Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

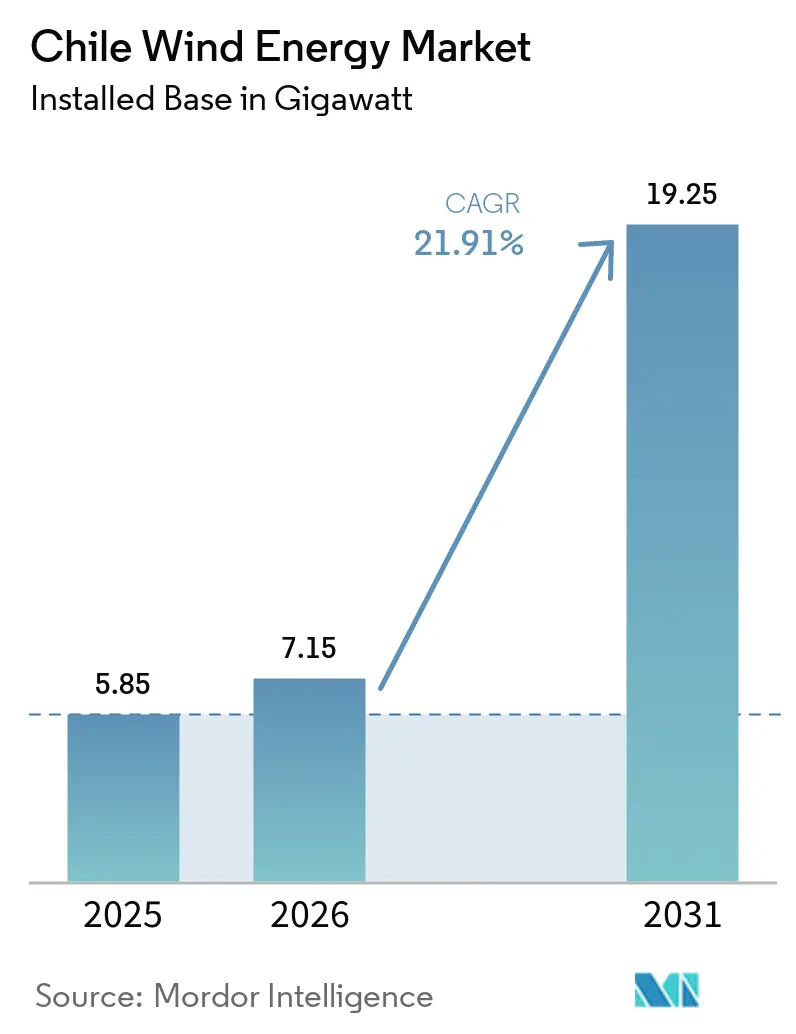

| Base Year Market Size (2025) | 5.85 gigawatt |

| Market Volume (2026) | 7.15 gigawatt |

| Market Volume (2031) | 19.25 gigawatt |

| Growth Rate (2026 - 2031) | 21.91% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Chile Wind Energy Market Analysis by Mordor Intelligence

The Chile Wind Energy Market size in terms of installed base was valued at 5.85 gigawatt in 2025 and is estimated to grow from 7.15 gigawatt in 2026 to reach 19.25 gigawatt by 2031, at a CAGR of 21.91% during the forecast period (2026-2031).

Supply-side momentum stems from merchant power-purchase agreements, green-hydrogen off-take contracts, and the 3 GW Kimal–Lo Aguirre HVDC line, which together remove curtailment bottlenecks and improve capacity factors. Copper miners demanding 24/7 renewable power anchor long-term contracts and smooth nodal prices, while a USD 50 billion pipeline dominated by Magallanes hydrogen projects signals a structural shift toward industrial off-grid demand.[1]Ministerio de Energía, “Planificación Energética de Largo Plazo 2023-2027,” ENERGIA.GOB.CL Developers increasingly favor ≥6 MW turbines that lower balance-of-system cost, and utility-scale wind-plus-storage portfolios are emerging to capture intraday price spreads of up to USD 200 per. Chinese OEM price competition compresses capex below USD 1 million per MW, but a proposed 2027 duty on imported turbines clouds near-term procurement strategy.[2]Coordinador Eléctrico Nacional, “Estadísticas,” COORDINADOR.CL Social-license conflicts and nodal-price cannibalisation persist as restraining factors, yet are partially mitigated by storage auctions and new consultation protocols.

Key Report Takeaways

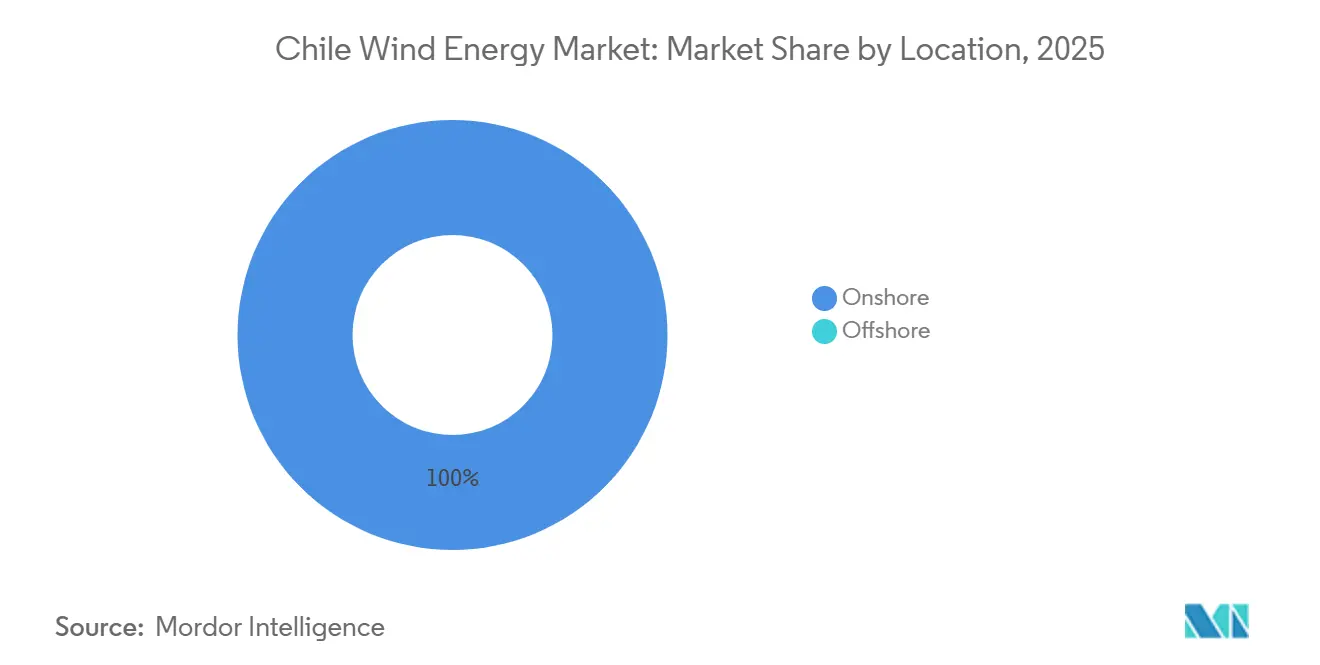

- By location, onshore wind held 100% of installed capacity and led with 21.9% CAGR to 2031, while offshore remained in feasibility stages.

- By turbine capacity, units rated up to 3 MW captured 44.9% of the Chile wind energy market share in 2025, whereas the above-6-MW class is forecast to expand at a 28.2% CAGR through 2031.

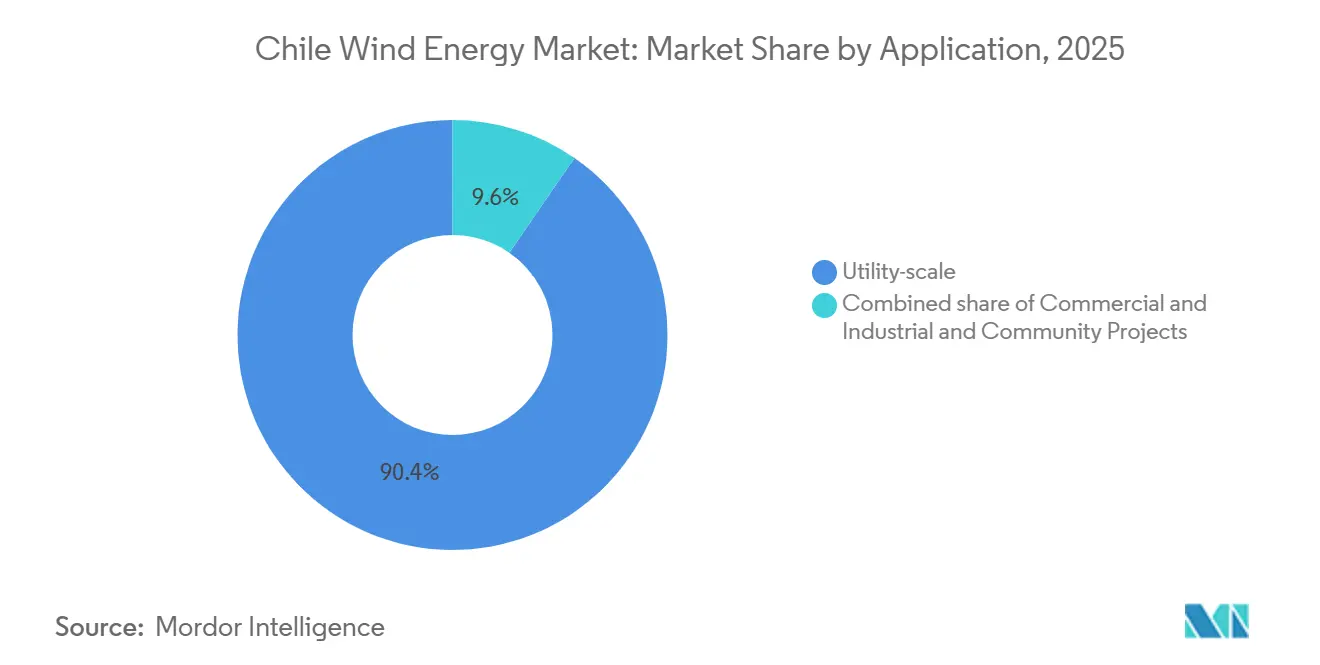

- By application, utility-scale projects commanded 90.4% of the Chile wind energy market size in 2025; the commercial-industrial segment posts the highest projected CAGR at 27.5% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Chile Wind Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Record-low onshore LCOE drives merchant PPAs | +3.8% | Antofagasta, Atacama, Coquimbo | Short term (≤ 2 years) |

| Green-hydrogen hubs pull wind off-take | +5.2% | Magallanes, Antofagasta | Long term (≥ 4 years) |

| HVDC Kimal-Lo Aguirre debottlenecks wind | +4.1% | Antofagasta, Atacama, Tarapacá | Medium term (2-4 years) |

| Floating-wind R&D tax credits | +0.9% | Valparaíso, Biobío | Long term (≥ 4 years) |

| Mining sector clean-power mandates | +3.6% | Antofagasta, Atacama, Coquimbo | Medium term (2-4 years) |

| Long-duration storage auctions | +2.4% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Record-low onshore LCOE drives merchant PPAs

Chile’s onshore levelized cost dropped below USD 30 per MWh in 2024, making wind 40% cheaper than coal or gas and enabling merchant contracts without auction backstops.[3]International Renewable Energy Agency, “Renewable Power Generation Costs in 2024,” IRENA.ORG Capacity factors above 45% in Patagonia and sub-USD 1 million per MW capex from Chinese turbines underpin this advantage. Merchant PPAs now cover 35% of new projects, transferring price risk from utilities to sponsors. AES Andes signed a 15-year merchant deal with BHP’s Escondida mine at a USD 40 floor indexed to copper, aligning energy costs with commodity cycles.[4]AES Corporation, “AES Andes Secures Financing for Wind-Storage Portfolio,” AES.COM Shorter development cycles and creditworthy mining off-takers accelerate installations in the northern corridor.

Green-hydrogen hubs pull wind off-take

Magallanes hosts 16.9 GW of wind aimed at hydrogen, 57% of Chile’s queue, with USD 31.5 billion in announced capex. HNH Energy’s 1.4 GW San Gregorio farm will feed 800,000 t/y green ammonia from 2026-2028 under 20-year Asian contracts. Electrolyzers run at 60-70% utilization, smoothing intermittency and bypassing grid studies. EDF-Enap’s 1.2 GW Cabo Negro hub integrates desalination and port facilities to supply green methanol to shipping lines. Private lines avoid grid congestion, insulating projects from nodal-price volatility and curtailment.

HVDC Kimal–Lo Aguirre de-bottlenecks wind

The 3 GW, 1,500 km HVDC link awarded in 2025 will move stranded northern wind to central demand, removing a 14.5% curtailment rate recorded in early 2024. Voltage-source converters stabilize weak grids and enable reverse power flows. The line unlocks 8 GW of stalled projects and reduces intraday price swings to a USD 40 range. Colbún advanced a 400 MW expansion after the award, showing how transmission certainty converts pipelines to bankable assets.

Floating-wind R&D tax credits

Chile’s 2026-2028 program refunds 40% of pre-commercial floating-wind spending, targeting 50-150 MW pilots off Valparaíso and Biobío. Studies by Mainstream and Equinor found 12 GW of potential, but seismic risk raises insurance premiums, and caps leverage at 60%. Tax credits offset prototype costs and shorten the path to early-2030s commercialization, especially for hydrogen hubs needing coastal proximity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Nodal price cannibalisation in SIC grid | -2.7% | Santiago, Valparaíso, Antofagasta | Short term (≤ 2 years) |

| Social-licence conflicts in Biobío & Araucanía | -1.8% | Biobío, Araucanía | Medium term (2-4 years) |

| Rising Chinese turbine import duties | -1.2% | National | Medium term (2-4 years) |

| Offshore seismic-tsunami risk premiums | -0.6% | Valparaíso, Biobío, Los Lagos | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Nodal price cannibalisation in SIC grid

Curtailment hit 14.5% in Q1 2024 as midday solar forced nodal prices negative in northern nodes, making wind uneconomic and hindering 2.2 GW under construction. Developers renegotiated debt covenants after a 22% revenue drop. Relief hinges on the HVDC line, yet four years of exposure raises required equity returns by 300-400 basis points and delays final investment decisions.

Social-licence conflicts in Biobío & Araucanía

Mapuche communities invoked ILO 169 to challenge EIAs, stalling 500 MW since 2024. Pattern Energy’s Arauco project saw capex rise 8% and permitting extend 14 months after revenue-sharing demands. New 2025 protocols add binding arbitration and 120-day engagement, lengthening timelines by six to nine months and escalating pre-construction costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Location: Onshore Dominance Persists Through 2031

Onshore installations represented 100% of capacity in 2025 and will grow at a 21.9% CAGR, reflecting sub-USD 30 LCOE and streamlined permitting. The Chile wind energy market size for onshore projects is projected to reach 19.25 GW by 2031, sustained by a 29.4 GW pipeline and the absence of viable offshore alternatives. Goldwind’s 342 MW Lomas de Taltal, completed in 2024, delivered a 48% capacity factor at USD 950,000 per MW, showcasing cost leadership.

Offshore wind remains pre-commercial. Mainstream and Equinor identified 12 GW of floating potential, yet seismic premiums and supply-chain gaps restrict leverage and inflate LCOE. A 40% R&D tax credit covers prototypes, but full rollout will arrive in the 2030s. Until capex converges, onshore will supply all incremental capacity, cementing Chile’s status as a land-based wind leader within Latin America.

By Turbine Capacity: Above-6-MW Units Reshape Economics

Turbines up to 3 MW held 44.9% of Chile's wind energy market share in 2025, a legacy of 2014-2022 fleets using Vestas V110-2.0 MW models. However, the above-6-MW segment is forecast at a 28.2% CAGR as developers deploy Goldwind 7.5 MW and forthcoming Vestas V172-7.2 MW platforms, cutting balance-of-system costs 12-15%. The Chile wind energy market size for these large units is expected to surpass 8 GW by 2031.

Mid-range 3 to 6 MW turbines grow at the market average, favored by developers prioritizing proven logistics. Sub-3-MW units will focus on repowering where existing grid connections remain. Larger turbines require specialized cranes and transport, yet higher energy yield offsets logistics cost, driving fleet migration toward above 6 MW ratings.

By Application: Commercial-Industrial Growth Outpaces Utility-Scale

Utility-scale projects accounted for 90.4% of installed capacity in 2025. The segment adds bulk volume through 500 MW-plus farms contracted to miners and hydrogen hubs. The commercial-industrial niche will rise at a 27.5% CAGR under PMGD rules that exempt <9 MW projects from dispatch and transmission fees. BHP’s 7.5 MW Escondida turbine is locked in at USD 32 per MWh behind-the-meter, underscoring the economics.

Community projects remain under 1% due to limited finances. Utility-scale still leads absolute megawatts, but industrial self-supply grabs the fastest growth as firms bypass grid volatility and secure cost savings, elevating diversification within the Chile wind energy market.

Geography Analysis

Northern Antofagasta, Atacama, and Tarapacá host 4.2 GW of pipeline aimed at mining loads that consume 2.8 GW, supported by copper-indexed PPAs. Capacity factors exceed 45% yet curtailment spiked to 14.5%. The HVDC link will move 3 GW south, unlock 8 GW now stalled, and compress price swings.

Central Santiago-Valparaíso absorbed 38% of 2024 wind generation. Enel’s Sierra Gorda Este and Colbún’s Horizonte supply fixed-price contracts around USD 42 per MWh, giving utilities firm capacity toward Chile’s 80% renewable target. Mapuche consultations in adjoining regions delay over 500 MW, adding 6-9 months to permitting.

Magallanes in Patagonia holds 16.9 GW pipeline, 57% of the total, for export hydrogen. HNH’s San Gregorio and EDF-Enap’s Cabo Negro pair wind with electrolyzers and port infrastructure, avoiding the national grid and reaching 50% capacity factors. Remoteness lifts capex 20-25% yet isolates projects from curtailment, illustrating a bifurcated Chile wind energy market anchored by domestic demand in the north-central belt and export-oriented hubs in the far south.

Competitive Landscape

Enel Green Power leads with 29% generation share, followed by Colbún at 14% and AES Andes at 12%. Incumbents pursue vertical integration: Colbún raised USD 500 million in green bonds to refinance Horizonte and fund Peruvian expansion, while AES Andes secured USD 550 million for 500 MW storage co-located with wind. Mid-tier players such as Mainstream, Innergex, Pattern, and EDF diversify through storage or hydrogen partnerships.

Goldwind disrupted the supply chain by delivering 7.5 MW turbines at Lomas de Taltal, priced 15-20% below European rivals. Vestas responded with a 128 MW order, pairing 20-year service guarantees to protect its share. Draft 2027 duties on Chinese turbines create a near-term purchasing window and pressure Western OEM localization.

White space opportunity lies in <9 MW PMGD projects offering 14% returns. Developers able to arbitrage OEM pricing, storage value stacking, and captive mining demand will outperform within an increasingly competitive Chile wind energy market.

Chile Wind Energy Industry Leaders

Acciona Energía

Enel Green Power Chile

Colbún S.A.

AES Andes

Mainstream Renewable Power

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Mainstream Renewable Power announced that the Ckhúri Wind Farm has received Commercial Operations Date (COD) certification, representing a further expansion of Chile's renewable energy generation portfolio.

- September 2025: Colbún issued USD 500 million green bond at 4.8% coupon to refinance 816 MW Horizonte wind farm and fund Peru expansion.

- August 2025: Vestas won a 128 MW order for V150-4.2 MW turbines, bundling 20-year service and machine-learning-based maintenance.

- July 2025: AES Andes began building a 1.325 GW wind-plus-storage portfolio across Antofagasta and Atacama, total capex of USD 1.8 billion.

Chile Wind Energy Market Report Scope

Wind energy refers to the process of using the movement of air to convert it into mechanical power or electricity.

The Chilean wind energy market is segmented by location of deployment and application. By location of deployment, it is segmented into onshore and offshore. By application, the market is divided into utility-scale, commercial and industrial, and community projects. The market size and forecasts for each segment have been done regarding installed capacity (GW).

By Location

| Onshore |

| Offshore |

By Turbine Capacity

| Up to 3 MW |

| 3 to 6 MW |

| Above 6 MW |

By Application

| Utility-scale |

| Commercial and Industrial |

| Community Projects |

By Component (Qualitative Analysis)

| Nacelle/Turbine |

| Blade |

| Tower |

| Generator and Gearbox |

| Balance-of-System |

| By Location | Onshore |

| Offshore | |

| By Turbine Capacity | Up to 3 MW |

| 3 to 6 MW | |

| Above 6 MW | |

| By Application | Utility-scale |

| Commercial and Industrial | |

| Community Projects | |

| By Component (Qualitative Analysis) | Nacelle/Turbine |

| Blade | |

| Tower | |

| Generator and Gearbox | |

| Balance-of-System |

Key Questions Answered in the Report

How fast is the Chile wind energy market expected to grow to 2031?

Installed capacity is set to rise from 7.15 GW in 2026 to 19.25 GW by 2031, reflecting a 21.91% CAGR.

What drives new investment in Chilean wind projects?

Merchant PPAs, green-hydrogen off-take contracts, and supportive storage auctions underpin capital inflows.

Which region holds most future wind capacity in Chile?

Magallanes accounts for 16.9 GW of the pipeline, primarily linked to export-oriented hydrogen hubs.

Why are above 6 MW turbines gaining share in Chile?

Larger units raise capacity factors and reduce balance-of-system cost per MW, lowering LCOE by up to 15%.

How will the Kimal'Lo Aguirre HVDC line affect wind curtailment?

Once commissioned in 2029, it will move 3 GW of northern wind south and is expected to cut curtailment materially.

Page last updated on: