Boat And Ship Telematics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

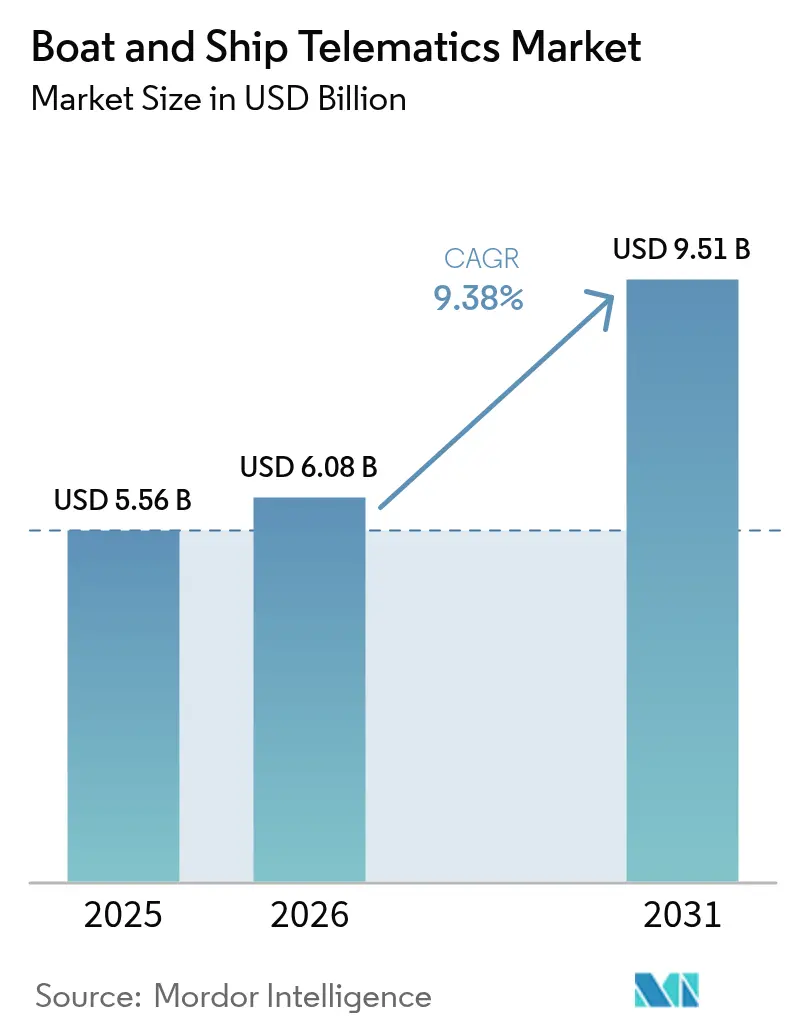

| Market Size (2026) | USD 6.08 Billion |

| Market Size (2031) | USD 9.51 Billion |

| Growth Rate (2026 - 2031) | 9.38% CAGR |

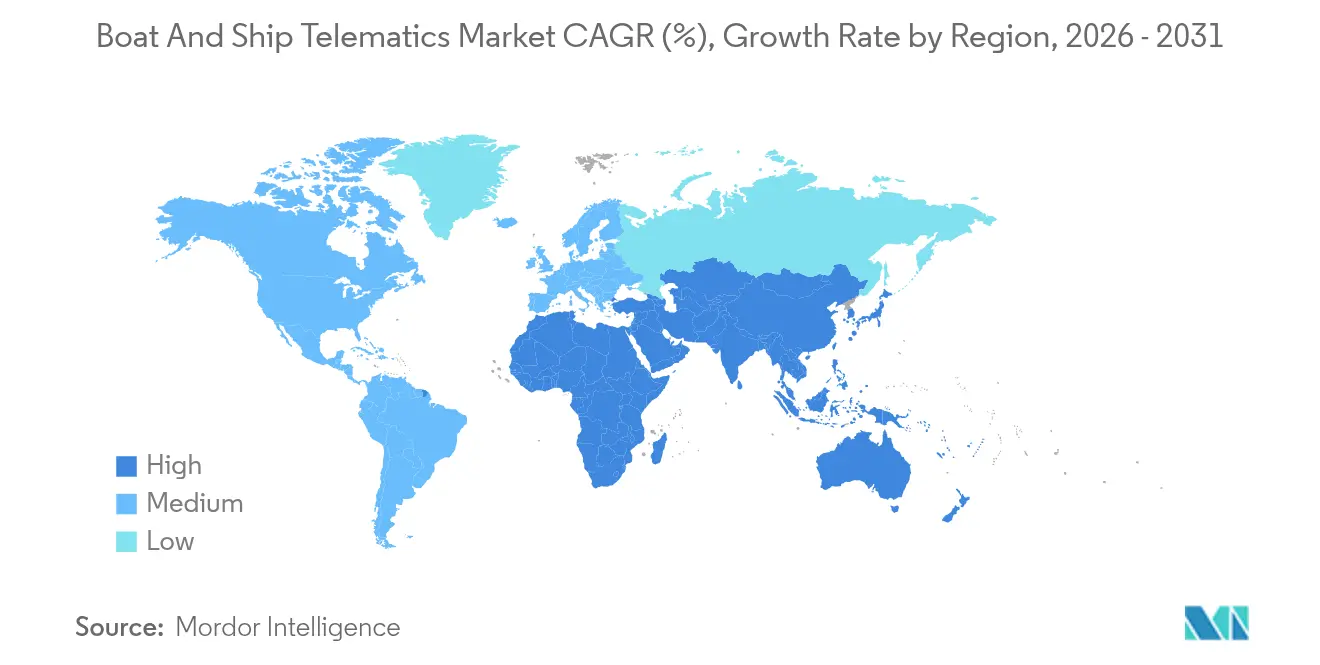

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

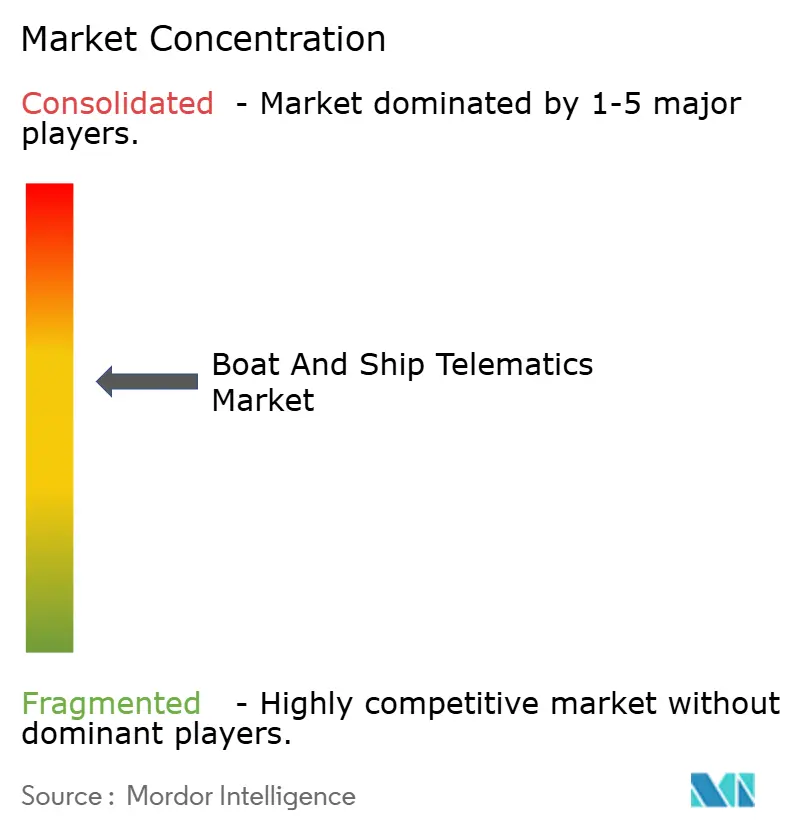

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Boat And Ship Telematics Market Analysis by Mordor Intelligence

The Boat and Ship Telematics market size is expected to grow from USD 5.56 billion in 2025 to USD 6.08 billion in 2026 and is forecast to reach USD 9.51 billion by 2031 at 9.38% CAGR over 2026-2031. Growth is propelled by mandatory long-range identification rules, expanding low-earth-orbit satellite networks, and rising demand for real-time fleet visibility that helps operators cut fuel use and emissions. Commercial fleets are standardizing cloud-based analytics for predictive maintenance, while defense agencies accelerate autonomous-vessel programs that require secure, always-on connectivity. Regional momentum is strongest in Asia-Pacific, where smart-port investments align with the Regional Comprehensive Economic Partnership, and in the Middle East, where the United Arab Emirates scales AI-enabled logistics corridors. Hardware still accounts for most spending, yet the fastest gains come from software platforms that turn streaming sensor data into actionable intelligence.

Key Report Takeaways

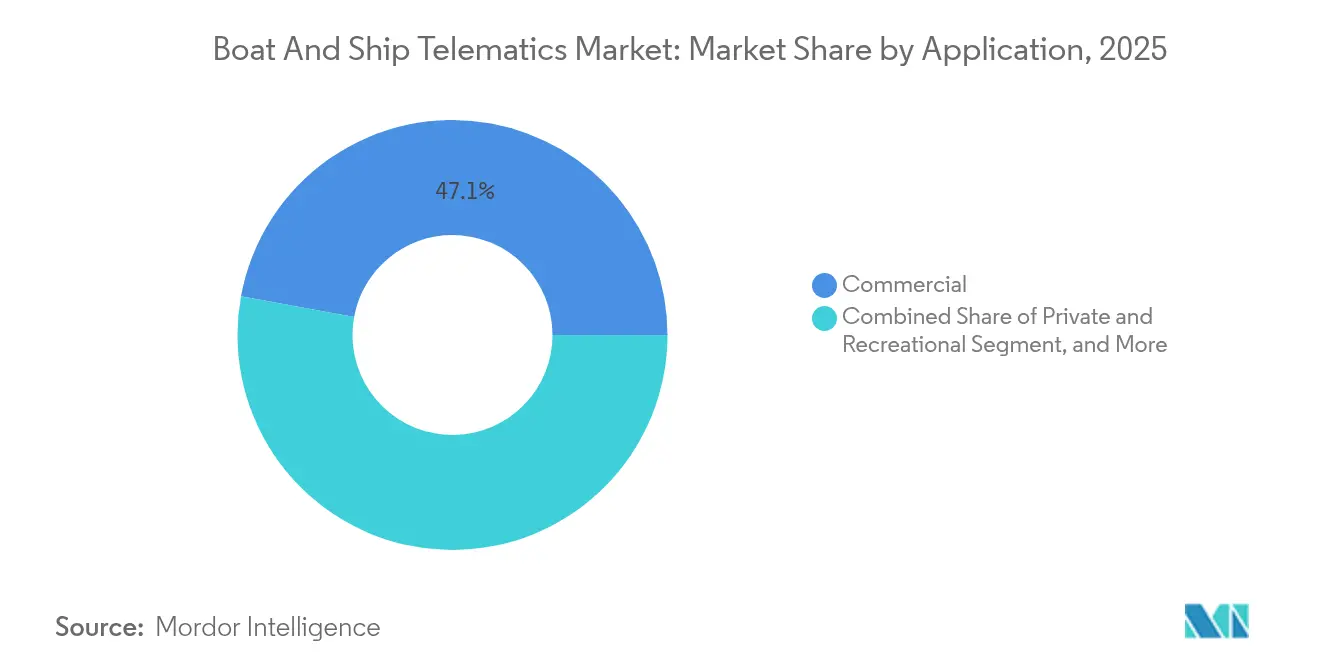

- By application, commercial vessels held 47.12% of the boat and ship telematics market share in 2025, whereas defense and security are set to expand at an 11.02% CAGR through 2031.

- By function, communication systems led with 37.88% revenue share of the boat and ship telematics market in 2025; data collection and analytics are forecast to grow at a 9.87% CAGR to 2031.

- By component, hardware captured 58.95% share of the boat and ship telematics market size in 2025, while software and platforms are pacing a 8.98% CAGR.

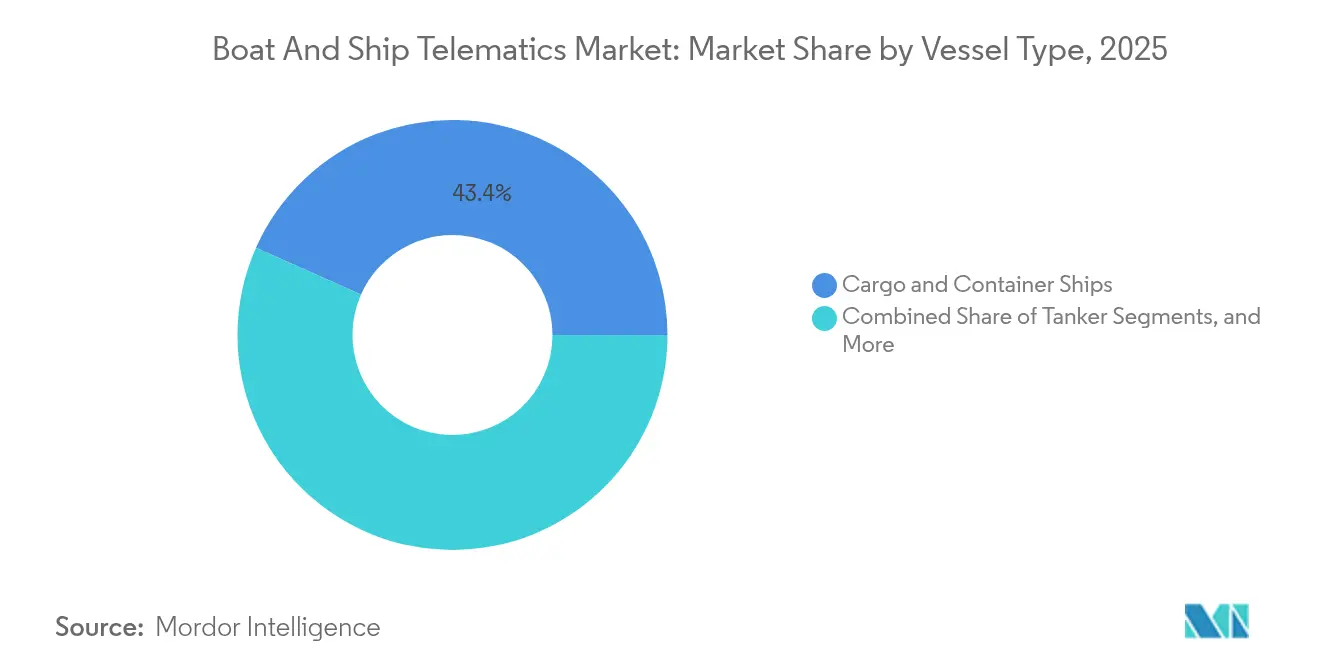

- By vessel type, cargo and container ships held a 43.35% share of the boat and ship telematics market in 2025; workboats and offshore support vessels showed the fastest 8.55% CAGR through 2031.

- By communication technology, satellite links dominated with a 54.62% share of the boat and ship telematics market in 2025 and are poised for an 10.98% CAGR as low-earth-orbit constellations mature.

- By geography, Asia-Pacific led with 36.55% market share of the boat and ship telematics market in 2025; the Middle East and Africa region is projected to post a 9.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Boat And Ship Telematics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Real-Time Fleet-Wide Visibility Demand | +2.1% | Global, led by Asia-Pacific and Europe | Medium term (2-4 years) |

| Stringent IMO/SOLAS Compliance Push | +1.8% | Global, mandatory for international vessels | Short term (≤ 2 years) |

| Satellite-IoT Coverage Expansion | +1.5% | Global, especially remote ocean routes | Long term (≥ 4 years) |

| Growth In Global Seaborne Trade | +1.3% | Core in Asia-Pacific, spill-over to MEA and Europe | Medium term (2-4 years) |

| Insurance Premium Incentives For Connectivity | +1.0% | North America and Europe leading, expanding globally | Medium term (2-4 years) |

| AI-Powered Predictive Maintenance Value | +0.9% | Advanced maritime economies, gradual global adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Real-Time Fleet-Wide Visibility Demand

Operators now integrate multi-sensor platforms that track position, fuel burn, and cargo status each minute. Weathernews processes routing data from 5,000 ships monthly, enabling managers to reroute around storms and slash operating costs by up to 15% [1]“Global Fleet Routing Services Overview,”, Weathernews Inc., weathernews.com. IoT devices funnel data through satellite and 5G pipelines into cloud dashboards where analytics flag anomalies before they escalate. The result is a shift from reactive to proactive decisions that protect schedules and margins. Autonomous-vessel trials intensify this need by requiring continuous situational awareness for safe remote control.

Stringent IMO/SOLAS Compliance Push

Revised SOLAS Chapter IV obliges all cargo ships over 300 GT to transmit identity and position every six hours, widening the addressable boat and ship telematics market [2]“SOLAS Consolidated Edition 2024,”, International Maritime Organization, imo.org. LRIT subscribers exceeded 46,000 vessels in 2024, generating strong demand for secure L-band channels[3]“LRIT Subscriber Growth Report 2024,”, Satellite Today Staff, satellitetoday.com. Compliance now extends to cyber-risk audits and emissions reporting, pushing owners toward integrated platforms that automatically log Carbon Intensity Indicator scores for regulators.

Satellite-IoT Coverage Expansion

Low-earth-orbit constellations cut latency to 50 milliseconds, unlocking bandwidth-heavy use cases such as live video from engine rooms. Eastern Pacific Shipping tested Starlink links via Marlink and reported crew-welfare gains and smoother data offload cycles The Maritime Executive. Equipment prices are stabilizing at USD 3,300 per terminal, while flexible service tiers enable smaller operators to enter the boat and ship telematics market without prohibitive upfront costs.

AI-Powered Predictive Maintenance Value

DeepSea Technologies models reach 99% accuracy in forecasting hull and propeller efficiency, enabling operators to plan cleaning stops just in time. Magellan X’s ChordX digital twin pairs physics with machine learning to extend machinery life and curb unplanned downtime by 20%. These gains reinforce the case for scaling data-rich telematics fleets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX and Bandwidth Costs | −1.4% | Global, strongest on small and emerging-market operators | Short term (≤ 2 years) |

| Maritime Cyber-Risk Exposure | −0.8% | Advanced digital economies, widening worldwide | Medium term (2-4 years) |

| Shortage Of Maritime Data Scientists | −0.6% | Global, acute in developing maritime economies | Long term (≥ 4 years) |

| RF Spectrum Congestion In Busy Sea-Lanes | −0.4% | High-traffic corridors and major port approaches | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High CAPEX and Bandwidth Costs

Full-suite installations can top USD 50,000 per ship when VSAT, 5G modems, sensors, and crew training are rolled together. Monthly data fees above USD 10,000 strain budgets of operators running slim margins. Although LEO competition is pushing tariffs down, new antennas and network-management software still require capital that many small firms postpone, slowing penetration of the boat and ship telematics market.

Maritime Cyber-Risk Exposure

Integrated bridges blend operational and information technology, widening attack surfaces for spoofing and malware. Documented AIS hacks show ships set off course or hidden from radar for hours, highlighting gaps in crew cyber skills. IMO guidelines now demand encryption and continuous monitoring, adding complexity and recurring cost that some operators view as burdensome.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Commercial Dominance Drives Defense Innovation

Commercial vessels accounted for 47.12% of the boat and ship telematics market share in 2025 as cargo lines adopted mandatory tracking and fuel-optimization suites. Higher bunker prices pushed owners to integrate weather-routing algorithms that saved up to 15% on voyage costs, converting telematics from compliance expense to a profit lever. The defense segment, though smaller, is expanding at an 11.02% CAGR as navies roll out uncrewed surface vessels that depend on encrypted sensor backhauls. Thales’ Tacticos system now equips 25 navies, illustrating how military demand accelerates secure data-fusion capabilities. Passenger and leisure craft follow suit, with insurers offering lower premiums for connected yachts, deepening consumer adoption.

The boat and ship telematics market size for commercial operators is projected to advance steadily as ports enforce digital document exchange and emissions logging. Meanwhile, defense budgets earmark funds for integrated threat detection, propelling the specialized software layer. Recreational adoption remains fragmented yet is gathering pace as platforms like Yacht Sentinel report thousands of new activations each quarter.

By Function: Communication Leads While Analytics Surges

Communication services held 37.88% of the boat and ship telematics market revenue in 2025, reflecting the basic need for dependable links between ship and shore. Hybrid terminals that auto-switch among L-band, Ku-band, and cellular channels minimize blackouts and cost spikes. Data-collection and analytics functions display the fastest 9.87% CAGR due to AI modules that transform raw engine feeds into predictive alerts. Kongsberg Digital’s Vessel Insight funnels signals from hundreds of sensors into unified dashboards that chart fuel, trim, and maintenance risk. Navigation and monitoring tools piggyback on this expanding data pipe, driving multipurpose deployment aboard workboats and cruise ships.

Elevated fuel standards will continue to shift spending toward analytics that fine-tune hull and route performance. As a result, the boat and ship telematics market size devoted to advanced analytics is on track to double before 2031, squeezing pure-play communication margins and nudging suppliers toward value-added software.

By Component: Hardware Dominance Challenged by Software Innovation

Hardware represented 58.95% of the boat and ship telematics market outlays in 2025, covering antennas, multi-band modems, and rugged sensors. Yet software subscriptions are rising 8.98% annually as fleet managers opt for cloud updates rather than periodic hardware swaps. KVH’s TracNet Coastal delivers 300 Mbps cellular speeds paired with dollar-per-GB pricing, underscoring how smarter devices lower data barriers and push owners further into the boat and ship telematics market. Sensor advances enable real-time hull stress and emissions tracking with minimal power draw, paving the way for smaller vessels to adopt previously high-end capabilities.

Software-defined functions now unlock over-the-air upgrades that extend equipment life. Consequently, vendors bundle SaaS licenses with terminal leasing, protecting margins while distributing acquisition costs across multiyear agreements.

By Vessel Type: Cargo Ships Lead While Workboats Accelerate

Cargo and container ships commanded 43.35% of the boat and ship telematics market revenue in 2025 because their scale can absorb capital costs, and regulatory stakes remain highest. ALBIS V-PER weather routing cut fuel burn by 15%, confirming ROI and reinforcing leadership. Workboats and offshore support vessels track the fastest 8.55% CAGR due to dynamic positioning rules in the offshore energy sector. Predictive analytics reduces downtime on high-day-rate assets, justifying quick payback for advanced telematics.

Tanker owners focus on cargo-temperature and hull-stress sensors that integrate with navigation suites, whereas cruise lines deploy 5G private networks for passenger Wi-Fi and engine diagnostics. Recreational craft connects through simplified mobile apps such as Seanapps, which reported 15,000 boats online in 2024, signaling an untapped long-tail market.

By Communication Technology: Satellite Leadership Strengthens

Satellite links supplied 54.62% of the boat and ship telematics market revenue in 2025 and are projected to expand at 10.98% CAGR as LEO constellations fill polar and mid-ocean gaps. Learnmarine notes that new “Recognized Mobile Satellite Service” options have doubled since 2023, driving price competition. Near-shore operators hand off to 4G and 5G to curb costs.

Vodafone Maritime Mobility now blankets 93% of world coastlines with automated switching that preserves session integrity for telematics streams. Shore-to-ship 5G trials in Riga proved stable video links 30 NM from port, opening pathways for remote inspections at a fraction of satellite tariffs.

Geography Analysis

Asia-Pacific retained the largest 36.55% of the boat and ship telematics market share in 2025 as China’s RCEP-aligned digital transformation and Singapore’s smart-port investments made connected-vessel capabilities a de facto operating standard. Public-private projects link 5G coastal corridors with low-earth-orbit satellites, giving fleets continuous coverage from berth to mid-ocean and supporting real-time fuel-efficiency apps that cut bunker consumption by up to 15%. Japan and South Korea pilot autonomous coastal carriers that need sub-50 ms latency, adding demand for multi-sensor gateways and cyber-secure clouds. Australia and New Zealand reinforce the region’s leadership by mandating emissions-tracking uploads before port entry, which pushes smaller operators to adopt subscription-based telematics platforms. As a result, Asia-Pacific's boat and ship telematics market size is projected to widen its lead through 2030, even as growth moderates from double-digit rates.

The Middle East and Africa post the fastest 9.95% CAGR to 2031, helped by the UAE’s AI-enabled logistics corridors and Saudi Arabia’s Vision 2030 spending on new deep-water terminals. Gulf operators also leverage hybrid satellite 5G bundles that cut data costs by 40%, making enterprise-grade connectivity accessible to midsize fleets. In Africa, South Africa and Nigeria deploy coastal surveillance nets that blend AIS, radar, and drone feeds, stimulating demand for modular hardware kits that integrate with cloud analytics. As oil majors resume offshore exploration, workboat owners across Angola and Ghana adopt predictive-maintenance software to minimize downtime in remote fields.

Europe and North America show steady replacement demand as regulations tighten on carbon intensity and cyber-risk management. Norway’s autonomous-tug trials and Baltic 5G ferry corridors keep the regions at the forefront of technology pilots, even though overall spending rises at mid-single-digit rates. South America gradually scales telematics as Brazilian port-community systems require voyage-data uploads before pilotage, while Pacific Alliance nations co-invest in satellite gateways that improve coverage along high-current routes. Collectively, these trailing regions ensure the boat and ship telematics market continues to diversify geographically, reducing over-reliance on any single trade lane and encouraging vendors to localize support hubs and pricing models.

Regulatory Landscape

The regulatory baseline for vessel tracking continues to rely on IMO instruments, including SOLAS requirements and the LRIT performance standard (MSC.263(84)/Rev.1), which keep international-trading fleets on mandated identity and position reporting workflows. In December 2024, the IMO adopted Resolution MSC.570(109) updating performance standards for a universal shipborne AIS, strengthening equipment and message-handling expectations that flow into telematics terminal specifications and bridge integration.

In 2026, regulatory pressure extended beyond position reporting to digital interoperability, emissions monitoring, and cybersecurity. The European Commission adopted Implementing Regulation (EU) 2026/394, defining functional and technical specifications for the FuelEU database, and Implementing Regulation (EU) 2026/1233, specifying the common addressing service supporting the European Maritime Single Window environment created under Regulation (EU) 2019/1239. In the United States, the US Coast Guard set cybersecurity plan training requirements effective January 2026 (33 CFR 101.650), pushing operators to embed security controls, logging, and personnel training into telematics-enabled operational processes. The IMO also progressed work in May 2026 to add VDES into its framework (with final adoption steps noted), which points to higher-bandwidth VHF data pathways that can influence ship-to-shore connectivity architectures.

Value Chain Analysis

The boat and ship telematics value chain begins with onboard hardware (multi-band satellite/cellular terminals, antennas, gateways, and sensors) and extends into edge software that normalizes data for shipboard networks before backhauling through satellite operators and terrestrial cellular providers. Connectivity management and IoT platforms then handle device identity, provisioning, and roaming across sea, port, and inland networks, while cloud layers deliver analytics, dashboards, and APIs for route optimization, predictive maintenance, and compliance reporting. System integrators, OEMs, and class-aligned service partners support deployments during newbuild outfitting or scheduled port calls, with recurring revenues concentrated in bandwidth plans, software subscriptions, cybersecurity services, and lifecycle support contracts.

Ports and logistics nodes increasingly affect the downstream chain through Port Community Systems (PCS) that centralize electronic exchange among carriers, terminals, and authorities. This elevates the need for standardized data interfaces and addressable digital reporting. A.P. Moller - Maersk’s May 2025 OneWireless rollout across about 450 vessels illustrates this integration, combining NB-IoT, Cat-M, and LTE with private wireless and an operator-agnostic switching approach supported by partners including Nokia (private wireless infrastructure and network management), Onomondo (cellular switching between vessel private LTE and public networks), and Zededa (edge management for remote application deployment). On the port-side asset visibility layer, Netmore Group and Zenze partnered in March 2025 to deploy LoRaWAN networks for cargo and asset monitoring at ports and terminals, linking vessel telematics data flows with terminal visibility networks where relevant.

Competitive Landscape

Competition remains moderate. Companies like Kongsberg Digital, ABB Marine & Ports, and Wärtsilä Voyage offer integrated stacks from sensors to cloud analytics that earn long-term service contracts. Inmarsat Maritime, Iridium, and ORBCOMM defend bandwidth territory by pairing VSAT upgrades with value-added data services. Satlink’s purchase of Xeos Technologies and AST Networks’ purchase of Reygar signal consolidation aimed at controlling end-to-end telematics workflows.

Strategic alliances center on AI engines and hybrid connectivity. Kongsberg’s Vessel Insight adds third-party apps through an open marketplace, letting owners mix route optimization with regulatory dashboards in one subscription. ZeroNorth’s 2024 merger with Alpha Ori fused fuel-efficiency algorithms with onboard IoT bridges to manage over 4,500 ships, underscoring a trend toward ecosystem scale. Emerging entrants focus on recreational craft, offering smartphone-centric kits that link bilge alarms, batteries, and geofences at consumer price points.

5G and LEO systems reshape economics by lowering per-megabyte costs, prompting incumbents to pivot beyond pure connectivity. Iridium’s Certus portfolio now bundles cybersecurity and weather routing, while ABB integrates the former DTN weather business to enrich voyage planning. Demonstrations of autonomous tugboats in Norway and remotely operated ferries in Japan showcase the premium value of resilient, high-bandwidth networks that only advanced telematics can supply.

Boat And Ship Telematics Industry Leaders

Kongsberg Digital Ltd.

ABB Marine & Ports (ABB Ltd.)

Wartsila Corporation

Marlink SAS

Inmarsat Global Limited

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Compliance-driven digital reporting and standardized ship-to-shore data exchange create room for platforms that combine connectivity, identity management, and regulatory-grade data products into a single workflow. In the EU, demand is shaped by the European Maritime Single Window environment under Regulation (EU) 2019/1239, supported by Implementing Regulation (EU) 2026/1233 on a common addressing service, and Implementing Regulation (EU) 2026/394 for FuelEU database specifications. Together, these frameworks increase the pull for telematics solutions that can package voyage, port-call, and emissions-related datasets into interoperable submissions. Vendors that offer pre-integrated connectors to port and authority systems, along with auditable data lineage and automated reporting, have a clearer route to enterprise deployment beyond standalone tracking.

Cyber resilience and onboard interoperability standards are also widening the addressable software and integration layer. IACS Unified Requirements E26 and E27 apply to ships contracted for construction on or after July 1, 2024, tightening cybersecurity-by-design expectations for onboard networks that telematics devices connect into, and ISO 4891:2024 provides interoperability requirements for smart ship applications and onboard IoT data collection. In parallel, crew connectivity requirements create near-term spend around bandwidth optimization and onboard Wi-Fi management: in March 2026 the UK published guidance (MGN 707 (M)) and legislation (2026 No. 260) covering social connectivity facilities for seafarers on UK-flagged ships. This strengthens the business case for hybrid satellite-cellular architectures and policy-based traffic management that can segregate welfare traffic from operational telemetry. Autonomous and remotely controlled vessel programs provide another adoption pathway, supported by the IMO Maritime Safety Committee’s non-mandatory MASS Code (MSC.595(111)) adopted in May 2026, which supports integration of remote and autonomous operations where secure, continuous telemetry, authenticated communications, and edge-to-cloud control loops become core requirements.

Recent Industry Developments

- July 2026: Wartsila signed a five-year Lifecycle Agreement with Ireland-based Pardus Energy to strengthen maintenance predictability and operational reliability for the FSRU vessel TURQUOISE P, with the agreement effective from April 2026. The scope reinforces the shift toward long-term remote support and data-driven maintenance models that rely on continuous vessel connectivity and telemetry.

- December 2025: ABB Marine and Ports was selected by Rotterdam Shore Power (a joint venture of the Port of Rotterdam and Eneco) to engineer and construct shore power systems covering 35 connection points across three deep-sea container terminals. The project expands electrification infrastructure at a major port complex and increases the need for integrated monitoring, control, and digital interfaces that tie berth operations to vessel and terminal systems.

- June 2024: ABB acquired DTN’s weather-routing unit, adding Routeguard services into its marine digital suite. The deal strengthened ABB’s voyage optimization and decision-support stack, tightening integration between onboard data capture, routing analytics, and shore-side fleet performance management.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue generated from telematics used on boats and ships to track, communicate, monitor condition, and support navigation and safety, using connected hardware, software, and related services. We measure values at the solution level where telematics is delivered to the vessel operator or owner.

Scope exclusions: We exclude general shipbuilding electronics that do not transmit data off-vessel and pure port infrastructure systems that are not installed or licensed for vessel use.

Segmentation Overview

- By Application

- Commercial

- Private/Recreational

- Defense and Security

- By Function

- Navigation

- Communication

- Monitoring and Diagnostics

- Data Collection and Analytics

- By Component

- Hardware

- Sensors and Antennas

- On-board Terminals

- Software and Platforms

- Hardware

- By Vessel Type

- Cargo and Container Ships

- Tankers

- Passenger and Cruise

- Workboats and Offshore Support

- Yachts & Leisure Craft

- By Communication Technology

- Satellite (LEO/MEO/GEO)

- Cellular/5G

- Hybrid and Mesh Networks

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Indonesia

- Malaysia

- Australia

- New Zealand

- Rest of Asia-Pacific

- Middle East & Africa

- Saudi Arabia

- United Arab Emirates

- Egypt

- Turkey

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the guardrails of the market and to keep assumptions realistic across regions and vessel categories. We relied on public shipping and fleet signals, then cross-checked them with technology adoption commentary from credible maritime sources.

Common inputs came from sources such as IMO publications (including safety and tracking-related requirements), ITU references on maritime communications, UN Comtrade trade statistics for relevant equipment flows, and UNCTAD maritime transport indicators. We also used patent databases to understand where innovation is focused, along with company filings, investor presentations, and association websites to sanity check commercial narratives. Some market mapping and financial normalization were supported using a paid subscription for company financials and a paid subscription for shipment-level import and export records where available. The examples listed here are not exhaustive, and many other sources were used for data collection, validation, and clarification during the work.

Primary Interviews and Surveys

Primary work focused on confirming what is actually being purchased as telematics on vessels, and how pricing is packaged (device sales, software licenses, and recurring connectivity and service fees). We spoke with stakeholders across commercial fleets, passenger and leisure operators, and solution ecosystem participants, then tested regional assumptions across APAC, EMEA, and the Americas so the demand picture was not driven by a single trade lane or vessel mix.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 14% | APAC: 50% |

| Mid tier: 57% | Functional/Unit leaders: 31% | EMEA: 29% |

| Smaller Players: 14% | Managers: 55% | Americas: 21% |

Market-Sizing & Forecasting

Sizing started with a top-down build where the addressable vessel base and operating activity were translated into a telematics spending pool, then split by typical install and subscription behavior. To keep the math grounded, we used practical inputs such as global fleet counts by vessel type, retrofit versus new-install mix, average devices per vessel, recurring service attach rates, and typical annual pricing ranges for software and connectivity.

After shaping the demand pool, we cross-checked results using selective bottom-up approximations, such as sampled average selling price times estimated shipment volume for key hardware classes, and a reasonableness check against recurring revenue intensity for subscribed fleets. Where direct volume evidence was thin, gaps were handled by applying conservative penetration bands validated through interviews, then stress-tested so one optimistic assumption did not drive the total.

For forecasting, scenario analysis was used, supported by simple multivariate relationships between telematics demand and indicators like seaborne trade activity, fuel and emissions efficiency programs, satellite coverage availability, and safety compliance adoption. The final trajectory was adjusted only when multiple signals moved together, which keeps the forecast explainable on a client call and repeatable during updates.

Data Validation & Update Cycle

Validation was done through step-by-step checks across data sources, interview feedback, and model behavior across regions. We compared outputs with independent signals such as vessel activity trends, known adoption patterns for tracking and communication systems, and the implied average spend per connected vessel, then investigated any large jumps before sign-off.

Variance checks were run at the region and vessel-type level so a single geography did not distort the global total. If primary respondents flagged a clear mismatch in pricing, attach rates, or installation cycles, the relevant assumptions were revisited and the related model parts recalculated. Reports are refreshed annually, with interim updates when material events change demand conditions, and a final pre-delivery pass is done so clients receive the latest view.

Mordor Intelligence's Boat and Ship Telematics Market Size Measured Against Other Published Estimates

Published market values for boat and ship telematics can differ even when they appear to cover the same use cases, since the included revenue streams and the base year used can shift the total. We also see differences when studies rely more on broad technology spend narratives versus vessel-linked demand drivers that can be checked against fleet activity.

The main gap comes from whether recurring connectivity and software platform fees are counted alongside device revenue, where Mordor Intelligence includes telematics hardware plus software and services tied to vessel operation, then validates the implied spend per active vessel. Totals can also change when a study includes port-side digital systems into the same bucket, applies aggressive penetration for retrofits, or uses different currency timing and inflation treatment for multi-year comparisons.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.56 B (2025) | |

| Industry Publisher A | USD 6.71 B (2025) | Often uses a wider marine telematics scope with service bundles that can include adjacent onboard digital services, and the base-year mix of passenger, defense, and commercial applications can be weighted differently. |

| Research Portal B | USD 5.60 B (2023) | Uses an earlier base year, and the page shows internally inconsistent size statements, which can happen when definitions or revisions are not aligned across sections, leading to a different starting point for the growth curve. |

The spread across sources is mainly explained by scope choices and how recurring service revenue is treated over time, not by a single simple math difference. By anchoring assumptions to vessel counts, install behavior, and realistic pricing progression, the estimate stays traceable to clear inputs and can be refreshed without changing the logic each year.

Key Questions Answered in the Report

What is the current size of the boat and ship telematics market?

The market was valued at USD 6.08 billion in 2026 and is on track to reach USD 9.51 billion by 2031.

Which region holds the largest share of the boat and ship telematics market?

Asia-Pacific led in 2025 with 36.55% of global revenue, driven by smart-port projects and RCEP-aligned digital upgrades.

Where is the fastest growth expected through 2031?

The Middle East and Africa are forecast to expand at a 9.95% CAGR as AI-enabled logistics corridors and new deep-water terminals come online.

Which vessel segment is adopting telematics the quickest?

Workboats and offshore support vessels show the highest adoption momentum, advancing at an 8.55% CAGR thanks to dynamic-positioning and predictive-maintenance needs.

What payback can operators expect from telematics investments?

Integrated weather-routing and fuel-optimization platforms can reduce bunker consumption by up to 15%, delivering measurable cost savings alongside regulatory compliance benefits.

Page last updated on: