Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

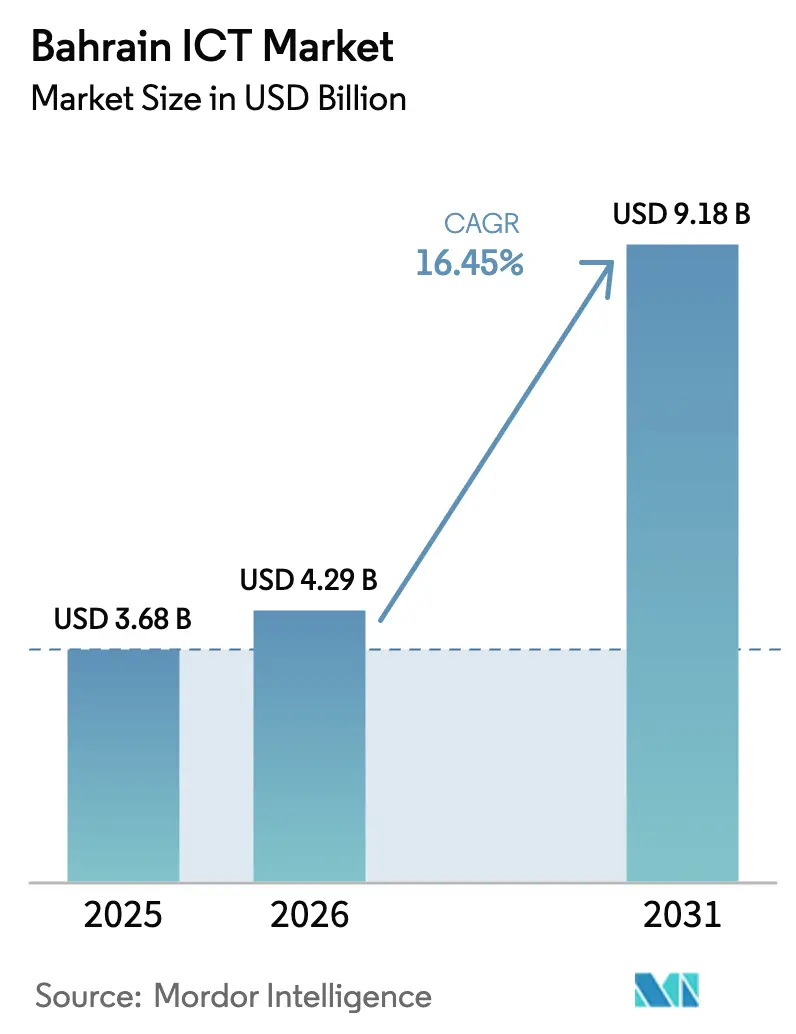

| Base Year Market Size (2025) | USD 3.68 Billion |

| Market Size (2026) | USD 4.29 Billion |

| Market Size (2031) | USD 9.18 Billion |

| Growth Rate (2026 - 2031) | 16.45% CAGR |

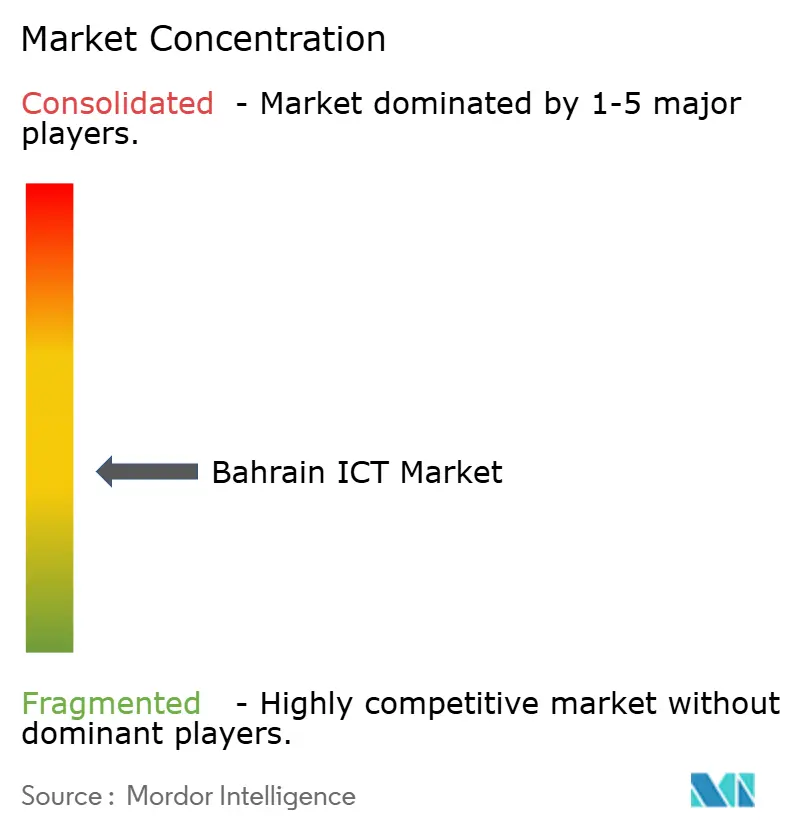

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bahrain ICT Market Analysis by Mordor Intelligence

Bahrain ICT market size in 2026 is estimated at USD 4.29 billion, growing from 2025 value of USD 3.68 billion with 2031 projections showing USD 9.18 billion, growing at 16.45% CAGR over 2026-2031. Strong 5G and fiber roll-outs, a Cloud-First public-sector mandate, and vibrant fintech regulation continue to pull international vendors into the Kingdom. Demand accelerates across hardware, software, IT services, and telecom services as enterprises pursue cost-efficient digitization while the government targets 100% household fiber coverage by 2026[2]Ookla, “Connectivity Insights with BNET Bahrain,” ookla.com. Investment momentum is reinforced by AWS, Microsoft, and Oracle regional cloud nodes, which guarantee data-residency compliance for regulated industries. Telecom operators leverage private 5G and edge architectures to unlock low-latency use cases in metals, banking, and logistics. Meanwhile, SME digital adoption gains pace, aided by Tamkeen grants and an expanding venture-capital pipeline that lifts local SaaS start-ups.

Key Report Takeaways

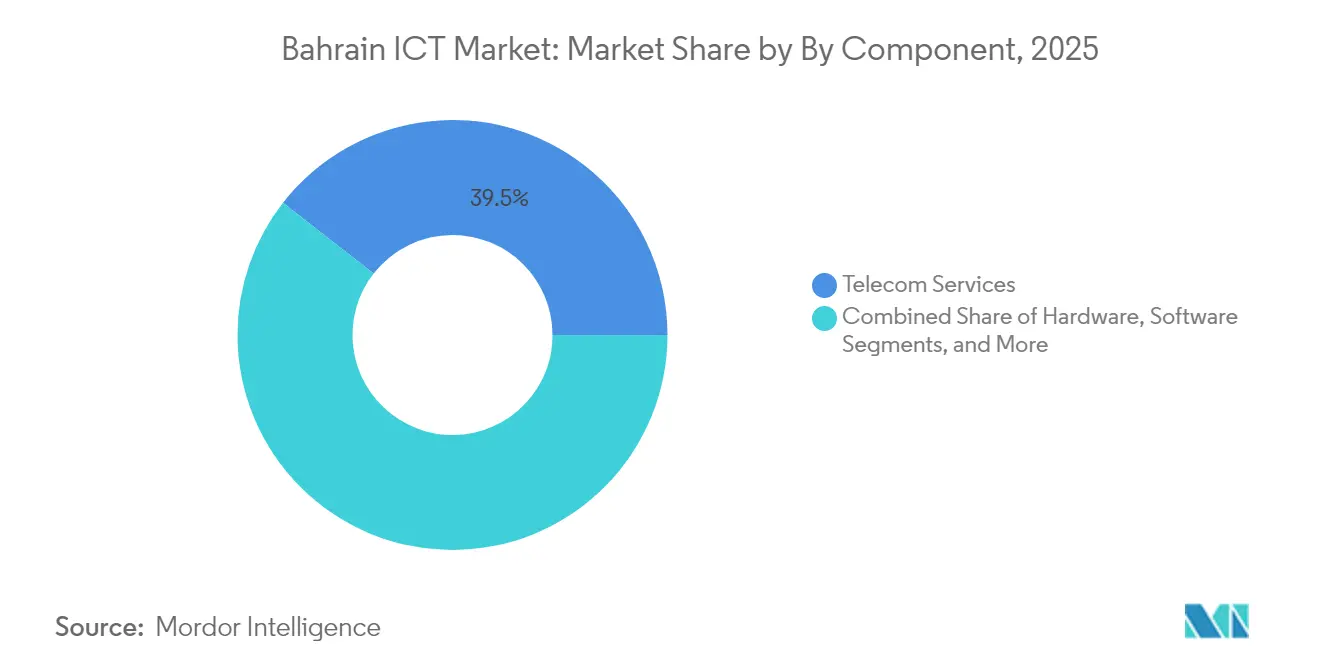

- By component, telecom services led with 39.46% of Bahrain ICT market share in 2025; IT services are on track for the fastest 10.92% CAGR through 2031.

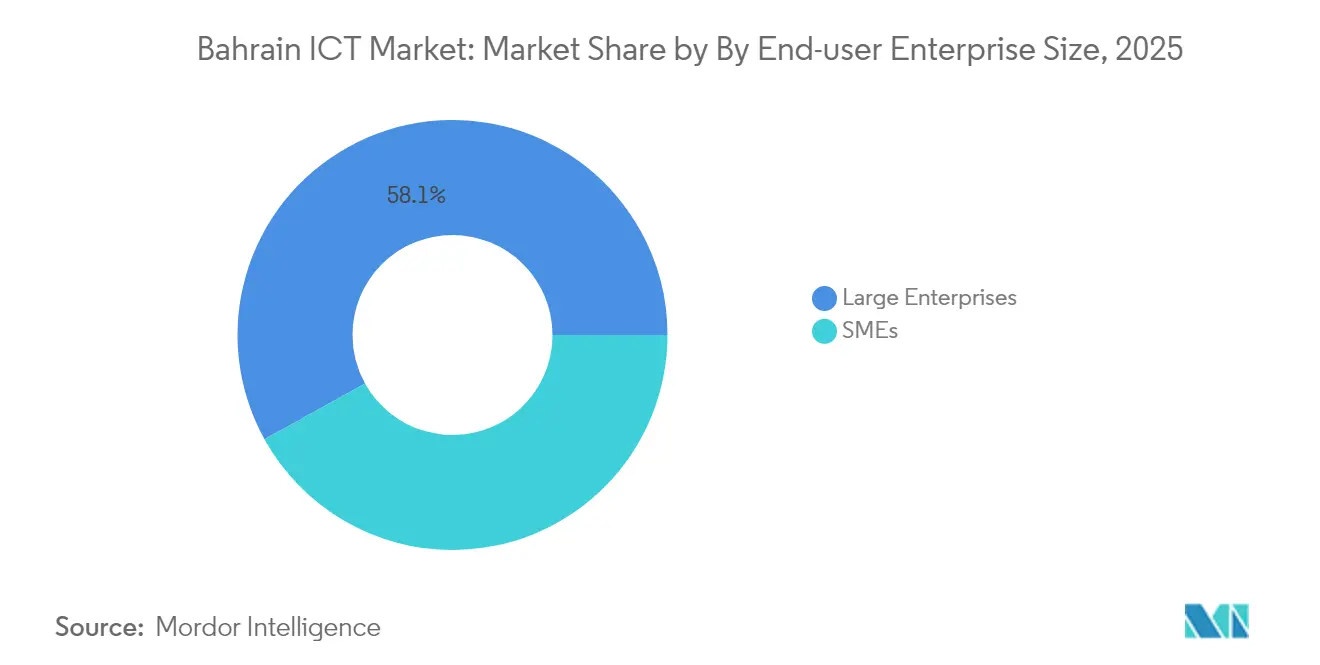

- By enterprise size, large enterprises controlled 58.05% of the Bahrain ICT market size in 2025, while SMEs are growing at a 11.85% CAGR to 2031.

- By industry vertical, BFSI captured 35.92% revenue share in 2025; retail and e-commerce is projected to expand at 13.25% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Bahrain ICT Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust 5G roll-out and fibre backhaul densification | +2.8% | National, with concentration in Manama and industrial zones | Medium term (2-4 years) |

| Cloud-First public-sector mandate accelerates enterprise migration | +2.1% | National, with spillover to GCC markets | Short term (≤ 2 years) |

| Fintech sandbox attracting foreign SaaS vendors | +1.7% | National, with regional expansion potential | Medium term (2-4 years) |

| National data-centre build-out lowers latency and improves data-residency compliance | +1.9% | National, with regional connectivity benefits | Long term (≥ 4 years) |

| Growing local cybersecurity talent pool through Tamkeen incentives | +1.4% | National, with regional talent export potential | Long term (≥ 4 years) |

| Mandated Arabic e-service accessibility standards (2025) spur GovTech spend | +1.2% | National, with potential GCC standardization | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Robust 5G Roll-out and Fibre Backhaul Densification

Private 5G networks already power Aluminium Bahrain’s smart-factory program after Batelco and Nokia completed the Kingdom’s first industrial 5G site in 2025. STC Bahrain’s 5G New Calling upgrade expands enterprise voice, while BNET is targeting 95% home fiber penetration by 2026, lifting average fixed speeds 2.5-fold. Ultra-low-latency links attract high-frequency traders and real-time IoT applications across ports and logistics hubs. Operators expect densification to cut edge-compute latency below 10 ms, sharpening Bahrain’s regional competitiveness.

Cloud-First public-sector mandate

More than 30% of ministries migrated core workloads to AWS since 2019, cutting project lead times by 60% and operating costs by up to 90%. Success stories in justice and education accelerate private-sector migrations, helped by training subsidies that address skill shortages. Sovereign data guarantees also reassure foreign banks servicing GCC clients from Manama. The Bahrain ICT market benefits as cloud spending displaces legacy capex and opens subscription opportunities for managed-service partners.

Fintech sandbox draws foreign SaaS vendors

The Central Bank grants nine-month testing windows for novel fintech solutions, recently licensing crypto custodian Fasset under updated virtual-asset rules[3]Central Bank of Bahrain, “Fasset Crypto License,” cbb.gov.bh . Bahrain FinTech Bay supplies co-working labs, while Open Banking rules enacted in 2024 spur API-driven payment and data-aggregation start-ups. International SaaS providers view the sandbox as a rapid-entry route to the wider GCC, boosting demand for cloud infrastructure, cybersecurity, and compliance tools.

National data-center build-out

Batelco’s Hamala facility offers 2.7 MW Tier III capacity over 12,236 m², providing low-latency colocation for banks and hyperscalers. Six submarine cables anchor Bahrain’s role as a Gulf interconnect node. Local hosting satisfies looming data-sovereignty mandates, cuts round-trip latency to <40 ms for key trading routes, and underpins edge AI and content-delivery services.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Concentrated telecom market keeps broadband tariffs high | -1.8% | Nationwide | Medium term (2-4 years) |

| Dependence on expatriate tech workforce | -1.3% | Nationwide, GCC spillover | Long term (≥ 4 years) |

| Limited venture-capital depth beyond seed stage | -1.0% | Nationwide | Medium term (2-4 years) |

| Rising cyber-risk premiums for SMEs | -0.9% | Nationwide | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Concentrated telecom market keeps broadband tariffs high

Three operators—Batelco, Zain, and STC—dominate connectivity, and wholesale reforms have yet to unlock material retail price competition despite BNET’s structural separation. Elevated tariffs inflate TCO for cloud migration, deterring smaller enterprises even as internet penetration tops 99%.

Dependence on expatriate tech workforce

Expat professionals fill many advanced cloud, DevOps, and cybersecurity roles; visa churn and regional salary competition create project continuity risks. Tamkeen’s SANS cybersecurity academy and Hope Talents programs aim to certify Bahrainis, yet near-term shortages persist.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Telecom services anchor digital ambitions

Telecom services held 39.46% Bahrain ICT market share in 2025 as nationwide 5G and fiber grids formed the backbone for data-intensive workloads. The Bahrain ICT market size for IT services is projected to rise at 10.92% CAGR, outpacing hardware and software as enterprises outsource cloud migrations, cybersecurity, and AI consulting. Operators explore tower carve-outs and wholesale fiber leasing to shift toward service-centric revenues. Meanwhile, hyperscalers stimulate local ISV ecosystems, driving software subscriptions across ERP, HR, and CX stacks. Hardware growth concentrates on data-center servers, edge appliances, and radio units, but margins compress amid global supply-chain normalization.

Second-order effects include growing cross-sell between managed security and connectivity, bolstering average revenue per enterprise line. Government e-service expansion—200+ digital services since 2007—creates predictable demand for application-maintenance contracts. Professional-services powerhouses such as KPMG leverage multi-year Microsoft alliances to bundle AI accelerators with compliance expertise.

By End-user Enterprise Size: SME digitization unlocks new revenue pools

Large enterprises controlled 58.05% of spending in 2025 thanks to deep IT budgets and regulatory compliance needs. Yet SMEs deliver the fastest 11.85% CAGR as Tamkeen covers up to 80% of cloud adoption costs and Al Waha Fund injects USD 100 million into early-stage tech funds. Ninety-four percent of Bahraini SMEs now use at least one digital sales channel, accelerating demand for SaaS accounting, POS, and cybersecurity bundles.

As digital maturity grows, SMEs pivot from single-cloud to multi-cloud for price arbitration and resilience, often via MSPs. Large enterprises pursue SAP S/4HANA transformations and zero-trust architectures to meet Central Bank cyber directives. The Bahrain ICT industry thus faces a dual-track opportunity: standardized SaaS for small businesses and bespoke integration for corporates.

By Industry Vertical: BFSI anchors, retail races ahead

BFSI accounted for 35.92% of 2025 outlays, reflecting 190 shared-service centers and progressive fintech governance. Open Banking APIs spark payments competition, while crypto custody rules draw blockchain start-ups. Retail and e-commerce posts 13.25% CAGR as consumers migrate online; omnichannel chains embrace AI-driven inventory and loyalty engines. Government agencies intensify citizen-service digitization, pushing secure ID and e-payment infrastructure.

Healthcare investment spikes around telemedicine and e-pharmacies after pandemic lessons, yet insurance reimbursement gaps temper immediate scale. Manufacturing leans on private 5G and IoT for predictive maintenance at Alba and Gulf Industrial Investment Co. Energy and utilities deploy smart meters and grid analytics aligned with net-zero goals by 2060.

Geography Analysis

Bahrain leverages compact geography and six submarine cables to serve as a Gulf data interchange hub while posting the region’s highest telecom-maturity index score of 70. BNET’s fiber roll-out aims for universal gigabit access by 2026, lifting fixed-line speeds 150% since 2023 and underpinning national smart-city projects.

The Kingdom ranks 18th on the UN e-Government Development Index, backed by USD 250 million of digital-infrastructure capex from Beyon in 2023. Cost benchmarking finds ICT operating expenses 28% below GCC averages, aided by zero corporate tax outside hydrocarbons and one-day business-registration portals.

Human-capital metrics reinforce competitiveness: first globally in digital literacy and second among Arab states on the World Bank Human Capital Index. Tamkeen’s wage-support schemes plan to upskill 50,000 nationals annually, further strengthening the local talent pipeline.

Competitive Landscape

Market structure is moderately fragmented: Batelco, Zain, and STC control connectivity while hyperscalers dominate IaaS, and global SIs chase transformation projects. Batelco collaborates with Nokia on industrial 5G and explores wholesale fiber monetization; STC pilots a Web3 Launchpad to future-proof revenue[4]stc wholesale, “Web3 Launchpad Program,” wholesale.stc.com.bh. Zain’s cloud marketplace bundles SaaS for SMEs, intensifying service-layer rivalry.

Global vendors such as Microsoft, Oracle, and Google Cloud partner with regulators to ensure compliance, while cybersecurity specialists Palo Alto and Trend Micro localize SOC services. White-space remains in tower-company carve-outs and neutral-host indoor DAS, mirroring regional M&A patterns where digital-infra deals topped USD 92.3 billion in 2024.

Domestic start-ups capitalize on fintech sandbox flexibility, often exiting via regional acquirers seeking Bahraini licenses. Government funding plus expatriate know-how seed niches in GovTech, health-tech, and gaming, but scale-up capital gaps invite foreign VC participation, shaping a dynamic yet opportunity-laden competitive scene.

Bahrain ICT Industry Leaders

Oracle

Amazon

IBM

Microsoft Corporation

Wipro

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Batelco and Nokia deploy the first private 5G network at Aluminium Bahrain.

- March 2025: STC Bahrain partners with Lionscraft on Web3 infrastructure, deal signed in the metaverse.

- February 2025: ARRAY Innovation signs AI agreements with Alba and NBB at Gateway Gulf Forum.

- January 2025: Bahrain Space Agency and TRA coordinate satellite-spectrum planning under the Al Munther file.

Bahrain ICT Market Report Scope

Bahrain's ICT market includes deep analysis of critical technology investments such as cloud technologies and artificial intelligence.

Bahrain ICT Market is Segmented by type (hardware, software, IT services, telecommunication services), by the size of the enterprise (small and medium enterprises, large enterprises), by end-user vertical (BFSI, IT & Telecom, government, retail, and E-Commerce, manufacturing, energy, and utilities, and other industry verticals).

The market sizes and forecasts are in terms of value (USD million) for all the above segments.

By Type

| Hardware | Computer Hardwar |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | Managed Services |

| Business Process Services | |

| Business Consulting Services | |

| Cloud Services | |

| IT Infrastructure | |

| IT Security | |

| Communication Services |

By End-user Enterprise Size

| Large Enterprises |

| SMEs |

By Industry Vertical

| BFSI |

| Government and Public Sector |

| ICT and Telecom |

| Retail and E-Commerce |

| Manufacturing |

| Energy and Utilities |

| Healthcare |

| By Type | Hardware | Computer Hardwar |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | Managed Services | |

| Business Process Services | ||

| Business Consulting Services | ||

| Cloud Services | ||

| IT Infrastructure | ||

| IT Security | ||

| Communication Services | ||

| By End-user Enterprise Size | Large Enterprises | |

| SMEs | ||

| By Industry Vertical | BFSI | |

| Government and Public Sector | ||

| ICT and Telecom | ||

| Retail and E-Commerce | ||

| Manufacturing | ||

| Energy and Utilities | ||

| Healthcare | ||

Key Questions Answered in the Report

How large is the Bahrain ICT market in 2026?

The Bahrain ICT market size equals USD 4.29 billion in 2026.

What CAGR is projected for Bahrain’s ICT spending to 2031?

Spending is forecast to expand at a 16.45% CAGR between 2026 and 2031.

Which component grows fastest through 2031?

IT services record the highest 10.92% CAGR, driven by cloud, cybersecurity, and consulting demand.

Why are SMEs key to future ICT growth in Bahrain?

Subsidies and simplified SaaS adoption push SME ICT outlays at a 11.85% CAGR, outpacing large enterprises.

What deployment model is gaining momentum among regulated firms?

Hybrid/multi-cloud is the fastest-growing mode at 14.62% CAGR, balancing residency and flexibility.

Page last updated on: