Blind Spot Monitor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

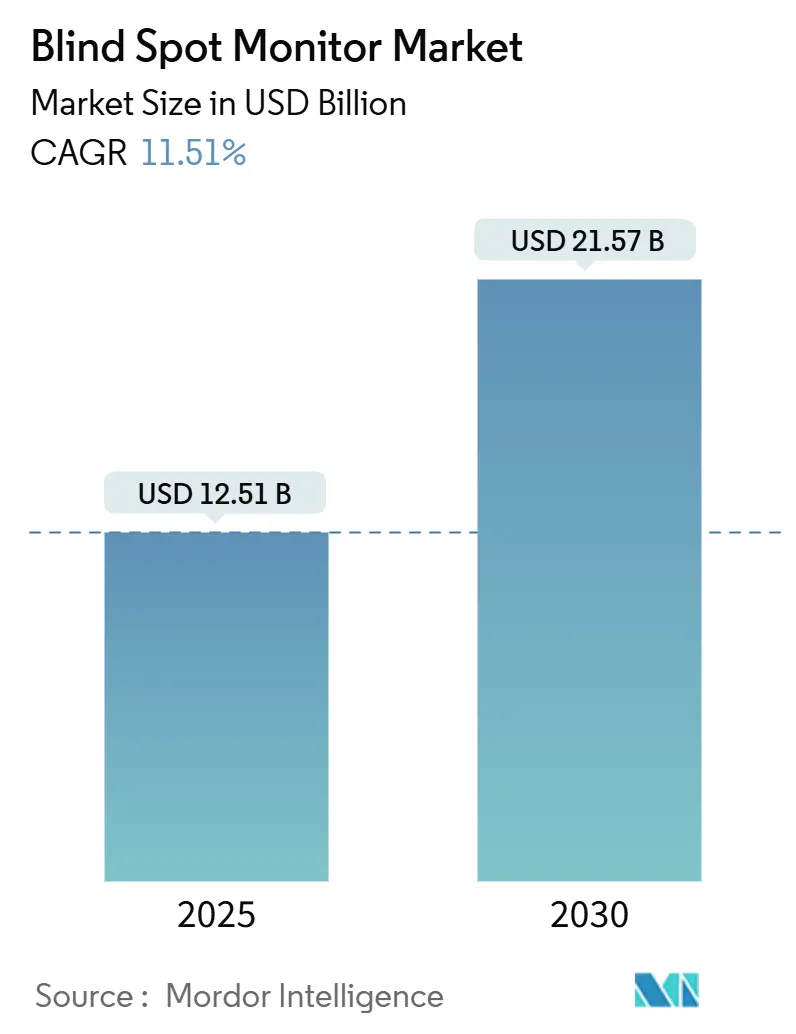

| Market Size (2025) | USD 12.51 Billion |

| Market Size (2030) | USD 21.57 Billion |

| Growth Rate (2025 - 2030) | 11.51% CAGR |

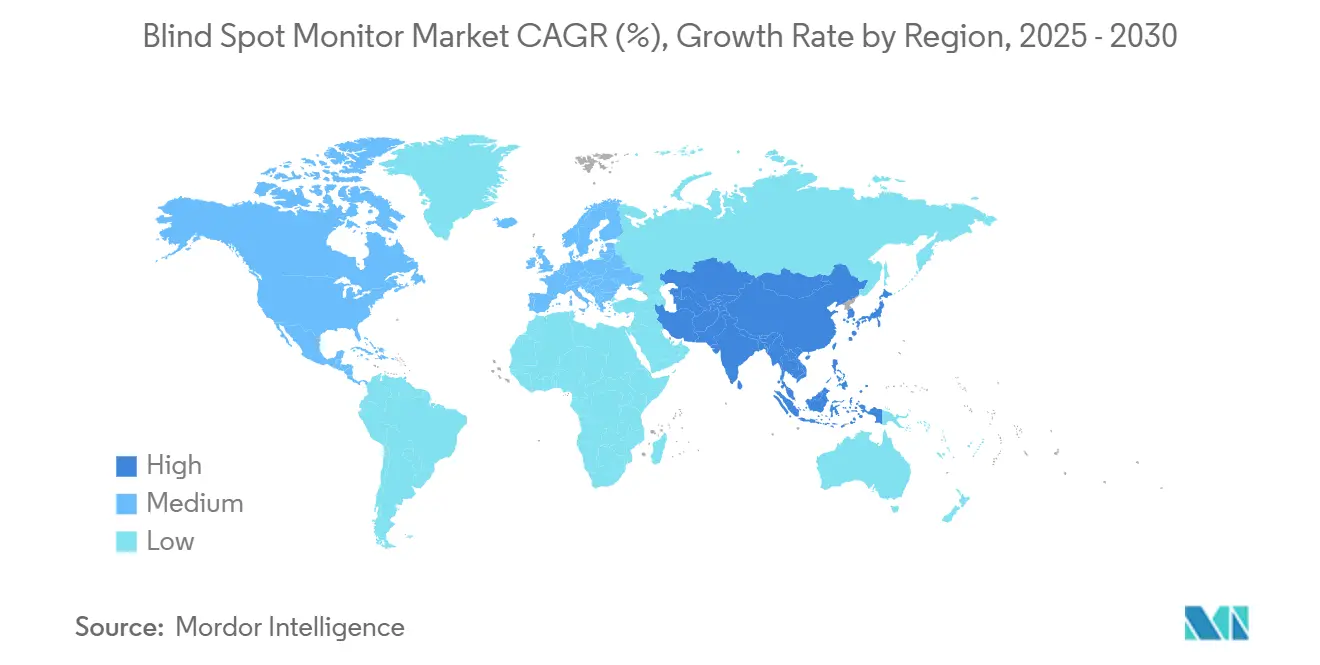

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Blind Spot Monitor Market Analysis by Mordor Intelligence

The Blind Spot Monitor market size stood at USD 12.51 billion in 2025 and is forecast to expand at an 11.51% CAGR, reaching USD 21.57 billion by 2030. Regulatory mandates in the European Union, the United States, and China are converting blind-spot detection from an optional add-on into compulsory safety infrastructure, accelerating original-equipment integration and reshaping procurement strategies. Automakers now favor sensor-fusion platforms that blend radar, camera, and ultrasonic inputs, allowing multiple advanced driver-assistance functions to run on a single processor and lowering per-vehicle costs. Semiconductor advances have pushed radar and automotive-grade CMOS camera modules below key price thresholds, encouraging volume adoption across mid-segment vehicles.

Key Report Takeaways

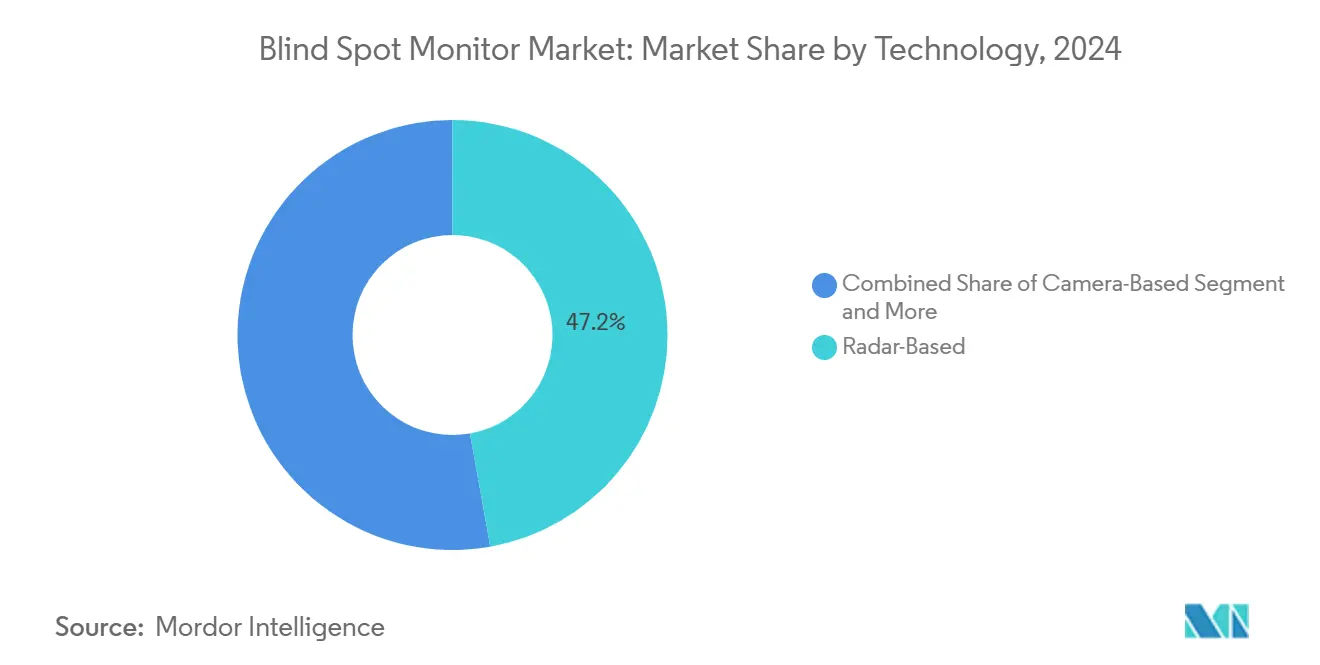

- By technology, radar-based systems led with 47.15% of the Blind Spot Monitor market share in 2024; camera-based solutions are projected to advance at a 14.05% CAGR through 2030.

- By product type, blind-spot detection systems accounted for 32.46% of the Blind Spot Monitor market size in 2024, while surround-view systems are set to grow at a 13.27% CAGR to 2030.

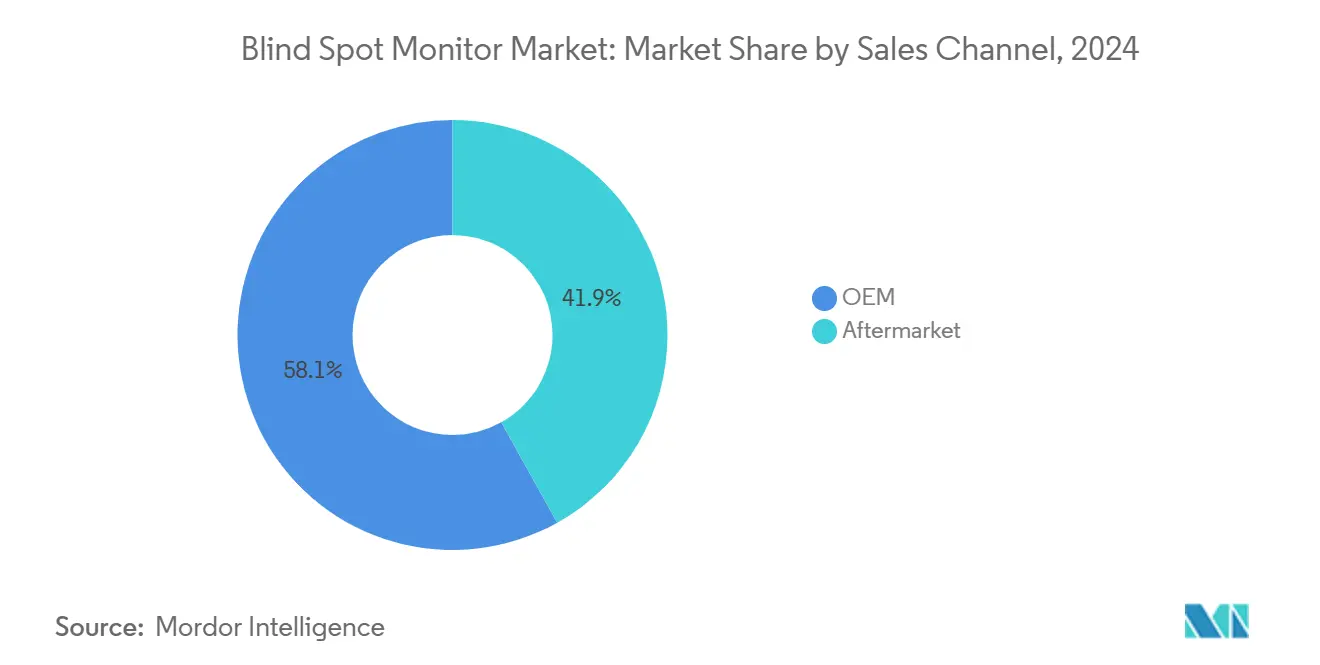

- By sales channel, original-equipment installations captured 58.11% of the Blind Spot Monitor market share in 2024; the aftermarket channel is forecast to post a 12.74% CAGR.

- By vehicle type, passenger vehicles dominated with a 74.22% of the Blind Spot Monitor market share in 2024, whereas medium and heavy-duty trucks are poised for a 13.68% CAGR.

- By geography, North America held 30.16% of the Blind Spot Monitor market share in 2024, yet Asia-Pacific is expected to log a 12.18% CAGR through 2030.

Global Blind Spot Monitor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter Global Safety Mandates | +2.8% | Global with EU and China leading | Medium term (2-4 years) |

| Cost Decline in Sensors | +2.1% | Global, Asia-Pacific manufacturing advantage | Short term (≤ 2 years) |

| OEMs Bundling BSM Mid-Segment | +1.9% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Surge in Autonomous Vehicle Production | +1.7% | APAC core, spill-over to North America and EU | Long term (≥ 4 years) |

| Insurance Rebates for ADAS Fleets | +1.4% | North America and EU, emerging in APAC | Medium term (2-4 years) |

| V2X-Enabled Cooperative Perception | +1.2% | EU and China pilot regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Stricter Global Safety Mandates for ADAS

Multiregional regulation is transforming the Blind Spot Monitor market by eliminating discretionary fitment and synchronizing technical specifications across continents. The EU General Safety Regulation now obligates Blind-Spot Information Systems on all new M2, M3, N2, and N3 vehicles, while China’s GB 15084-2022 applies comparable requirements to commercial trucks [1]“General Safety Regulation 2019/2144,” European Commission, ec.europa.eu. NHTSA’s refresh of the United States New Car Assessment Program scoring makes blind-spot performance a weighted factor, effectively turning compliance into a prerequisite for five-star safety ratings. This convergence grants suppliers scale economies, accelerates platform reuse, and forces late-adopting OEMs to meet a looming compliance cliff. Commercial fleets face licensing and operational penalties for non-compliance, which pulls forward demand in heavy-duty segments. Collectively, mandates lift baseline sensor content per vehicle and push the Blind Spot Monitor market toward standardized feature sets.

Rapid Cost Decline and Performance Gains in Radar/Camera Sensors

System-on-chip radar designs now integrate analog front ends and digital signal processors into a single package, cutting component counts by up to 60% and lowering bill-of-materials costs, while automotive CMOS imagers have fallen below key per-unit price thresholds. These trends compress price ceilings, making BSM economically viable in compact cars sold across Asia-Pacific. Enhanced image-processing algorithms also allow camera-only blind-spot coverage under most driving conditions, narrowing the performance gap with radar. Suppliers leveraging 300-mm fab capacity in Taiwan and South Korea can meet surging demand without significant capital bottlenecks. As unit economics improve, profit margins stabilize even as ASPs trend downward, supporting broader deployment in the Blind Spot Monitor market.

Growing OEM Bundling of BSM in Mid-Segment Vehicles

Toyota, Honda, and Hyundai standardized blind-spot monitoring in several volume models during 2024, transforming a once-premium option into a buyer expectation [2]“ADAS Technology Strategy Brief,” MITRE Corporation, mitre.org. Bundling multiple ADAS features onto shared processors spreads development costs and simplifies homologation. Insurance rebates further nudge consumers toward BSM-equipped trims, creating a virtuous cycle of uptake. Platform-sharing alliances among OEMs support common wiring harnesses and sensor placements, enabling cost control across regional variants. As bundling becomes the norm, differentiation shifts from basic presence of BSM to its sensor-fusion accuracy and over-the-air update roadmap, escalating software importance in the Blind Spot Monitor market.

Surge in Autonomous and Electric Vehicle Production Boosting ADAS Sensor Content

Electric-vehicle platforms provide abundant electrical bandwidth and centralized compute nodes, encouraging higher sensor counts per vehicle. BYD allocated USD 14 billion to smart-driving R&D, anchoring blind-spot modules as part of its L2+ autonomy stack. Autonomous test programs demand redundant corner radars and fisheye cameras, each covering blind zones previously handled by single-point sensors, thereby lifting average selling prices for BSM packages. As autonomy matures, technology cascades into mainstream trims, reinforcing sensor-fusion architectures and expanding addressable volume in the Blind Spot Monitor market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High System Cost | -1.8% | APAC emerging markets, South America, Africa | Short term (≤ 2 years) |

| Sensor Degradation In Fog | -1.2% | Northern regions and mountainous areas | Medium term (2-4 years) |

| 77 GHz Spectrum Congestion | -0.9% | Dense urban zones worldwide | Medium term (2-4 years) |

| mmWave Chipset Supply Disruptions | -0.7% | Global, acute on United States-China routes | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High System Cost in Price-Sensitive Markets

Entry-level vehicles in India, Brazil, and parts of Africa still sell on razor-thin margins, adding USD 200-400 to accommodate BSM hardware challenges, affordability. Local content rules and import tariffs on electronics inflate costs further, preventing OEMs from meeting universal safety goals without eroding profits [3]“Pre-Crash Safety Technologies Cost Analysis,” U.S. Department of Transportation, transportation.gov. Suppliers attempt regional sourcing and reduced-feature designs, yet lower-cost variants sometimes fail to meet EU-style performance thresholds. Until broader economies of scale emerge, this restraint tempers Blind Spot Monitor market penetration in the lowest-priced segments.

Sensor-Performance Degradation in Snow/Fog Causing False Alerts

Snow accumulation on radar housings and heavy fog that obscures cameras drive up false-alert rates, eroding driver trust. In Canada, Alaska, and Nordic nations, adverse weather persists for several months each year, prompting some operators to disable BSM functions. Although machine-learning-based environmental classifiers reduce nuisance warnings, additional processing overhead escalates cost and power draw. The need for self-heating radomes or hydrophobic lens coatings adds incremental complexity, partially offsetting the cost decline benefits in the Blind Spot Monitor market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Radar Dominance Faces Camera-Based Disruption

Radar modules supplied the backbone of blind-spot functions and captured 47.15% of 2024 revenue, making them the single largest technology contributor to the blind spot monitor market share. High-resolution chipsets maintain performance in rain and darkness, keeping them indispensable for heavy-duty fleets. Yet camera-centric systems are expected to log a 14.05% CAGR, leveraging AI object classification to deliver lane-change assist, traffic-sign recognition, and driver monitoring from one image sensor. This convergence compresses incremental cost per function and accelerates OEM migration to vision-heavy architectures. Hybrid thermal-radar prototypes from Magna illustrate future sensor-fusion paths that promise redundancy without escalating hardware counts. Over the forecast window, the blind spot monitor market size for camera solutions is projected to approach that of radar as software maturity closes the weather-resilience gap and economies of scale cut unit prices further.

Technological evolution also shifts supplier negotiating power. Radar stalwarts must prove superior value through micro-doppler classification and interference cancellation, while camera vendors gain leverage by bundling multi-purpose perception algorithms. The ensuing competition intensifies price compression yet fosters innovation, reinforcing a dynamic where component and software quality outrank raw hardware specs. This transition will shape design wins, production allocation, and capital investment priorities across the Blind Spot Monitor industry.

By Product Type: Detection Systems Anchor 360-Degree Suites

Core blind-spot detection modules retained 32.46% of 2024 sales, securing their place as the foundational layer of the Blind Spot Monitor market size. Their limited sensor footprint and proven reliability align well with mid-segment price points, ensuring steady pull from mainstream passenger cars. Surround-view systems, however, are forecast to clock a 13.27% CAGR, benefiting from integration that folds parking assistance, cross-traffic alert, and lane-merge support into a single 360-degree camera network. OEM demand for dashboard simplicity drives consolidation, so future models will likely merge detection, lane-change assist, and rear-collision warning into unified control units.

Suppliers that deliver scalable software stacks gain an edge as automakers seek to future-proof hardware with over-the-air feature unlocks. Continental’s spinoff of its aftermarket ADAS arm under the Aumovio brand underscores a shift toward modular kits that retrofit existing vehicles while satisfying OEM warranties. The Blind Spot Monitor market, therefore, balances legacy detection modules, prized for cost efficiency, with rapidly ascending surround-view suites, prized for functional breadth.

By Sales Channel: OEM Leads, Aftermarket Accelerates

Factory-installed systems accounted for 58.11% of the blind spot monitor market share in 2024, illustrating automakers’ preference for fully validated and warranty-compliant sensor suites. Regulatory enforcement at the vehicle approval stage leaves little room for post-sale adaptation, compelling OEMs to integrate compliant blind-spot technology on the assembly line. Nonetheless, the retrofit market is forecast to progress at a 12.74% CAGR, driven by fleets aiming to extend asset lifecycles while securing insurance benefits.

Aftermarket suppliers confront engineering challenges: sensor mounting points vary by model, and electronic control units often lack spare processing capacity. Yet agile product cycles and direct customer feedback let retrofit vendors iterate rapidly. Continental’s Aumovio approach packages modular BSM kits with cloud-based calibration tools, reducing installation times and broadening addressable vehicle classes. In parallel, regulatory bodies may accept certified retrofit devices for compliance in legacy trucks, offering a secondary tailwind to the Blind Spot Monitor market.

By Vehicle Type: Passenger Vehicle Scale Meets Commercial Urgency

Passenger vehicles generated 74.22% of the blind spot monitor market share in 2024, underscoring their sheer volume in global production. The blind spot monitor market benefits from models such as the Toyota Corolla and Hyundai Elantra standardizing BSM as part of multi-feature safety suites, expanding penetration into compact subclasses. Medium and heavy-duty trucks, however, are on track for a 13.68% CAGR, propelled by stringent fleet-safety mandates and measurable insurance savings.

Commercial platforms need extended detection zones and robust housings to survive vibration and debris exposure. Integration with telematics back-ends allows fleet managers to audit system uptime and driver behavior, converting blind-spot metrics into risk-management dashboards. Euro NCAP’s decision to grade commercial-vehicle safety from 2026 elevates ADAS visibility in procurement decisions. As a result, the Blind Spot Monitor industry will see disproportionate revenue growth in the commercial class, even though absolute unit shipments remain higher in passenger segments.

Geography Analysis

North America controlled 30.16% of the blind spot monitor market share in 2024, buoyed by mature aftermarket networks and insurance programs that monetize collision-reduction data. Safety-rating revisions within the United States now assign greater weight to blind-spot performance, prompting OEMs to include the feature by default in new sedan and SUV trims. Yet semiconductor tariffs inflated input costs, compelling Tier-1s to secure non-Chinese mmWave silicon to protect delivery schedules, a shift that sharpened focus on supply-chain resilience.

Asia-Pacific is set for the fastest growth, projected at 12.18% CAGR, as China’s GB 15084-2022 mandates blind-spot capability in new commercial vehicles. BYD’s smart-driving investment and a vibrant domestic EV ecosystem amplify sensor demand, turning regional fabs into cost-leadership hubs. Japan and South Korea contribute advanced packaging and AI algorithm expertise, while Southeast Asian markets gradually adopt BSM on higher-trim imports, held back mainly by price constraints rather than consumer indifference.

Europe benefits from the EU General Safety Regulation, which requires blind-spot information systems across multiple vehicle classes from 2026. OEM engineering centers in Germany and France work closely with Tier-1s on radar-camera fusion benchmarks, feeding into Euro NCAP star-rating criteria. However, cost-competitive offerings from Asian suppliers intensify price pressure, pushing European vendors to anchor differentiation in software features such as adaptive waveform control and over-the-air parameter tuning. Together, these forces maintain Europe’s steady contribution to the global Blind Spot Monitor market while positioning Asia-Pacific as the upcoming volume engine.

Competitive Landscape

The Blind Spot Monitor market shows moderate concentration. Continental, Bosch, and Denso remain leading Tier-1s, yet face challengers such as Magna, Valeo, and startup Arbe Robotics that exploit software-defined radar and AI edge processing. Continental’s carve-out of Aumovio illustrates strategic bifurcation between OEM and retrofit channels, each demanding distinct product roadmaps.

Supply-chain robustness is emerging as a new competitive frontier. Denso signed long-term wafer capacity agreements with ROHM, ensuring preferential allocation during industry shortages, while startups in the United States partner with on-shore fabs to sidestep tariff exposure. Vendors that blend in-house silicon, robust software stacks, and global manufacturing footprints mitigate geopolitical risk and secure OEM confidence.

Future differentiation will revolve around lifecycle software monetization. Platforms capable of over-the-air functional expansion allow OEMs to upsell lane-change assist and cross-traffic alert after initial vehicle sale, generating recurring revenue. This software-centric trajectory redefines value capture, favoring suppliers able to maintain cybersecurity certifications and digital-twin validation models. Consequently, the Blind Spot Monitor market rewards players with end-to-end capability spanning custom ASICs, cloud analytics, and fleet management APIs.

Blind Spot Monitor Industry Leaders

Continental AG

Robert Bosch GmbH

Denso Corporation

Magna International Inc.

Valeo SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Stoneridge unveiled its next-generation MirrorEye MP II camera-monitor system for buses and rigid trucks, integrating Blind-Spot Information System and Moving-Off Information System functions.

- April 2025: The Tamil Nadu government launched an AI-driven driver-monitoring pilot on 500 buses to enhance operational safety.

- November 2024: Mercedes-Benz upgraded Active Parking Assist with PARKTRONIC, doubling parking speed capability to 4 km/h for upcoming models.

- November 2024: The United States Department of Transportation announced a 2026 overhaul of New Car Assessment Program star ratings, adding blind-spot assistance and pedestrian tests.

Global Blind Spot Monitor Market Report Scope

| Camera-Based |

| Radar-Based |

| Ultrasonic-Based |

| Blind Spot Detection System |

| Park Assist System |

| Backup Camera System |

| Surround View System |

| OEM |

| Aftermarket |

| Passenger Vehicle |

| Light Commercial Vehicle |

| Medium and Heavy-Duty Truck |

| Bus and Coaches |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| Spain | |

| Italy | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Technology | Camera-Based | |

| Radar-Based | ||

| Ultrasonic-Based | ||

| By Product Type | Blind Spot Detection System | |

| Park Assist System | ||

| Backup Camera System | ||

| Surround View System | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Vehicle Type | Passenger Vehicle | |

| Light Commercial Vehicle | ||

| Medium and Heavy-Duty Truck | ||

| Bus and Coaches | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| Spain | ||

| Italy | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the Blind Spot Monitor market in 2025?

The blind spot monitor market size reached USD 12.51 billion in 2025.

What CAGR is expected for blind-spot monitoring solutions through 2030?

Global revenue is projected to grow at an 11.51% CAGR from 2025 to 2030.

Which technology leads current sales?

Radar-based systems held 47.15% of 2024 revenue thanks to reliable all-weather performance.

Which vehicle class is adopting BSM fastest?

Medium and heavy-duty trucks are forecast to log a 13.68% CAGR as fleets chase insurance rebates and regulatory compliance.

Page last updated on: