger EVs to 55-60% in 2024.[4]Bloomberg, “China’s LFP Battery Costs Hit Record Low in 2024,” Bloomberg.com BYD’s Blade architecture removed module casings, matching 400-500 km range requirements and undercutting NMC’s historical energy-density edge. LMFP cathodes add 15-20% energy density and broaden LFP’s addressable market. However, premium models needing 600 km+ range still opt for NMC, sustaining a bifurcated chemistry mix. Suppliers holding LFP and high-nickel lines can flex output as metal prices shift, protecting margins against feedstock swings.

Localization Push for High-Purity Lithium Carbonate and Phosphate Supply

Domestic lithium carbonate output jumped 47% to 680,000 t LCE in 2024, yet imports of 230,000 t highlighted ongoing gaps in battery-grade hydroxide. Jiangxi now grants tax holidays to converters meeting 99.5% purity thresholds, while Sichuan subsidies revive lepidolite extraction to diversify feedstock. Hydroxide premiums widened to 18% over carbonate as NMC producers locked in supply. Domestic refining shields China from prospective export controls flagged in Australia’s 2024 Critical Minerals review. Integrated miners, therefore, enjoy lower transport costs and favorable green-bond rates tied to carbon intensity.

State-Backed Battery-Swapping Corridors for Heavy Trucks

CATL and Sinopec plan 10,000 swap stations, each requiring 6-8 buffer packs that multiply per-vehicle material intensity. Heavy-truck operators slash capex by up to 50% when batteries remain asset-owner property, shortening payback periods. The NDRC subsidizes 30% of station capex along 15 trunk corridors. Yet divergent pack standards risk stranding assets if convergence fails by 2026. Material suppliers aligned with dominant platforms will capture recurring demand for replacement packs, separators, and electrolytes as swap cycles accelerate wear.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising spodumene auction prices ≥ USD 1,350/t | -1.8% | Global, affecting Chinese importers dependent on Australian supply | Short term (≤ 2 years) |

| Environmental audits tightening HF-based wet-process cathode plants | -1.2% | Hunan, Jiangxi, Guangdong cathode production clusters | Medium term (2-4 years) |

| IP restrictions on next-gen silicon-rich anodes held by foreign firms | -0.7% | National, constraining energy density improvements for premium EVs | Long term (≥ 4 years) |

| Overcapacity risk from 2 TWh planned cathode lines by 2028 | -1.4% | National, particularly affecting mid-tier producers without OEM partnerships | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Spodumene Auction Prices ≥ USD 1,350/t

Forward contracts indicate a spodumene floor near USD 1,350/t amid supply concentration in Western Australia, exposing converters to margin pressure when delivered costs exceed USD 1,200/t LCE. Large converters hedge with fixed-discount offtakes, while smaller players pivot to costlier lepidolite feedstock, sacrificing profitability to reduce import dependence. Vehicle chemistries remain lithium-dependent for 400 km+ range, keeping spodumene prices structurally elevated.

Environmental Audits Tightening HF-Based Wet-Process Cathode Plants

Surprise inspections idled 12 precursor plants in 2024, lifting high-nickel cathode spot premiums 5-8%. Compliance retrofits add USD 8-12 million per 10,000 t line and cut margins 3-5 points. Provinces offering centralized waste treatment, notably Fujian, attract new capacity, whereas dispersed clusters in Jiangxi face exit or LFP conversion. This regulatory spread accelerates geographic consolidation and embeds a structural cost gap favoring integrated producers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Chemistry: Lithium-Ion Dominance Faces Niche Disruption

Lithium-ion retained 90.65% of the China Electric Vehicle Battery Materials market share in 2025, reflecting entrenched supply chains and wide OEM adoption. Emerging chemistries are forecast at a 35.62% CAGR, propelled by CATL’s sodium-ion packs now deployed in entry-level EVs. Solid-state prototypes have reached 360 Wh/kg semi-solid configuration in commercial sedans, pointing to incremental, not overnight, displacement of incumbent cells.

Chinese producers balance cost and energy density: LFP serves mass-market sedans, high-nickel NMC anchors premium ranges, and sodium-ion targets low-range mobility. Lead-acid persists in rural micro-mobility but continues to cede share as lithium chemistry costs fall below USD 100/kWh. Hybrid-focused NiMH demand fades as Japanese OEMs transition to plug-in systems, trimming procurable metal hydride inputs by nearly 18% annually.

By Material: Cathode Dominance Meets Auxiliary Innovation

Cathodes contributed 61.78% to the China Electric Vehicle Battery Materials market size in 2025, yet saturated capacity and raw-material swings push margin focus to binders, additives, and thermal interfaces, the “Others” segment growing 24.05% CAGR. Separator specialists launch 7-9 µm ceramic-coated films that enable 3C fast charging, while electrolyte firms add film-forming additives to exceed 2,000 cycles, meeting battery-swap durability specs.

Anode suppliers confront U.S. graphite restrictions by scaling domestic synthetic lines and developing silicon-carbon blends that skirt foreign patent landscapes. LMFP and high-voltage spinel cathodes open avenues for manganese and iron supply chains, diluting nickel/cobalt dependence. The result is a broader material portfolio where auxiliary inputs drive safety and cycle life leadership even as cathode share remains dominant.

By Vehicle Type: Passenger Cars Lead, Commercial Fleets Accelerate

Passenger cars commanded 49.92% of the 2025 value in the China Electric Vehicle Battery Materials market, and a 14.88% CAGR will keep them central through 2031. Falling battery costs push compact sedans to price parity with internal-combustion peers.

Heavy trucks and buses, though smaller in volume, yield outsized material intensity; battery-swapping platforms double or triple pack inventory per vehicle. Light commercial fleets, pressured by e-commerce logistics, adopt LFP packs for durability, and two- and three-wheelers transition from lead-acid as pack prices drop below USD 150/kWh. Off-highway EVs for mining and construction add lumpy but high-value demand, favoring thermally stable chemistries for harsh duty cycles.

Geography Analysis

Eastern coastal clusters dominate mid- and downstream stages, while lithium extraction and refining concentrate in western provinces. Fujian’s Ningde hub anchors cathode and cell capacity around CATL, leveraging port access for import logistics. The Yangtze River Delta hosts 70% of separator and electrolyte exports, with integrated chemical complexes in Jiangsu and Zhejiang providing feedstocks.

Jiangxi delivers 35% of national refining, aided by tax waivers for plants meeting high-purity thresholds. Sichuan’s hydropower cuts carbon intensity for hydroxide conversion, yielding green-bond eligibility and 50-80 basis-point financing discounts. Inner Mongolia and Qinghai attract recycling investments that close the loop and supply reclaimed metals back to coastal cell factories.

Export linkages reshape geography: Fujian and Jiangsu manage 70% of outbound shipments, while Belt and Road corridors funnel cathode and separator volumes to ASEAN assembly plants. Provincial incentive competition risks localized overcapacity as land and power subsidies pull projects to regions lacking downstream demand.

Mordor Intelligence examines the electric vehicle battery materials market across diverse other regional markets as well, including Asia, Middle East and Africa, and North America, while also offering granular country-level perspectives for India, United States, Germany, France, United Kingdom, and Italy and more.

Competitive Landscape

Top producers control roughly 55-60% of cathode capacity but less than 40% of anode and separator lines, putting the China Electric Vehicle Battery Materials industry in a moderately concentrated state.[5]China Battery Industry Association, “Market Concentration Analysis 2024,” Cbia.org.cn CATL and BYD deploy seamless vertical chains from mining to pack assembly, achieving cost advantages unattainable for capital-constrained peers. Mid-tier firms respond by forming joint ventures in Indonesia for nickel and in Finland for cathode lines, blending overseas feedstock with Chinese process know-how.

Technology licenses remain a chokepoint: Japanese and U.S. patent owners hold core IP for silicon-rich anodes and solid-state electrolytes, forcing Chinese suppliers toward workarounds or cross-licensing. MIIT’s “White List” trims non-compliant producers, accelerating consolidation: 87 certified cathode firms remain, down from 112 two years earlier.

Process digitization separates leaders from followers: AI-driven synthesis cuts precursor reaction time 20-30%, lowering energy bills and CO2 intensity. Green-bond markets reward such metrics with cheaper capital, allowing scale players to extend their lead. Niche opportunities survive in specialty additives and LMFP cathodes, where first movers still secure defensible margins before giants replicate.

China Electric Vehicle Battery Materials Industry Leaders

Contemporary Amperex Technology Co., Limited

BYD Auto Co., Ltd.

Ganfeng Lithium

Ronbay Technology

BTR New Material

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Tinci Materials, bolstering its foothold in the global battery supply chain, has garnered attention with a fresh batch of invention patents. The company is also deepening its longstanding partnerships with top Chinese cell manufacturers. Recently, Tinci announced the acquisition of eight patents from the National Intellectual Property Administration. These patents pertain to sulfide solid electrolytes and their use in all-solid-state lithium batteries.

- June 2025: CATL is committed to 1,000 Choco-Swap heavy-truck stations, investing USD 800 million to lower fleet capex.

- February 2025: Ganfeng Lithium, the leading lithium producer in China, has kicked off operations at a lithium mine in Argentina. This move underscores Argentina's proactive efforts to bolster supplies for its vast domestic market. Ganfeng announced the official launch of the first phase of its Mariana project located in Salta, Argentina, highlighting the nation's growing significance as a key overseas production hub for the company.

China Electric Vehicle Battery Materials Market Report Scope

Electric vehicle (EV) battery materials are the specific substances and components used in the construction of batteries for powering electric vehicles. These materials determine electric vehicles' efficiency, range, longevity, and safety. The report offers the market size in value terms (USD) for all the above-mentioned segments. The China electric vehicle battery materials market report includes:

| Lithium-ion (NMC, LFP, NCA) |

| Emerging (Solid-state, Li-S, Na-ion) |

| Lead-acid |

| Nickel-metal-hydride |

| Anode |

| Cathode |

| Separator |

| Electrolyte |

| Others |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Trucks |

| Buses and Coaches |

| Two and Three-wheelers |

| Off-Highway and Specialty EVs |

| By Battery Chemistry | Lithium-ion (NMC, LFP, NCA) |

| Emerging (Solid-state, Li-S, Na-ion) | |

| Lead-acid | |

| Nickel-metal-hydride | |

| By Material | Anode |

| Cathode | |

| Separator | |

| Electrolyte | |

| Others | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| Medium and Heavy Trucks | |

| Buses and Coaches | |

| Two and Three-wheelers | |

| Off-Highway and Specialty EVs |

Key Questions Answered in the Report

How large is the China Electric Vehicle Battery Materials market in 2026?

It carries forward from USD 26.72 billion in 2026 toward USD 48.24 billion by 2031, implying steady double-digit annual expansion.

What chemistry dominates battery packs for Chinese EVs?

Lithium-ion cells, chiefly LFP and high-nickel NMC variants, controlled 90.65% of 2025 value, with sodium-ion and solid-state cells growing from a low base.

Which segment grows fastest through 2031?

Specialty “Others” materials—binders, conductive additives, and thermal interfaces—rise at 24.05% CAGR thanks to cell-to-pack and fast-charge designs.

Why are LFP cathodes gaining share?

They cost USD 53 per kWh versus USD 75-80 for NMC, avoid nickel/cobalt supply risk, and meet 400-500 km range needs for mainstream sedans.

How do battery-swap corridors affect material demand?

Each heavy-truck swap station holds 6-8 spare packs, multiplying cathode and separator throughput and accelerating replacement cycles.

Is the market fragmented or concentrated?

Moderate concentration prevails: the top 10 control about 55-60% of cathode capacity yet less than 40% of anode and separator output, yielding a score of 6.

Page last updated on: