Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.39 Billion |

| Market Size (2026) | USD 3.27 Billion |

| Market Size (2031) | USD 15.77 Billion |

| Growth Rate (2026 - 2031) | 36.95% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Canada Mobile Payments Market Analysis by Mordor Intelligence

The Canada mobile payments market size is expected to grow from USD 2.39 billion in 2025 to USD 3.27 billion in 2026 and is forecast to reach USD 15.77 billion by 2031 at 36.95% CAGR over 2026-2031. The surge reflects rapid digitization of financial services, aggressive modernization of payment infrastructure, widespread consumer acceptance of contactless technology, and the displacement of cash at the point of sale. Digital payments already account for 86% of national payment volume, with contactless transactions representing 53% of all payments in 2024, highlighting a broad behavioral shift among Canadians.[1]Innovation, Science and Economic Development Canada, “High-Speed Access for All: Canada’s Connectivity Strategy,” ised-isde.canada.ca Government programs such as Real-Time Rail (RTR) and the Consumer-Driven Banking Framework are unlocking new avenues for product innovation while addressing latency and data-sharing barriers that historically limited market expansion. Retailers are bolstering uptake by embedding payments into loyalty programs, while wearable and smartphone-enabled fare collection is transforming urban mobility and accelerating transaction volumes. Together, these forces place the Canada mobile payments market among the fastest-growing ecosystems worldwide.

Key Report Takeaways

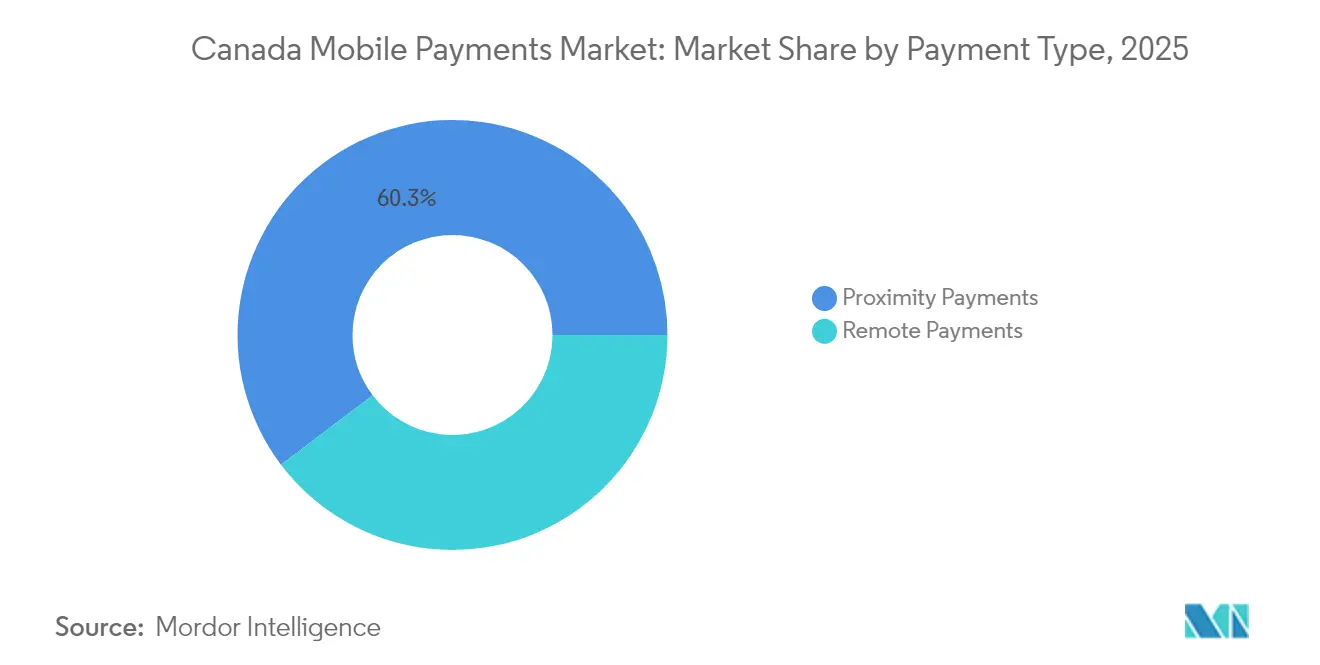

- By payment type, proximity transactions led with a 60.30% revenue share in 2025, while remote payments are set to post the highest CAGR at 38.05% through 2031.

- By transaction type, point of sale held 53.40% of the Canada mobile payments market share in 2025, whereas transit and ticketing transactions are projected to advance at a 39.95% CAGR to 2031.

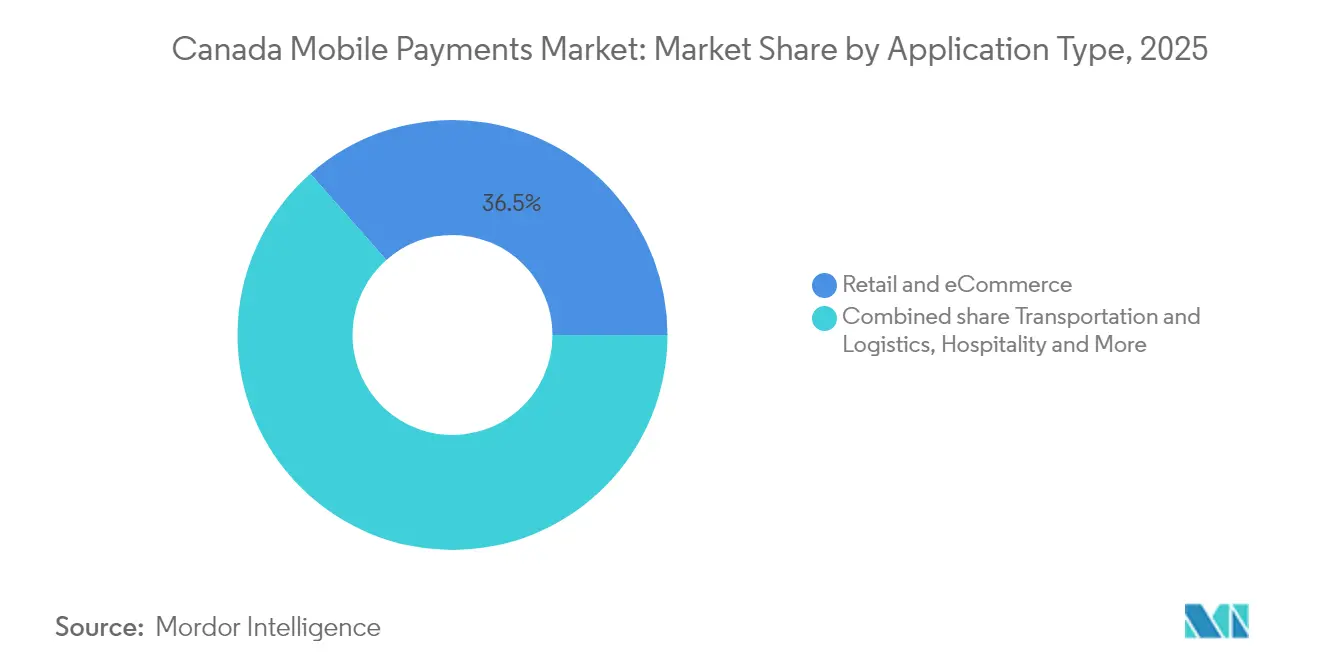

- By application, retail and wholesale captured 36.50% of the Canada mobile payments market size in 2025; transportation and logistics is poised for the fastest growth at 40.40% CAGR.

- By end-user, personal users commanded 56.40% of the market in 2025, but business adoption is forecast to accelerate at a 38.70% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Canada Mobile Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Internet Penetration Boosting Mobile Commerce Adoption | +8.2% | National, with stronger gains in Ontario, Quebec, British Columbia | Medium term (2-4 years) |

| Rising Adoption of Interac Debit Rails for Contactless In-store Payments | +9.1% | National, concentrated in urban centers | Short term (≤ 2 years) |

| Expansion of Loyalty-Integrated Closed-Loop Mobile Wallets by Canadian Retailers | +6.7% | National, early adoption in Toronto, Vancouver, Montreal | Medium term (2-4 years) |

| Government Push for Real-Time Rail & Open Banking Framework | +11.3% | National implementation with phased rollout | Long term (≥ 4 years) |

| Growing Acceptance of Wearable Payments at Mass Transit Systems | +3.5% | Urban centers: Toronto, Vancouver, Montreal, Ottawa | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Increasing Internet Penetration Boosting Mobile Commerce Adoption across Canadian Provinces

Enhanced broadband availability is accelerating e-commerce activity, with mobile commerce transactions expanding 42% year over year in 2024. The CAD 6 billion (USD 4.37 billion) connectivity strategy aims to deliver 50 Mbps speeds nationwide by 2030, reducing rural-urban disparities and enlarging the total addressable base for payment providers. British Columbia’s regional plan alone delivered CAD 2.5 billion (USD 1.82 billion) in economic benefits by 2024, a result that demonstrates the economic multiplier of reliable connectivity. More than 73,000 rural households are set to benefit from 132 projects in flight, directly translating to incremental transaction volume for digital wallets. Mobile app payment usage rose from 37% of adults in 2022 to 45% in 2024, signaling sustained appetite for smartphone-based settlement mechanisms.

Rising Adoption of Interac Debit Rails for Contactless In-store Payments

Interac processes more than 16 million daily transactions, while sustaining fraud at below CAD 0.01 per CAD 100. Its tiered interchange policy, introduced in October 2024, reduced fees for small merchants, sparking greater acceptance of tap-to-pay debit.[2]Canadian Federation of Independent Business, “Lower Visa and Mastercard fees for small business start this week,” cfib-fcei.ca Interac e-Transfer penetration grew seven percentage points to 58% in 2024, and contactless debit accounted for 70% of all debit purchase volume. Integration with Apple Pay, Google Pay, and Samsung Pay widens consumer choice and strengthens Interac’s position against global card schemes. Independent merchants already report 27% savings on processing costs, enhancing cash-flow resilience for small businesses.[3]Apple, “Developers Can Soon Offer In-App NFC Transactions Using the Secure Element,” apple.com

Expansion of Loyalty-Integrated Closed-Loop Mobile Wallets by Canadian Retailers

Retailers capitalize on closed-loop architecture to aggregate consumer data, drive repeat visits, and deploy personalized promotions. Tim Hortons’ Scan & Pay model issues 10 points per dollar spent, blending payment and rewards in a single user journey. Loblaw Companies’ PC Optimum program boasts 17 million members and generated CAD 3.9 billion (USD 2.84 billion) in e-commerce revenue in 2024, underscoring the power of data-driven personalization. The success of these models is influencing quick-service restaurants, grocery chains, and drugstores to accelerate wallet development. Market projections show Canadian digital wallets scaling from USD 1.39 billion in 2024 to USD 20.48 billion by 2030, with loyalty embedded as a core differentiator.

Government Push for Real-Time Rail & Open Banking Framework Accelerating Mobile Payment Innovation

RTR will provide 24 × 7 real-time settlement by 2026 using ISO 20022 data standards, enabling richer messaging and advanced fraud controls. Parallel implementation of the Consumer-Driven Banking Framework in 2025 creates a secure API layer that lets consumers share financial data with accredited fintechs. Combined, these initiatives shrink settlement windows, reduce reconciliation costs, and trigger product innovation across B2C and B2B use cases. Payments Canada’s collaboration with IBM and CGI has already completed the exchange component, pointing to an on-schedule launch. Once live, RTR will align Canada with global leaders such as Brazil’s Pix, catalyzing a new generation of instant, data-rich payment experiences.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Provincial Privacy Regulations Restricting Data-Sharing Across Ecosystems | -4.8% | National, with varying intensity by province | Medium term (2-4 years) |

| Higher Merchant Discount Fees for Mobile Wallets vs. Interac Debit Discouraging SMB Adoption | -3.2% | National, particularly affecting small merchants | Short term (≤ 2 years) |

| Latency Issues in Rural Broadband Limiting Seamless Proximity Transactions | -2.1% | Rural and remote areas, Northern territories | Medium term (2-4 years) |

| Consumer Security Concerns over Tokenization Failures in NFC Devices | -1.9% | National, with higher impact among older demographics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Provincial Privacy Regulations Restricting Data-Sharing Across Ecosystems

Canada operates under a dual privacy regime: the federal PIPEDA statute and multiple provincial acts. Divergent compliance obligations inflate development expenses for wallet providers that must tailor data-handling protocols by jurisdiction. While Ottawa’s 2024 proposal to modernize PIPEDA aspires to harmonize standards with the EU’s GDPR, implementation timelines and final provisions remain uncertain. The fragmentation undermines network effects that rely on seamless data exchange, limiting the scale of loyalty programs and targeted offers. Open banking participants face additional hurdles because API frameworks must satisfy overlapping federal and provincial mandates before launch.

Higher Merchant Discount Fees for Mobile Wallets vs. Interac Debit Discouraging SMB Adoption

Mobile wallets often impose blended fees of 1–4% per sale, noticeably above the sub-1% effective rate of Interac debit, leading to merchant reluctance, especially in rural and low-margin sectors. Ottawa negotiated a reduction in average credit card fees to 1.4% in 2024, yet some processors did not pass the savings to merchants, dulling the policy’s intended effect. Fixed costs to enable contactless terminals and tokenization further weigh on small retailers with limited volume. The cost gap entrenches Interac’s advantage and slows the diffusion of international wallet brands beyond metropolitan cores.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Payment Type: Proximity Dominance Faces Remote Surge

Proximity transactions commanded 60.30% of the Canada mobile payments market in 2025, driven by near-field communication ubiquity at more than 500,000 merchant locations nationwide. Over 70% of debit purchases cleared via tap-to-pay as consumers embraced quick checkout. The segment benefits from habit formation during the pandemic and trusted domestic rails such as Interac Flash. Yet the remote cohort is expanding at a 38.05% CAGR to 2031 as e-commerce volumes, QR code scans, and biometrically authenticated in-app payments grow. Mobile wallet providers exploiting single-click checkout and tokenized credentials are eroding the historical gap between online and in-store experiences. Payment orchestration platforms now enable merchants to route transactions dynamically, optimizing authorization rates and reducing fraud. Apple’s decision to open Secure Element access to developers further blurs proximity and remote boundaries by allowing in-app NFC experiences outside the browser.

Remote payments also gain from the softPOS revolution, which converts Android or iOS devices into full-service terminals at minimal cost, expanding acceptance among micro-merchants at pop-up markets and service professionals on the move. As RTR delivers instant funds availability, settlement anxiety for remote sellers diminishes, widening adoption. The Canada mobile payments market size for remote channels is expected to surpass USD 6.48 billion by 2031, roughly 41.10% of overall flows, signaling a more balanced channel mix. Canada mobile payments industry observers note that fraud mitigation through dynamic CVV and biometric pairing is shortening the trust gap between proximity and remote payment types.

By Transaction Type: POS Leadership Challenged by Transit Innovation

Point-of-sale interactions accounted for 53.40% of the Canada mobile payments market size in 2025, supported by mature acceptance infrastructure, predictable purchase patterns, and solid consumer trust. Merchants continue to upgrade POS firmware to accept wallet tokenization, dynamic QR, and in-app loyalty redemption. Interac Flash and dual-tap flows accelerate throughput for high-volume sectors such as grocery, convenience, and quick-service restaurants. However, transit and ticketing transactions, bundled under “other” today, are scaling at a 39.95% CAGR. Urban operators in Toronto, Vancouver, Montréal, and Ottawa have embraced open-loop acceptance, allowing riders to tap wearables or phones directly at fare gates without PIN verification.

The appeal of touch-less entry and time savings is catalyzing ridership recovery post-pandemic. Transit agencies are also capturing richer ridership analytics that feed capacity planning and dynamic pricing. Beyond subways and buses, smart-ticketing solutions are penetrating sports arenas, museums, and parking garages, transforming event ticketing into an all-in-one experience. Payments for micro-mobility choices such as bike and scooter rentals are also processed through embedded wallet rails, adding incremental value. These developments imply that POS growth will moderate while transit, mobility-as-a-service, and venue ticketing carve out a larger share of transaction mix inside the Canada mobile payments market.

By Application: Retail Supremacy Meets Transportation Disruption

Retail and ecommerce held 36.50% of Canada mobile payments market share in 2025. Supermarket chains, pharmacy outlets, and quick-service food brands continue to layer loyalty, personalized offers, and buy-online-pick-up-in-store (BOPIS) flows into wallet experiences. Tim Hortons’ loyalty-linked Scan & Pay and Loblaw’s PC Optimum are notable exemplars of successful customer engagement strategies anchored in mobile payment enrollment. Retailers rely on consumer data reservoirs to refine assortment, optimize promotions, and reduce queue times. The Canada mobile payments market size for retail is projected to reach USD 5.66 billion in 2031, supported by omnichannel commerce and expanded same-day delivery options.

Transportation and logistics is the fastest-growing vertical, advancing at a 40.40% CAGR. Fleets utilize mobile wallets to automate driver fuel payments and tolls, while parcel carriers disburse instant payroll via RTR, improving workforce liquidity. Ports and rail operators experiment with IoT-linked smart contracts that trigger payment upon verified delivery events. Wearable fare collection in mass transit is driving incremental wallet activation among commuters, compounding network effects. As RTR provides immediate settlement, logistics firms reduce working-capital buffers and accelerate asset rotation, improving sector economics.

By End-user: Personal Adoption Leads Business Acceleration

Personal users represented 56.40% of market volume in 2025, underpinned by smartphone penetration of 84% among Canadians aged 15+. Generation Z is the vanguard, with 69% using wallets weekly. Consumer security perception has improved with tokenization and biometric two-factor authentication, yet Bank of Canada data indicates mobile payment usage remains only 16% among adults, signaling vast headroom. Loyalty benefits, account aggregation, and instant P2P transfers are expanding the value proposition for late adopters.

Businesses are increasingly migrating to mobile point-of-sale solutions for inventory management, staff scheduling, and analytics, driving a 38.70% CAGR in enterprise transaction value. Real-Time Rail promises real-time payroll, supplier settlement, and treasury optimization, features that resonate with corporate finance chiefs. Mid-market firms are deploying API-driven mobile disbursements to contractors and gig workers. The Canada mobile payments industry is also witnessing banks embed card-based spend controls and receipt capture into mobile corporate cards, simplifying audit trails.

Geography Analysis

Ontario and Quebec dominate adoption due to dense urban populations, head offices of major banks, and early deployment of advanced transit wallets. Toronto’s integration of Presto cards inside Apple Wallet illustrates how provincial agencies cooperate with global platforms to streamline fare collection, boosting daily transaction counts. Quebec’s distinct linguistic context necessitates French-language wallet interfaces, offering differentiation opportunities for localized providers. Ontario accounts for roughly 38.60% of the Canada mobile payments market, partly because technology clusters in the Greater Toronto Area accelerate fintech experimentation.

British Columbia and Alberta exhibit robust growth as technology workforces and foreign investment rise. British Columbia’s CAD 584 million rural connectivity plan improved internet service to 73,000 households, adding USD 467 million in economic impact and lifting transaction demand in previously underserved communities. Calgary and Edmonton benefit from energy-sector digitalization projects that route fuel and expense payments through mobile‐first platforms, cutting back-office paperwork. Government commitments to universal 5G coverage are expected to ease latency issues that hamper wallet performance in resource extraction zones.

Atlantic provinces and northern territories lag on penetration but represent a material upside as low-Earth-orbit satellite coverage and government subsidies extend broadband reach. CRTC’s mandate for 100% mobile coverage by 2026 will reduce the disconnect between urban and rural consumer experiences. Once connectivity is stable, service providers can leverage geotargeted marketing to onboard remote populations. Northern mining sites already deploy mobile wallets for safety wearables and shift payments, establishing proof points for broader retail usage. Taken together, regional disparities are narrowing, and policy initiatives suggest a more nationally uniform growth curve for the Canada mobile payments market.

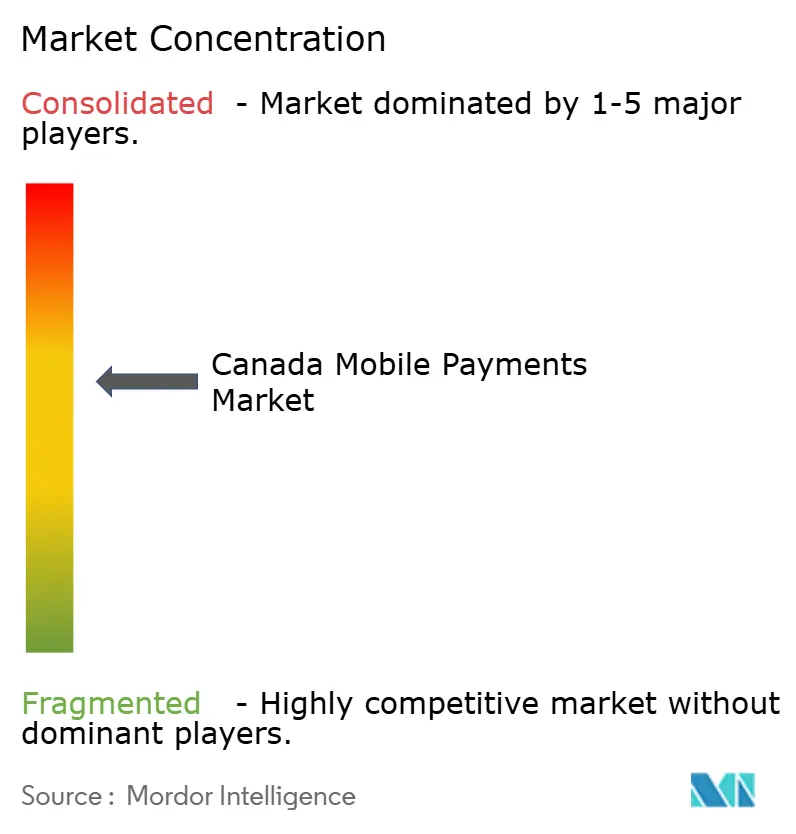

Competitive Landscape

Competition is moderate and characterized by a mix of domestic incumbents, global technology platforms, and agile fintech entrants. Interac’s domestic network processed 16 million daily debit and P2P transactions in 2024 with nominal fraud, reinforcing its incumbency advantage. Major banks pursue digital leadership through acquisitions and in-house innovation; RBC’s integration of HSBC Canada expands scale and cross-border reach, while TD’s fourth consecutive “Best Consumer Digital Bank” award underscores user-experience investment. These institutions leverage trusted brands and deposit bases to bundle value-added wallet functions such as instant credit top-ups and dynamic spend insights.

Technology majors aim to reshape customer interfaces. Apple’s enablement of in-app NFC using the Secure Element opens merchant creativity well beyond card tokenization, positioning the firm to monetize transaction routing and ecosystem royalties. Google and Samsung compete via open-source partnerships and deeper Android OS hooks. PayPal and Wise expand cross-border capabilities, catering to expatriate and SMB remittance needs. Lightspeed Commerce and Moneris differentiate by combining payments with inventory and loyalty modules for small merchants.

Market entrants focus on vertical niches and under-served geographies. Wage-advance provider DailyPay entered Canada in April 2025, leveraging RTR’s upcoming instant rails to deliver earned-wage access. Processing specialists experiment with cannabis retail and tele-health subverticals where compliance complexity offers defensible moats. The impending open-banking regime will lower switching costs, enabling fintech players to intermediate data-driven value propositions such as micro-saving, pay-by-bank, and BNPL alternatives that bypass card schemes. Strategic alliances with telecom operators and government agencies will be critical to unlocking rural customer acquisition as connectivity gaps close.

Canada Mobile Payments Industry Leaders

Canadian Imperial Bank of Commerce

Apple Inc.

PayPal Holdings Inc.

Google LLC

Samsung Electronics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DailyPay expanded into Canada, using its earned-wage-access model to tap employer demand for real-time payroll solutions. The move positions DailyPay to capitalize on RTR-enabled instant settlement.

- February 2025: Royal Bank of Canada completed strategic planning for its HSBC Canada acquisition, aiming to harmonize core banking and mobile platforms. The strategy consolidates customer data sets and enhances cross-sell potential across newcomers and commercial clients.

- December 2024: TD Bank Group retained its “Best Consumer Digital Bank in North America” title for the fourth year, reflecting continued investment in mobile security, API openness, and personalized insights. The accolade supports brand equity and customer acquisition.

- November 2024: Payments Canada confirmed renewed momentum on the Real-Time Rail project with IBM and CGI, targeting 24 × 7 availability by 2026. Successful delivery will expand competitive field access to instant payment rails.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our analysis defines the Canada mobile payments market as the total dollar value of transactions initiated on a smartphone or tablet that reach merchants or peers through card tokenization, Interac debit rails, or direct bank links, whether they occur in-store or remotely.

Scope exclusion: handset hardware sales and card-not-present web checkouts that start on a desktop are outside this study.

Segmentation Overview

- By Payment Type

- Proximity Payments

- Remote Payments

- By Transaction Type

- Peer-to-Peer (P2P)

- In-store Point-of-Sale (POS)

- Person-to-Merchant (P2M/Checkout)

- Other Transaction Types

- By Application

- Retail and eCommerce

- Transportation and Logistics

- Hospitality and Food-Service

- Government and Public Sector

- Other Applications (Education, Healthcare)

- By End-user

- Personal

- Business

Detailed Research Methodology and Data Validation

Primary Research

We spoke with issuing-bank product heads, tier-one grocers, transit agencies, and fintech associations across Ontario, Québec, British Columbia, and Alberta. Their insights helped us confirm uptake assumptions, fee structures, and the rollout timing of new payment schemes.

Desk Research

We gathered headline volumes, ticket sizes, and adoption ratios from Payments Canada, Statistics Canada, the Bank of Canada, the Canadian Bankers Association, and open customs data. Company filings and reputable news feeds accessed via Dow Jones Factiva enriched merchant acceptance insights, while D&B Hoovers supplied revenue splits for wallet providers. This list is illustrative. Many additional public sources informed data collection and clarification.

Market-Sizing & Forecasting

A top-down build began with national retail and peer-to-peer payment totals, which are then filtered through mobile initiation shares taken from surveys and issuer data. Selective bottom-up checks, sampled wallet active users multiplied by annual spend, validate and adjust totals. Key variables include smartphone penetration, NFC terminal density, Interac e-Transfer volumes, merchant discount fees, Real-Time Rail launch timing, and median ticket drift. Multivariate regression ties these drivers to historic values, and scenario analysis accommodates delayed RTR launch or fee reforms.

Data Validation & Update Cycle

Our analysts cross-check outputs against quarterly issuer disclosures and Payments Canada flash statistics, reconcile anomalies, and escalate gaps for peer review. Reports refresh each year, with interim updates triggered by material events.

Why Our Canada Mobile Payments Numbers Inspire Confidence

Published estimates often differ because firms vary scope, data vintage, and inflation methods.

We preview the key gap drivers below.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.39 B (2025) | Mordor Intelligence | NA |

| USD 2.89 B (2023) | Global Consultancy A | Rolls forward a pre-COVID base year and ignores RTR impact |

| USD 0.23 B (2024) | Regional Consultancy B | Counts only remote in-app transactions, omitting in-store proximity spend |

| USD 3.32 B (2024) | Trade Journal C | Blends digital wallets with prepaid card loads, inflating totals |

This comparison shows that Mordor's disciplined scope choices and annually refreshed driver set yield a balanced, transparent figure decision-makers can trust.

Key Questions Answered in the Report

What is the size of the Canada mobile payments market in 2026?

The market is valued at USD 3.27 billion in 2026 and is projected to expand at a 36.95% CAGR to USD 15.77 billion by 2031.

Which segment holds the largest share of the Canada mobile payments market?

Proximity transactions lead with a 60.30% share, reflecting strong consumer preference for tap-to-pay at retail locations.

How will Real-Time Rail affect businesses?

RTR will enable real-time payroll, supplier settlement, and improved cash-flow visibility, reducing the working-capital cycle for enterprises.

Why do small merchants hesitate to accept mobile wallets?

Higher merchant discount fees of 1–4% per transaction compared with lower Interac debit costs discourage adoption among cost-sensitive retailers.

Which regions are experiencing the fastest growth?

Western provinces such as British Columbia and Alberta are registering rapid uptake thanks to technology sector expansion and targeted connectivity investments.

What role do loyalty programs play in the market?

Loyalty-integrated wallets from retailers like Tim Hortons and Loblaw drive repeat purchases and deepen consumer engagement, materially influencing transaction volumes.

Page last updated on: