Automotive Battery Management Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

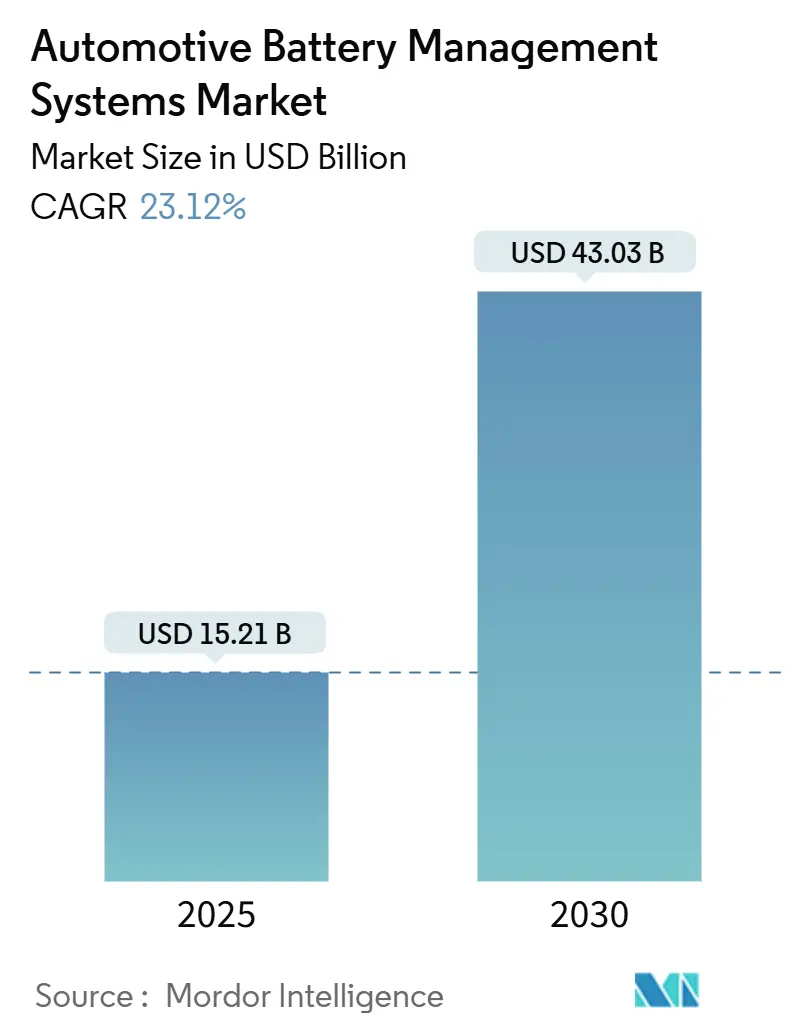

| Market Size (2025) | USD 15.21 Billion |

| Market Size (2030) | USD 43.03 Billion |

| Growth Rate (2025 - 2030) | 23.12% CAGR |

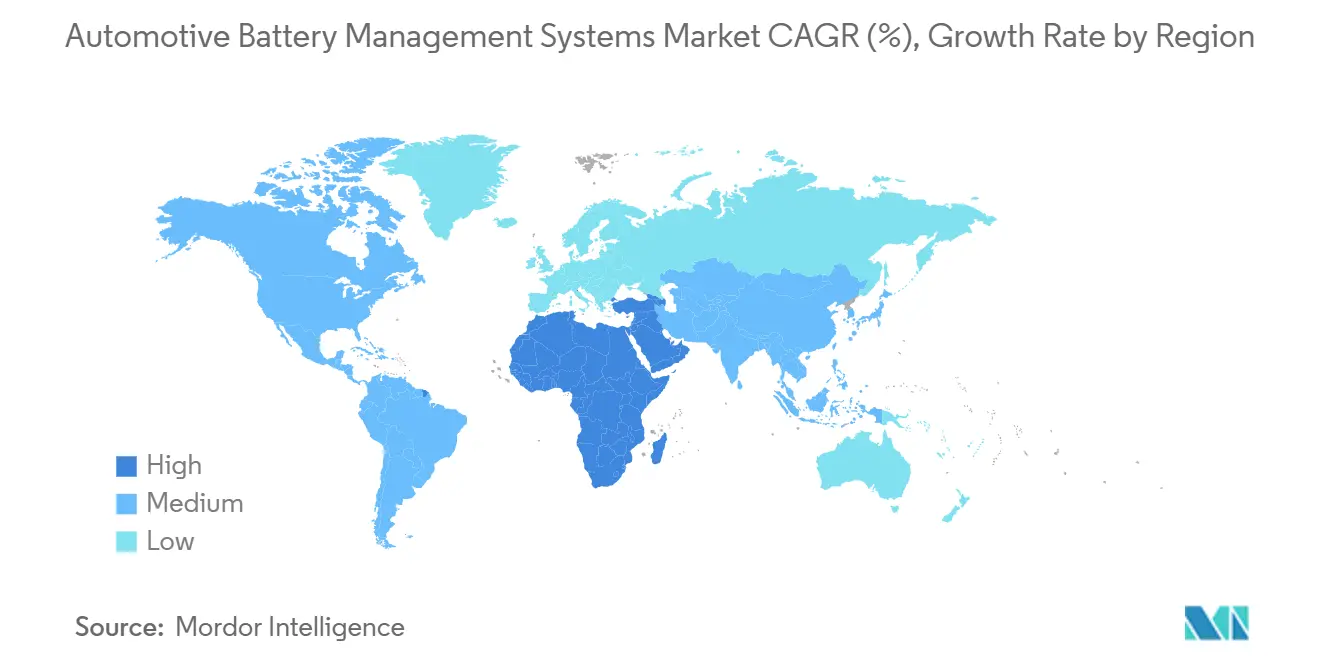

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

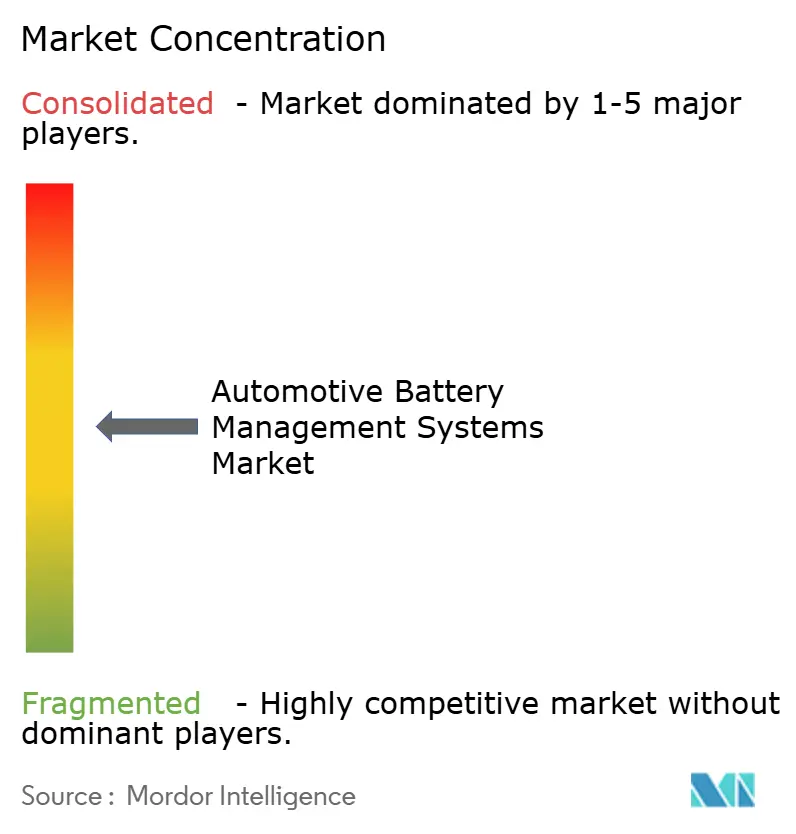

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Battery Management Systems Market Analysis by Mordor Intelligence

The automotive battery management system market size is valued at USD 15.21 billion in 2025 and is forecast to climb to USD 43.03 billion in 2030, reflecting a vigorous 23.12% CAGR. This expansion mirrors the global pivot from internal-combustion engines toward electrified propulsion, where a battery management system (BMS) functions as the vehicle’s central nervous system. Regulatory pressure, notably ISO 21434 cybersecurity rules that came into force for new vehicle models in 2024, is accelerating demand for cyber-secure designs. At the same time, rapid migration from hard-wired to modular and wireless topologies is trimming harness weight, boosting energy density, and shortening assembly time. Wireless solutions such as NXP’s ultra-wideband BMS, released for OEM trials in 2025, exemplify how next-generation architectures can align safety, efficiency, and cost goals.[1]NXP Semiconductors, “NXP Launches Ultra-Wideband Wireless BMS for Automotive,” nxp.com Heightened electric-vehicle (EV) sales targets, falling battery pack cost, and mainstream adoption of lithium-iron-phosphate (LFP) chemistries continue to stimulate design upgrades that place more intelligence at the cell and module level, reinforcing a robust growth path for the automotive battery management system market.

Key Report Takeaways

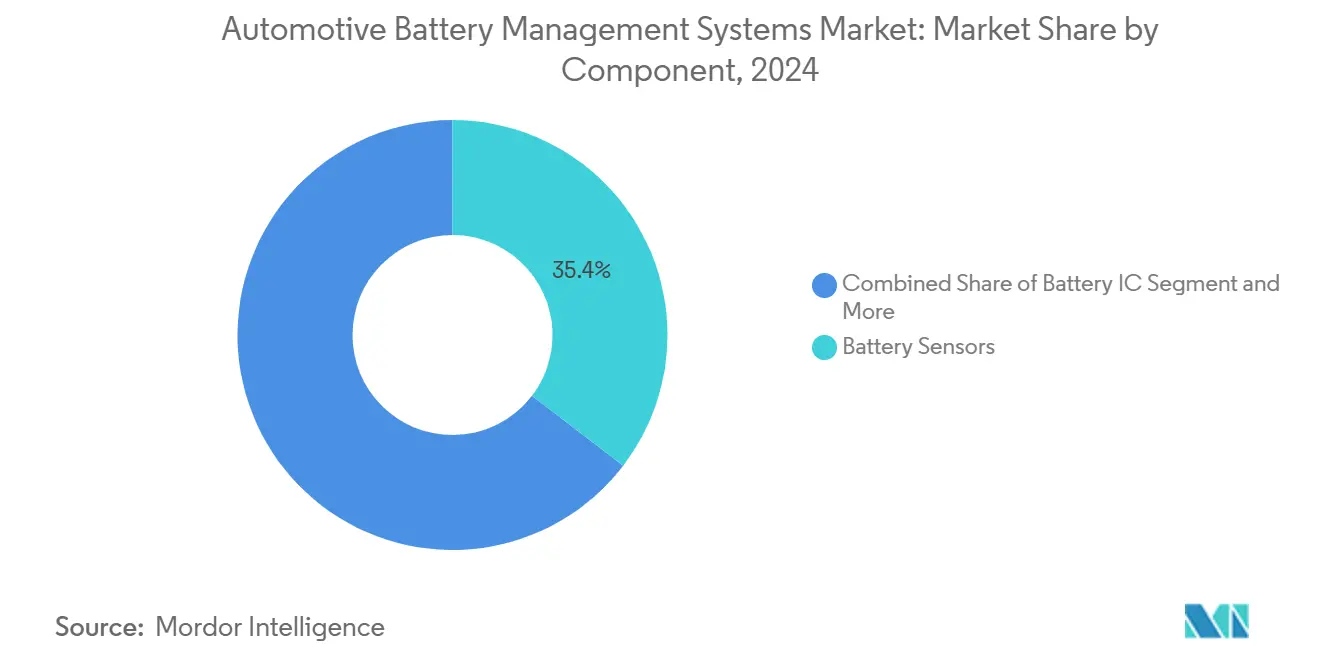

- By component, Battery Sensors held 35.41% of the automotive battery management system market share in 2024 and are expanding at a 24.66% CAGR through 2030.

- By topology, Modular systems led with a 48.95% revenue share in 2024; Wireless topology is projected to surge at a 35.17% CAGR to 2030.

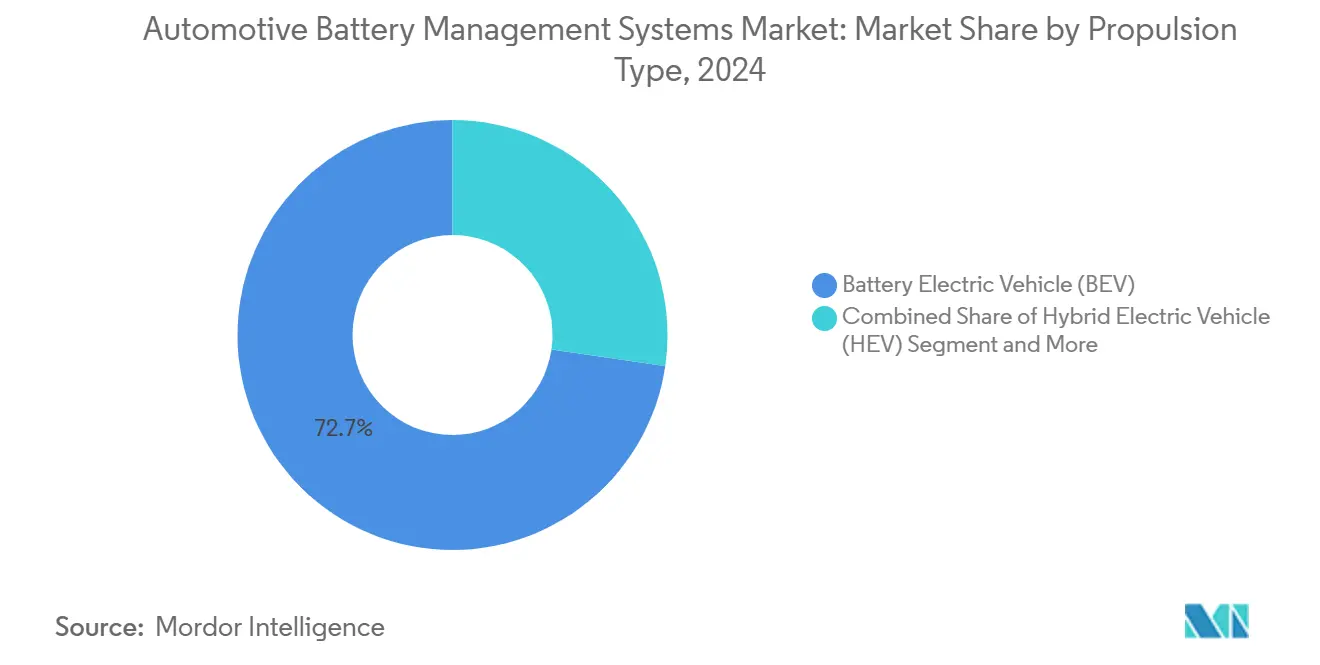

- By propulsion type, Battery Electric Vehicles captured 72.70% share of the automotive battery management system market size in 2024, whereas Fuel-Cell Electric Vehicles are forecast to advance at a 37.84% CAGR over 2025-2030.

- By vehicle type, Passenger Cars accounted for a 54.61% stake in 2024 and are expanding at a 25.26% CAGR toward 2030.

- By geography, Asia-Pacific dominated with a 61.33% slice of the automotive battery management system market in 2024, while the Middle East and Africa region is accelerating at a 27.55% CAGR through 2030.

Global Automotive Battery Management Systems Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Sales Mandates Widening Globally | +5.5% | EU, China, United States | Medium term (2-4 years) |

| Falling Cost of Battery Packs | +4.2% | APAC and emerging markets | Short term (≤ 2 years) |

| Shift from Centralized to Modular and Wireless Topologies | +3.3% | North America, EU | Medium term (2-4 years) |

| Soaring Demand for LFP Chemistry requiring Advanced Active Balancing | +3.1% | China, North America | Short term (≤ 2 years) |

| ISO 21434-driven Cyber-secure BMS Demand | +2.2% | EU, North America | Short term (≤ 2 years) |

| OEM move to In-house BMS ASIC Design to cut IP Royalty Cost | +1.7% | Germany, Japan, South Korea, United States | Long term (≥ 4 years) |

Source: Mordor Intelligence

EV sales mandates widening globally

Binding ZEV policies in regions such as the EU and California raise the baseline for durability, range retention, and transparency of battery health. Euro 7 rules will be effective in 2026, and California’s Advanced Clean Cars II demands 80% range retention for 150,000 miles, compelling BMS suppliers to incorporate more refined state-of-health analytics and degradation modeling. Harmonizing rules incentivize global platforms to adopt one compliance-ready architecture, elevating the automotive battery management system market as OEMs avoid region-specific designs. Suppliers that already embed adaptive algorithms gain a head start, whereas legacy providers face added validation cycles and cost.

Falling cost of battery packs

Rapid declines in lithium-ion battery-pack prices are reshaping cost structures. Mainstream LFP packs averaged USD 75 per kWh in 2024, and pilot sodium-ion runs have demonstrated costs as low as USD 10 per kWh. As cells get cheaper, OEMs can allocate larger portions of the battery budget to smarter BMS functions, such as predictive analytics and wireless connectivity, rather than focusing solely on hardware cost reduction. This shift toward higher value content per pack reinforces demand for advanced battery management solutions across the automotive battery management system market.

Shift from centralized to modular and wireless topologies

Manufacturers are adopting modular boards linked by wireless nodes that can be reconfigured by software, cutting up to 90% of copper harnesses. Analog Devices and NXP have demonstrated ISO 21434-compliant wireless stacks that maintain precision measurement while simplifying pack assembly. These designs improve serviceability and lay the groundwork for over-the-air BMS firmware updates, a key requirement for software-defined vehicles. Rapid uptake of wireless units is therefore set to enlarge the automotive battery management system market over the medium term.

Soaring demand for LFP chemistry requiring advanced active balancing

LFP’s flat discharge profile complicates SOC estimation, pushing vendors to integrate multi-physics sensors, adaptive Kalman filtering, and active balancing circuits. CATL’s 1,000-km Shenxing PLUS cell illustrates that performance gaps are closing, yet stable voltage still hampers traditional monitoring.[2]CATL, “Shenxing PLUS LFP Battery Delivers 1,000 km Range,” catl.com Suppliers delivering hardware-agnostic algorithms capable of handling cell-to-cell drift secure a premium in the automotive battery management system market, particularly for commercial fleets that value safety and low total cost of ownership.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Thermal-runaway recalls Raising Warranty Reserves | -2.7% | North America, Global | Short term (≤ 2 years) |

| Acute Power-Semiconductor Shortages | -2.2% | APAC production hubs | Short term (≤ 2 years) |

| Post-2027 EU Battery-passport Traceability Overheads | -1.5% | EU, export markets | Medium term (2-4 years) |

| AI-based Predictive BMS still Lacks Functional-safety Certification | -1.3% | Global premium segments | Long term (≥ 4 years) |

Source: Mordor Intelligence

Thermal-runaway recalls raising warranty reserves

High-profile fire events have led to sizable recalls, forcing automakers to boost warranty accruals and adopt conservative pack design. Samsung SDI’s multi-brand recall and Hyundai Mobis’ development of self-extinguishing modules underscore industry urgency. Added cost for insulation, fire suppression, and redundant sensors can slow deployment of experimental BMS functions, tempering near-term growth in the automotive battery management system market.

Acute power-semiconductor shortages

Shortfalls in IGBTs and high-current MOSFETs are disrupting the production of active balancing boards, resulting in redesigns involving secondary suppliers and increased procurement costs. BMS vendors relying on single-sourced dies or legacy lithography nodes have encountered schedule delays. While fabs in Japan, Malaysia, and the US are expanding capacity, limited availability continues to be a challenge that hampers volume ramp-ups for the automotive battery management system market over the next one to two years.

Segment Analysis

By Component: Integration Intensifies around Battery ICs

Battery Sensors captured 35.41% of the automotive battery management system market share in 2024, and the segment is forecast to post a 24.66% CAGR through 2030. Wider deployment of multi-physics sensing, covering temperature, pressure, off-gas, and humidity, allows OEMs to move from passive protection toward real-time predictive diagnostics. Adoption accelerates as regulators demand enhanced thermal-runaway detection and as fleet operators seek granular data to optimize duty cycles and warranty coverage. Integrating CO₂ and H₂ sensors into module-level boards improves early-warning capabilities, helping avoid costly recalls and downtime. As EV packs scale above 800 V, high-resolution shunt and Hall-effect sensors become indispensable for accurate state-of-charge and state-of-health estimation, cementing the segment’s long-term expansion path.

Tight cell-level voltage accuracy, now reaching ±2 mV, enables finer charge balancing and extended pack life, making IC precision a decisive purchase criterion. Leading chipmakers have fused measurement, balancing, and communication blocks onto single dies, shrinking board footprints and simplifying automotive qualifications. The residual “Other electronics and materials” bucket, encompassing thermally conductive gap fillers, aerogel sheets, and phase-change composites, continues to broaden as energy density rises, calling for superior heat-spreading and insulation solutions.

Note: Segment shares of all individual segments available upon report purchase

By Topology: Modular Dominance with Wireless Momentum

In 2024, Modular arrangements accounted for 48.95% of the automotive battery management system market share, reflecting OEM preference for scalable sub-battery modules that can be rearranged without wholesale redesign. Box-level isolation of sensing and actuation delivers fault tolerance suited to commercial fleets and high-utilization ride-hailing vehicles. Incremental hardware blocks also facilitate rapid line-side replacement, lifting vehicle uptime.

Wireless designs are scaling rapidly, showing a 35.17% CAGR across 2025-2030 as antenna miniaturization, secure mesh protocols, and certified RF stacks reach production maturity. Eliminating daisy-chain harnesses cuts pack weight and opens valuable cubic centimeters for active cooling plates or extra cells. Centralized topologies continue in entry-price passenger cars, where minimal components trump expandability, whereas niche distributed architectures meet extreme redundancy mandates in motorsports and aerospace crossover programs, cushioning product diversity inside the automotive battery management system market.

By Propulsion Type: BEV Lead Spurs FCEV Uptake

Battery Electric Vehicles, responsible for 72.70% of sector revenue in 2024, have set the benchmark for pack capacity, thermal loads, and software update cadence, creating scale economies for BMS suppliers. High-energy packs demand multi-layer monitoring, driving continual firmware revisions that validate over-the-air workflows across the automotive battery management system market.

Fuel-Cell Electric Vehicles, although smaller in absolute volumes, post the fastest 37.84% CAGR as automakers use hybrid stacks that merge ultra-capacitors, hydrogen cells, and buffer batteries. These mixed energy architectures need BMS units adept at juggling transient loads, cold-start behavior, and hydrogen safety norms. The Hybrid Electric and Plug-in Hybrid segments offer interim revenue, allowing suppliers to validate algorithms in varied duty cycles before full BEV deployment.

Note: Segment shares of all individual segments available upon report purchase

By Vehicle Type: Passenger Cars Scale While Commercial Fleets Tighten Specs

Passenger Cars produced both the largest 54.61% revenue slice and a robust 25.26% CAGR, driven by mainstream adoption across compact and mid-size classes. High unit counts spread R&D cost, letting suppliers amortize ASIL-D compliance, secure bootloaders, and advanced diagnostics. As EV options proliferate in sub-USD 25,000 brackets, OEMs expect BMS features once reserved for premium trims, broadening total addressable demand inside the automotive battery management system market.

Light Commercial Vehicles benefit from passenger-car technology trickle-down yet require extended duty-cycle validation, while Medium and Heavy Commercial Vehicles necessitate ruggedized casings, redundant contactors, and fleet telematics tie-ins. Two- and Three-Wheelers in Southeast Asia and Africa prize stripped-down BMS boards with essential safety gates at rock-bottom prices, sustaining volume even if per-unit revenue is thin. Specialty off-highway equipment deploys enhanced thermal envelopes and wide-temperature electronics that later migrate into mainstream cars, illustrating cross-segment innovation flow.

Geography Analysis

Asia-Pacific retained a commanding 61.33% share of the automotive battery management system market in 2024. China’s vertically integrated battery value chain—from upstream refining to final vehicle assembly—compresses cost structures and quickens design iterations. Government purchase incentives, favorable license-plate policies in megacities, and a mature charging ecosystem lift EV penetration and reinforce BMS unit shipments. Supply-chain leverage even extends to Europe and North America, as Chinese cell and module suppliers open factories in Poland, Hungary, and Nevada to secure tariff-free access and shorten logistics lanes.

The Middle East and Africa region, although emerging from a low base, is the fastest-growing region with a 27.55% CAGR through 2030. Dubai, Riyadh, and Cairo are rolling out e-bus corridors and last-mile delivery electrification targets that demand heat-tolerant BMS designs. Public-private alliances channel investment into grid-tied battery storage, creating adjacent sales for repurposed vehicle packs and second-life BMS software.

North America gains momentum as the Inflation Reduction Act galvanizes domestic cell and module manufacturing. Investments by BMW, Toyota, and Hyundai in the Carolinas, Georgia, and Ontario shrink reliance on Asian imports and underpin local sourcing of BMS boards. Europe remains a regulatory trailblazer, with the upcoming battery passport pushing traceability features that increase system complexity and software content. Such requirements elevate per-vehicle revenue and differentiate suppliers ready with secure cloud pipelines, sustaining a healthy overall outlook for the automotive battery management system market.

Competitive Landscape

Competition is moderate, featuring established semiconductor houses, niche software players, and OEM in-house units. Texas Instruments, Analog Devices, and NXP anchor the precision measurement field, leveraging decades of quality-management know-how and deep functional-safety portfolios. Their reference designs shorten OEM verification time, preserving market relevance even as price pressure mounts.

Software-oriented challengers such as Eatron Technologies and Twaice promote edge analytics and physics-based digital twins capable of predicting remaining useful life. These firms partner with cloud hyperscalers to offer subscription models tied to fleet uptime, injecting recurring revenue streams into the automotive battery management system market. OEMs, intent on owning battery IP, have launched joint ASIC design centers; Volkswagen’s Cariad venture, Renault’s Ampere spin-off, and Stellantis’ efforts with Foxconn illustrate vertical integration momentum.

Wireless BMS certification has emerged as a niche capability. Test-equipment specialists like Rohde & Schwarz provide RF compliance suites, while hardware vendors bundle over-the-air update frameworks to meet ISO 21434 threat analysis.[3]Rohde & Schwarz, “RF Test Solution for Automotive Wireless BMS,” rohde-schwarz.com Material innovators developing ceramic-filled gap pads and intumescent coatings complete the ecosystem, creating a multi-faceted playing field where electronic, software, and materials science skills intersect.

Automotive Battery Management Systems Industry Leaders

-

LG Energy Solution

-

Panasonic (Ficosa)

-

CATL

-

Robert Bosch GmbH

-

Continental AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Eberspacher and Farasis Energy forged a partnership around low-voltage automotive batteries that combines ASIL-C-rated 12 V BMS expertise with high-power LFP cells.

- November 2024: NXP introduced an ultra-wideband wireless BMS that eliminates 90% of wiring harnesses and meets ISO 21434 CAL-4, opening OEM evaluations in Q2 2025.

- August 2024: LG Energy Solution launched a battery safety diagnostics software line, widening its reach into BMS and fleet monitoring.

- June 2024: About:Energy and STMicroelectronics unveiled a demonstrator merging Voltt battery data with ST’s automotive microcontrollers to help OEMs build in-house BMS solutions.

Global Automotive Battery Management Systems Market Report Scope

A battery management system or battery control unit is one of the essential power electronic modules of automobiles. It monitors and controls the charging and discharging processes of the battery pack, thereby enhancing the battery's lifespan by avoiding any damage risk due to overcharging and over-discharging situations.

The automotive battery management system market is segmented by components, propulsion type, vehicle type, and geography. The market is segmented by components into battery IC, sensors, and other components (electronics and materials used in BMS). By propulsion type, the market is segmented into IC engine vehicles and electric vehicles (HEV, PHEV, and BEV). The market is segmented by vehicle type into passenger cars and commercial vehicles. The market is segmented by geography into North America, Europe, Asia-Pacific, and the Rest of the World.

The report offers market size and forecasts for the market in value (USD) for all the above segments.

| By Component | Battery IC | ||

| Battery Sensors | |||

| Other Electronics and Materials | |||

| By Topology | Centralized | ||

| Modular | |||

| Distributed | |||

| Wireless | |||

| By Propulsion Type | Hybrid Electric Vehicle (HEV) | ||

| Plug-in Hybrid Electric Vehicle (PHEV) | |||

| Battery Electric Vehicle (BEV) | |||

| Fuel-Cell Electric Vehicle (FCEV) | |||

| By Vehicle Type | Passenger Cars | ||

| Light Commercial Vehicles | |||

| Medium and Heavy Commercial Vehicles | |||

| Two and Three-Wheelers | |||

| Off-Highway and Specialty Vehicles | |||

| By Geography | North America | United States | |

| Canada | |||

| Rest of North America | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Spain | |||

| Italy | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Saudi Arabia | ||

| United Arab Emirates | |||

| Turkey | |||

| Egypt | |||

| South Africa | |||

| Rest of Middle East and Africa | |||

| Battery IC |

| Battery Sensors |

| Other Electronics and Materials |

| Centralized |

| Modular |

| Distributed |

| Wireless |

| Hybrid Electric Vehicle (HEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Battery Electric Vehicle (BEV) |

| Fuel-Cell Electric Vehicle (FCEV) |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Two and Three-Wheelers |

| Off-Highway and Specialty Vehicles |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Spain | |

| Italy | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

Key Questions Answered in the Report

What is the projected value of the automotive battery management system market by 2030?

The market is expected to reach USD 43.03 billion in 2030, growing at a 23.12% CAGR from 2025.

Which component currently dominates the automotive battery management system market?

Battery Sensors lead the field, accounting for 35.41% of 2024 revenue thanks to their essential role in precise cell monitoring.

Why are wireless topologies gaining traction in battery management systems?

Wireless architecture removes bulky wiring harnesses, cut pack weight, and support flexible module layouts while meeting new cybersecurity mandates.

Which region is forecast to grow the fastest in the automotive battery management system market?

The Middle East and Africa is projected to expand at a 27.55% CAGR between 2025 and 2030 due to new e-mobility programs and infrastructure investment.

Page last updated on: June 27, 2025