Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

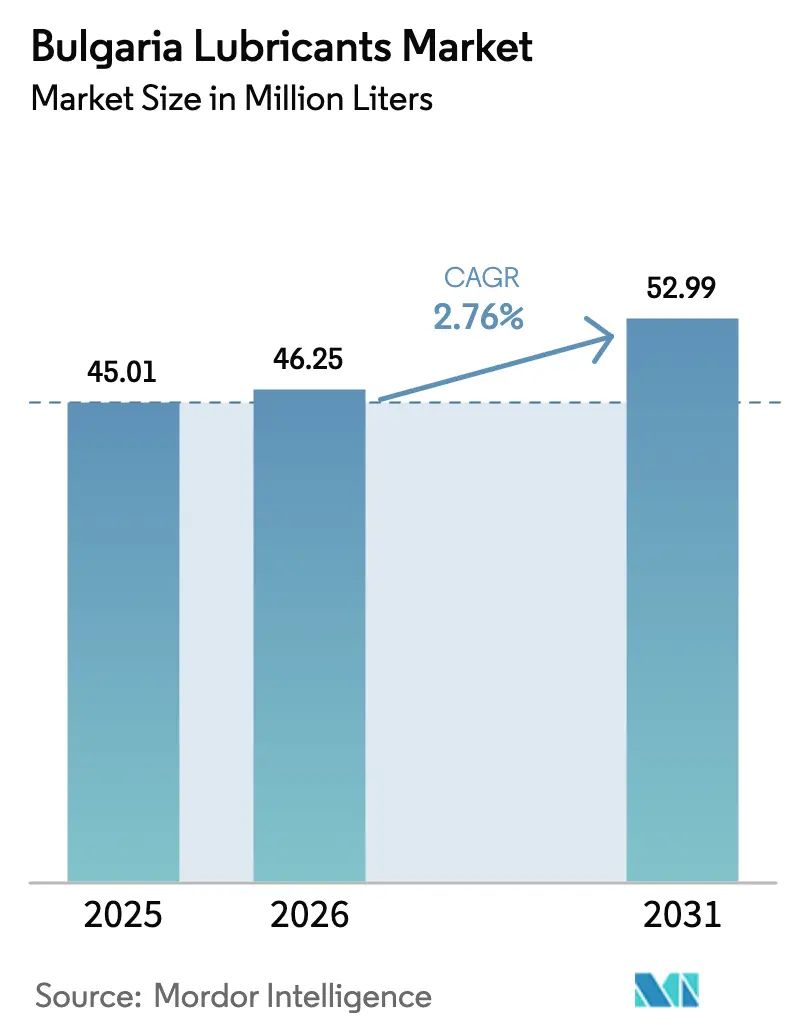

| Base Year Market Size (2025) | 45.01 Million liters |

| Market Volume (2026) | 46.25 Million liters |

| Market Volume (2031) | 52.99 Million liters |

| Growth Rate (2026 - 2031) | 2.76% CAGR |

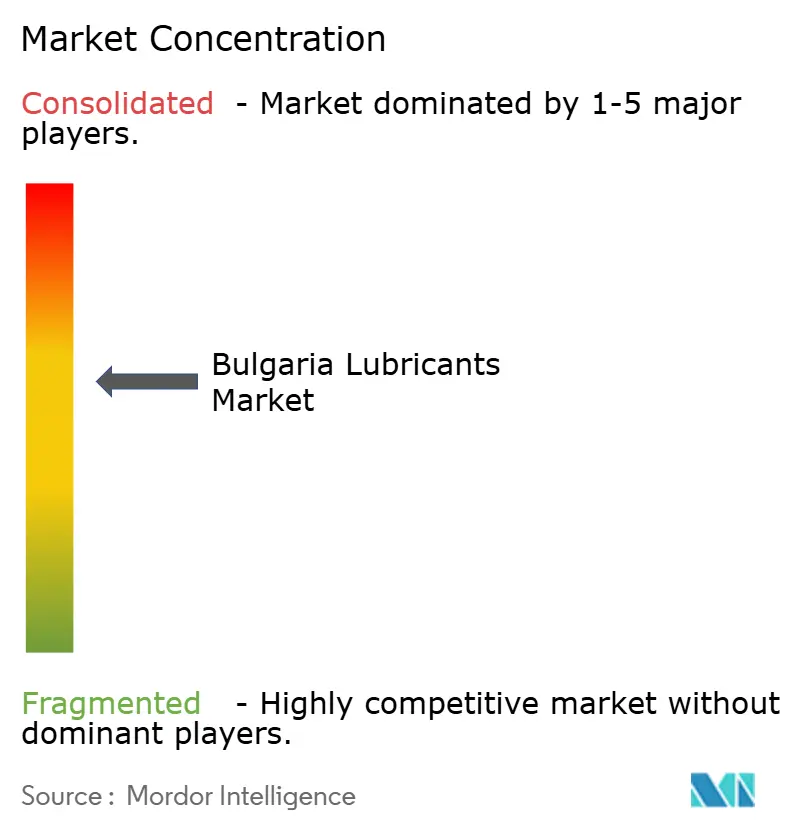

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bulgaria Lubricants Market Analysis by Mordor Intelligence

The Bulgarian Lubricants Market size in 2026 is estimated at 46.25 million liters, growing from 2025 value of 45.01 million liters with 2031 projections showing 52.99 million liters, growing at 2.76% CAGR over 2026-2031. Aging vehicles, selective industrial resilience, and EU-driven sustainability mandates together shape near-term volumes and long-term formulation shifts. Conventional engine oil demand remains strong, as the majority of Bulgaria’s registered vehicles have exceeded 15 years of service life. Industrial usage is supported by metallurgical and mining output, offsetting the slump in domestic vehicle manufacturing. EU Recovery and Resilience funds, totaling EUR 5.7 billion (USD 6.1 billion) through 2026, are set to boost construction and heavy-equipment activity, providing additional demand for hydraulic, gear, and grease products. On the supply side, reliance on a single refinery under Lukoil ownership amplifies feedstock risk, although local blending leader Prista Oil and new distribution alliances by international majors continue to widen product access.

Key Report Takeaways

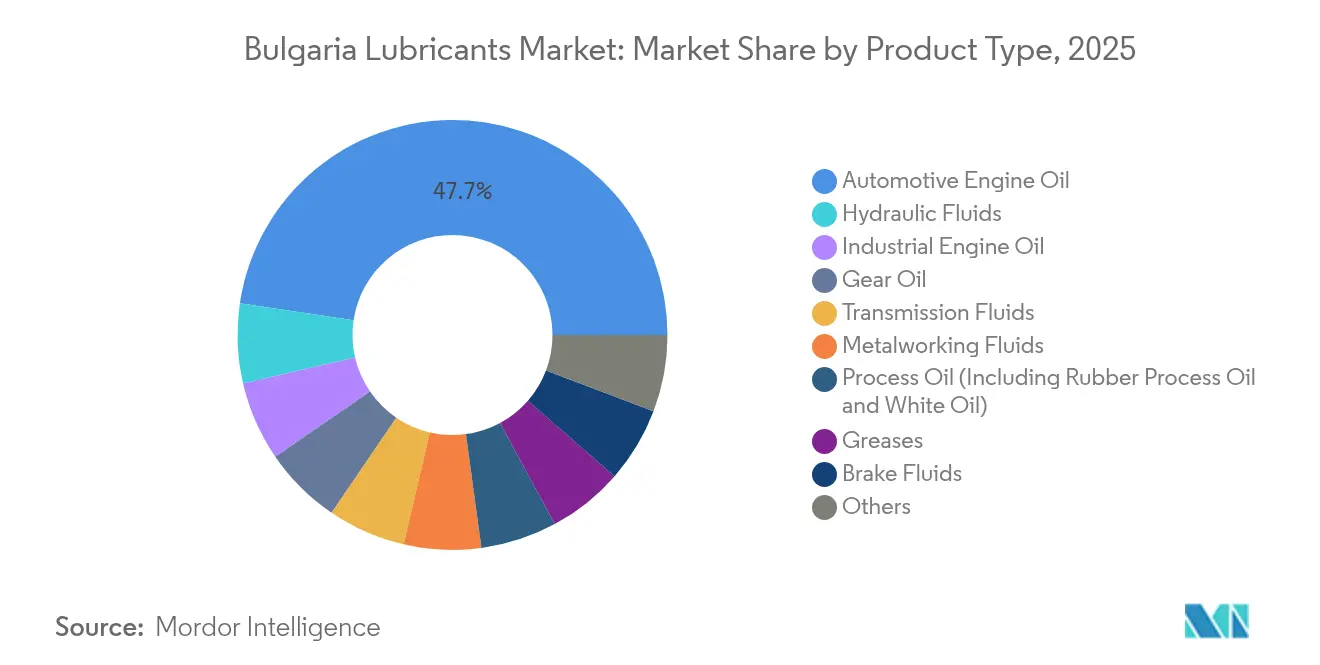

- By product type, Automotive Engine Oil held 47.65% of the Bulgarian lubricants market share in 2025. Industrial Engine Oil is projected to post the fastest 3.33% CAGR through 2031.

- By end-user industry, Automotive captured 59.60% of the Bulgarian lubricants market size in 2025. Industrial applications are advancing at a 2.93% CAGR to 2031.

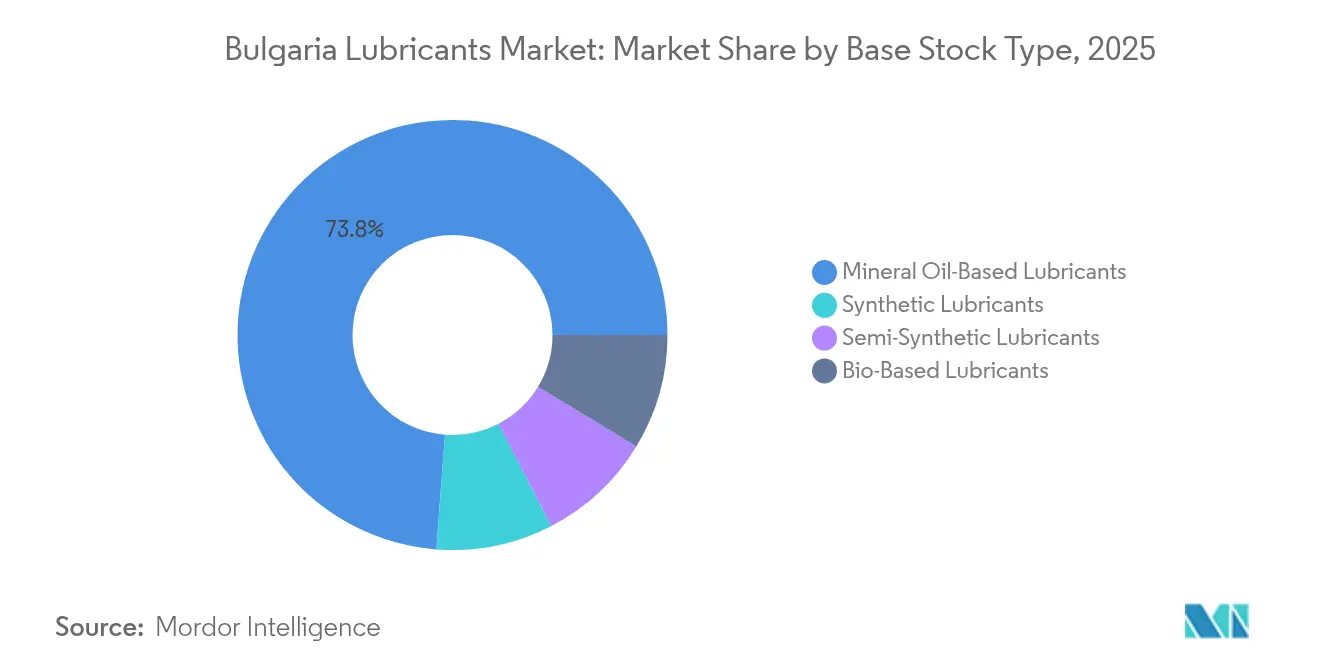

- By base stock, mineral oil formulations accounted for 73.80% of the 2025 volume; bio-based products led growth at a 3.17% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Bulgaria Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ICE-dominant vehicle parc | +0.8% | National, urban centers | Medium term (2-4 years) |

| Industrial rebound in metallurgy and heavy equipment | +0.6% | Mining regions | Medium term (2-4 years) |

| Euro 7 and ACEA C7 push low-viscosity synthetics | +0.4% | EU-wide | Long term (≥ 4 years) |

| Distributor consolidation | +0.3% | Rural penetration | Short term (≤ 2 years) |

| Base-oil rerefining investments | +0.2% | Bulgaria and Central Asia | Long term (≥ 4 years) |

| Predictive-maintenance telematics | +0.2% | Industrial clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

ICE-dominant vehicle parc sustains engine-oil demand

More than 70% of Bulgaria’s light-duty fleet exceeds 15 years, and 82.6% of new registrations in early 2025 were gasoline models[1]Marin Milkov, “New Car Registrations Down Y/Y in EU, Bulgaria,” bta.bg. The age profile translates into higher-viscosity oil consumption, frequent top-ups, and robust aftermarket sales through multi-brand service chains that serve over 80% of out-of-warranty vehicles. Limited EV incentives and in-use battery vehicles are expected to preserve the Bulgarian lubricants market’s dependence on internal-combustion formulations over the medium term.

Industrial output rebound in metallurgy and heavy equipment

Despite an overall decline in manufacturing in March 2025, fabricated metal products rose, and mining output increased, underpinning demand for hydraulic fluids, gear oils, and extreme-pressure greases. Bulgaria extracts minerals, with lignite and copper ore leading volumes, generating continuous lubricant requirements for draglines, mills, and haul trucks. Upcoming EU-funded modernization programs will add remote monitoring and longer-life synthetics to the consumption mix.

Euro 7 and ACEA C7 push low-viscosity synthetics

Regulation (EU) 2024/1257 introduces crankcase emission limits and onboard diagnostics, effective November 2026, which compel automakers to specify 0W-20 and thinner oils with low-SAPS chemistry[2]European Union, “Regulation (EU) 2024/1257 (Euro 7),” eur-lex.europa.eu. ACEA C7 further tightens volatility, ash, and oxidation criteria. Suppliers must therefore dual-track their portfolios for Bulgaria’s legacy fleet and its gradual influx of compliant vehicles, reshaping the Bulgarian lubricants market toward synthetics after 2027.

Distributor consolidation expands nationwide lubricant reach

TotalEnergies’ tie-up with Inter Cars unlocks a 250-branch aftermarket network, improving rural availability of branded fluids. Coupled with Lukoil’s 220-station retail grid, consolidated channels lower unit logistics cost and widen SKU offerings. Wholesalers dedicate a portion of revenue to inventory digitalization, enabling predictive stock and JIT delivery that benefits small garages.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing EV penetration and extended drain intervals | -0.5% | EU-wide | Long term (≥ 4 years) |

| Single-refinery base-oil dependence | -0.3% | National | Short term (≤ 2 years) |

| Tight waste-oil compliance costs | -0.2% | Industrial regions | Medium term (2-4 years) |

| Import-price volatility from Black-Sea freight disruptions | -0.2% | Regional | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing EV penetration and extended drain intervals

While EV adoption is modest, EU-wide targets imply an acceleration in uptake post-2026. Synthetics enabling 15,000-20,000 km of drains halve the annual oil volume per ICE vehicle, compounding the volumetric challenge even before electrification is fully established.

Single-refinery base-oil dependence risks feedstock shocks

Neftohim Burgas accounts for the domestic Group I supply; sanctions against parent Lukoil and crude-switch trials from Kazakhstan, Iraq, and Tunisia raise concerns about output stability. The Competition Protection Commission’s levy penalty for restricting rival imports underscores the fragility of Bulgaria's lubricants market logistics.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Automotive dominance drives conventional demand

Automotive Engine Oil accounted for 47.65% the Bulgarian lubricants market in 2025 and occupied the primary volume anchor for the Bulgarian lubricants market. Industrial Engine Oil is forecast to grow at a 3.33% CAGR, driven by rebounds in mining and fabricated metal industries that require high-load gear and compressor oils. Transmission fluids and gear oils experience incremental gains because older drivetrains require more frequent changes, while hydraulic fluid volumes benefit from infrastructure projects funded under EU recovery funds. Greases serve ports at Varna and Burgas, where water-resistant calcium-sulfonate grades are specified for ship-loader bearings.

Process oils supply Bulgaria’s plastics and tire producers; metalworking fluids expand in tandem with growth in the fabricated metals sector. Turbine and transformer oils protect power assets under grid modernization schemes, and low-SAPS synthetics are beginning to permeate the brake-fluid and ATF segments as Euro 7 rolls out.

By End-user Industry: Automotive leads while industrial accelerates

The Automotive segment generated 59.60% of the Bulgarian lubricants market size in 2025, thanks to a sizable million registered passenger cars and commercial-vehicle transit fleet that services the EU-Turkey trade corridor. Heavy-duty diesel trucks crossing Danube and Black-Sea ports add long-drain CK-4 and FA-4 demand, while two-wheelers contribute niche volumes of mono-grade or API SN oils.

Industrial usage, advancing at a 2.93% CAGR, spans power generation, metallurgy, and oil and gas exploration, including OMV Petrom’s Han Asparuh offshore block. Marine consumption is expected to increase through growth at Port Burgas, introducing ISO-FME-approved cylinder oils into the Bulgarian lubricants market. Agriculture and construction machinery, backed by EU-funded mechanization, lift demand for multifunctional tractor fluids and biodegradable hydraulic oils to meet eco-zone rules near river basins.

By Base Stock Type: Mineral oils dominate amid synthetic growth

Mineral formulations retained 73.80% volume in 2025, reflecting cost sensitivity across the Bulgarian lubricants industry workshops. Yet, bio-based lubricants, growing at a rate of 3.17% annually, are gaining traction in forestry, agriculture, and municipal fleets, aligning with EU Green Public Procurement criteria. Semi-synthetics bridge performance and price, particularly in light-duty gasoline vehicles seeking 10,000 km drains.

Full synthetics lead premium migration in industrial gearboxes and Euro 7 passenger cars, where 0W-20 and 0W-16 grades slash pumping losses. Prista’s rerefining initiatives and Motor Oil’s Greek Group II output ensure a stable feedstock alternative should Neftohim supply falter, supporting the Bulgarian lubricants market against external shocks.

Geography Analysis

Bulgaria’s lubricant demand is concentrated in Sofia, Plovdiv, Varna, and Burgas. Urban concentration shapes service-station placement and quick-lube footprints, favoring integrated distributors that can replenish high-turnover SKUs daily. Southeastern Burgas houses the single refinery and the nation’s largest petroleum port, enabling direct ship-borne base-oil inflow; Varna supports northern industrial clusters and naval facilities.

Mining regions in central-western provinces drive specialty industrial demand, particularly for open-gear lubricants and rock-drill oils used in the extraction of lignite and copper. Agricultural belts in the Danube Plain employ universal tractor transmission oils and biodegradable hydraulic fluids that are compatible with EU eco-zone regulations. Cross-border corridors to Greece and Turkey support heavy-haul diesel volumes, while Romanian transit generates top-up sales at the Danube River crossings.

Geopolitical shifts away from Russian feedstock have triggered diversification of crude supply through Azerbaijani, Iraqi, and North African grades, altering supply logistics along the Black Sea coast. The EUR 5.7 billion recovery program earmarks regional infrastructure upgrades, which will propel the use of road-building machinery lubricants. Consequently, the Bulgarian lubricants market is expected to see Burgas and Sofia combined consume almost 37.50% of national volume by 2031, even as rural penetration improves through distributor consolidation.

Competitive Landscape

The Bulgarian lubricants market is moderately concentrated. Small importers focus on private-label mineral oils, particularly in rural retail settings. Digital tools such as IoT-enabled fluid monitoring and e-commerce portals differentiate premium players, whereas smaller firms compete on price and localized service. White-space opportunities lie in EV-specific fluids—such as dielectric coolants and e-axle greases—and circular-economy services, including waste-oil collection, rerefining, and carbon-footprint reporting. Market entry barriers remain moderate: EU regulations demand technical conformity but do not impose local content rules, while aggressive pricing and warranty partnerships can offset brand loyalty in the automotive aftermarket.

Bulgaria Lubricants Industry Leaders

Prista Oil

Lukoil

Shell Plc

BP Plc (Castrol)

TotalEnergies SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BP Plc (Castrol) announced the divestment process for its Castrol unit, a move that could reshape product availability across Eastern Europe, including Bulgaria.

- March 2024: Alpha Bulgaria’s shareholders have approved a plan to purchase up to 200,000 shares in Prista Oil for BGN 20 million, with the aim of funding capacity upgrades and market expansion.

Bulgaria Lubricants Market Report Scope

Lubricant products are made from a combination of base oils and additives. The composition of base oil in the formulation of lubricants is primarily between 75-90%. The Bulgaria lubricants market is segmented by product type and end-user industry. The market is segmented by product type: engine oils, transmission and gear oils, hydraulic fluid, metalworking fluid, greases, and other product types. The market is segmented by end-user industries: power generation, automotive, heavy equipment, metallurgy and metalworking, and other end-user industries. For each segment, the market sizing and forecasts have been provided based on volume (million liters).

By Product Type

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

By End-user Industry

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-Use Industries |

By Base Stock Type

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-Use Industries | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

Key Questions Answered in the Report

What is the current size and growth outlook for lubricants demand in Bulgaria?

Consumption reached 46.25 million liters in 2026 and is projected to rise to 52.99 million liters by 2031, reflecting a 2.76% CAGR.

Which product category generates the highest sales volume?

Automotive engine oil, with a 47.65% share of the 2025 volume, is expected to remain dominant through 2031.

How will Euro 7 regulations change lubricant specifications in the country?

The rule takes effect for new vehicle types in November 2026 and will accelerate the shift to ultra-low-viscosity, low-SAPS synthetics that meet ACEA C7 criteria.

What effect could electric-vehicle adoption have on lubricant volumes?

Rising electrification, combined with longer drain intervals, is forecast to trim approximately 0.5% from long-term volume growth.

Page last updated on: