Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

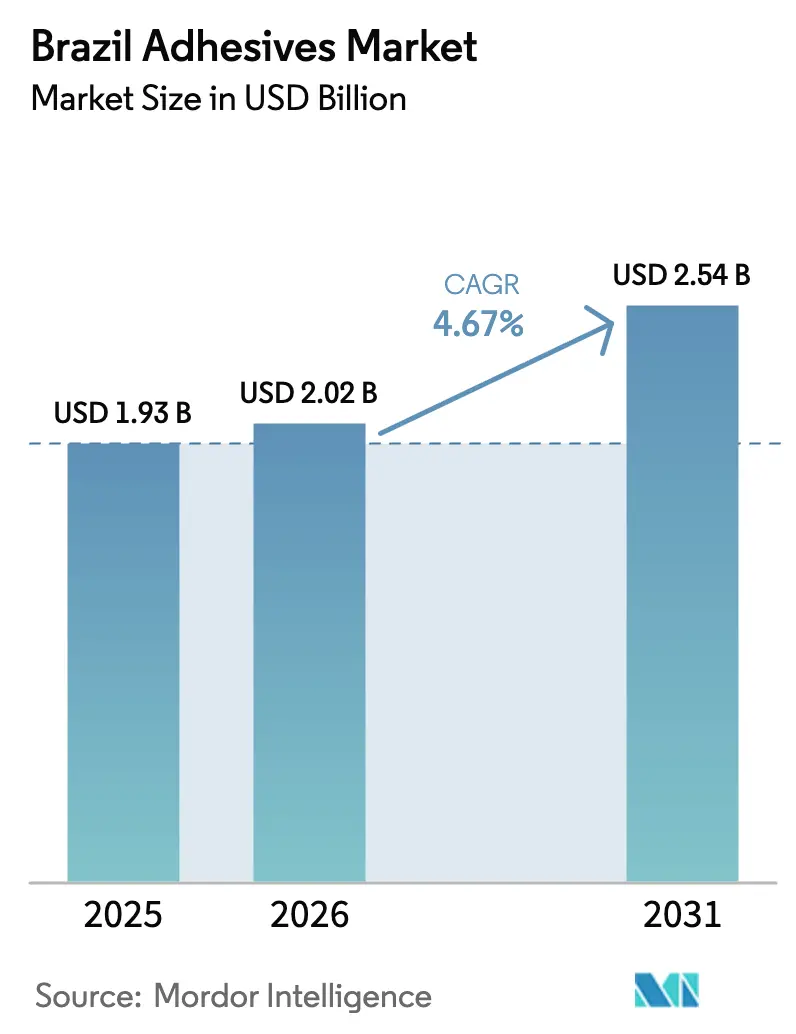

| Base Year Market Size (2025) | USD 1.93 Billion |

| Market Size (2026) | USD 2.02 Billion |

| Market Size (2031) | USD 2.54 Billion |

| Growth Rate (2026 - 2031) | 4.67% CAGR |

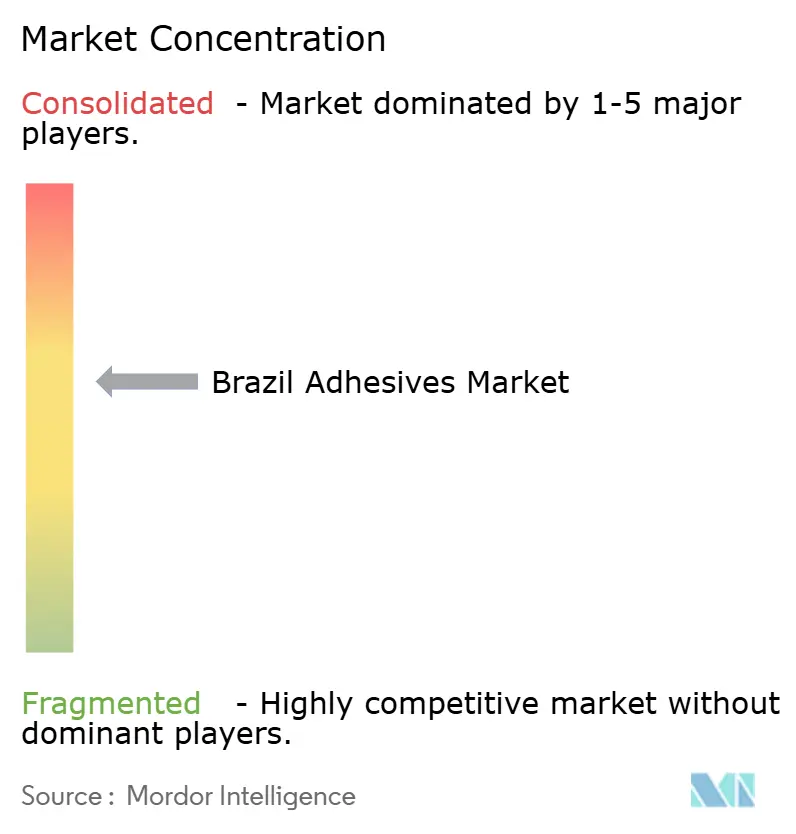

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Brazil Adhesives Market Analysis by Mordor Intelligence

The Brazil Adhesives Market size was valued at USD 1.93 billion in 2025 and is estimated to grow from USD 2.02 billion in 2026 to reach USD 2.54 billion by 2031, at a CAGR of 4.67% during the forecast period (2026-2031). Shifts in consumer demand for packaging, coupled with the expansion of federal infrastructure projects and a regulatory tilt toward low-VOC chemistries, are driving steady volume gains in the adhesive market. These developments are also reducing the volatility that has historically affected this cyclical segment. Water-borne technologies, already at the forefront of high-throughput packaging and labeling, are well-positioned to maintain their dominance, especially as ANVISA tightens solvent-emission standards. As industries such as aerospace, wind energy, and electric vehicles expand, they are increasingly adopting reactive systems for lightweight structural bonding, a requirement that mechanical fasteners cannot fulfill. In a strategic shift, multinational companies are realigning their supply-chain strategies by moving closer to end users. By localizing compounding and prototyping, they are not only mitigating freight challenges but also outpacing regional specialists known for their agility.

Key Report Takeaways

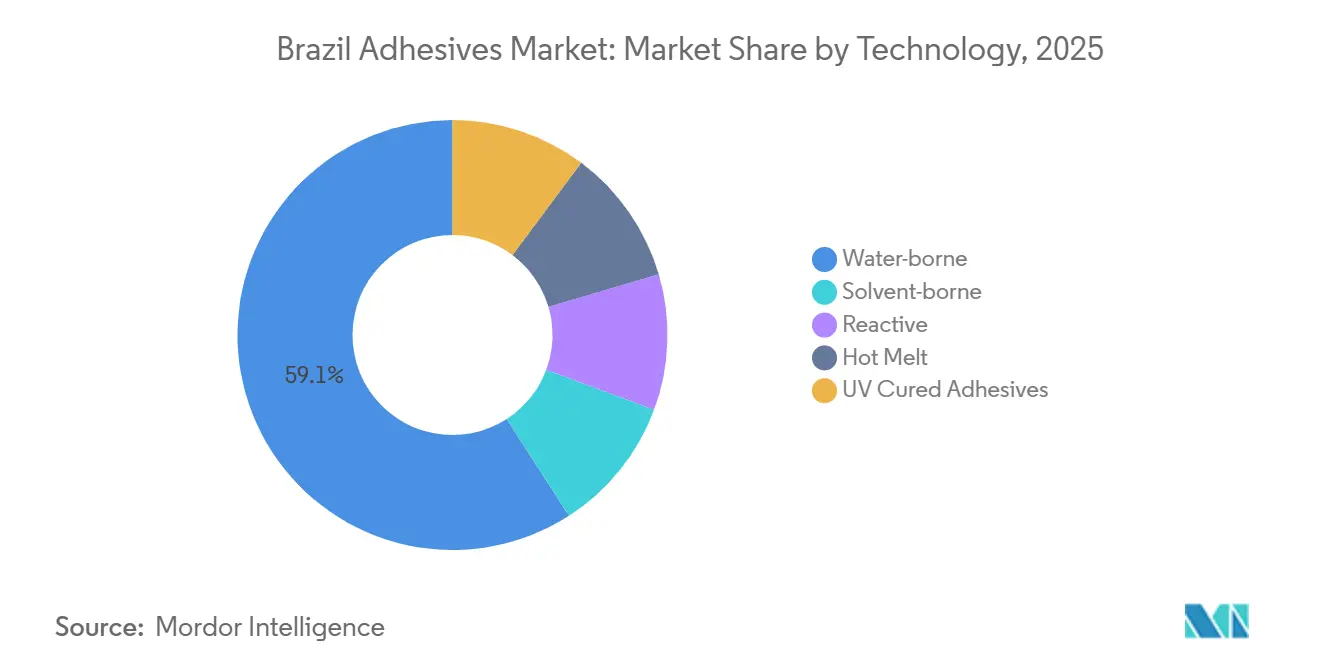

- By technology, water-borne products held 59.12% of Brazil's adhesive market share in 2025. Reactive formulations are forecast to register the fastest 5.12% CAGR through 2031.

- By resin, acrylic systems led with 29.22% share of the Brazil adhesives market size in 2025. Epoxy resins are advancing at a 5.18% CAGR between 2026-2031.

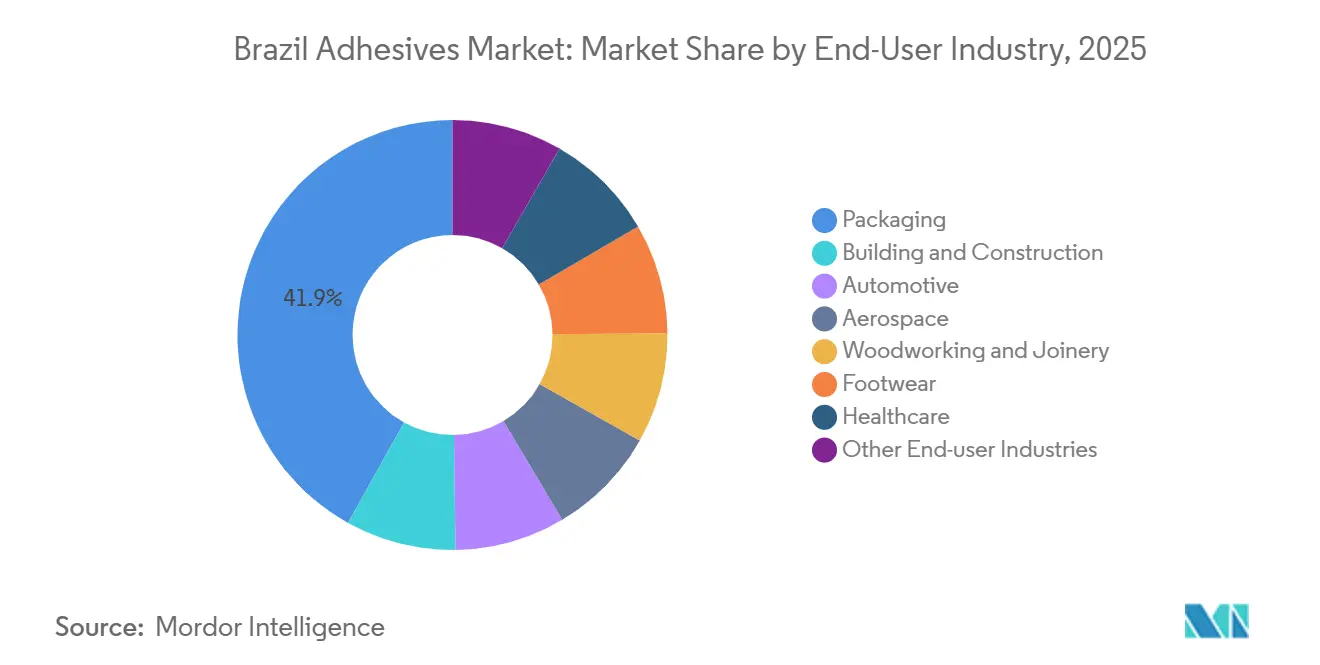

- By end-user industry, packaging commanded 41.93% revenue share in 2025. Aerospace applications are projected to expand at a 6.49% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Brazil Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce-led boom in consumer-packaging demand | +1.2% | National, concentrated in São Paulo, Rio de Janeiro, Minas Gerais metro areas | Medium term (2-4 years) |

| Federal infrastructure PAC-3 spending pipeline | +0.8% | National, with early gains in Southeast and Northeast corridors | Long term (≥ 4 years) |

| Regulatory shift toward low-VOC and bio-based adhesives | +0.9% | National, driven by ANVISA and environmental agencies | Medium term (2-4 years) |

| Adoption of specialty adhesive tapes in agribusiness logistics | +0.5% | South and Center-West regions (soy, corn, cattle corridors) | Short term (≤ 2 years) |

| Surging demand for PV-module encapsulant adhesives in rooftop solar | +0.7% | National, with concentration in Southeast (São Paulo, Minas Gerais) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-Commerce-Led Boom in Consumer-Packaging Demand

By 2025, online retail sales will have experienced significant growth. The packaging sector, supported by this expansion, is witnessing a notable increase, particularly in carton-sealing, lamination, and label adhesives. As free-shipping thresholds decrease, converters are increasingly utilizing hot-melt and acrylic pressure-sensitive adhesives. These adhesives enable the use of thinner substrates without compromising seal strength. Following the Rapid Pix settlement, subscription shipments have risen, driving adhesive demand from direct-to-consumer brands. Recent reforms in cross-border duties have reduced the price advantage of imports, benefiting local converters skilled in quick pack format customizations. Additionally, investments in solventless lamination are expanding the market for water-borne acrylic dispersions and reactive polyurethanes. These materials comply with new VOC limits while maintaining the barrier performance required by multinational brand owners.

Regulatory Shift Toward Low-VOC and Bio-Based Adhesives

In February 2025, ANVISA's Resolution 961 approved new monomers for food contact. However, it tightened migration caps, pushing formulators to either validate new certificates or exit lucrative niches. Rooted in Law 15,022/2024, this decree introduces a National Inventory, which imposes annual fees and emphasizes risk management for substances flagged as perilous by GHS[1]Ministério do Meio Ambiente, “Decree Regulating Law 15,022/2024,” gov.br. While multinationals are boosting bio-based research and development and pursuing mass-balance certification, regional producers are focusing on cost-effective water-borne acrylics to meet domestic construction and packaging demands. Academic reviews highlight soy protein, cassava starch, and lignin as the most cost-effective local feedstocks. However, challenges such as moisture resistance and curing speed continue to hinder high-speed production lines. The evolving regulatory landscape is creating a divide - one faction is advocating for sustainability-driven exports, while the other remains focused on price-sensitive domestic markets.

Surging Demand for PV-Module Encapsulant Adhesives in Rooftop Solar

Rising electricity tariffs have spurred a surge in rooftop solar adoption. This uptick amplifies the demand for silicone and modified-epoxy encapsulants, designed to withstand thermal cycles from -40 °F to +185 °F over 25 years. Bifacial glass-glass modules, which require more adhesive per panel, also demand specially formulated adhesives with matched thermal expansion to reduce interface stress. In response, suppliers are rolling out one-component moisture-cure silicones and UV-cure acrylics. These advancements not only shorten lamination cycles but also assist assemblers in cutting labor costs. However, certification hurdles from TÜV and UL pose formulation challenges, protecting established players with their proprietary test data. While grid interconnection delays in some states have slowed installations, incentives and net-metering initiatives offer a hopeful medium-term outlook.

Federal Infrastructure and Construction Activity

Brazil's PAC-3 plan is channeling public funds into roads, housing, and sanitation. This initiative is poised to elevate the demand for cement and related adhesives during the forecast period of 2026–2031. Sika's strategic expansion in Belo Horizonte is bolstering admixture capacity, leveraging Minas Gerais' prominence in concrete and its mining logistics. Tile adhesives are gaining traction, eclipsing traditional sand-cement mortars. This trend is attributed to the benefits of thinner beds and expedited curing times, which enhance project efficiency. Prefabricated modules are now employing structural adhesives to bond composite panels and windows seamlessly, significantly reducing on-site labor. Furthermore, fire safety and indoor air quality regulations are driving specifiers toward low-emission products, providing technical leaders with increased pricing flexibility.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter ANVISA solvent-emission caps | -0.6% | National, affecting all manufacturing facilities and import compliance | Short term (≤ 2 years) |

| Chronic highway-freight bottlenecks inflating distribution costs | -0.4% | National, most acute in North and Northeast regions; moderate impact in Center-West | Medium term (2-4 years) |

| Scarcity of domestic bio-based platform-chemical supply chain | -0.3% | National, with greatest impact on formulators pursuing sustainable product development in Southeast industrial corridor | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter ANVISA Solvent-Emission Caps

In March 2024, RDC 847 expanded its hazard-based oversight, moving from paints to include adhesives. This shift mandates registrants to submit migration, toxicology, and efficacy dossiers, putting a strain on the budgets of small and medium-sized enterprises (SMEs). Converters are now required to retrofit their production lines to accommodate water-borne or reactive grades, a change that demands both capital investment and training. Enforcement of these regulations varies by state, leading formulators to manage multiple stock-keeping units (SKUs) to ensure compliance everywhere, which, in turn, diminishes their economies of scale. Furthermore, the hazard-priority list suggests that mainstream monomers, such as toluene di-isocyanate, might soon face phased restrictions, introducing an added risk of reformulation.

Chronic Highway-Freight Bottlenecks Inflating Distribution Costs

In Brazil, roads play a pivotal role in transporting freight. However, challenges such as congestion, rising fuel prices, and tolls force adhesive suppliers to rely on temperature-controlled trucks. These trucks increase operational costs and face additional challenges during the harvest season, when capacity is limited. Smaller distributors, meanwhile, maintain a higher safety stock. This approach ties up their working capital, particularly for products with a shorter shelf life. Furthermore, customs inspections on hazardous materials can extend lead times by as much as three days, jeopardizing commitments to deliver just in time to major converters.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Water-Borne Formulations Anchor Volume, Reactive Systems Capture Margin

Water-borne products held 59.12% share of the Brazil adhesives market in 2025, underscoring a trend toward regulatory compliance and enhanced safety in plant handling. Acrylic and vinyl acetate-ethylene emulsions are favored by packaging and label converters for their quick-drying properties and low odor, especially on high-speed coaters. Flexible film lamination lines have been energized by solventless polyurethane and water-borne acrylic mixes. Hot-melts, prized for their zero VOCs and instant bonding capabilities, dominate both bookbinding and diaper assembly, ensuring seamless production lines. Reactive systems are on track for a 5.12% CAGR through 2031, lifted by epoxy and polyurethane uptake in aerospace, wind-blade shell bonding, and EV battery assembly, where bond integrity and heat resistance outclass mechanical fasteners. While facing pressures from VOC regulations, solvent-borne chemistries continue to cater to the footwear and leather industries, where immediate tack is essential. Although UV-cured products occupy a niche, they are witnessing growth in electronics and medical devices, buoyed by declining LED lamp prices and advancements in precision dispensing. Henkel's Latin America Inspiration Center in Jundiaí, which opened at the end of 2025, prototypes next-generation water-borne and reactive grades. These are specifically designed for Brazilian substrates, expediting the time-to-market for converters in pursuit of LEED-compliant bonds[2]Henkel, “Henkel to Construct Novel Inspiration Center,” henkel.in.

By Resin: Acrylic Versatility Versus Epoxy Performance

Acrylic systems accounted for a 29.22% share in 2025, thanks to cost efficiency and compatibility with multiple platforms, from water-borne to hot-melt. Acrylic polymers, essential in pressure-sensitive tapes and labels, maintain a delicate balance of tack and shear, making them indispensable in refrigeration units and engine-bay heat zones. Epoxy grades, forecast to grow 5.18% CAGR to 2031, reap tailwinds from composite airframe panels, wind blades, and printed-circuit boards that demand strength, thermal endurance, and chemical resistance. The automotive industry favors polyurethanes for their flexibility and compatibility with thermoplastic olefins, making them ideal for interiors and sealant joints. Cyanoacrylates, known for their rapid curing properties, dominate precision repairs in the medical sector and electronics, significantly reducing labor time. VAE and EVA copolymers, chosen for their cost-effectiveness, are widely used in woodworking and paper lamination. Silicones, despite having a smaller tonnage footprint, are critical for high-temperature gaskets and photovoltaic encapsulation due to their UV and heat stability. In a strategic move, Arkema's acquisition of Dow's lamination adhesives has enhanced Brazilian access to the Adcote and Mor-Free solventless lines, integrating them into Bostik's pressure-sensitive range and expanding formulation choices under a unified technical umbrella.

By End-User Industry: Packaging Scale Meets Aerospace Momentum

Packaging absorbed 41.93% of the Brazil adhesives market size in 2025. Converters increasingly turned to laminated films, sealed cartons, and labels, catering to both fast-moving consumer goods and the surging e-commerce sector. Water-borne acrylics and solventless polyurethanes predominantly drove most flexible-film bonds. Meanwhile, high-speed case erectors efficiently secured corrugated flaps using hot-melt. The aerospace sector, buoyed by Embraer's composite-rich airframes, leads growth at a 6.49% CAGR through 2031. These airframes, adhering to stringent aviation standards, depend on flame-retardant epoxies with low outgassing properties. Government housing initiatives and the rise of private retail complexes have bolstered the building and construction sector's adhesive demand. In this realm, there is a noticeable shift as polymer-modified tile mortars and panel sealants increasingly supplant traditional sand-cement mixes. With the rising penetration of electric vehicles (EVs), the automotive assembly is transitioning to high-modulus, crash-durable epoxies and thermal gap fillers. In woodworking, while PVA glues remain the go-to for furniture, moisture-curing polyurethanes are gradually making their mark for exterior joinery. The footwear industry, especially in high-end and safety boots, favors polyurethane cements, emphasizing solvent resistance despite the cost. Lastly, the medical device sector is leveraging biocompatible silicones and UV-cure acrylics to streamline and expedite sterile production lines.

Geography Analysis

São Paulo, Rio de Janeiro, and Minas Gerais are the dominant hubs for the automotive, packaging, and consumer-goods industries in Southeast Brazil. São Paulo leads with a dense concentration of flexible-film lamination, corrugators, and label makers, which drives a robust demand for acrylic emulsions, hot-melts, and reactive polyurethanes. Meanwhile, Minas Gerais, traditionally recognized for its mining strength, not only drives demand for cement and tile adhesives but also benefits from Sika’s expanding admixture operations, which optimize supply chains for construction clientele. In the southern regions, industries such as furniture, footwear, and cold-chain perishables thrive, relying on PVA wood glues, polyurethane shoe cements, and specialty tapes to ensure pallet stability. Brazilian formulators leverage Mercosur tariff benefits, facilitating cross-border flows into Argentina and Uruguay. The Northeast, energized by a growing middle class and infrastructural advancements, experiences heightened demand for commodity water-borne adhesives. However, the elevated freight costs from the Southeast prompt a shift toward local warehousing and small-batch compounding. In the North and Center-West, agribusiness export logistics dictate consumption patterns, particularly for package reinforcement tapes. However, persistent highway bottlenecks in these areas inflate premiums on temperature-controlled freight, tightening margins on lower-value grades. Highlighting the region's strategic significance, Henkel has established its inspiration center in Jundiaí, targeting the co-creation of products within Brazil’s densest converter corridor. These co-created products are on track for prestigious certifications such as LEED Gold and WELL Silver, making them particularly appealing to export-oriented clients.

Competitive Landscape

The market is moderately consolidated. Multinational giants dominate high-performance segments, bolstered by certification credentials, technical services, and integrated research and development. Meanwhile, regional players cater to SMEs by offering shorter lead times, custom batch flexibility, and smaller minimum orders. There is a push for white-space innovation, particularly in bio-based systems that capitalize on Brazil’s soy and pulp by-products. However, achieving moisture resistance performance parity remains a challenge.

Brazil Adhesives Industry Leaders

Henkel AG & Co. KGaA

3M

H.B. Fuller Company

Dow

Artecola Química

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Arkema finalized the acquisition of Dow’s flexible packaging laminating adhesives business, adding the Adcote and Mor-Free brands and five production sites, impacting the Brazilian adhesives Market.

- February 2024: Henkel announced construction of its first integrated innovation and technology center in Latin America, located in Jundiaí, São Paulo. The facility will support the Adhesive Technologies business unit.

Brazil Adhesives Market Report Scope

Adhesives are substances that join or bond two or more surfaces together by sticking to them. They are a type of material that provides cohesion between different substrates, creating a durable and often permanent bond. Adhesives are used in various applications, from everyday household use to industrial and technological processes.

The adhesives market is segmented by technology, resin, and end-user industry. By technology, the market is segmented into water-borne, solvent-borne, reactive, hot melt, and UV-cured adhesives. By resin type, the market is segmented into polyurethane, epoxy, acrylic, cyanoacrylate, VAE/EVA, silicone, and other resins. By end-user industry, the market is segmented into building and construction, packaging, automotive, aerospace, woodworking and joinery, footwear, healthcare, and other end-user industries. For each segment, the market sizing and forecasts have been done based on revenue (USD).

By Technology

| Water-borne |

| Solvent-borne |

| Reactive |

| Hot Melt |

| UV Cured Adhesives |

By Resin

| Polyurethane |

| Epoxy |

| Acrylic |

| Cyanoacrylate |

| VAE/EVA |

| Silicone |

| Other Resins |

By End-User Industry

| Building and Construction |

| Packaging |

| Automotive |

| Aerospace |

| Woodworking and Joinery |

| Footwear |

| Healthcare |

| Other End-user Industries |

| By Technology | Water-borne |

| Solvent-borne | |

| Reactive | |

| Hot Melt | |

| UV Cured Adhesives | |

| By Resin | Polyurethane |

| Epoxy | |

| Acrylic | |

| Cyanoacrylate | |

| VAE/EVA | |

| Silicone | |

| Other Resins | |

| By End-User Industry | Building and Construction |

| Packaging | |

| Automotive | |

| Aerospace | |

| Woodworking and Joinery | |

| Footwear | |

| Healthcare | |

| Other End-user Industries |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Woodworking & Joinery, Footwear & Leather, Healthcare, and Others are the end-user industries considered under the adhesives market.

- Product - All adhesive products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Cyanoacrylate, VAE/EVA, and Silicone are considered

- Technology - For the purpose of this study, Water-borne, Solvent-borne, Reactive, Hot Melt, and UV Cured adhesive technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms