Brazil Lime Market Analysis by Mordor Intelligence

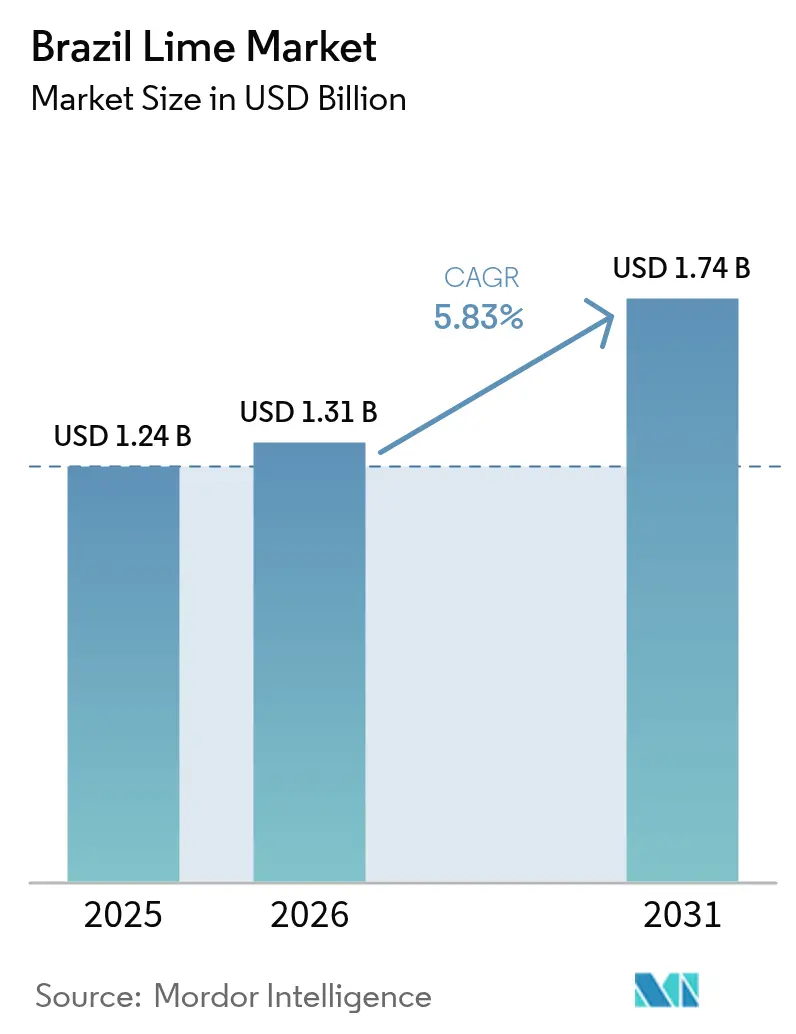

The Brazil lime market size is expected to grow from USD 1.24 billion in 2025 to USD 1.31 billion in 2026 and is forecast to reach USD 1.74 billion by 2031 at 5.83% CAGR over 2026-2031. This steady expansion reflects the country’s reinforced status as a global lime powerhouse, supported by a 70.3% leap in export value between 2020 and 2023 and underscored by its position as the world’s seventh-largest lime exporter in 2023. Export strength coincides with resilient domestic demand, where premium cocktail culture, clean-label food trends, and health-oriented diets sustain year-round consumption growth. Improving phytosanitary access, most recently, the April 2025 approved that opened India’s 1.4 billion-person market, offers new geographic outlets that are likely to temper Brazil’s long-standing reliance on the European Union for 85% of volumes. Meanwhile, water-efficient irrigation, no-till practices, and semi-dwarf rootstocks mitigate yield risk tied to rising disease pressure, keeping cost structures competitive even as energy, certification, and logistics costs rise.

Key Report Takeaways

- Brazil's lime market structure reveals production as the dominant value component, representing approximately 69.62% of total market value, with domestic consumption absorbing the majority of output while exports capture premium pricing for quality grades.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Lime Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing global demand for fresh lime | +1.8% | Global, led by European Union and expanding Asian markets | Long term (≥ 4 years) |

| Favorable climate and agricultural conditions | +1.2% | Southeast and Northeast production belts | Long term (≥ 4 years) |

| Expansion of food and beverage industry | +1.0% | Urban centers nationwide | Medium term (2–4 years) |

| Premium cocktail culture lifting domestic demand | +0.8% | Metropolitan areas, especially Southeast | Medium term (2–4 years) |

| New Asian market openings after phytosanitary deals | +0.7% | India, China, broader Asia-Pacific | Short term (≤ 2 years) |

| Climate-smart farming | +0.4% | Technology-enabled clusters in producing states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Global Demand for Fresh Lime

International appetite for Brazilian limes continues expanding, driven by health-conscious consumption patterns and culinary diversification across key export markets. Brazil's export performance demonstrates this trend, with lime exports achieving 14.35% year-over-year growth in 2023, significantly outpacing traditional citrus categories. In 2024, the European Union remains the dominant destination, absorbing approximately 85% of Brazilian lime exports, while South American markets capture the remaining 15%. This geographic concentration creates both opportunity and risk, as recent market access agreements with India represent critical diversification, potentially reducing dependence on European demand cycles. The processed lime segment benefits from industrial applications in beverage manufacturing, where Natural One's acquisition of lime farms from Vêneto Agrícola in 2024 exemplifies vertical integration strategies to secure raw material supply chains.

Favorable Climate and Agricultural Conditions

Brazil's tropical and subtropical climate zones provide optimal growing conditions for Tahiti lime cultivation, with year-round production capability distinguishing Brazilian supply from seasonal competitors. The Northeast region, particularly Bahia, emerges as a strategic expansion zone due to lower disease pressure compared to traditional São Paulo production areas. Climatic advantages extend beyond temperature and rainfall patterns to include reduced Huanglongbing incidence in newer production regions, creating natural barriers against the sector's most devastating disease. Water resource availability supports irrigation expansion, with precision agriculture adoption accelerating across major production states. Recent research demonstrates that no-tillage systems with cover crops significantly improve root development, water uptake, and photosynthetic efficiency in Tahiti lime cultivation, providing producers with sustainable intensification pathways.

Expansion of Food and Beverage Industry

Brazil's dynamic food and beverage sector drives sustained lime demand through both traditional applications and innovative product development. The domestic market benefits from robust foodservice recovery, with the sector reaching R$548 billion (USD 106 billion) in 2022, increasing out-of-home consumption that directly supports fresh lime demand[1]Source: Frontiers in Sustainable Food Systems, “Physiological Responses of Tahiti Lime,” frontiersin.org . Premium cocktail culture particularly influences lime consumption patterns, with citrus flavors representing 50% of Brazilian cocktail preferences according to Kerry's comprehensive field study across 40 top Brazilian bars. The mocktail trend further expands addressable markets, driven by Generation Z consumption patterns where only 45% consume alcoholic drinks, creating demand for sophisticated non-alcoholic beverages that maintain citrus flavor profiles. Industrial applications grow through vertical integration strategies, exemplified by Natural One's farm acquisitions to secure lime supply for juice production and shelf-life optimization.

Premium Cocktail Culture Lifting Domestic Demand

Brazilian cocktail culture undergoes sophisticated evolution, with lime emerging as an indispensable ingredient across traditional and contemporary beverage applications. Market research reveals citrus flavors dominate 50% of cocktail recipes in Brazil's top establishments, with lime specifically highlighted as a primary citrus component. This trend extends beyond alcoholic beverages to encompass the rapidly growing mocktail segment, driven by demographic shifts where Generation Z shows reduced alcohol consumption but maintains demand for sophisticated flavor profiles. The premium positioning of Brazilian bars increasingly emphasizes fresh, high-quality ingredients, creating opportunities for specialty lime varieties and organic production. Regional fruit diversification, including native ingredients like capim-limão, complements rather than displaces traditional lime usage, suggesting market expansion rather than substitution.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production and transportation costs | -1.5% | All producing regions, export corridors | Medium term (2–4 years) |

| Competition from Mexico, Peru and others | -1.2% | Europe and North American markets | Short term (≤ 2 years) |

| Rising citrus canker and HLB (Huanglongbing) incidence | -0.8% | São Paulo core belt, spreading zones | Long term (≥ 4 years) |

| Harvest-season labor shortages | -0.6% | Legacy orchards in Southeast | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Production and Transportation Costs

Brazil's lime sector faces mounting cost pressures that threaten export competitiveness and domestic market accessibility. Transportation infrastructure limitations create significant logistical bottlenecks, particularly for fresh produce requiring cold chain management from interior production regions to major ports and urban consumption centers. The concentration of production in São Paulo state, while historically advantageous, now creates vulnerability as land costs escalate and labor availability tightens during peak harvest seasons. Energy costs for irrigation systems, essential for maintaining year-round production and fruit quality, add substantial operational expenses that smaller producers struggle to absorb. Currency fluctuations compound these challenges, as input costs often correlate with USD-denominated imports while domestic pricing remains in Brazilian reais, creating margin compression during periods of real weakness.

Competition from Mexico, Peru, and Others

International competition intensifies as established lime-producing countries expand capacity and new entrants emerge with competitive advantages. Mexico maintains a dominant global market position through proximity to the lucrative North American market, supplying over 90% of US lime imports and leveraging established distribution networks that Brazilian exporters struggle to penetrate [2]Source: U.S. International Trade Commission, “Lemon Juice from Brazil and South Africa,” usitc.gov . Peru's aggressive expansion in citrus production, supported by favorable trade agreements and lower labor costs, creates direct competition in European markets where Brazilian exporters traditionally held strong positions. The competitive landscape shifts as climate change affects traditional producing regions differently, with some competitors benefiting from reduced disease pressure while Brazil faces increasing Huanglongbing incidence in core production areas.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

Brazil's lime production demonstrates pronounced regional concentration, with the Southeast region commanding the largest market share in 2025, anchored by São Paulo state's position as the undisputed production leader, generating over 1.2 million metric tons annually . São Paulo's dominance stems from established infrastructure, specialized expertise, and proximity to major ports that facilitate export operations to European markets, absorbing 85% of Brazilian lime exports. Minas Gerais and Rio de Janeiro contribute additional production capacity within the Southeast region, benefiting from similar climatic conditions and established supply chains. The region faces mounting challenges from Huanglongbing and citrus black spot diseases that threaten long-term sustainability, prompting producers to explore alternative locations with lower disease pressure.

The Northeast region emerges as the fastest-growing region, driven by Bahia's leadership in organic lime production and favorable disease profiles that support sustainable expansion. Itacitrus exemplifies this regional potential, operating 1,700 hectares in Inhambupe with plans to triple production within 5 years, achieving R$60 million (USD 11.1 million) revenue in 2023 through European export focus. Pernambuco and Ceará contribute additional Northeast production, though scale remains limited compared to traditional regions. The region's growth potential requires substantial irrigation investment due to semi-arid conditions, but offers advantages including year-round production capability and reduced transportation costs to European markets through northeastern ports. Climate-smart farming adoption accelerates in the Northeast, with biodynamic production systems demonstrating viability in Caatinga soils while meeting stringent European organic certification requirements. The South region maintains smaller-scale production primarily serving domestic markets, while the North region shows emerging potential through Pará state developments, though infrastructure limitations constrain expansion pace. Geographic diversification strategies respond to disease concentration risks while capturing regional competitive advantages in land costs, climate conditions, and government incentives. The region offers compelling advantages, including lower Huanglongbing pressure, favorable state financing through constitutional funds, and abundant land availability at competitive prices. Irrigation becomes essential due to high temperatures and sandy soils, but enables high productivity when properly managed.

Recent Industry Developments

- April 2025: Brazil secured market access to India for five citrus products, including Tahiti lime, representing the 55th market opening achieved in 2025 and unlocking access to over 1.4 billion consumers in Brazil's 10th largest agricultural export market.

- June 2023: The Brazilian Agriculture Research Corporation, the Coopercitrus Credicitrus Foundation, and the Sylvio Moreira Citriculture Center have jointly introduced a new Tahiti lime variety called Ponta Firme for the central, north, and northwest regions of the state of São Paulo. The productivity of the new variety has reached an average of 80 tons per hectare, 242% higher than the average for the state of São Paulo.

- January 2023: The Brazilian government announced a new industrial policy called "New Industry Brazil," set to run until 2033. This initiative includes equity investments of USD 802.9 million. The policy aims to stimulate productive and agricultural machinery development, enhance technological advancement, and increase overall competitiveness. Additionally, it places innovation and sustainability at the core of economic development, promoting research and technology in the agriculture sector.

Brazil Lime Market Report Scope

Lime is a small, green or yellow citrus fruit, known for its tart and acidic flavor. It is typically round or oval in shape and belongs to the Citrus genus, which also includes lemons and oranges. Limes are rich in vitamin C and are commonly used in cooking, beverages, and for their juice. The report analyzes key parameters of the lime market, focusing on commercial lime fruit as a commodity and highlighting significant developments in this niche market. The report includes production analysis (volume), consumption analysis (value and volume), export analysis (value and volume), import analysis (value and volume), and price trend analysis. The report offers market estimation and forecast in value (USD) and volume (Metric tons) for the above-mentioned segments.

Key Questions Answered in the Report

What is the 2026 value of the Brazil lime market?

The market is valued at USD 1.31 billion in 2026.

How fast is the market projected to grow through 2031?

It is projected to expand at a 5.83% CAGR, reaching USD 1.74 billion by 2031.

Which region is growing fastest for lime cultivation?

The Northeast is advancing at a significant share as producers seek lower disease pressure.

Why is India significant for Brazilian lime exporters?

India's 1.4 billion consumers became accessible in 2025 following a new phytosanitary agreement, offering diversification beyond Europe.

Page last updated on: