Carbon Fiber Reinforced Thermoplastic (CFRTP) Composite Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

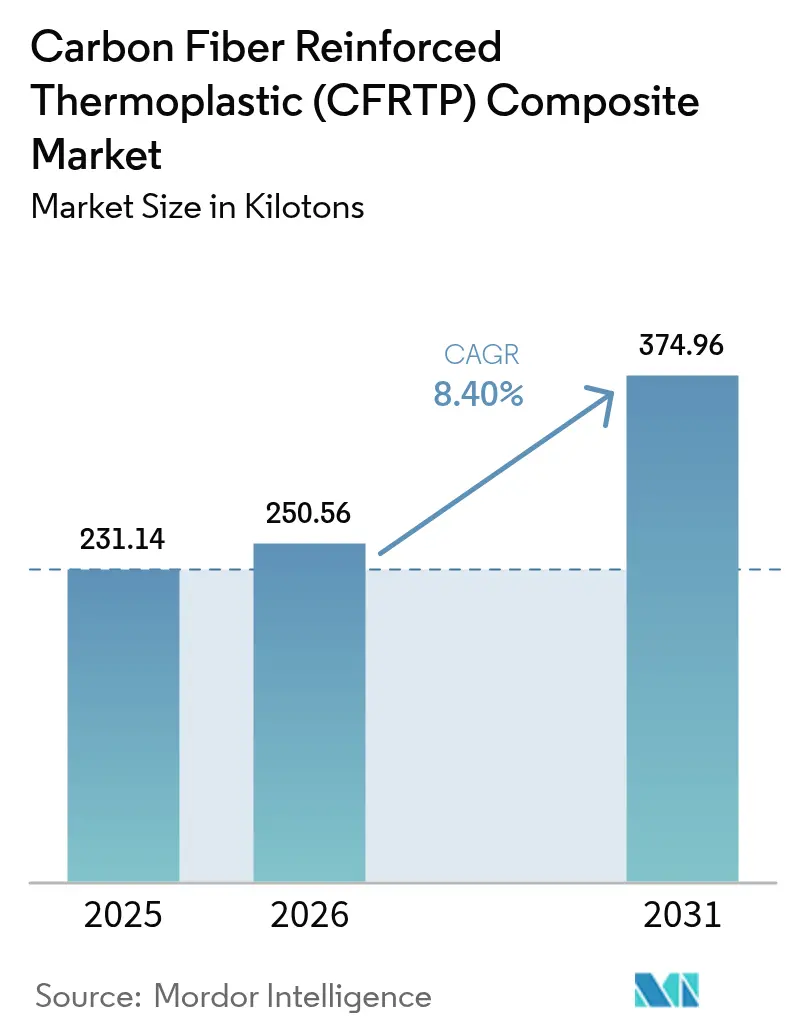

| Market Volume (2026) | 250.56 kilotons |

| Market Volume (2031) | 374.96 kilotons |

| Growth Rate (2026 - 2031) | 8.40% CAGR |

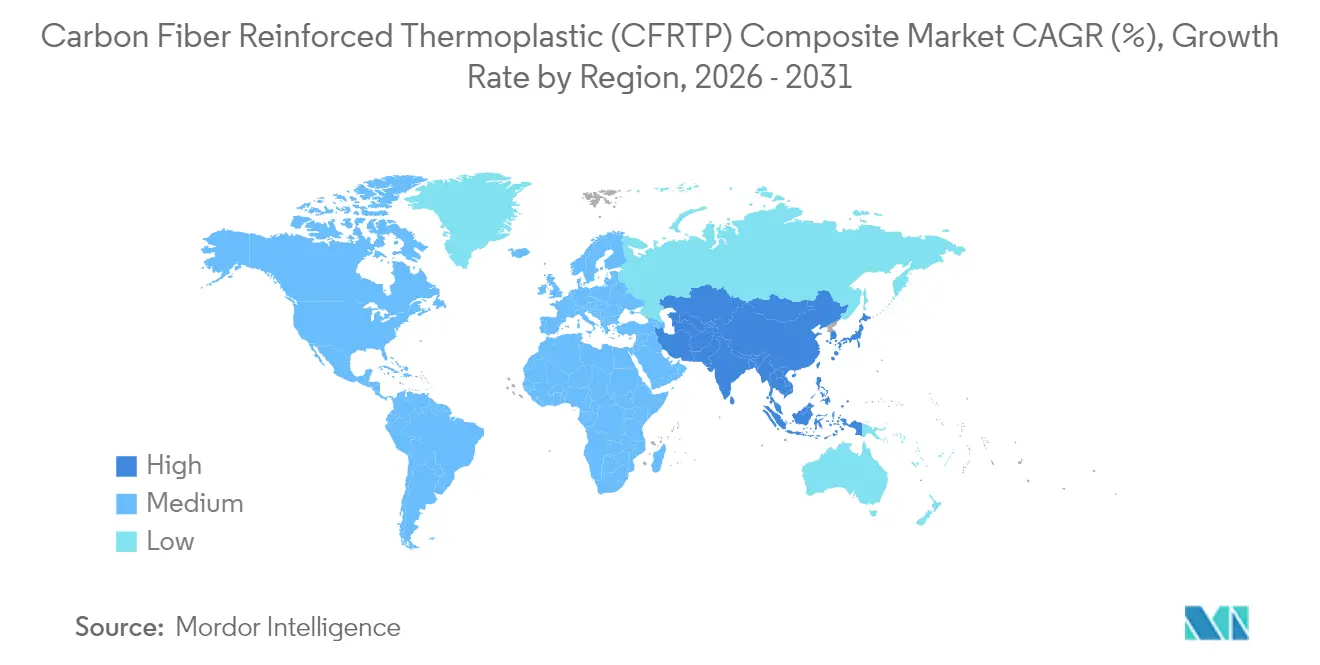

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

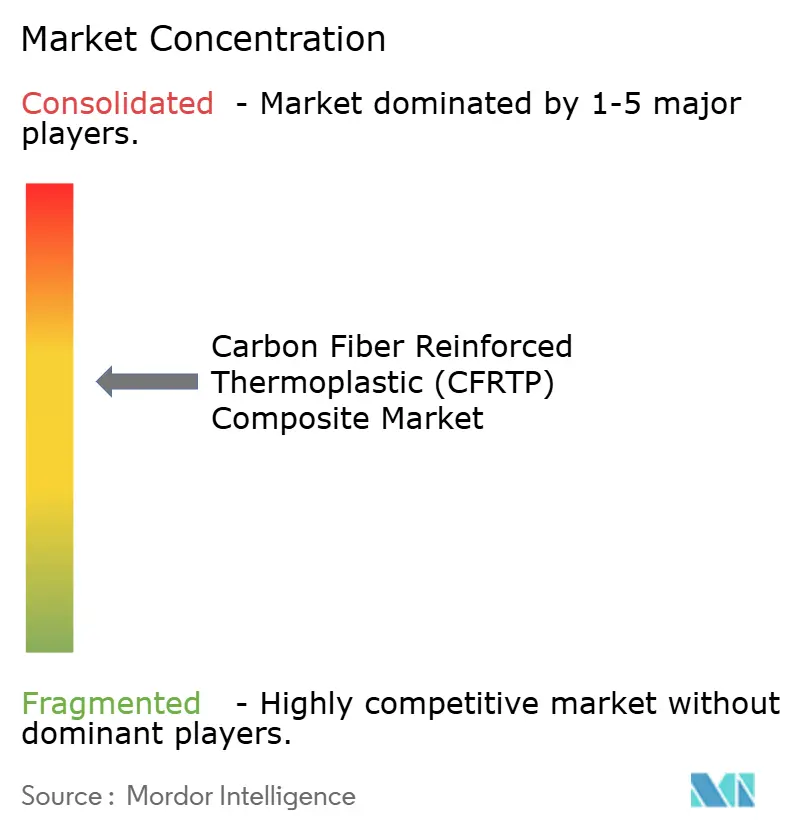

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Carbon Fiber Reinforced Thermoplastic (CFRTP) Composite Market Analysis by Mordor Intelligence

Carbon Fiber Reinforced Thermoplastic Composite market size in 2026 is estimated at 250.56 kilotons, growing from 2025 value of 231.14 kilotons with 2031 projections showing 374.96 kilotons, growing at 8.40% CAGR over 2026-2031. Robust growth reflects the material’s ability to pair aerospace-grade strength-to-weight ratios with full recyclability, aligning with decarbonization targets across transportation, energy, and construction. Rising electric‐vehicle production, a rebound in commercial aircraft build rates, and fast-moving hydrogen storage programs form the core demand pillars. At the same time, breakthroughs in energy-efficient fiber production and additive manufacturing lower entry barriers, while regional recycling mandates open fresh revenue pools for suppliers. Competitive intensity is building as integrated incumbents defend share against regional capacity buildouts and specialist recyclers.

Key Report Takeaways

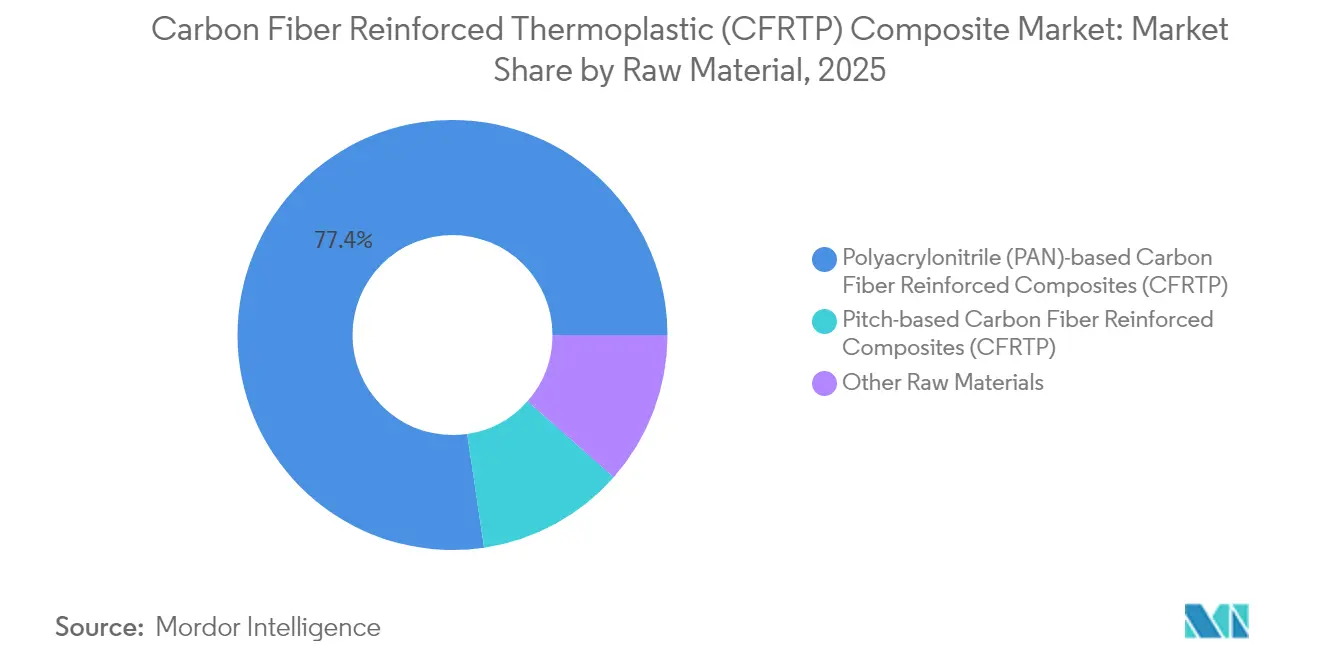

- By raw material, PAN-based grades led with 77.35% revenue share in 2025, while the Other Raw Materials segment is advancing at a 9.42% CAGR through 2031.

- By resin, PEEK captured 34.25% of the carbon fiber reinforced thermoplastic composite market share in 2025 and is also the fastest-growing resin at 9.61% CAGR through 2031.

- By manufacturing process, compression and stamp molding held 39.05% of the 2025 volume, whereas additive manufacturing records the highest projected CAGR of 9.46% to 2031.

- By end-user industry, aerospace and defense accounted for 41.68% share of the carbon fiber reinforced thermoplastic composite market size in 2025 and is progressing at a 9.23% CAGR through 2031.

- By geography, North America dominated with 35.78% share in 2025, and Asia-Pacific is the fastest-expanding region at 8.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Carbon Fiber Reinforced Thermoplastic (CFRTP) Composite Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for lightweight EV structures | +2.1% | Global, with concentration in China, Europe, North America | Medium term (2-4 years) |

| Accelerating commercial aircraft production ramp-ups | +1.8% | Global, led by North America and Europe | Medium term (2-4 years) |

| Stringent global emission and recyclability mandates | +1.5% | Global, with EU leading regulatory framework | Long term (≥ 4 years) |

| Increasing usage in the construction sector | +1.2% | APAC core, spill-over to North America and Europe | Long term (≥ 4 years) |

| Rapid scale-up of hydrogen pressure-vessel programs | +1.9% | Global, with early gains in Japan, Germany, California | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Lightweight EV Structures

Automakers increase carbon fiber thermoplastic use in battery enclosures, body panels, and chassis members to extend driving range and cut charging time. The material’s reversible melt behavior supports end-of-life recycling, satisfying circular-economy rules now unfolding in China and the European Union. Fleet operators benefit from easier repair because damaged parts can be reheated and reshaped instead of replaced. Tesla’s application of carbon fiber composites in its humanoid robot underscores versatility beyond vehicles, suggesting spillover into multiple mobility platforms. China consumed 69,000 metric tons of carbon fiber in 2024, evidence of a deepening Asian demand base.

Accelerating Commercial Aircraft Production Ramp-ups

Airframe OEMs are rebuilding supply chains to meet higher 737 MAX and 787 Dreamliner output targets, sustaining composite demand for secondary structures that cut fuel burn. Hexcel reaffirmed investment in lightweight thermoplastic solutions in its Q1 2025 earnings report, despite lower top-line sales. The shift to more-electric aircraft fosters thermoplastic adoption because the matrix insulates wiring and integrates anti-icing heaters. European initiatives under the ThermoPlastic Composites Research Center (TPRC) accelerate certification of large-volume parts, shortening design-to-flight timelines. Superior fatigue resistance over metals lengthens service intervals, an advantage keenly valued by airlines after COVID-19 disruptions.

Stringent Global Emission and Recyclability Mandates

Regulators link life-cycle emissions to material choice, pushing OEMs toward recyclable thermoplastics. The EU is debating a ban on non-recyclable carbon composites in vehicles from 2029, steering R&D into mechanically recoverable fiber streams. Process innovators recover fibers retaining 93.6% tensile strength, opening secondary markets in sporting goods and electronics. The U.S. Department of Energy lists carbon fiber reinforced thermoplastic composites as critical for energy-efficiency goals, unlocking federal funding for pilot plants[1]U.S. Department of Energy, “Harsh Environment Materials Roadmap,” energy.gov. Fairmat and similar start-ups export recycled chips that substitute virgin material in non-safety-critical uses, lowering cost and carbon footprint.

Rapid Scale-up of Hydrogen Pressure-Vessel Programs

Type 3, 4, and 5 tanks require burst strength beyond 700 bar, an area where thermoplastic composites excel because of superior fatigue performance. Toray forecasts 42% annual growth in hydrogen tank demand as mobility and stationary projects leave the lab and enter scale-up. Infinite Composites collaborates with Oak Ridge National Laboratory to design field-repairable thermoplastic liners that lengthen vessel life. German and Japanese policymakers subsidize refueling corridors, catalyzing early offtake for certified tank suppliers. Re-formability lets operators cut downtime by requalifying vessels on site instead of full replacement.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High initial investment and manufacturing cost | -1.4% | Global, with higher impact in emerging markets | Short term (≤ 2 years) |

| Limited large-scale thermoforming press capacity | -0.8% | Global, concentrated in established manufacturing hubs | Medium term (2-4 years) |

| Supply-chain weaponization risk in aerospace | -0.6% | Global, with focus on US-China trade tensions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Investment and Manufacturing Cost

Autoclaves, compression presses, and automated fiber placement cells can top USD 30 million per line, curbing entry and slowing adoption in price-sensitive segments. SGL Carbon reported a 35.2% sales drop in its Carbon Fibers unit in 2024, citing demand swings that leave high fixed-cost assets under-utilized. Plasma + microwave heating demonstrated at the University of Limerick cuts energy up to 70%, yet commercial readiness remains several years out. Raw fiber remains costlier than aluminum or steel, keeping composites out of economy-class vehicles. Economics improve only when volumes amortize tooling, thus OEMs hesitate until downstream demand is locked.

Limited Large-scale Thermoforming Press Capacity

Presses working above 300 °C and 100 bar are scarce, creating lead-time bottlenecks for large auto body-in-white and aircraft skin panels. Hexcel’s automated preform lines shorten cycle time but cannot alone satisfy rising volume. Albany International bought CirComp to gain specialty thermoplastic molding expertise, signaling industry need to secure press infrastructure. New installs can take 18 months from order to start-up, complicating OEM ramp schedules. Without wider deployment, thermoplastic uptake in high-volume programs may lag projections.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material: PAN-based Dominance Faces Recycling Disruption

PAN-based grades delivered 77.35% of 2025 volume, underlining their entrenched production lines and aerospace heritage. High tensile modulus lets designers trim structural weight while meeting safety margins. The carbon fiber reinforced thermoplastic composite market size for PAN-based grades is projected to expand at a stable 7.76% CAGR as incumbents retrofit continuous lines for higher throughput. Cost-effective reheat cycles improve scrap rates, enhancing plant economics.

Other Raw Materials, including recycled fiber, register a 9.42% CAGR—the highest within raw materials—as end-users adopt circular procurement goals. Recycled fiber now retains 93.6% of virgin tensile strength, widening suitability for secondary load paths. Bio-sourced acrylonitrile under study by Syensqo and Trillium signals a longer-term pivot to greener feedstocks. Niche pitch-based grades serve thermal management in battery packs because of metal-like conductivity. Though volume small, premium pricing balances supply constraint, keeping margins attractive.

By Resin: PEEK’s Dual Leadership Reflects Performance Premium

PEEK secured 34.25% 2025 share and leads growth at 9.61% CAGR thanks to 250 °C continuous-use temperature and chemical inertness. The carbon fiber reinforced thermoplastic composite market share advantage strengthens where flammability and smoke toxicity rules are strict, notably in jet engines and offshore platforms. Medical device usage diversifies revenue, spreading risk across sectors.

Cost-focused segments rely on PU, PES, or PEI which trade peak temperature for price. These resins feed interior panels and consumer electronics where operating loads are moderate. Bio-based PEI under exploration could add a sustainability differentiator without forfeiting mechanical properties. Resin formulators also blend nano-fillers to enhance conductivity, fostering integrated de-icing layers in aerospace systems.

By Manufacturing Process: Compression Molding Leads as Additive Manufacturing Accelerates

Compression and stamp molding delivered 39.05% 2025 volume on the strength of automotive investments that favor short takt times and 60% fiber volume fractions. Automation trims labor and increases repeatability, supporting six-sigma quality. The carbon fiber reinforced thermoplastic composite market size associated with compression molding grows steadily as OEMs scale fuel-cell vehicle floor pans.

Additive manufacturing, at a 9.46% CAGR, disrupts low-volume, high-complexity parts. Continuous-fiber filament printers from Markforged and 9T Labs enable lattice-filled brackets with 60% lighter weight than machined aluminum. University of Limerick’s plasma heating may cut energy during sintering, bringing per-part cost closer to injection molding. Automated tape laying reaches 1,000 in/min lay-up speeds, meeting fuselage rate demands.

By End-user Industry: Aerospace Drives Both Volume and Growth

Aerospace and defense absorbed 41.68% of 2025 tonnage and expands at 9.23% CAGR as Boeing and Airbus restore single-aisle build cadences. The carbon fiber reinforced thermoplastic composite market size inside aerospace benefits from regulatory familiarity with composites, lowering certification hurdles. Defence primes layer radar-absorbing additives, giving weight savings plus stealth.

Automotive remains second in volume but faces EU scrutiny over respirable fiber dust, pushing firms to prove recycling pathways. Construction uptake in carbon fiber reinforced concrete grows as architects target net-zero structures. The CUBE building in Germany showcases 50% material savings versus steel reinforcement. Wind turbine blades lengthen beyond 100 m as fatigue-proof carbon spars enable larger swept area.

Geography Analysis

North America held 35.78% share in 2025, anchored by the United States’ aerospace and defence complex and supported by Canada’s MRO hubs. Local presence of Toray, Hexcel, and Solvay shortens lead times, safeguarding programs against geopolitical risk. Government grants under the Inflation Reduction Act encourage domestic hydrogen tank production, widening downstream pull.

Asia-Pacific posts the fastest 8.98% CAGR to 2031. China scales electric-vehicle output and now hosts multiple kiloton-scale carbon fiber lines, reducing earlier import dependence. Japanese pioneers Toray and Teijin double capacity to serve regional wind and marine projects. South Korea leverages electronics know-how to integrate EMI-shielding composites into 5G infrastructure.

Europe mixes strong demand with new regulatory headwinds. Germany’s auto base remains the largest segment consumer, but looming recyclability rules fast-track thermoplastic substitution. The ThermoPlastic Composites Research Center in the Netherlands anchors R&D alliances across OEMs and suppliers. Nordic wind investments and French aerospace clusters offset softness in general industrial demand.

Competitive Landscape

The market shows moderate concentration with the top five suppliers controlling just under 60% of global tonnage, led by Toray, Hexcel, Solvay, Teijin, and SGL Carbon. Integrated chains from precursor to prepreg shield incumbents from raw-material volatility. Toray’s 2024 acquisition of Gordon Plastics’ Colorado facility widens continuous carbon fiber thermoplastic capacity[2]Toray Advanced Composites, “Acquisition of Gordon Plastics,” toraytac.com.

Hexcel invests in automated preforming to compress cycle times and retain engine nacelle contracts, while Solvay re-branded its composites unit as Syensqo to sharpen focus on circular products. Mid-tier firms pursue vertical mergers; Albany International’s purchase of CirComp delivers filament-winding capability in high-temperature thermoplastic grades.

Recycling specialists such as Fairmat enter long-term supply agreements with consumer-electronics makers, shifting competitive metrics toward carbon footprint and reclaim percentage. Regional Chinese producers add 25 kt of PAN-based capacity by 2026, pressuring price but easing downstream shortages. Digital manufacturing startups court aerospace primes with topology-optimized lattice parts that cut assembly count.

Carbon Fiber Reinforced Thermoplastic (CFRTP) Composite Industry Leaders

Toray Industries Inc.

Solvay SA

Teijin Ltd.

Hexcel Corporation

SGL Carbon SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Syensqo joined the ThermoPlastic Composites Research Center (TPRC) and established partnerships with Trillium for bio-based acrylonitrile production and with Baker Hughes to develop offshore composite systems.

- November 2024: Toray Advanced Composites acquired Gordon Plastics' assets to increase its continuous carbon fiber thermoplastic composite production capacity in Colorado.

Global Carbon Fiber Reinforced Thermoplastic (CFRTP) Composite Market Report Scope

Carbon fiber-reinforced thermoplastic composites are composed of two primary elements: a reinforcement and a matrix. Carbon fiber serves as the reinforcement in CFRP, lending it its robustness. Meanwhile, the matrix, typically a thermosetting plastic-like polyester resin, acts as the binding agent for these reinforcements. These composites boast remarkable traits, including a superior strength-to-weight ratio, heightened wear resistance, and exceptional stiffness. These attributes not only surpass those of traditional materials like metals but also render them indispensable in a wide array of industrial settings.

The carbon fiber-reinforced thermoplastic composite market is segmented by raw material, resin, end-user industry, and geography. By raw material, the market is segmented into polyacrylonitrile (PAN)-based CFRTP, pitch-based CFRTP, and other raw materials. By resin, the market is categorized into polyether ether ketone (PEEK), polyurethane (PU), polyethersulfone (PES), polyetherimide (PEI), and other resins. By end-user industry, the market is segmented into aerospace and defense, automotive, construction, electrical and electronics, marine, sports equipment, wind turbines, and other end-user industries. The report also covers the market size and forecasts for the carbon fiber-reinforced thermoplastic composite market for 27 major countries. For each segment, the market sizing and forecasts are done in terms of value (USD).

| Polyacrylonitrile (PAN)-based Carbon Fiber Reinforced Composites (CFRTP) |

| Pitch-based Carbon Fiber Reinforced Composites (CFRTP) |

| Other Raw Materials (Recycled Carbon Fibers, etc.) |

| Polyether Ether Ketone (PEEK) |

| Polyurethane (PU) |

| PolyetherSulfone (PES) |

| Polyetherimide (PEI) |

| Others (Polyamide, Polycarbonate, etc.) |

| Compression and Stamp Moulding |

| Automated Fibre Placement / Tape Laying |

| Injection and Over-Moulding |

| Additive Manufacturing (Carbon Fiber-filled filaments) |

| Aerospace and Defence |

| Automotive |

| Construction |

| Electrical and Electronics |

| Wind Turbines |

| Marine |

| Sporting Equipments |

| Other End-user Industries (Healthcare, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Raw Material | Polyacrylonitrile (PAN)-based Carbon Fiber Reinforced Composites (CFRTP) | |

| Pitch-based Carbon Fiber Reinforced Composites (CFRTP) | ||

| Other Raw Materials (Recycled Carbon Fibers, etc.) | ||

| By Resin | Polyether Ether Ketone (PEEK) | |

| Polyurethane (PU) | ||

| PolyetherSulfone (PES) | ||

| Polyetherimide (PEI) | ||

| Others (Polyamide, Polycarbonate, etc.) | ||

| By Manufacturing Process | Compression and Stamp Moulding | |

| Automated Fibre Placement / Tape Laying | ||

| Injection and Over-Moulding | ||

| Additive Manufacturing (Carbon Fiber-filled filaments) | ||

| By End-user Industry | Aerospace and Defence | |

| Automotive | ||

| Construction | ||

| Electrical and Electronics | ||

| Wind Turbines | ||

| Marine | ||

| Sporting Equipments | ||

| Other End-user Industries (Healthcare, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How fast will the carbon fiber reinforced thermoplastic composite market grow through 2031?

Industry volume is projected to rise from 250.56 kilotons in 2026 to 374.96 kilotons by 2031, reflecting an 8.40% CAGR.

Which raw material leads the carbon fiber reinforced thermoplastic composite industry?

PAN-based grades dominate with 77.35% 2025 share, thanks to mature supply chains and proven performance.

Why is PEEK seeing the highest growth among resins?

PEEK pairs exceptional 250 °C heat resistance with chemical stability, giving it 34.25% share and a 9.61% CAGR in aerospace, energy, and medical parts.

What region offers the fastest demand upside?

Asia-Pacific is forecast to expand at 8.98% CAGR to 2031, propelled by electric-vehicle scaling in China and hydrogen programs in Japan and South Korea.

How is recycling shaping competitive dynamics?

Mechanical recovery processes now retain 93.6% fiber strength, letting recyclers feed secondary markets and compelling incumbents to integrate closed-loop offerings.

Page last updated on: