China Electric Vehicle Battery Manufacturing Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

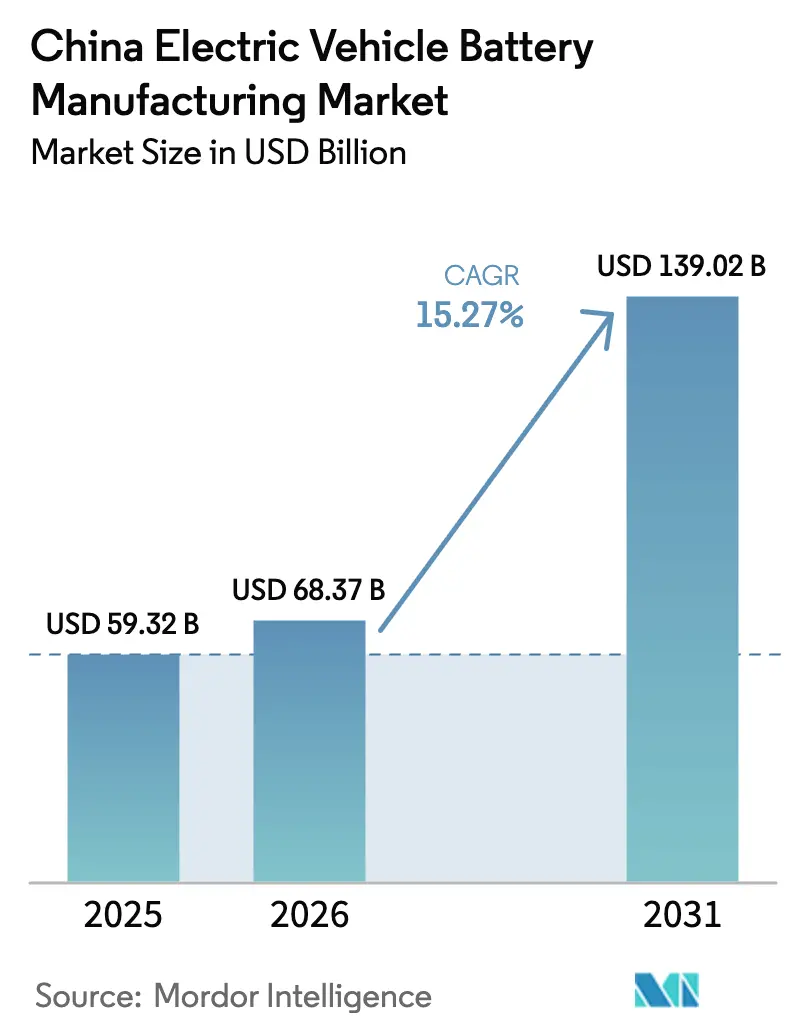

| Base Year Market Size (2025) | USD 59.32 Billion |

| Market Size (2026) | USD 68.37 Billion |

| Market Size (2031) | USD 139.02 Billion |

| Growth Rate (2026 - 2031) | 15.27% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

China Electric Vehicle Battery Manufacturing Market Analysis by Mordor Intelligence

The China Electric Vehicle Battery Manufacturing Market size is expected to grow from USD 59.32 billion in 2025 to USD 68.37 billion in 2026 and is forecast to reach USD 139.02 billion by 2031 at 15.27% CAGR over 2026-2031.

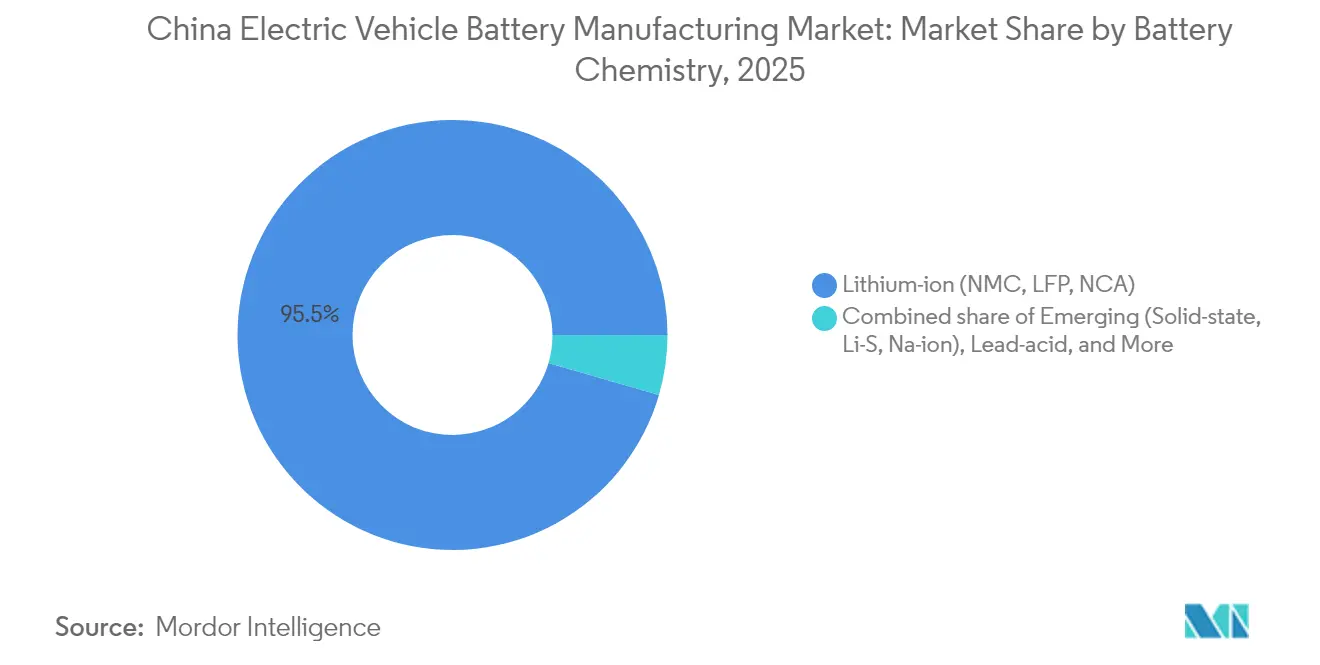

The expansion is propelled by rising new-energy-vehicle (NEV) penetration, large-scale gigafactory construction, and ongoing policy incentives. Lithium-ion chemistries held 95.5% of output in 2024, yet solid-state and sodium-ion formats are on a 36.8% annual growth trajectory, indicating an approaching diversification inflection. Capacity additions already exceed short-term demand, pushing utilization down to 50% in 2024, which in turn accelerates price pressure and industry consolidation. Tier-1 producers are responding with global offtake pacts and vertical-integration moves, while inland plants co-located near lithium and phosphate deposits lower logistics costs and mitigate feedstock risk.[1]Reuters Staff, “China NEV Sales Soar 35.7% in 2024,” Reuters, reuters.com

Key Report Takeaways

- By battery chemistry, lithium-iron-phosphate (LFP) captured roughly 69.42% of the Chinese electric vehicle battery manufacturing market share in 2025, while emerging solid-state and sodium-ion lines are forecast to expand at a 35.12% CAGR through 2031.

- By cell format, pouch cells led with 54.35% revenue share in 2025; prismatic architectures are projected to rise at a 21.03% CAGR to 2031.

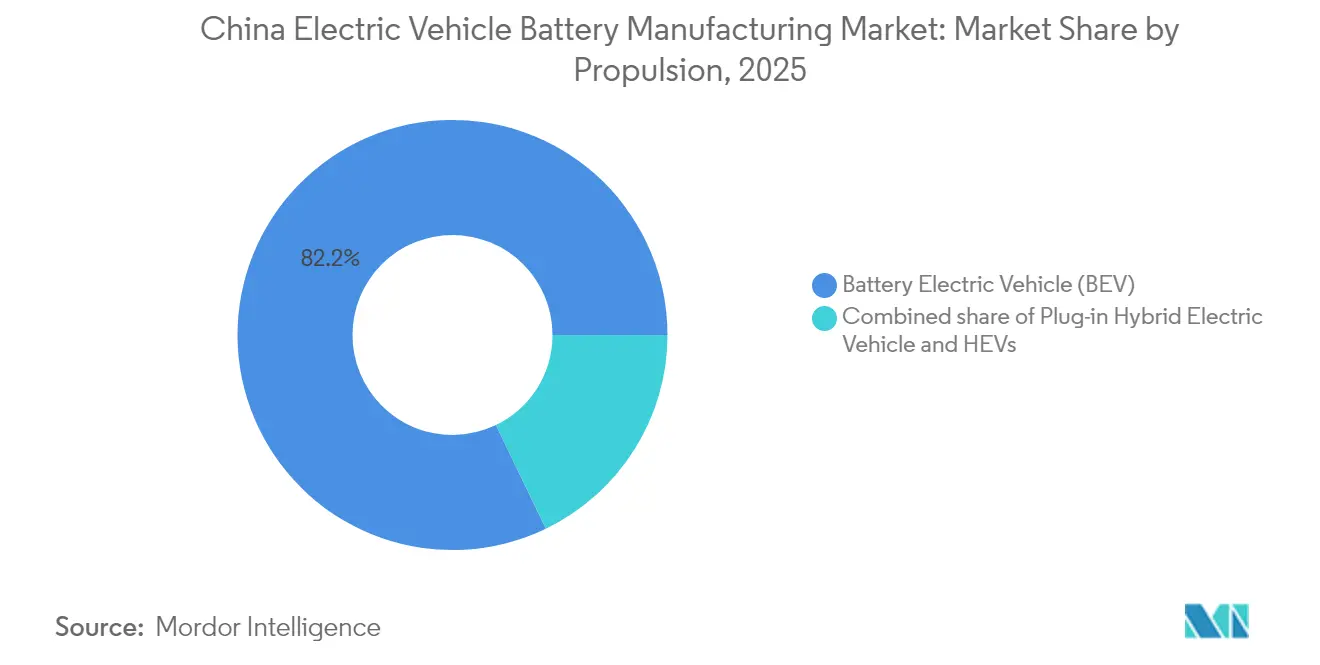

- By propulsion, battery electric vehicles accounted for 82.15% of the Chinese electric vehicle battery manufacturing market size in 2025 and are advancing at a 17.55% CAGR through 2031.

- By vehicle type, passenger cars commanded 87.76% share of the China electric vehicle battery manufacturing market size in 2025; light commercial vehicles are the fastest-growing segment at a 19.11% CAGR until 2031.

- CATL, BYD, and CALB jointly held about 74.25% domestic shipment share in 2025, indicating a concentrated leadership core.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

China Electric Vehicle Battery Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Policy-linked purchase subsidies and tax exemptions | 2.8% | National, with stronger uptake in tier-1 and tier-2 cities | Medium term (2-4 years) |

| Rapid domestic EV sales growth boosts installed battery demand | 4.2% | National, concentrated in coastal provinces and megacities | Short term (≤ 2 years) |

| Massive capex announcements by Tier-1 cell makers (≥ 2 TWh pipeline) | 3.5% | National, with export-oriented capacity in coastal hubs | Long term (≥ 4 years) |

| Battery recycling integration cuts raw-material cost volatility | 1.9% | National, early gains in Jiangsu, Guangdong, Hunan | Medium term (2-4 years) |

| Commercialization runway for sodium-ion pilot lines from 2025 | 1.6% | National, initial deployment in commercial vehicles | Long term (≥ 4 years) |

| Western China lithium and phosphate resource clustering advantages | 2.3% | Western provinces (Qinghai, Sichuan, Tibet) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Policy-Linked Purchase Subsidies and Tax Exemptions

The extension of NEV purchase-tax relief through 2027 retains a fiscal benefit close to CNY 52,000 (USD 7,300) per vehicle, cushioning demand even after direct subsidies lapsed in 2023. The Ministry of Industry and Information Technology (MIIT) paired the incentive with stricter eligibility rules that require battery makers to invest 3% of revenue in R&D and implement end-to-end traceability. These dual levers stimulate volume while raising the quality bar, prompting financially weaker plants to exit and favoring integrated leaders that can absorb compliance overhead. The policy’s continuation signals Beijing’s view that batteries are a strategic export engine, not merely a domestic industrial priority.

Rapid Domestic EV Sales Growth Boosts Installed Battery Demand

NEV sales hit 9.5 million units in 2024, lifting penetration to 35.7% and driving annual installed battery demand above 400 GWh. Automakers are shifting from 50–60 kWh packs in compact sedans to 80–100 kWh configurations for SUVs, increasing per-vehicle battery content by around 30% since 2022. Overseas shipments add further lift; over 1.2 million China-built NEVs were exported to Europe and Southeast Asia in 2024, each requiring locally manufactured cells to meet rules-of-origin thresholds. Consequently, gigafactories must serve domestic and export channels simultaneously, intensifying offtake races among CATL, BYD, and CALB with Volkswagen, Stellantis, and Thai start-ups.[2]Financial Times Reporters, “Indonesia’s Nickel Export Curbs Rattle Chinese Cathode Producers,” Financial Times, ft.com

Massive Capex Announcements by Tier-1 Cell Makers

CATL’s USD 7.8 billion Hungary plant, BYD’s six new mainland facilities totaling 150 GWh, and CALB’s 50 GWh Chengdu expansion collectively surpass 2 TWh of slated capacity by 2028. These commitments arrive even as utilization languishes at 50%, a mismatch born of scale-up races and provincial incentive packages. The strategic calculus rests on locking in economies of scale ahead of Europe’s internal-combustion bans and on leveraging land grants tied to GDP goals. The downside is intensifying price tension; LFP cells slipped to USD 53 per kWh in late 2024, eroding margins for all but the technology leaders.

Battery Recycling Integration Cuts Raw-Material Cost Volatility

New GB/T 44132-2024 rules set lithium recovery at 90% and nickel-cobalt-manganese above 98%, creating a formalized end-of-life supply loop. An estimated 1 million tons of retired batteries entering the system by 2025 could yield 150,000 tons of lithium carbonate equivalent, about 15% of 2024 primary output. CATL and BYD have integrated recycling subsidiaries, shaving cathode precursor costs by one-third and buffering geopolitical swings in Indonesian nickel or Chilean lithium. Mandatory traceability funnels scrap into certified channels, concentrating throughput among top-tier operators and edging out informal networks.[3]Ministry of Industry and Information Technology, “GB/T 44132-2024 Battery Recycling Standard,” miit.gov.cn

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Import dependency for high-nickel cathode precursors | -1.7% | National, acute for NMC-focused manufacturers | Short term (≤ 2 years) |

| Stricter wastewater and solvent emission norms raise compliance costs | -0.9% | National, heavier burden on inland plants | Medium term (2-4 years) |

| Looming overcapacity risk amid aggressive gigafactory build-out | -2.4% | National, concentrated in coastal provinces | Short term (≤ 2 years) |

| Flake-graphite supply squeeze delays anode scale-up plans | -1.2% | National, export-control spillover effects | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Import Dependency for High-Nickel Cathode Precursors

Roughly 70% of the nickel sulfate used in NMC 811 and NCA cathodes is sourced from Indonesia, tying Chinese producers to potential export quotas and currency swings. A temporary ore-export pause in early 2024 sent nickel sulfate prices up 40%, while cobalt supplies from the Democratic Republic of Congo carry similar geopolitical risk. Manufacturers are pivoting toward LFP to cut exposure, yet premium EV models targeting 500+ km range still need high-nickel chemistries, leaving a sizeable slice of demand vulnerable to upstream disruptions.

Looming Overcapacity Risk Amid Aggressive Gigafactory Build-Out

Installed capacity climbed to about 2,500 GWh in 2024 versus only 1,250 GWh in shipments, forcing utilization down to 50% and driving a price war that compressed gross margins below 10% for most players. MIIT has warned provinces to curb new approvals, but local governments continue to court investments for employment gains. If overseas EV uptake slows or tariffs rise, China could face a prolonged shake-out, with distressed sales and bankruptcies consolidating the field further in the Chinese electric vehicle battery manufacturing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Battery Chemistry: LFP Dominance Amid Emerging Alternatives

LFP commanded roughly 69.42% of 2025 lithium-ion shipments, thanks to 30% cost savings versus NMC 811, 3,000+ cycle life, and freedom from cobalt exposure. BYD’s Blade Battery proved that prismatic LFP can pass nail-penetration tests without thermal runaway, reassuring premium OEMs. High-nickel NMC cells continue in range-focused flagships like Tesla’s Model S Plaid, yet their share is eroding as cell-to-pack designs push LFP energy density toward 180 Wh/kg. Sodium-ion, solid-state, and lithium-sulfur chemistries collectively expand at a 35.12% CAGR, signaling a hedge against future lithium or nickel price spikes. Pilot sodium-ion lines start mass output in June 2025 at 175 Wh/kg and -40 °C tolerance, perfect for northern commercial fleets. Overall, chemistry diversification buffers supply risk and positions the Chinese electric vehicle battery manufacturing market for multi-chemistry flexibility.

The China electric vehicle battery manufacturing market size for LFP cells stood near USD 41.18 billion in 2025 and is forecast to top USD 94.35 billion by 2031 as cost parity with internal-combustion powertrains accelerates adoption. Solid-state programs by CATL, BYD, and Envision AESC target >400 Wh/kg but still face solid-electrolyte interface stability hurdles, keeping them pre-commercial until 2026-2027. Nonetheless, early-stage investment unlocks optionality for mid-decade technology step-changes. NCA remains niche (<5% share) due to its higher cobalt content and limited domestic OEM deployment. The market’s chemistry mix illustrates China’s strategy of de-risking raw-material exposure while retaining performance headroom for premium export models.

By Cell Format: Prismatic Surge Driven by Manufacturing Efficiency

Pouch designs led in 2025 at 54.35%, prized for volumetric efficiency in irregular vehicle architectures. Yet prismatic variants are scaling at a 21.03% CAGR as automated stacking cuts handling steps and integrated cooling channels trim thermal gradients 15-20%. BYD’s Blade and CATL’s Qilin rely on long-format prisms to delete module frames and raise volumetric density to 255 Wh/L. Cylindrical 46 mm cells, while only 15% of shipments, target high-performance sedans where energy density trumps cost. The shift underlines how production economics guide format choice: prismatic suits high-volume, low-mix lines; pouch supports luxury derivatives; cylindrical serves performance niches.

Within this realignment, the China electric vehicle battery manufacturing market size for prismatic cells is projected to almost triple between 2025 and 2031, outpacing overall market CAGR as cell-to-pack designs proliferate. Scrap-rate reductions and lower tooling costs further tilt adoption toward prismatic. Meanwhile, pouch capacity consolidates among players with sophisticated winding expertise, and cylindrical growth hinges on automakers standardizing 46 mm formats across multiple platforms. Format diversity thus mirrors OEM segment strategies yet converges on shared goals of density uplift and cost efficiency.

By Propulsion: BEV Dominance Reinforced by Infrastructure Expansion

Battery electric vehicles (BEVs) absorbed 82.15% of 2025 battery demand and should sustain a 17.55% CAGR to 2031, far eclipsing plug-in hybrids (PHEVs). BEV architectures shed ICE components, automating production and cutting lifetime operating costs 15-20%. China’s public charging network exceeded 2.5 million stations in 2024, quelling range anxiety in top-tier cities. Policy design awards higher NEV credits to BEVs, steering automaker investment away from dual-powertrain complexity. Consequently, capacity planning in the China electric vehicle battery manufacturing market increasingly centers on 60-100 kWh pack formats.

PHEV and HEV modules remain transitional. PHEVs held roughly 15.4% of propulsion demand in 2025 but face diminishing relevance as fast-charging spreads nationwide. HEVs, reliant on sub-2 kWh batteries for idle-stop functions, account for a trivial share and are trending down. The propulsion mix points to battery makers prioritizing large-format cell lines, further consolidating scale advantages for suppliers aligned with long-range BEV platforms.

By Vehicle Type: Passenger Cars Lead, LCVs Accelerate

Passenger cars captured 87.76% of 2025 consumption, driven by consumer uptake of compact sedans and crossovers. Yet light commercial vehicles (LCVs) are the growth hotspot, expanding at a 19.11% CAGR through 2031 as tier-1 cities impose diesel restrictions on last-mile fleets. LCV operators emphasize total cost of ownership, making them receptive to long-cycle LFP or sodium-ion packs that promise >3,000 cycles. CATL’s sodium-ion launch targets exactly this segment, offering cold-weather resilience and raw-material savings. Medium and heavy trucks remain nascent (<5% share) but could scale once highway megawatt-level chargers proliferate.

The Chinese electric vehicle battery manufacturing market size linked to LCVs is expected to quadruple by 2031, supporting inland gigafactories near freight corridors. Buses plateau as early adoption cycles mature, and two-wheeler batteries, though high volume, deliver marginal revenue due to 1-3 kWh pack sizes. Therefore, while passenger cars underpin absolute volume, LCVs are evolving into a margin lever within the overall Chinese electric vehicle battery manufacturing market.

Geography Analysis

China’s battery footprint is split between export-oriented coastal hubs and resource-centric inland corridors. Coastal provinces, Jiangsu, Guangdong, and Fujian, host about 60% of installed capacity, leveraging proximity to Shanghai and Shenzhen ports for Europe-bound shipments. CATL’s Ningde base and BYD’s Shenzhen complex capitalize on deep supply ecosystems and skilled labor. Yet land scarcity, rising costs, and tighter emission enforcement are nudging incremental gigawatt-hour pipelines inland. Western provinces such as Qinghai and Sichuan now pitch a 20-25% logistics cost advantage by co-locating plants with lithium brine lakes and spodumene mines; Qinghai alone supplies 50% of national lithium carbonate.

Central provinces, Henan, Hubei, and Anhui, offer mid-cost manufacturing nodes with high-speed rail links to export harbors. CALB’s Chengdu line and SVOLT’s Changzhou campus illustrate this mid-corridor positioning, balancing inland incentives with export logistics. Renewable-rich regions such as Inner Mongolia provide discounted industrial power, slashing cathode sintering costs by up to one-fifth and improving environmental footprints. The result is a multi-node production lattice: coastal plants feed exports, western cells leverage feedstock proximity, and central hubs serve domestic OEMs.

Subsidy competition shapes the map. Sichuan granted CATL a decade-long property-tax holiday and half-price land to land a 50 GWh LFP plant; Guangdong fast-tracked permits to secure BYD’s 80 GWh Shenzhen expansion. While incentives accelerate technology diffusion, requiring knowledge-transfer clauses, they also risk entrenching structural overcapacity. Nonetheless, the geographic shift diversifies risk and enhances resilience for the Chinese electric vehicle battery manufacturing market.

Competitive Landscape

The top three suppliers, CATL, BYD, and CALB, held around 75% domestic shipments in 2024, underscoring high concentration even as overcapacity compresses margins. CATL emphasizes technology leadership and overseas localization, building a USD 7.8 billion Hungary plant to serve BMW, Ford, and Stellantis under EU rules. BYD leans on vertical integration, supplying its Dynasty and Ocean vehicle ranges and selectively selling to Tesla and Toyota, thereby insulating itself from price swings but capping external revenue. CALB targets commercial vehicles, exploiting LFP economics to win Geely and Chery contracts.

Technology innovation drives differentiation. CATL’s Qilin integrates cooling plates within the cell, hitting 255 Wh/kg and enabling OEMs to boost range without enlarging packs. BYD’s Blade passes nail-penetration safety tests, convincing premium OEMs of LFP suitability. SVOLT’s cobalt-free NMX cathode, launched in 2024, removes conflict-mineral exposure while matching NMC energy density. Patent filings back these moves: CATL lodged 1,200-plus battery patents in 2024, and BYD filed over 800, focusing on cell-to-body integration and thermal control.[4]World Intellectual Property Organization, “Patent Filings by Leading Battery Makers, 2024,” wipo.int

New entrants hunt white-space opportunities. HiNa Battery and Qing Tao Energy chase sodium-ion and solid-state niches where incumbent lithium-ion scale confers less advantage. Venture funding and provincial grants support their 2026-2027 commercialization timelines. Meanwhile, second-tier players like Gotion and EVE seek differentiation via vertical material integration or export licensing partnerships. The overarching contest in the Chinese electric vehicle battery manufacturing market revolves around technology moats and cost curves as commodity LFP prices slide toward USD 50 per kWh, demanding innovation-led margin defense.

China Electric Vehicle Battery Manufacturing Industry Leaders

BYD Co. Ltd

Panasonic Corporation

CALB (China Aviation Lithium Battery)

SVOLT Energy Technology

Gotion High-Tech

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: CATL began mass production of sodium-ion cells rated at 175 Wh/kg for 24-V truck auxiliary systems, broadening its chemistry portfolio.

- September 2024: CATL confirmed a USD 7.8 billion, 100 GWh plant in Debrecen, Hungary, targeting a 2025 start-up for Volkswagen and Stellantis supply.

- August 2024: BYD broke ground on six mainland plants totaling 150 GWh to back its 4 million EV sales objective by 2026.

- August 2024: CALB allocated USD 1.3 billion to expand its Chengdu site by 50 GWh, prioritizing LFP cells for light commercial vehicles.

China Electric Vehicle Battery Manufacturing Market Report Scope

The electric vehicle (EV) battery manufacturing market in China is experiencing rapid growth, driven by the country's aggressive push towards electrification and clean energy. The market is experiencing rapid growth, driven by increasing EV adoption and government incentives. Key materials essential for battery production include lithium, cobalt, nickel, and graphite. The demand is fueled by China's ambition to become a leading EV market promotes investment and innovation in battery manufacturing.

The China Electric Vehicle Battery Manufacturing Market is Segmented by Battery Chemistry (Lithium-ion (NMC, NCA, LFP, LTO), Nickel-Metal Hydride (NiMH), Lead-acid, and Emerging Solid-State/Sodium-ion), By Cell Format (Cylindrical, Prismatic, and Pouch), By Propulsion (BEV, PHEV, HEV), By Vehicle Class (Passenger Cars, Light Commercial Vehicles, Medium and Heavy Trucks, Buses and Coaches, and Two and Three-wheelers. The report also covers the market size and forecasts for the China Electric Vehicle Battery Manufacturing Market across the country. The Report Offers the Market Size and Forecasts in Revenue (USD) for all the Above.

| Lithium-ion (NMC, LFP, NCA) |

| Emerging (Solid-state, Li-S, Na-ion) |

| Lead-acid |

| Nickel-metal-hydride |

| Cylindrical |

| Prismatic |

| Pouch |

| Battery Electric Vehicle (BEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Hybrid Electric Vehicle (HEV) |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Trucks |

| Buses and Coaches |

| Two and Three-wheelers |

| By Battery Chemistry | Lithium-ion (NMC, LFP, NCA) |

| Emerging (Solid-state, Li-S, Na-ion) | |

| Lead-acid | |

| Nickel-metal-hydride | |

| By Cell Format | Cylindrical |

| Prismatic | |

| Pouch | |

| By Propulsion | Battery Electric Vehicle (BEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) | |

| Hybrid Electric Vehicle (HEV) | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| Medium and Heavy Trucks | |

| Buses and Coaches | |

| Two and Three-wheelers |

Key Questions Answered in the Report

How large is the China electric vehicle battery manufacturing market in 2026?

The market stands near USD 68.37 billion in 2026.

Which chemistry dominates cell output today?

LFP holds about 69.42% of 2025 shipments, favored for cost and safety advantages.

Why are prismatic cells gaining on pouch designs?

Automated stacking and integrated cooling make prismatic formats cheaper to scale and easier to assemble at pack level.

What risks threaten future capacity utilization?

Overcapacity from aggressive gigafactory build-outs and reliance on imported nickel sulfate could depress plant utilization and margins.

When will sodium-ion batteries reach commercial scale?

CATL began mass production in June 2025 for commercial-vehicle auxiliary systems, with broader applications expected after 2026.

Page last updated on: