Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 141.5 Billion |

| Market Size (2031) | USD 184.94 Billion |

| Growth Rate (2026 - 2031) | 5.50% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

C4ISR Market Analysis by Mordor Intelligence

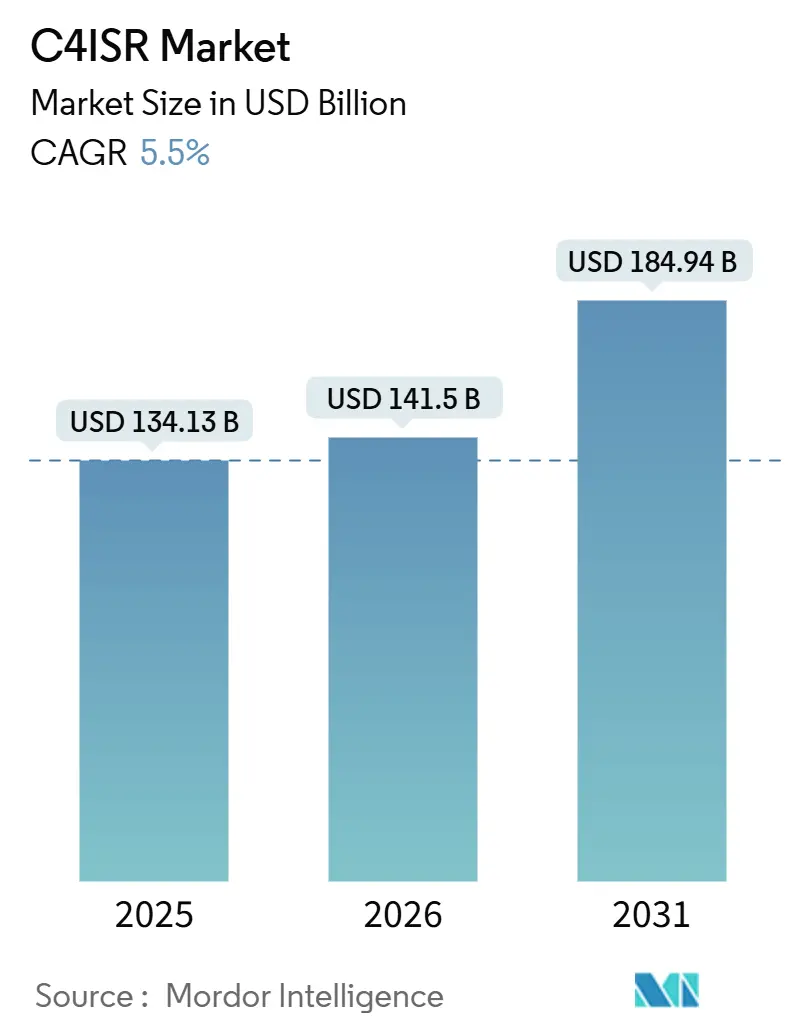

The C4ISR market size is expected to grow from USD 134.13 billion in 2025 to USD 141.50 billion in 2026 and is forecast to reach USD 184.94 billion by 2031 at a 5.50% CAGR over 2026-2031. The C4ISR market is moving toward networked command systems, resilient communications, and shared operating pictures rather than isolated platform upgrades. Allied defense investment remained a major driver of demand in 2026, with the US DoD stating that NATO allies pledged more than USD 120 billion in additional spending beyond 2025 levels. Open architecture rules are also changing procurement, because acquisition teams now expect software upgrades and cyber compliance to continue after fielding rather than end at delivery. The spread of autonomous systems and edge processing is raising demand for data fusion, secure links, and faster decision support across the C4ISR market. At the same time, coalition interoperability gaps, cyber accreditation demands, and export compliance issues continue to shape vendor selection and program timing across the C4ISR market.

Key Report Takeaways

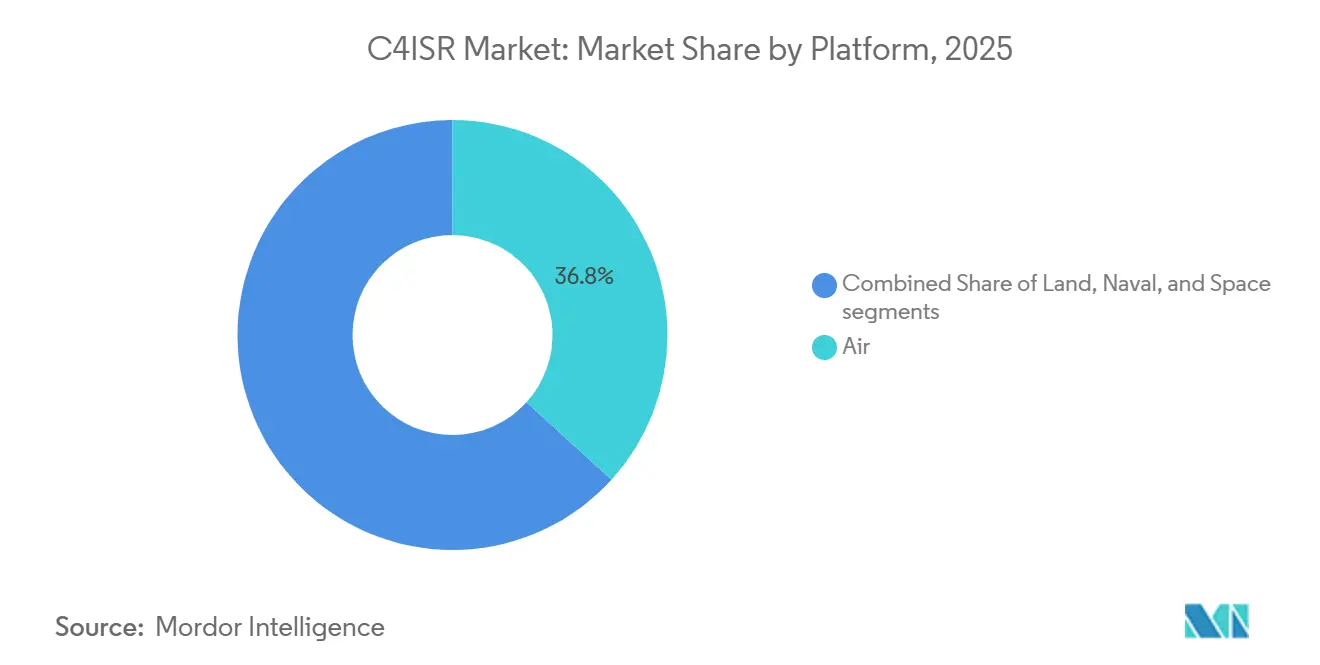

- By platform, air held 36.75% of the C4ISR market share in 2025, while naval is projected to grow at an 8.25% CAGR through 2031.

- By purpose, ISR accounted for 44.38% of the C4ISR market size in 2025, while C4 is forecast to grow at a 6.29% CAGR through 2031.

- By component, hardware led with 55.97% share in 2025, while software is forecast to grow at a 7.49% CAGR through 2031.

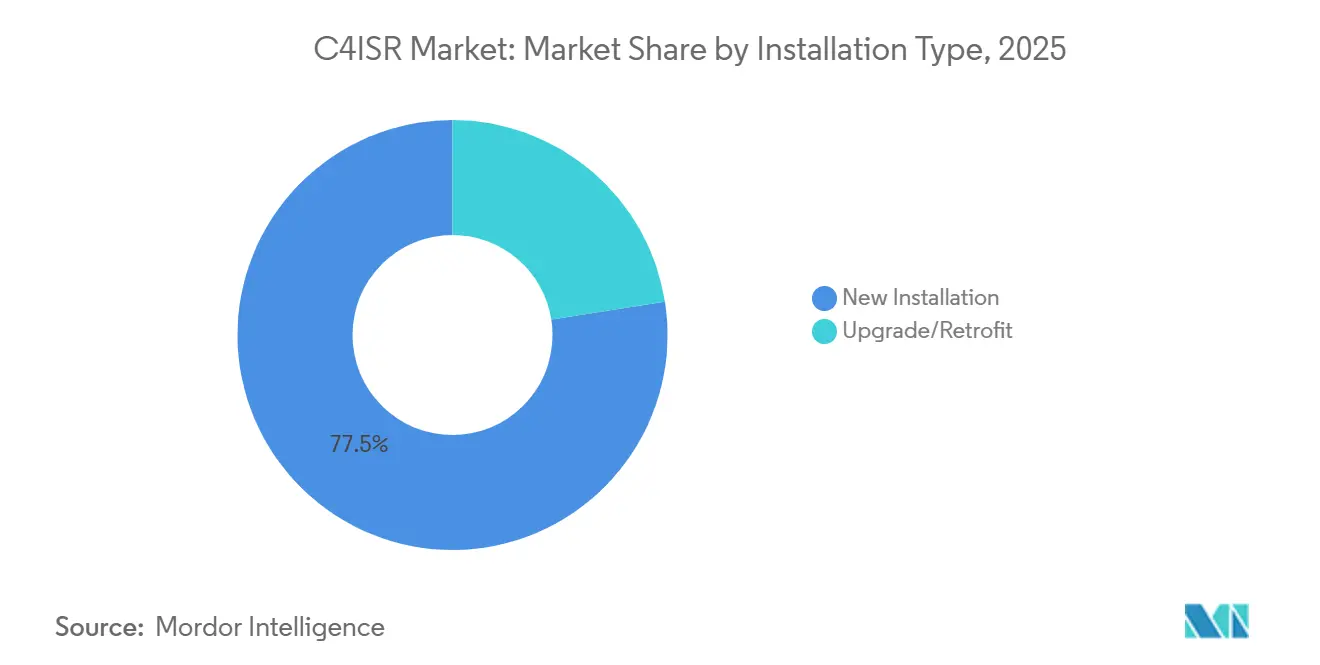

- By installation type, new installations captured 77.48% share in 2025, while upgrades and retrofits are projected to grow at a 7.18% CAGR through 2031.

- By end user, defense and military accounted for 66.28% of the market in 2025, while government and law enforcement are projected to grow at a 9.42% CAGR through 2031.

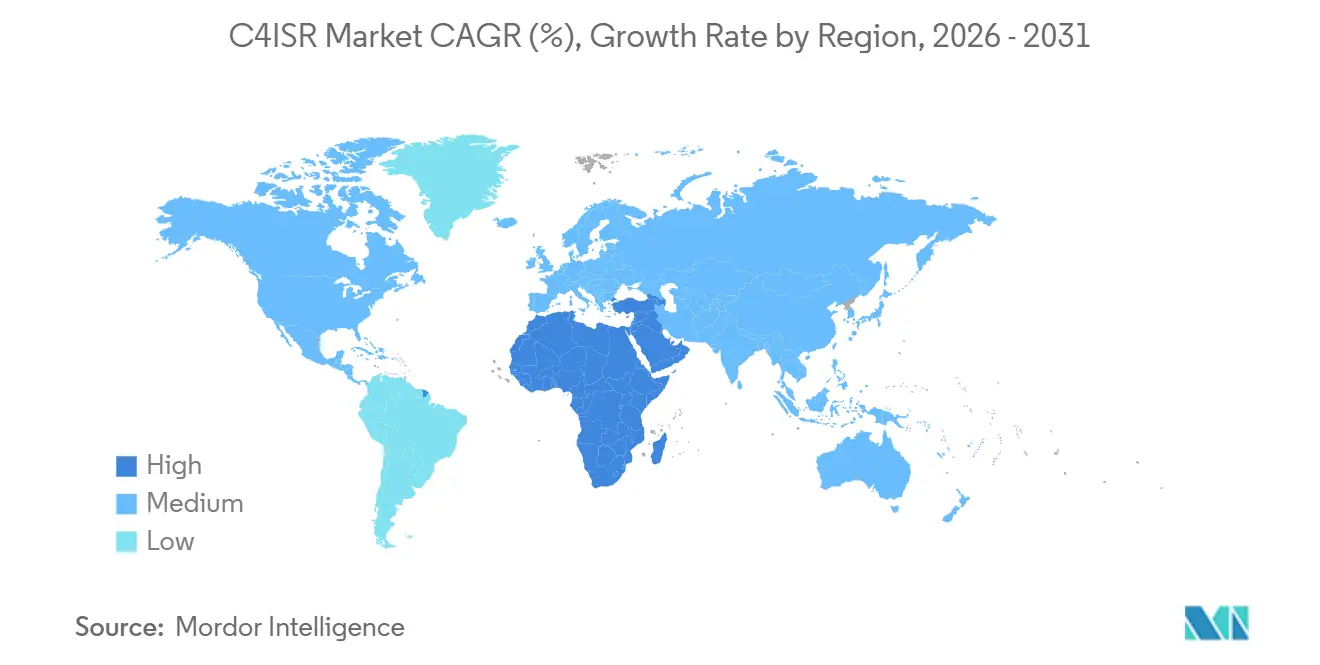

- By geography, North America held 34.18% share in 2025, while the Middle East and Africa are forecast to grow at an 8.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global C4ISR Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| NATO rearmament and modernization raise digital command, ISR, and secure comms demand | +1.50% | Europe, North America, spillover to Asia-Pacific and Middle East and Africa | Short term (≤ 2 years) |

| Multi-domain C2 programs (JADC2/CJADC2, ABMS) accelerate interoperable C4ISR deployments | +1.20% | North America, Five Eyes allies, NATO partners | Medium term (2-4 years) |

| Proliferation of unmanned and autonomous platforms increases sensor and data-link density | +1.20% | Asia-Pacific, North America, spillover to Europe and Middle East and Africa | Medium term (2-4 years) |

| Edge AI/ML and cloud-to-tactical fusion compress kill chain and drive upgrade cycles | +1.00% | North America, Europe, South Korea, Australia | Medium term (2-4 years) |

| Space-based ISR and SATCOM architectures shift to LEO/MEO with resilient mesh networking | +0.90% | Global, with concentration in North America, Europe, and Northeast Asia | Long term (≥ 4 years) |

| Open architectures (MOSA/CMOSS/SOSA) enable rapid tech insertion and shift spend to software/services | +0.70% | Global, led by the US and allied procurement programs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

NATO Rearmament Creates a Structural, Multi-Year Procurement Cycle

The C4ISR market received a stronger, longer-term procurement signal after NATO members moved toward higher spending targets and broader security infrastructure commitments. European allies increasingly shifted spending toward secure communications, ISR fusion, and interoperable command layers rather than relying only on major platform buys. This matters because digital command backbones usually require follow-on software updates, integration work, and cyber certification after the initial order is placed. In July 2026, the US DoD stated that allies committed more than USD 120 billion in additional spending beyond 2025 levels, with USD 4 billion directed to space and surveillance projects. That funding pattern supports a multi-year demand base for resilient data links, command software, ISR nodes, and mission networking in the C4ISR market. It also favors vendors that can support coalition standards, certification, sustainment, and upgrades across multiple national programs simultaneously.

CJADC2 and ABMS Drive a Software-Defined C2 Architecture Transition

The C4ISR market is increasingly shaped by the move from isolated service systems to joint command architectures built around shared data and software integration. The DoD's FY2027 budget request exceeded USD 2 billion for CJADC2 consolidation, indicating that joint command modernization has entered a larger spending phase. As this shift continues, the value chain becomes less centered on platform ownership and more centered on the software layer that connects sensors, operators, and weapons. L3Harris stated in May 2026 that the US Air Force selected the company to develop digital infrastructure for the ABMS network, which shows that fielded procurement is now following the architecture transition. The same transition also appeared in June 2026, when L3Harris received USD 84 million in US Army orders for NGC2 manpack systems tied to the next-generation command-and-control transport layer. The result is a C4ISR market where recurring software delivery, open integration, and secure transport are gaining strategic weight relative to single-platform hardware wins.

Unmanned Platform Proliferation Is Multiplying the Data Problem, Not Just the Sensor Count

The C4ISR market is also expanding because each new unmanned platform adds communications traffic, sensor feeds, and command links that must be fused into a common operating picture. The DoD’s FY2026 budget allocated USD 54.60 billion to autonomous warfare programs, including USD 16.90 billion for the procurement of uncrewed systems across domains. That rise means the workload has shifted from collecting more data to processing, distributing, and acting on already dense streams of mission information. It also explains why software, edge computing, and protected data links are rising faster in strategic importance than standalone sensor hardware in the C4ISR market. This pattern strengthens demand for mission systems that can support large autonomous fleets without overloading human operators or congesting tactical networks. Vendors that can simplify fusion, automate prioritization, and maintain secure throughput are therefore positioned well as the C4ISR market absorbs more autonomous platforms.

Edge AI and Tactical Fusion Are Collapsing Sensor-to-Shooter Timelines

The C4ISR market is gaining another push from edge processing and tactical AI tools that reduce the time between detection, assessment, and response. The DoD allocated USD 25.2 billion in FY2025 to programs incorporating AI and autonomous systems, indicating that tactical processing has become an embedded budget priority. In field terms, that shift supports rugged systems that can fuse sensor inputs at the edge, even when connectivity is degraded or intermittent. Leonardo DRS introduced THOR in March 2026 as an open-architecture embedded computing chassis for tactical AI processing and multi-sensor fusion on combat platforms. An open-architecture policy is reinforcing this movement because acquisition teams now want compute layers that can accept updated software stacks without a full hardware redesign.[1]United States Department of Defense, “Tri-Service Memorandum,” U.S. Department of Defense, cto.mil This keeps the C4ISR market on a path where battlefield nodes behave less like fixed boxes and more like continuously updatable digital systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Integration complexity and data interoperability across legacy/coalition systems | -0.50% | Global, with higher pressure in NATO multinational programs and Asia-Pacific coalitions | Medium term (2-4 years) |

| Cyber/EW resilience requirements increase cost, schedule, and accreditation burden | -0.40% | North America, Europe, Five Eyes countries | Long term (≥ 4 years) |

| Export controls/ITAR and security of supply limit cross-border C4ISR sharing | -0.30% | North America, Europe, and US ally markets | Medium term (2-4 years) |

| Spectrum congestion and EMSO deconfliction constrain networked operations | -0.30% | Asia-Pacific, Europe, and Middle East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Integration Complexity and Data Interoperability Across Legacy and Coalition Systems

The C4ISR market still faces a serious execution constraint because many programs must connect new tools to legacy fleets, service-specific architectures, and coalition networks. The GAO reported in 2025 that the DoD lacked a comprehensive framework to evaluate whether service investments collectively achieved CJADC2 goals, which points to fragmented modernization across the force. When systems move from a national program to coalition use, they often require revalidation of classification rules, encryption standards, and waveform compatibility. That burden slows fielding, delays revenue recognition, and raises integration risk for both primes and subcontractors in the C4ISR market. The challenge becomes sharper as joint exercises expand and more allied forces try to exchange data in real time across mixed command stacks. This makes interoperability readiness and certification discipline as important as pure technical performance in large C4ISR market competitions.

Cyber and EW Resilience Requirements Inflate Cost and Extend Accreditation Timelines

The C4ISR market also faces a growing compliance burden as more open software, AI workloads, and connected nodes create a broader attack surface. Vendors now need to invest earlier in zero-trust design, encrypted flows, anti-tamper controls, and resilience against both cyber intrusion and electronic attack. That work extends development schedules and favors larger contractors that already maintain accreditation teams and secure engineering pipelines. Allied and foreign military sales (FMS) programs often face duplicated compliance requirements, as exporters and recipients must satisfy separate security regimes. In the government end-user space, the Government Surveillance Reform Act of 2026 would add another layer of compliance by requiring agencies to protect domestic communications data while preserving operational capabilities. In the government end-user space, the Government Surveillance Reform Act of 2026 adds another layer of compliance by requiring agencies to protect domestic communications data while preserving operational capabilities. The effect is a C4ISR market where security assurance, certification capacity, and sustainment discipline can determine contract outcomes as much as the hardware or software itself.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Platform: Air Retains the Largest Base, While Naval Demand Scales Faster

Air platforms held 36.75% of the C4ISR market share in 2025, which kept airborne systems at the center of real-time multi-domain operations. This position reflects steady demand for airborne ISR suites, battle management tools, mission computers, and high-capacity tactical data links across major air fleets. The C4ISR market continues to favor airborne architectures because they connect sensing, relay, and command functions across large operational areas in a single mission chain. Collaborative combat programs also reinforce this pattern because distributed air sensing requires more data sharing and command coordination than older centralized payload models. In 2025, HENSOLDT received a contract extension from Airbus Defence and Space to continue developing the Eurofighter ECRS Mk1 radar for Germany and Spain, underscoring the ongoing depth of investment in airborne sensing.

Land remained an important base segment because ground-mobile command systems, soldier networking, and vehicle-integrated electronic support still account for a wide installed base in the C4ISR industry. Space is also becoming a larger growth vector because proliferated constellations extend ISR persistence and communications resilience across contested environments. Naval platforms, however, are projected to grow at an 8.25% CAGR, the highest rate in this platform split and a clear sign of shifting maritime priorities in the C4ISR market. The report ties that shift to distributed maritime operations, contested undersea conditions, and the need to preserve command continuity at low electromagnetic signature levels. L3Harris strengthened that direction in February 2026 when it secured full-rate production for 26 submarine communication shipsets for Virginia- and Columbia-class submarines through 2033.

By Purpose: ISR Dominates, but C4 Software Is the Fastest-Growing Revenue Driver

ISR accounted for 44.38% of the C4ISR market size in 2025, which kept surveillance, sensing, and target awareness as the largest purpose block. That share reflects a long investment cycle in persistent surveillance, signal collection, multi-spectral sensing, and mission exploitation tools. The addition of unmanned fleets, edge AI, and proliferated space layers does not diminish the importance of ISR, as these systems typically increase the volume of data that must be collected and fused. As a result, ISR continues to hold the broadest installed role across air, land, naval, and space missions in the C4ISR market. The scale of ISR spending also supports recurring demand for processing, storage, and dissemination tools after sensors have already been fielded.

C4 is projected to expand at a 6.29% CAGR through 2031, which makes it the fastest-growing purpose area in the current report structure. Growth is being driven by software-defined command architectures that replace rigid service-specific nodes with shared data layers and orchestration tools. L3Harris's May 2026 ABMS digital infrastructure award showed that the command layer is moving from concept work to funded implementation across the force.[2]L3Harris Technologies, “L3Harris Secures Full-Rate Production Contract for US Navy Submarine Communication Systems,” L3Harris Technologies, l3harris.com Electronic warfare remains a smaller-purpose block, but the report notes growing momentum as cyber and spectrum management increasingly connect to the same decision networks that support command and communications. Elbit Systems' May 2026 military modernization contract, which included C4ISR command applications, EW systems, unmanned platforms, and AI-enabled solutions, illustrates how these purpose layers are converging in live procurement programs.

By Component: Hardware Leads, Software Scales Faster On Open, Reusable Stacks

Hardware led with a 55.97% share in 2025, indicating that radios, terminals, compute modules, and sensor arrays still form the physical basis of the C4ISR market. These products remain essential because no software layer can operate without resilient transport, onboard compute, and mission-specific hardware interfaces. Even so, the report makes it clear that the economics shift once a platform achieves open-architecture compliance and can support repeated software refreshes. In that model, the hardware container stays in service longer while functionality is added through updates, cyber hardening, and application-level changes. This extends the revenue life of deployed systems and changes supplier competition from one-time integration toward ongoing digital delivery.

Software is projected to grow at a 7.49% CAGR, which makes it the strongest component growth path in the C4ISR market. The December 2024 tri-service memo and the MOSA implementation guidebook support that shift by pushing acquisition teams toward open, replaceable, and standards-based system design. In February 2026, Pacific Defense delivered the first seven CMOSS Mounted Form Factor systems, providing a production-stage example of the modular approach. Services form the third pillar, and their importance increases as programs require integration, training, sustainment, and continued accreditation support after delivery. This makes the C4ISR market increasingly attractive to firms that can maintain secure software pipelines and long-cycle support contracts rather than only ship hardware.

By Installation Type: New Platforms Dominate Spending, While Upgrades Outpace Growth

New installations accounted for 77.48% of the C4ISR market share in 2025, reflecting the scale of greenfield procurement tied to new platforms and fresh architecture programs. These programs include next-generation aircraft, submarines, space layers, and other systems that are designed from the start around more connected command and sensing requirements. New platforms are attractive because they allow cleaner integration, broader digital design choices, and fewer legacy constraints during early deployment. They also give primes more control over the full architecture stack, which can support larger contract scopes at the initial fielding stage. This keeps new installations as the largest revenue pool, even as other spending patterns begin to change.

Upgrade and retrofit is projected to grow at a 7.18% CAGR, indicating that many buyers prefer capability insertion over wholesale platform replacement in the C4ISR market. That pattern reflects a practical budget reality because many fleets remain in service for years or decades and cannot be replaced within a single planning cycle. The US Army stated in 2024 that the CMOSS Mounted Form Factor award initiated rapid prototype development for a modular open architecture designed to converge separate legacy electronics into a single chassis. The report treats this retrofit path as a durable opportunity because it depends less on launching entirely new programs and more on upgrading existing access points. It also opens room for specialized vendors that can fit modern mission functions into constrained platform envelopes without full vehicle or aircraft redesign.

By End User: Defense and Military Lead Share and Growth

The defense and military sectors accounted for 66.28% of the C4ISR market in 2025, keeping armed forces as the clear anchor customer base for the sector. Major spending lines such as joint command modernization, airborne sensing, space ISR, and unmanned platform networking continue to originate from this end-user block. The defense share remains high because military buyers control the largest long-cycle budgets, the strictest security requirements, and the broadest mission integration needs. These factors sustain demand across hardware, software, and services rather than concentrating value in only one component layer. The C4ISR market, therefore, still depends most heavily on defense procurement calendars, shifts in doctrine, and coalition modernization priorities.

Government and law enforcement are projected to grow at a 9.42% CAGR, making them the fastest-growing end-user category in the report. The US Coast Guard's published C4ISR program activity and its December 2025 contract for a next-generation Biometrics at Sea System show how civilian security agencies are adopting defense-grade command-and-control and surveillance tools. The Government Surveillance Reform Act of 2026 introduces a policy constraint, as public-sector buyers may need systems that preserve compliance with civil liberties while maintaining operational value. This gives the C4ISR market a second demand lane where privacy-aware design and public-sector compliance can matter alongside defense pedigree.

Geography Analysis

North America accounted for 34.18% of the C4ISR market share in 2025, maintaining its position as the largest regional revenue base. That lead rests on the scale of US command modernization, airborne networking, space sensing, and secure communications programs. The USD 120 billion commitment in additional investment beyond 2025 levels will support North American suppliers through FMS and co-production pathways.[3]White House, “Fact Sheet, President Donald J. Trump Secures Historic Defense Investment From NATO Allies,” The White House, whitehouse.gov North America also benefits from the pace of open-architecture adoption, as the US acquisition policy is actively pushing modular, replaceable system design across the force. This supports recurring work in software integration, certification, transport, and mission data services across the C4ISR market.

Europe is growing on a stronger defense modernization base than it has seen in years, and the regional pattern increasingly favors sovereign communications, ISR, and command capability. Allied rearmament, coalition readiness needs, and a stronger push for local program control are supporting the C4ISR market in Europe. Airbus, Leonardo, and Thales signed an MoU in October 2025 to combine their space activities into a new European company, which indicates that regional primes want greater scale in sovereign security programs. HENSOLDT's 2025 Eurofighter radar extension also showed that Europe is still investing in mission electronics and sensing depth across key defense fleets.

Asia-Pacific remains an important region for C4ISR volume and technology because ISR integration, command modernization, and local defense electronics programs continue to expand. The report links regional demand to India, South Korea, Japan, and Australia, where surveillance coverage, decision speed, and force networking remain central priorities. The Middle East and Africa are projected to grow at an 8.28% CAGR through 2031, making it the fastest-growing region for the C4ISR market. SIPRI stated that military expenditure in the Middle East reached USD 218 billion in 2025, even though overall regional growth remained modest. This means the regional premium in the C4ISR market is driven by selective modernization programs and ISR capability development rather than by broad spending growth across all countries.

Competitive Landscape

The C4ISR market is moderately concentrated, with a group of large systems integrators holding a strong position across command systems, sensors, communications, and mission integration. Lockheed Martin Corporation, Northrop Grumman Corporation, RTX Corporation, L3Harris Technologies, Inc., and Thales Group form the main prime tier in the report's competitive structure. Below them, a wide supplier base competes in software, components, subsystems, upgrade kits, and support work, which keeps bidding pressure active across many contract layers. A consistent advantage in this C4ISR market comes from early compliance with MOSA, CMOSS, SOSA, and cyber accreditation rules, because certified vendors can enter prime positions sooner. That pattern shifts competition away from standalone technical claims and toward delivery discipline, standards alignment, and secure update capacity.

L3Harris offers a clear example of this approach, as the company added an ABMS digital infrastructure role in May 2026 and expanded its NGC2 radio, submarine communications, and space-tracking positions. Elbit Systems provided another example in May 2026 when it secured a USD 1.4 billion military modernization contract covering C4ISR command applications, EW, unmanned systems, and AI-enabled solutions. Airbus, Leonardo, and Thales also signaled a scale strategy through their October 2025 space cooperation MoU, which points to stronger European ambition in the supply of sovereign C4ISR systems. These moves show that the C4ISR market rewards breadth across sensing, computing, communications, and integration rather than strength in only one equipment line.

The report also makes clear that white-space opportunities still exist where commercial AI capabilities must be validated, secured, and updated on defense-grade architectures. Another important competitive point is that company benchmarking should focus on commercial suppliers rather than state research bodies. DRDO develops systems for India but does not compete commercially in the same way as prime contractors, so its inclusion would distort the comparative view of the C4ISR market. Hanwha Systems is a more appropriate benchmark because it operates as a defense electronics supplier with a strong presence in C4ISR systems, radar, and battle management.

C4ISR Industry Leaders

Northrop Grumman Corporation

RTX Corporation

L3Harris Technologies, Inc.

Lockheed Martin Corporation

Thales Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Epirus, Inc. and Digital Force Technologies (DFT) announced a partnership to deliver a fully integrated C-UAS kill chain. This collaboration combines the companies' technologies to detect, track, identify, localize, and provide non-kinetic, low-collateral solutions to counter unmanned aerial systems (UAS) threats.

- February 2026: Pacific Defense announced the successful delivery of the first seven Mounted Common Infrastructure (MCI) systems under the US Army's CMOSS Mounted Form Factor (CMFF) MCI program. The contract, awarded in September 2025, saw the initial tranche of systems delivered within three months of the program's commencement, highlighting rapid execution in alignment with the Army's accelerated modernization goals.

- October 2025: Lockheed Martin Corporation received a USD 233 million firm-fixed-price contract to supply IRST21® Block II systems and initial spare parts to the US Navy and Air National Guard (ANG).

Global C4ISR Market Report Scope

C4ISR, an acronym for Command, Control, Communications, Computers, Intelligence, Surveillance, and Reconnaissance, serves as an integrated systems framework. Military and defense forces utilize it to gather information, analyze data, and coordinate actions across all domains: land, sea, air, space, and cyber.

The C4ISR market is segmented into platform, purpose, component, installation type, end user, and geography. By platform, the market is segmented into air, land, naval, and space. By purpose, the market is segmented into command, control, communications, and computer (C4), intelligence, surveillance, and reconnaissance (ISR), and electronic warfare (EW). By component, the market is segmented into hardware, software, and services. By installation type, the market is segmented into new installation and upgrade/retrofit. By end user, the market is segmented into defense and military, and government and law enforcement. The report also covers the market sizes and forecasts for the C4ISR market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

By Platform

| Air |

| Land |

| Naval |

| Space |

By Purpose

| Command, Control, Communications, and Computer (C4) |

| Intelligence, Surveillance, and Reconnaissance (ISR) |

| Electronic Warfare (EW) |

By Component

| Hardware |

| Software |

| Services |

By Installation Type

| New Installation |

| Upgrade/Retrofit |

By End User

| Defense and Military |

| Government and Law Enforcement |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Platform | Air | ||

| Land | |||

| Naval | |||

| Space | |||

| By Purpose | Command, Control, Communications, and Computer (C4) | ||

| Intelligence, Surveillance, and Reconnaissance (ISR) | |||

| Electronic Warfare (EW) | |||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Installation Type | New Installation | ||

| Upgrade/Retrofit | |||

| By End User | Defense and Military | ||

| Government and Law Enforcement | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current outlook for the C4ISR market through 2031?

The C4ISR market size is projected at USD 141.50 billion in 2026 and is forecast to reach USD 184.94 billion by 2031 at a 5.50% CAGR.

Which platform category leads C4ISR spending today?

Air platforms led with 36.75% share in 2025 because airborne sensing, battle management, and tactical data links remain central to multi-domain operations.

Which purpose area is expanding fastest in this space?

C4 is the fastest-growing purpose segment with a 6.29% CAGR through 2031 as defense buyers shift toward shared data fabrics and software-defined command layers.

Why is software growing faster than hardware?

Software is forecast to rise at 7.49% CAGR because open-architecture rules let buyers extend system value through updates, integration, and cyber hardening after deployment.

Which region offers the strongest near-term growth?

The Middle East and Africa is projected to grow at 8.28% CAGR through 2031, supported by selective modernization and ISR capability development programs.

What is the main execution risk for suppliers and buyers?

Integration across legacy and coalition systems remains a major risk because fragmented architectures and repeated certification steps can delay deployment and contract realization.

Page last updated on: