Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 30.56 Billion |

| Market Size (2031) | USD 38.86 Billion |

| Growth Rate (2026 - 2031) | 4.92% CAGR |

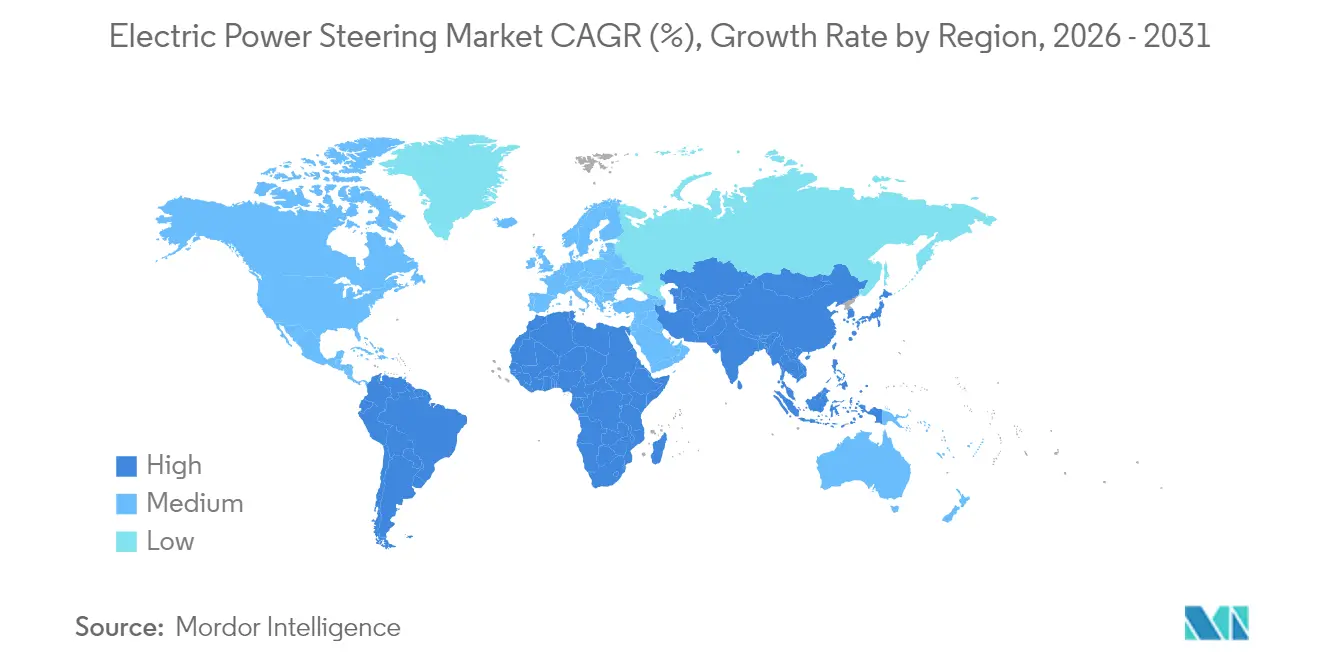

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

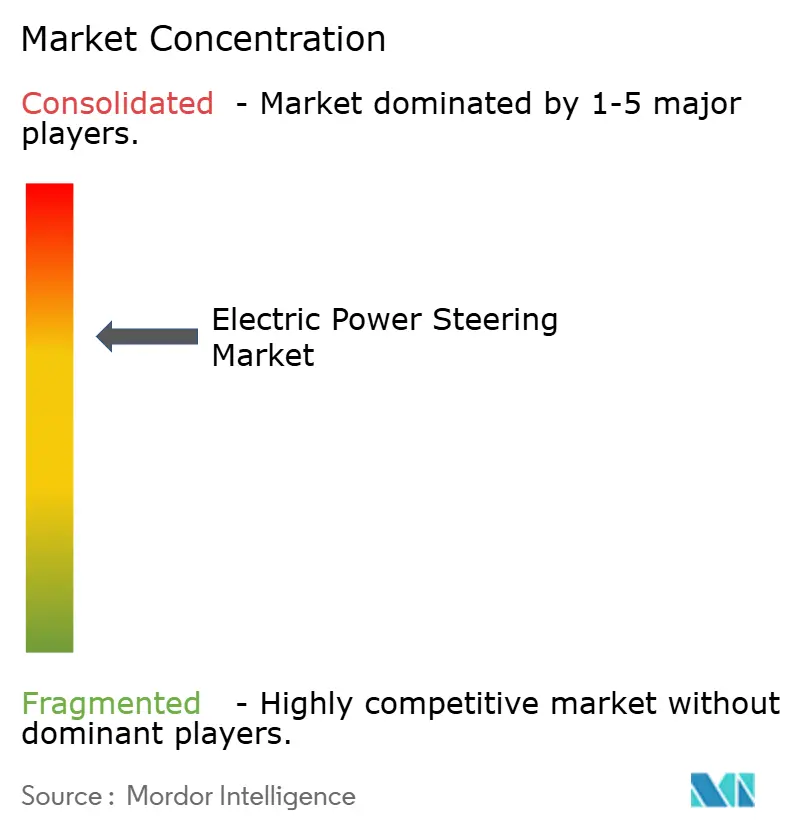

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Electric Power Steering Market Analysis by Mordor Intelligence

The electric power steering market size was valued at USD 29.13 billion in 2025 and estimated to grow from USD 30.56 billion in 2026 to reach USD 38.86 billion by 2031, at a CAGR of 4.92% during the forecast period (2026-2031). Rising penetration of steer-by-wire, tighter fuel-efficiency rules, and the shift toward software-defined vehicles underpin this steady trajectory. Automakers now emphasize intelligent software calibration delivered through over-the-air updates, using the steering system as a gateway for mass customization. Suppliers are pivoting from purely mechanical expertise to integrated electronic architectures that comply with ISO/SAE 21434 and UN R155 cybersecurity rules. At the same time, Asia-Pacific’s dominant share rests on China’s EV scale and Japan’s precision-component heritage. South America’s accelerating EV adoption signals the next demand wave in cost-sensitive markets. Incumbent Tier-1s defend their position by bundling electronic control units, sensors, and motor designs into turnkey modules that can be validated against evolving ADAS mandates.

Key Report Takeaways

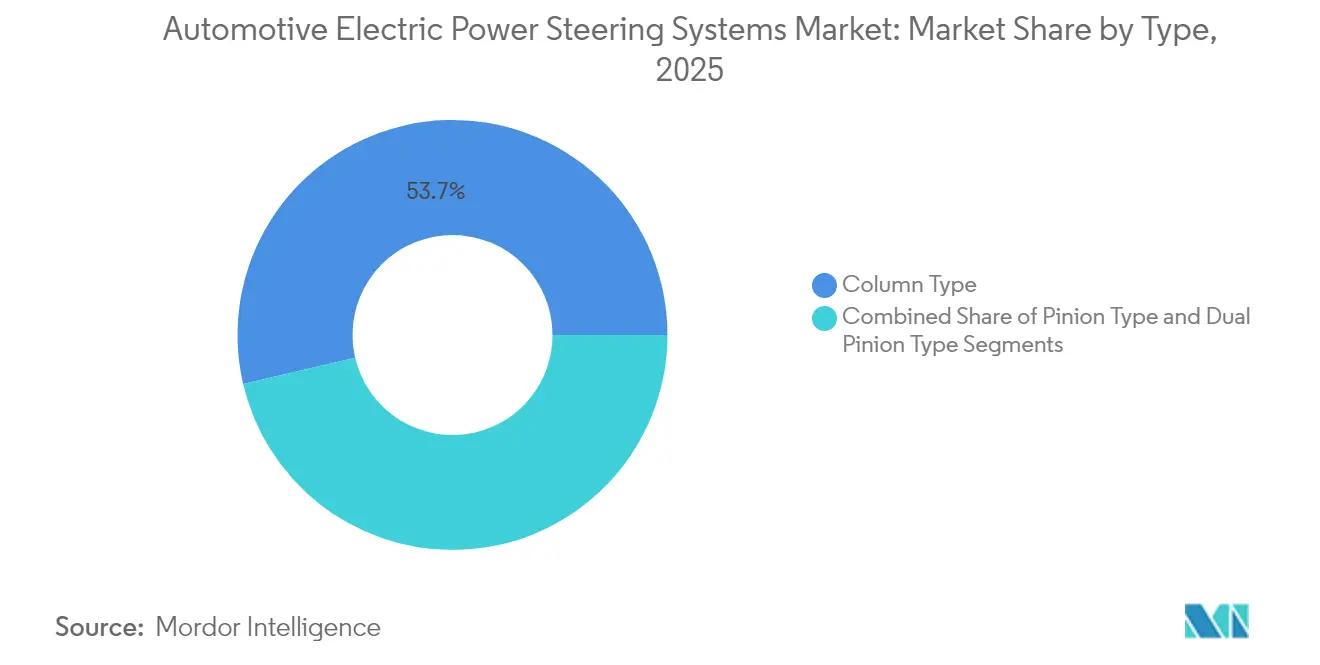

- By type, column type systems led with 53.65% of electric power steering market share in 2025; Dual Pinion Type is projected to expand at an 11.07% CAGR through 2031.

- By propulsion, internal combustion engine vehicles held 61.05% of the electric power steering market in 2025, while battery electric vehicles will post the fastest 15.92% CAGR.

- By component, steering rack/column accounted for 42.12% of the electric power steering market size in 2025; sensor components record the highest 9.86% CAGR to 2031.

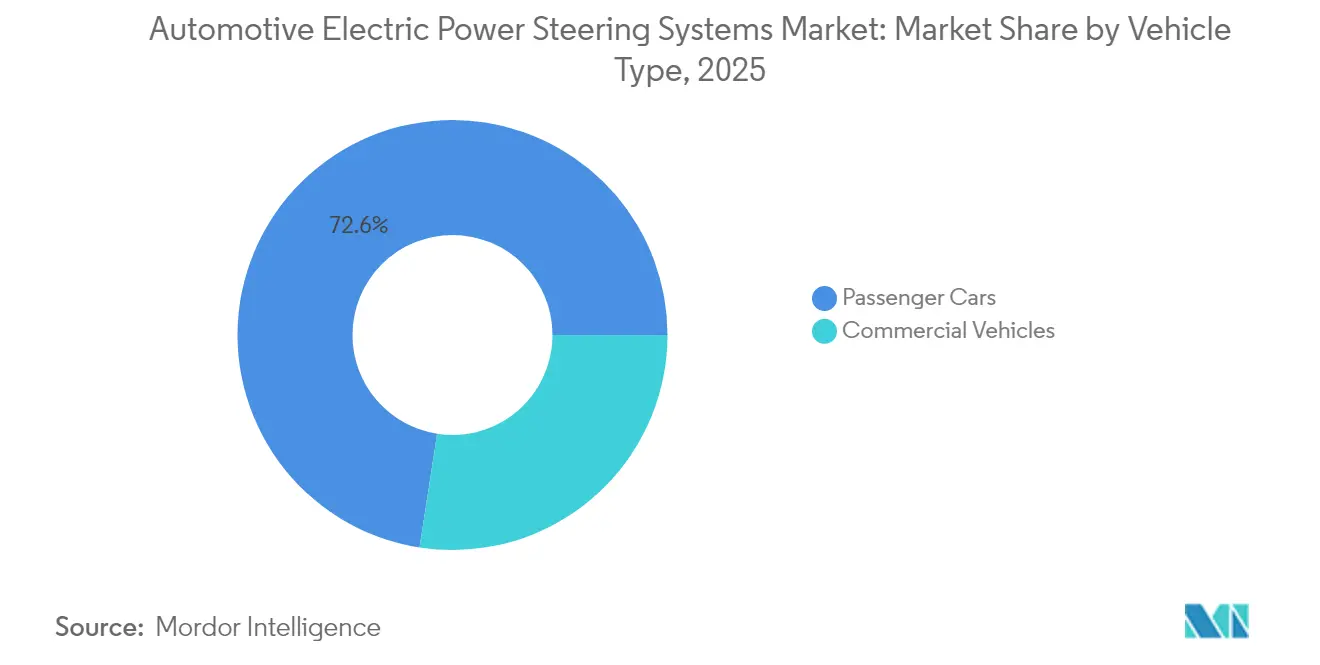

- By vehicle category, passenger cars dominated at 72.55% share in 2025, whereas commercial vehicles are set for a 9.32% CAGR.

- By region, Asia-Pacific captured 46.35% revenue in 2025; South America is forecast to advance at a 8.94% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Electric Power Steering Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification of Vehicle Platforms | +1.8% | Global, with Asia-Pacific and Europe leading adoption | Medium term (2-4 years) |

| Fuel Efficiency and Emission Reduction | +1.2% | Global, driven by NHTSA CAFE and EU regulations | Long term (≥ 4 years) |

| Regulatory Mandates | +0.9% | North America and EU primary, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Steer-by-Wire R&D Breakthroughs | +0.7% | Premium segments globally, early adoption in China | Long term (≥ 4 years) |

| Collaboration on 48-V e-Powertrain Modules | +0.4% | Europe and North America focus | Medium term (2-4 years) |

| OTA Software Steering Calibration | +0.3% | Software-defined vehicle markets globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Electrification of Vehicle Platforms

Vehicle electrification fundamentally reshapes EPS adoption patterns by eliminating the parasitic losses inherent in hydraulic systems that drain ICE engine power. Electric vehicles demand energy-efficient steering solutions, with hybrid EPS systems demonstrating over 50% energy consumption reduction compared to conventional hydraulic power steering in commercial vehicle applications. The transition accelerates as automakers recognize EPS as an essential infrastructure for regenerative braking integration and battery range optimization. NHTSA's Corporate Average Fuel Economy standards for model years 2027-2031 mandate 2% annual fuel efficiency improvements, making EPS adoption economically inevitable for ICE vehicles while providing competitive advantages for EVs[1]"Corporate Average Fuel Economy Standards for Passenger Cars and Light Trucks for Model Years 2027 and Beyond and Fuel Efficiency Standards for Heavy-Duty Pickup Trucks and Vans for Model Years 2030 and Beyond", NHTSA, nhtsa.gov. . This regulatory pressure creates a dual-market dynamic where EPS becomes compliance-driven for traditional vehicles and performance-enhancing for electric platforms.

Increasing Demand for Fuel Efficiency and Emission Reduction

Fuel efficiency mandates drive EPS adoption through measurable consumption benefits, with National Research Council studies indicating 1.3% fuel reduction for midsize cars and 1.1% for large cars when replacing hydraulic systems. Efficiency gains compound across fleet operations, making EPS economically attractive for commercial vehicle operators facing rising fuel costs and carbon pricing mechanisms. European Union's General Safety Regulation II, effective July 2024, mandates advanced safety technologies that integrate seamlessly with EPS systems, creating regulatory synergies that accelerate adoption. The convergence of efficiency requirements and safety mandates EPS as a foundational technology rather than optional equipment. Fleet operators increasingly recognize EPS as an infrastructure investment that delivers immediate operational cost reductions while enabling future autonomous capabilities.

Regulatory Mandates for ADAS Integration

Advanced Driver Assistance Systems integration requirements create technical dependencies that favor EPS over hydraulic alternatives due to electronic control precision and response speed capabilities. The United Nations Economic Commission for Europe adopted provisions for steer-by-wire systems and updated UN Regulations Nos. 79 and 171, establishing international frameworks that standardize EPS-ADAS integration protocols. NHTSA's New Car Assessment Program updates for the 2026 model year mandate Blind Spot Warning, Lane Keeping Assist, and Pedestrian Automatic Emergency Braking evaluations, all requiring EPS-level precision for effective operation[2]"New Car Assessment Program Final Decision Notice-Advanced Driver Assistance Systems and Roadmap", Federal Register, federalregister.gov.. The regulatory timeline creates market urgency as manufacturers must integrate these systems by specific deadlines, eliminating gradual adoption strategies. European regulations particularly emphasize vulnerable road user protection, requiring steering systems capable of emergency intervention maneuvers that exceed hydraulic system response capabilities.

Steer-by-Wire R&D Breakthroughs

Steer-by-wire technology eliminates mechanical linkages between the steering wheel and the road wheels, enabling variable steering ratios and enhanced safety through redundant electronic architectures. Mercedes-Benz's 2026 launch timeline for steer-by-wire in the updated EQS represents the first German manufacturer deployment, featuring customizable steering feedback and improved parking maneuverability. ZF's volume production contracts and NIO ET9 integration demonstrate commercial viability beyond premium segments, with ZF claiming significant market share capture potential by 2030. The technology enables interior design flexibility by allowing retractable steering wheels and supports autonomous driving through precise electronic control. Commercial vehicle applications show promise, with ZF's EPS systems providing up to 8,000 Nm output torque without hydraulic fluid requirements, reducing maintenance complexity and improving reliability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher Unit Cost vs. Hydraulic Systems | -0.8% | Emerging markets, price-sensitive segments globally | Short term (≤ 2 years) |

| Limited Steering Feel and Safety Concerns | -0.6% | Asia-Pacific emerging markets, rural applications | Medium term (2–4 years) |

| Semiconductor Supply-Chain Volatility | -0.4% | Global, with acute impact in Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Cyber-Security Risks | -0.2% | Connected vehicle markets globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Higher Unit Cost vs. Hydraulic Systems in Low-Cost Cars

Cost competitiveness remains challenging in price-sensitive market segments where hydraulic systems maintain economic advantages despite operational inefficiencies. Indian automakers demonstrate varied approaches to cost management, with Tata Motors achieving 80% localization for Harrier EV components while companies like Ola Electric develop magnet-less motors to avoid rare-earth material dependencies. The cost differential becomes more pronounced as China's rare-earth export restrictions create supply chain pressures, with India considering the relaxation of 50% localization requirements to maintain EV manufacturing viability. Manufacturing scale economics favor established hydraulic system suppliers in volume segments, creating market bifurcation where premium vehicles adopt EPS while economy segments resist transition. The challenge intensifies in commercial vehicle applications where initial capital costs directly impact fleet profitability, requiring a clear operational savings demonstration to justify higher acquisition prices.

Limited Steering Feel and Safety Concerns in Emerging Markets

Consumer acceptance challenges persist in markets where drivers expect traditional hydraulic steering feedback characteristics, particularly in commercial and agricultural applications requiring precise load sensing. Japanese automotive parts manufacturers acknowledge the difficulty in adapting EPS systems for heavier vehicles, maintaining reliance on electronically controlled hydraulic power steering for applications requiring substantial steering force. The safety perception gap becomes critical in emerging markets where infrastructure conditions demand robust steering systems capable of handling poor road surfaces and extreme operating conditions. Cybersecurity concerns compound acceptance issues as ISO/SAE 21434 compliance requirements create complexity that may not align with local market priorities or technical capabilities. Rural and commercial operators particularly value mechanical reliability over electronic sophistication, creating market resistance that slows adoption rates in specific geographic segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Column Type Systems Dominate But Face A Growing Challenge From Dual Pinion Designs.

Column Type EPS systems commanded a 53.65% market share in 2025, reflecting their established integration advantages and cost-effectiveness for mainstream vehicle platforms. However, dual-pinion type configurations emerge as the fastest-growing segment at 11.07% CAGR through 2031, driven by precision requirements for autonomous driving applications and enhanced steering response characteristics. Pinion Type systems maintain a steady market presence in mid-range applications, offering balanced performance between cost and capability. The segment evolution reflects manufacturers' strategic positioning for future mobility requirements, where steering precision becomes critical for safety-critical autonomous functions.

ZF's steer-by-wire technology deployment in NIO's ET9 demonstrates how advanced architecture enables new steering wheel designs and improved maneuverability, particularly benefiting electric vehicle platforms. Column Type systems retain advantages in retrofit applications and cost-sensitive segments, while Dual Pinion configurations attract premium manufacturers seeking differentiated driving experiences. Technology progression suggests market bifurcation where volume segments prioritize proven Column Type reliability while performance-oriented applications migrate toward Dual Pinion precision capabilities.

By Component Type: Sensor Growth Outpaces Traditional Hardware

Steering Rack/Column components maintained 42.12% market share in 2025, representing the mechanical foundation of EPS systems across all vehicle types. Sensor components accelerate fastest at 9.86% CAGR through 2031, reflecting the increasing sophistication of feedback mechanisms required for advanced driver assistance systems integration. Steering Motor segments provide consistent performance as the primary actuation component, while Other Component Types encompass emerging technologies like cybersecurity modules and OTA update capabilities. The component mix evolution indicates market maturation beyond basic electrification toward intelligent system architectures.

The sensor growth trajectory aligns with regulatory requirements for enhanced vehicle safety systems, where precise feedback enables emergency steering interventions and lane-keeping assistance functions. NSK's development of Force Feedback Actuators and Road Wheel Actuators for steer-by-wire applications exemplifies the component sophistication required for next-generation steering systems. Traditional mechanical components face commoditization pressure while electronic components command premium pricing through advanced functionality, reshaping supplier value propositions and competitive dynamics.

By Vehicle Type: Commercial Vehicles Drive Unexpected Growth

Passenger Cars dominated with 72.55% market share in 2025, reflecting the segment's early EPS adoption and volume production advantages. Commercial Vehicles emerge as the fastest-growing segment at 9.32% CAGR through 2031, driven by fleet operators' recognition of operational cost benefits and regulatory compliance requirements. The commercial vehicle acceleration reflects delayed adoption patterns where initial skepticism gives way to demonstrated efficiency gains and maintenance cost reductions. Fleet applications value EPS systems' reduced maintenance requirements compared to hydraulic alternatives, with energy savings translating directly to operational profitability.

Hybrid electric power steering systems in commercial vehicles demonstrate over 50% energy consumption reduction compared to conventional hydraulic systems, making adoption economically compelling for fleet operators facing fuel cost pressures. The commercial vehicle transition accelerates as manufacturers develop systems capable of handling higher torque requirements while maintaining reliability standards for commercial operations. ZF's commercial vehicle EPS systems provide up to 8,000Nm output torque without hydraulic fluid, addressing traditional concerns about power capability while eliminating maintenance complexity.

By Propulsion Type: Battery Electric Vehicles Lead Transformation

Internal-combustion engine vehicles retained 61.05% market share in 2025, representing the installed base of traditional automotive platforms still transitioning to electric steering systems. Battery Electric Vehicles drive market growth at 15.92% CAGR through 2031, creating demand for EPS systems optimized for energy efficiency and regenerative braking integration. Hybrid Vehicles occupy the middle ground, requiring EPS systems capable of seamless operation across multiple powertrain modes. The propulsion type segmentation reveals how vehicle electrification fundamentally reshapes steering system requirements and performance expectations.

Battery electric vehicle applications demand EPS systems that minimize parasitic losses while supporting advanced features like one-pedal driving and regenerative braking coordination. The energy efficiency imperative drives innovation in motor design and control algorithms, with manufacturers developing rare-earth-free solutions to address supply chain vulnerabilities highlighted by China's export restrictions. ICE vehicle applications focus on fuel efficiency improvements, where EPS systems provide measurable consumption benefits that help manufacturers meet increasingly stringent regulatory requirements.

Geography Analysis

Asia-Pacific anchored 46.35% of the electric power steering market revenue in 2025. China’s vertically integrated EV ecosystem packages domestic motor controllers, vehicle domains, and steering gears into cost-competitive modules serving local and export programs. NIO’s adoption of steer-by-wire from ZF underscores China’s readiness to leap directly into advanced architectures. Japan, meanwhile, protects leadership in high-precision bearings and angle sensors, enabling local suppliers to sell critical sub-assemblies to global Tier-1s. Government incentives for carbon neutrality accelerate demand, and regional capacity ensures component availability.

Europe represents a mature but regulation-driven arena. The EU General Safety Regulation II forces OEMs to fit lane-keeping and pedestrian-avoidance functions that rely on EPS precision. Suppliers gain from stable planning cycles as implementation dates are locked. Mid-decade cybersecurity rules further elevate barriers, consolidating volume among companies with dedicated software teams.

North America focuses on efficiency mandates. NHTSA’s CAFE standards impose 2% annual gains for passenger fleets through 2031. South America, led by Brazil, is the fastest-expanding region with a 8.94% CAGR through 2031. A 90% spike in EV sales in 2024 demonstrated pent-up demand once taxes were waived for imported battery modules. Stellantis followed with a EUR 5.6 billion commitment to develop Bio-Hybrid powertrains that integrate EPS for dual-fuel flexibility. The region’s growth illustrates tech leapfrogging, bypassing hydraulic incumbency.

Regulatory Landscape

EPS design, validation, and homologation increasingly sit under safety, steering-equipment, and connected-vehicle compliance stacks, with ISO 26262 functional safety remaining the foundational requirement for safety-critical steering assist (including ASIL-focused hazard analysis for unintended assist). On the steering-equipment side, UN Regulation No. 79 continues as the primary international framework for steering systems, and its ongoing updates around Automated Commanded Steering Functions (ACSF) tighten expectations for electronic control, driver warning and deactivation behavior, and redundancy concepts that favor EPS and steer-by-wire architectures.

Steer-by-wire standardization is also advancing through formal standards and UN regulatory work. UNECE GRVA initiated the 05 series of amendments to UN Regulation No. 79 in December 2025, and UNECE WP.29 considered and voted on multiple supplements and corrigenda tied to UN R79 in June 2026, reinforcing the compliance cadence OEMs and Tier-1s must plan around. In parallel, ISO 19725:2026 provides system safety guidelines specific to steer-by-wire systems in passenger cars and light commercial vehicles, adding another documented layer of system-safety expectations as production programs move from assisted steering to motion-by-wire implementations.

Value Chain Analysis

The EPS value chain runs from raw-material and semiconductor inputs through precision mechatronics manufacturing and software validation, then into OEM integration and aftersales service. Upstream dependencies center on motor materials (including neodymium-based magnets with concentrated processing), MCUs and power electronics for the ECU and inverter stages, and high-precision mechanical elements (rack/column, bearings, gears).

Midstream, Tier-1 suppliers such as JTEKT, ZF, Nexteer, Bosch, and NSK integrate motors, sensors, ECUs, and embedded software into platform-specific modules (column assist, pinion assist, rack assist, and emerging steer-by-wire sub-systems) and support EMC, durability, NVH, and cybersecurity-aligned development flows. Downstream, OEM program timing and validation cycles act as a gating mechanism for new EPS introductions, with durability and vehicle-level tuning extending development and limiting rapid supplier switching once a platform is frozen. Supply risk and cost volatility remain concentrated around magnets and semiconductors, while the shift to software-defined vehicles increases the share of value in control algorithms, diagnostics, and secure update readiness. As modular EPS portfolios expand, suppliers can reuse core subassemblies across architectures to reduce engineering duplication and shorten industrialization timelines while maintaining the required validation evidence for each vehicle program.

Competitive Landscape

Competition is moderate yet technologically intense. Five long-established suppliers—JTEKT, ZF, Nexteer, Bosch and NSK—still account for a dominant revenue slice. JTEKT cites its global leadership position, shipping more power-steering units than rivals. ZF, aiming to outpace peers in next-generation architecture, consolidated its chassis divisions to streamline steer-by-wire investment. The supplier secured volume contracts with Chinese EV brands and German luxury OEMs, anchoring future platform share.

Nexteer builds regional technical centers like its new Mexican laboratory to localize validation and shorten launch timelines. Bosch added European EPS capacity in Hungary to mitigate supply-chain risks. Strategic mergers, notably Schaeffler’s acquisition of Vitesco Technologies, reshape the ecosystem by combining drivetrain electronics with chassis know-how, extracting EBIT synergies of EUR 600 million by 2029.

As cybersecurity mandates mature, suppliers with ISO/SAE 21434-certified development flows enjoy pull-through across multiple programs. Smaller or niche players struggle to fund redundant electronics and long homologation cycles. The competitive arena, therefore, hinges on embedded software scale, ASIC roadmaps, and life-cycle service contracts rather than purely mechanical differentiation.

Electric Power Steering Industry Leaders

-

JTEKT Corporation

-

Nexteer Automotive Group Ltd

-

NSK Ltd

-

ZF Friedrichshafen AG

-

Robert Bosch GmbH

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A primary whitespace is the transition from conventional EPS to steer-by-wire and broader motion-by-wire stacks that support advanced lane-keeping and automated steering functions under the evolving UN R79 framework. Compliance pull from safety and steering-equipment requirements increases demand for higher-integrity sensing, redundancy strategies, and safety-case documentation, which shifts procurement toward suppliers that can deliver ASIL-aligned engineering, validated software, and production-ready electronic architectures. This raises opportunity in higher-content EPS modules (sensors, ECUs, cybersecurity-aware development processes) rather than purely mechanical rack/column hardware, aligning with the market shift toward software calibration and OTA-enabled feature tuning described in the report context.

Manufacturing and localization investments provide concrete headroom for capacity, lead-time reduction, and regional content alignment, particularly in Asia-Pacific where EPS demand is anchored by EV scale and rapid architecture adoption. Nexteer opened its manufacturing facility in Rayong, Thailand (March 2026) to produce Column-Assist EPS systems, and it also opened a manufacturing and testing campus in Changshu, China (January 2025) to expand advanced steering production and validation, both of which expand local supply to OEM clusters and reduce launch friction. On the technology side, series-production milestones such as ZF supplying steer-by-wire for NIO ET9 (February 2025 in the report context) and Nexteer placing steer-by-wire into series production (April 2026) show active platform pull for fully electronic steering, widening the addressable scope for redundant electronics, handwheel actuators, and safety power backup solutions in passenger cars and, over time, commercial applications where torque capability and validation evidence are already moving upward.

Recent Industry Developments

- April 2026: Nexteer Automotive commenced series production of its steer-by-wire system for a leading Chinese new energy vehicle manufacturer. Moving steer-by-wire from launches to sustained production elevates demand for safety-qualified electronics, actuator redundancy, and vehicle-level steering software calibration capabilities across OEM programs.

- October 2025: Nexteer Automotive announced its Direct Drive Hand Wheel Actuator (DD-HWA) for steer-by-wire applications, designed to support both 12V and 48V electrical architectures. The product expands the company's motion-by-wire building blocks and strengthens platform scalability for OEMs targeting software-defined steering features.

- December 2024: Bosch initiated electric steering systems production in Hungary, expanding European manufacturing capacity for EPS. Localized production shortens supply lines for European OEMs operating under tightening safety and efficiency mandates and supports higher-volume industrialization of electronically controlled steering modules.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers electric power steering (EPS) systems used in road vehicles, where steering assist is provided mainly through an electric motor and control unit rather than hydraulic pressure. We size the market in value terms for EPS supplied to passenger and commercial vehicles across major automotive regions.

Scope exclusions: We exclude non-automotive steering applications and standalone service activity that is not tied to EPS system sales for vehicles.

Segmentation Overview

-

By Type

- Column Type

- Pinion Type

- Dual Pinion Type

-

By Component Type

- Steering Rack/Column

- Sensor

- Steering Motor

- Other Component Types

-

By Vehicle Type

- Passenger Cars

- Commercial Vehicles

-

By Propulsion Type

- Internal Combustion Engine Vehicles

- Hybrid Vehicles

- Battery Electric Vehicles

-

By Geography

-

North America

- United States

- Canada

- Rest of North America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- Turkey

- South Africa

- Egypt

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the demand backdrop and to keep assumptions realistic by region and vehicle type. We relied on public sources such as vehicle production and registration releases from government statistics offices, customs trade databases for automotive parts flows, and standards or regulatory publications that influence EPS adoption and electronics content. Technical context was also taken from peer reviewed journals and patent publications to understand architecture shifts such as column, pinion, and dual pinion designs.

To connect these signals to revenue, we also reviewed company filings and investor presentations for steering and chassis suppliers, along with association websites and reputed automotive press for program launches and platform changes. Where needed, paid subscriptions covering company financials and intelligence, and another covering shipment level trade and patent lookups, were used to cross check ranges for pricing and content per vehicle. The desk research sources mentioned above are illustrative only, and other public documents were also referred to for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to test what we built from published data, especially for EPS fitment by vehicle class, typical system pricing, and how content changes with electrification and ADAS features. We spoke with a mix of steering system suppliers, component specialists, vehicle OEM level engineering and purchasing contacts, and aftermarket aware stakeholders. Coverage across APAC, EMEA, and the Americas helped compare regional patterns and refine the assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 14% | APAC: 42% |

| Mid tier: 50% | Functional/Unit leaders: 37% | EMEA: 33% |

| Smaller Players: 14% | Managers: 49% | Americas: 25% |

Market-Sizing & Forecasting

Sizing starts from a top-down demand pool, where vehicle production and parc signals are rebuilt by region and vehicle type, then filtered through EPS penetration and replacement patterns. Once the vehicle base is established, unit demand is translated into value using system level pricing adjusted by architecture mix (column, pinion, dual pinion) and by electronics and motor content.

To keep the totals grounded, we corroborate results with selective bottom-up approximations. These include sampled supplier revenue splits, channel checks on steering module pricing, and quick unit-by-ASP calculations for high volume countries. Inputs that mattered most in this market included passenger versus commercial production shares, EPS take rate versus hydraulic steering, the share shift toward rack assist solutions in larger vehicles, battery electric vehicle build rates, and the speed of ECU and motor cost changes. Forecasts were built using scenario analysis, where the macro vehicle outlook, electrification pace, and feature content per vehicle are varied, then aligned to expert views from interviews. If a country or sub-segment had weak visibility, we filled gaps using proxy ratios from similar markets and then rechecked the impact so totals did not get overstated.

Data Validation & Update Cycle

Model outputs are checked against independent signals, including vehicle production trends, import-export movement for steering components, and reported steering related revenue direction in public filings, before assumptions are finalized. When a variance shows up, it is investigated and either explained by scope or corrected through a second pass of inputs, then reviewed internally before sign-off.

The report is refreshed annually, and we also do interim updates when material events occur, such as regulation changes, major platform launches, or sharp shifts in vehicle output. Before delivery, a final review is completed so clients receive the most current view based on the latest available releases and follow-up contacts where needed.

Mordor Intelligence's Automotive Electric Power Steering Systems Market Estimate Compared With Other Published Estimates

Published market sizes for electric power steering often do not match because the underlying counting rules are not the same, even when the report titles look similar. Differences usually come from what is included in the system scope, which base year is chosen, and how pricing and penetration are projected across vehicle types.

Some estimates blend hydraulic and electro-hydraulic steering with EPS, or they widen the lens to include broader steering assemblies and service activity, which pushes the value upward. In other cases, the gap comes from how fast pricing is assumed to fall as volumes rise, how BEV mix is treated in the forecast years, and whether the study uses a recent currency timing and an updated vehicle production path.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 29.13 B (2025) | |

| Global Consultancy A | USD 26.82 B (2024) | Uses a different base year and applies mechanism splits that can miss late-cycle EPS content added on newer platforms, especially where ADAS driven steering calibration work increases system value. |

| Industry Publisher B | USD 29.38 B (2025) | Presents the total with less visibility on how architecture mix and regional pricing are built up, so the same unit outlook can land at a slightly different value when ECU and motor cost-down is applied. |

The table shows that the spread is mainly explained by timing and what is counted inside an EPS system. In Mordor Intelligence's model, only EPS supplied for passenger and commercial road vehicles is included, with pricing adjusted by column, pinion, and dual pinion mix and by propulsion shifts. These steps make the estimate easier to trace back to vehicle output, penetration, and a consistent system ASP path.

Key Questions Answered in the Report

What is the current size of the electric power steering market?

The market generated USD 30.56 billion in 2026 and is forecast to grow to USD 38.86 billion by 2031 at a 4.92% CAGR.

Which vehicle segment is expanding fastest for EPS adoption?

Commercial Vehicles are projected to post a 9.32% CAGR through 2031 as fleets capitalize on fuel-saving and maintenance benefits.

Which region leads EPS revenue, and which grows fastest?

Asia-Pacific led with a 46.35% share in 2025, while South America registers the highest 8.94% CAGR due to rapid EV uptake in Brazil.

What technological trend will most disrupt the EPS landscape by 2031?

Steer-by-wire, already entering series production, is set to redefine cabin design and enable software-defined steering functions that can be updated over the air.

Page last updated on: