Auto-Boxing Technology Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

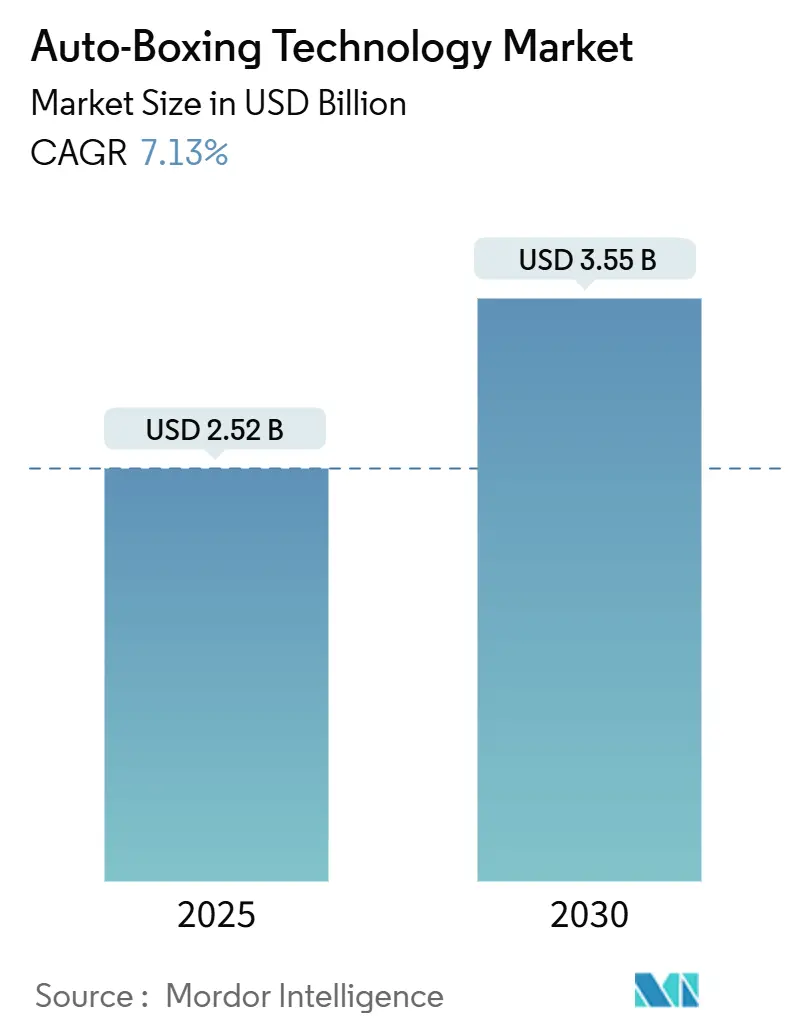

| Market Size (2025) | USD 2.52 Billion |

| Market Size (2030) | USD 3.55 Billion |

| Growth Rate (2025 - 2030) | 7.13% CAGR |

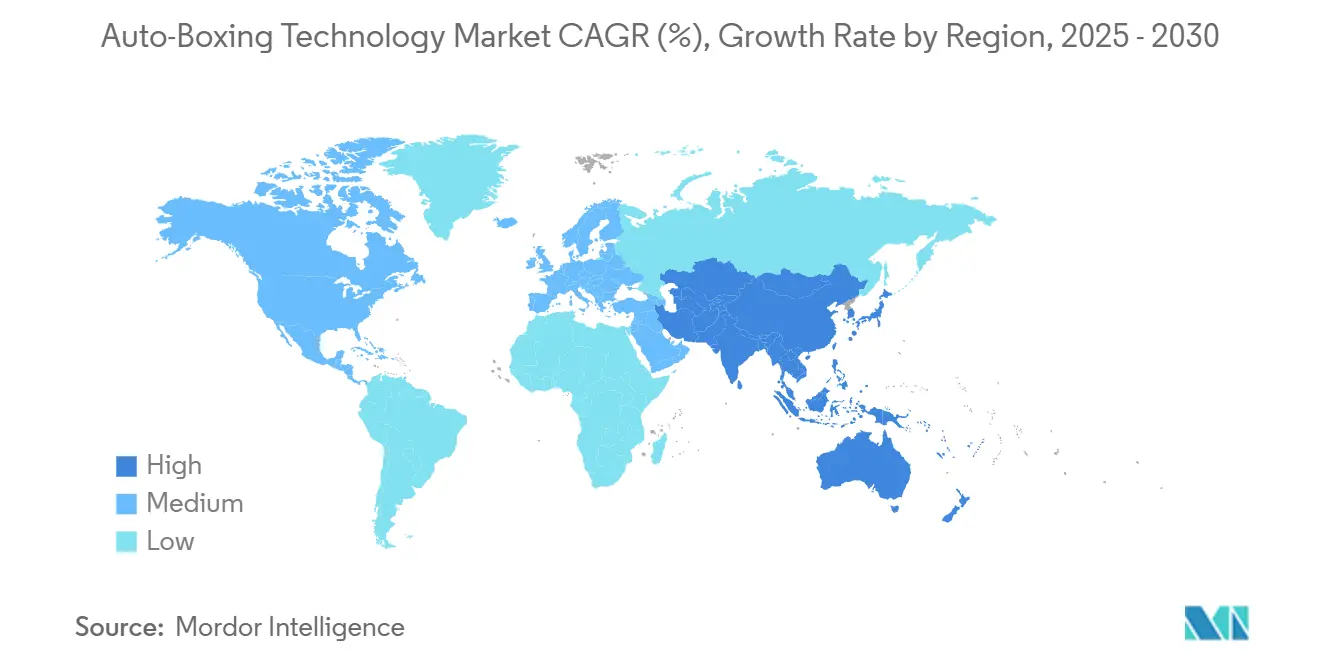

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

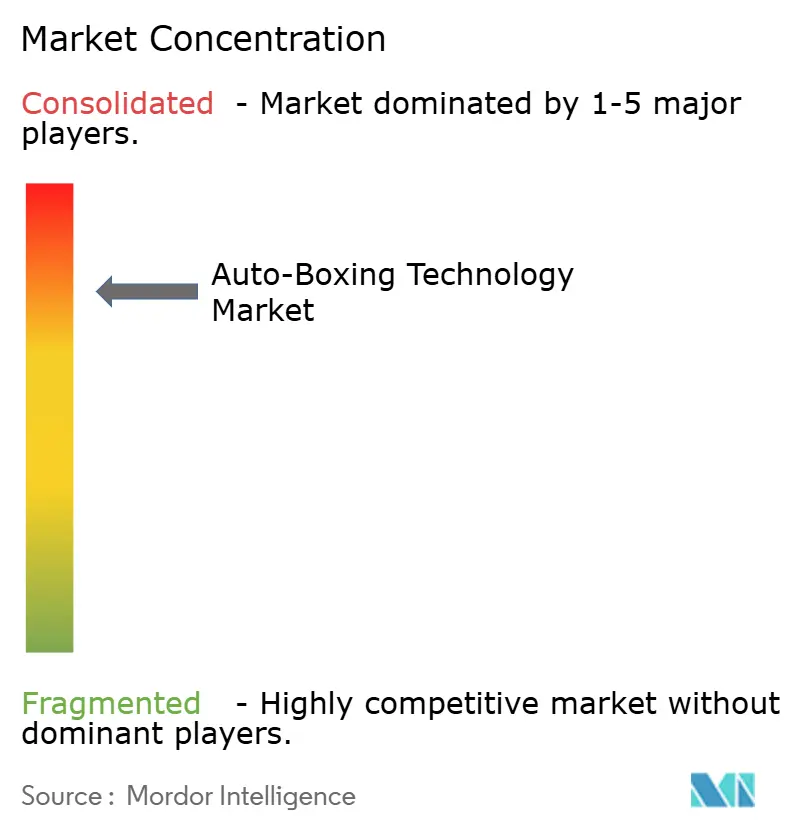

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Auto-Boxing Technology Market Analysis by Mordor Intelligence

The auto-boxing technology market size stands at USD 2.52 billion in 2025 and is projected to reach USD 3.55 billion by 2030, translating into a 7.13% CAGR over the forecast period. Accelerating e-commerce order volumes, rising labor costs in fulfillment centers, and heightened sustainability mandates are converging to strengthen the return on investment for right-sized, automated box-making solutions. Vendors are integrating AI-powered dimensioning cameras with warehouse management systems to improve throughput above 800 packs per hour while cutting corrugate usage by up to 40%. North America retains demand leadership through large-scale deployments by major online retailers, whereas Asia-Pacific records the fastest revenue expansion on the back of logistics infrastructure build-out in China, India, and Southeast Asian economies. Competitive strategies now revolve around end-to-end software integration, patent-protected computer vision, and subscription-based corrugate supply programs that lock in long-term consumable revenues for equipment suppliers.

Key Report Takeaways

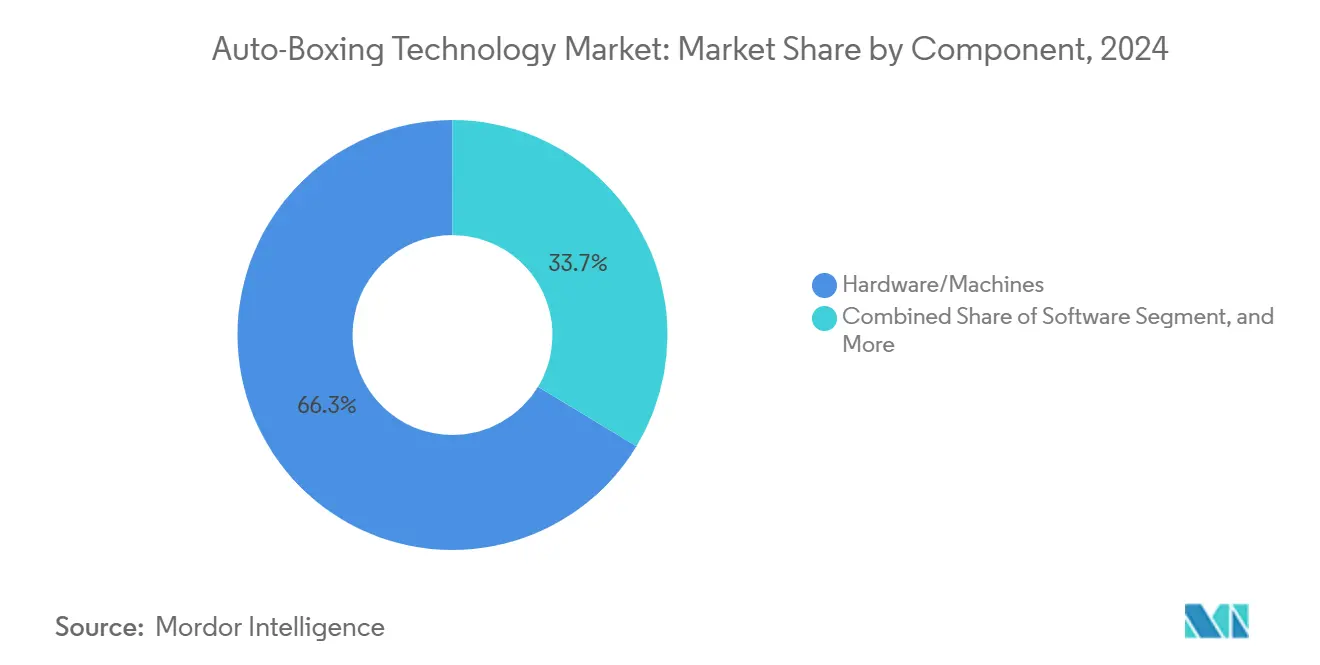

- By component, hardware and machines commanded 66.34% of the auto-boxing technology market share in 2024, while software captured the highest forecast growth at 8.67% CAGR to 2030.

- By machine type, fanfold-fed systems led with 44.32% revenue share in 2024; dual-mode box-and-mailer platforms are projected to expand at an 8.23% CAGR through 2030.

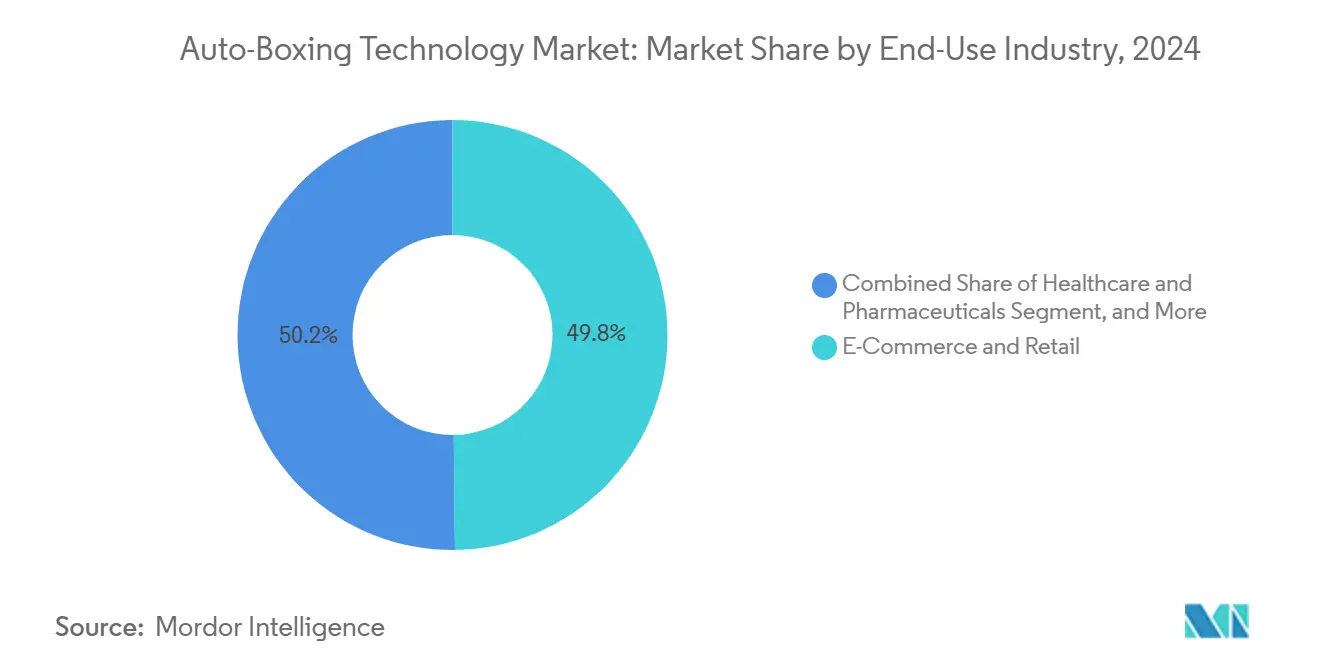

- By end-use, e-commerce and retail accounted for 49.82% of the auto-boxing technology market size in 2024; healthcare and pharmaceuticals exhibit the fastest expansion at 7.29% CAGR to 2030.

- By throughput capacity, high-speed systems above 800 packs per hour held 47.83% revenue share in 2024 and will advance at an 8.93% CAGR through 2030.

- By geography, North America retained 33.76% regional share in 2024, whereas Asia-Pacific is forecast to post a 7.76% CAGR to 2030.

Global Auto-Boxing Technology Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Explosive Growth of E-Commerce Order Volumes | +2.8% | Global - strongest in North America and Asia-Pacific | Short term (≤ 2 years) |

| Rising Labor Cost and Warehouse Automation Push | +1.9% | North America and Europe - spillover to Asia-Pacific | Medium term (2-4 years) |

| Sustainability Pressures to Reduce Corrugated Waste | +1.2% | Europe and North America - expanding to Asia-Pacific | Long term (≥ 4 years) |

| Shift Toward Right-Sized Packaging for Shipping Savings | +1.5% | Global - high-volume e-commerce markets | Medium term (2-4 years) |

| Emergence of Corrugate-as-a-Service Subscription Models | +0.8% | North America and Europe | Long term (≥ 4 years) |

| Integration of AI-Powered Box Dimensioning Cameras | +1.1% | Global - led by technology-advanced markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Explosive Growth of E-Commerce Order Volumes

Peak-season online orders now exceed baseline levels by more than 300%, exposing capacity gaps in manual packing stations.[1]Packsize International, “Right-Sized Packaging Solutions,” packsize.com High-speed auto-boxing systems capable of 1,100 orders per hour allow fulfillment operators to meet service-level agreements without adding temporary labor. Real-time integration with order management platforms ensures dynamic box selection that includes shipping costs and improves customer experience metrics. As omnichannel strategies increase SKU variety, automated dimensioning and cut-to-fit carton production have shifted from optional upgrades to operational necessities in large fulfillment centers. The resulting productivity gains position the auto-boxing technology market as a core pillar of warehouse automation roadmaps for retailers and third-party logistics providers.

Rising Labor Cost and Warehouse Automation Push

Hourly warehouse wages in the United States rose 15% in 2024, compressing margins for parcel fulfillment operations. Auto-boxing reduces headcount in packaging cells by up to 60% while enabling lights-out shifts during overnight sorting windows.[2]CMC SpA, “CartonWrap Series Specification,” cmcwrapping.com Standardized machine interfaces link packaging lines with autonomous mobile robots and sortation systems, further minimizing manual touches and cumulative ergonomic injuries. Operators benefit from predictable, 24-hour asset utilization that shields them from labor-market volatility and union-related work stoppages. These savings accelerate the capital payback curve to fewer than 30 months for high-volume sites, making automation financially compelling despite elevated interest rates.

Sustainability Pressures to Reduce Corrugated Waste

The European Union’s Regulation 2025/40 caps empty space in consumer shipments at 30% and mandates 65% recycled content, forcing retailers to abandon one-size-fits-all cartons.[3]European Commission, “Regulation 2025/40 on Packaging and Packaging Waste,” europa.eu Right-sized packaging cuts corrugate usage by up to 26 kg per 1,000 parcels and lowers volumetric freight charges by 20-40%. Major brands now tie executive bonuses to packaging emission reductions, which drives procurement of dimension-on-demand systems in regional distribution hubs. Automated box makers also improve recyclability by eliminating plastic void fill, meeting retailer pledges to ship “plastic-free by 2030.” As sustainability audits become part of RFP scoring for logistics contracts, fulfillment providers with advanced auto-boxing capabilities gain competitive differentiation.

Shift Toward Right-Sized Packaging for Shipping Savings

Dimensional-weight billing from global carriers charges for either actual or volumetric weight, whichever is higher, turning excess air into a direct profit leak. Predictive algorithms inside modern auto-boxing equipment calculate the lowest-cost carton footprint for each SKU bundle, reducing shipping expenses by 15-20% per parcel. With freight costs frequently outstripping the value of the product in low-price segments, right-sizing is now a CFO-level mandate. AI-enabled systems anticipate common order profiles, pre-score fanfold lengths, and trigger dynamic scheduling to maintain continuous flow, especially during seasonal spikes. The measurable bottom-line impact has made carton-on-demand equipment a standard line item in new fulfillment center construction budgets across the auto-boxing technology market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Expenditure of Auto-Boxing Systems | −1.8% | Global - greatest on SMEs | Short term (≤ 2 years) |

| Limited Compatibility with Irregularly Shaped SKUs | −0.9% | Global - specialty goods markets | Medium term (2-4 years) |

| Fanfold Corrugate Supply Chain Bottlenecks | −1.2% | Global - acute in Asia-Pacific | Short term (≤ 2 years) |

| Cybersecurity Concerns in Connected Packaging Lines | −0.7% | Developed markets with high IoT adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure of Auto-Boxing Systems

Comprehensive lines integrating scanner tunnels, multi-length fanfold unwinders, and conveyor interfaces range from USD 150,000 to more than USD 1 million, making financing a hurdle for mid-tier merchants. Up-front outlays double when facility retrofits require reinforced flooring, taller mezzanines, or power upgrades. Proprietary corrugate subscriptions, while stabilizing supply, add long-term consumables commitments that inflate the total cost of ownership. Equipment makers now partner with leasing firms and offer usage-based pricing, yet the payback period for low-volume sites can still exceed 48 months, slowing widespread penetration despite proven savings in high-throughput environments.

Fanfold Corrugate Supply Chain Bottlenecks

Global container shortages and mill rationalization constrained fanfold corrugate output in early 2025, lengthening lead times to 14 weeks in some Asian ports. Logistics operators in India and Southeast Asia reported temporary machine idling due to material deficits, eroding the reliability of automated lines that rely on continuous feedstock. To mitigate interruptions, retailers are multi-sourcing corrugate and installing sheet-fed backup modules, yet capacity mismatches persist until new fanfold conversion plants come online in 2027. Although suppliers have announced forward-buy programs, material volatility remains a short-term drag on adoption across the auto-boxing technology market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Accelerates Data-Driven Packaging

Hardware and machines commanded 66.34% revenue in 2024 as capital spending prioritized mechanical throughput. Software, however, is projected to outpace at an 8.67% CAGR, reflecting rising demand for AI dimensioning, predictive maintenance, and cloud-based optimization dashboards. Warehouse operators view algorithmic carton selection as a strategic lever, linking packaging to carrier APIs and carbon accounting systems for real-time cost and emissions reporting. Services such as system health monitoring and operator certification programs expand steadily, underpinning recurring revenue models that improve vendor profitability. Collectively, these trends reinforce the platform orientation of the auto-boxing technology market, where software orchestrates material, labor, and freight into a single decision loop.

The software layer also enables remote diagnostics that reduce downtime by 18 hours per year on average, a critical performance metric for high-volume e-commerce hubs. Vendors offer API toolkits that embed cartonization logic into ERP customizations, shortening integration timelines from months to weeks. As fulfillment networks regionalize to maintain next-day delivery promises, centrally managed configuration templates push standardized packaging rules to multiple sites in minutes. Consequently, the auto-boxing technology market gains resiliency and scalability, positioning software vendors for cross-sell opportunities in adjacent automation domains, such as in-line labeling and robotic palletizing.

By Machine Type: Dual-Mode Flexibility Gains Momentum

Fanfold-fed systems captured 44.32% share and remain staples in large fulfillment operations due to continuous-feed efficiency. Yet dual-mode box-and-mailer machines, blending fanfold precision with poly-mailer agility, will expand at an 8.23% CAGR. Forward-thinking retailers prefer platforms that seamlessly pivot between fragile electronics and soft goods without upstream reconfiguration. Integrated auto-packaging lines that bundle dimensioners, printers, and sealing units see growing appeal among brown-field sites that lack the space for multiple standalone systems. Sheet-fed models persist in premium applications requiring pristine print fidelity, including luxury cosmetics and high-end electronics.

Dual-mode adoption also rises because postal authorities surcharge rigid cartons under certain volumetric thresholds, whereas flexible mailers traverse at lower rates. New vision modules recognize deformable SKU profiles and signal the machine to switch media mid-stream, sustaining output above 700 parcels per hour. As parcel mix complexity intensifies, equipment flexibility becomes a procurement criterion equal to throughput, solidifying dual-mode innovation as a competitive differentiator across the auto-boxing technology market.

By End-Use Industry: Compliance Spurs Healthcare Uptake

E-commerce and retail channels represented 49.82% of the auto-boxing technology market size in 2024 on the strength of surging direct-to-consumer volumes. Third-party logistics firms followed, attracted by the prospect of standardized, high-margin packaging services that differentiate their bids for omnichannel contracts. Electronics brands leverage auto-boxing to minimize transit damage for tablets and peripherals while maintaining brand aesthetics. Healthcare and pharmaceuticals, though smaller in absolute dollars, will expand at a 7.29% CAGR through 2030 as drug traceability and cold-chain validation drive investment in validated, audit-ready packaging lines.

Pharmaceutical shippers appreciate the audit trail offered by computerized dimension logs and bar-coded fanfold usage that align with Good Manufacturing Practice requirements. When paired with RFID temperature monitors, auto-boxing solutions create end-to-end visibility crucial for biologics. Furthermore, patient-centric delivery models, including specialty pharmacy home shipments, rely on consistent carton integrity to protect drug efficacy, accelerating adoption across the auto-boxing technology market.

By Throughput Capacity: High-Speed Systems Dominate ROI Math

High-speed lines processing more than 800 parcels per hour owned 47.83% revenue in 2024 and are forecast to expand at 8.93% CAGR, illustrating the economies of scale when throughput consolidates in mega-depots. Medium speeds serve regional hubs, balancing volume and flexibility, while low-throughput units cater to boutique brands or pilot deployments. Operators gravitate to high-speed platforms because labor offset and shipping savings accumulate fastest at volume, driving a 27-month average payback compared with 40 months for mid-range systems.

New high-speed releases feature motion-control servos and non-contact glue systems that reduce wear, pushing mean time between failures above 7,500 run hours. Software overlays predict fanfold replenishment windows and preload supply-tower carts during micro-lulls, maintaining 98% overall equipment effectiveness. These capabilities align with the auto-boxing technology market imperative for resilience during peak Cyber Week loads, where any downtime translates directly into lost sales and brand damage.

Geography Analysis

North America held a 33.76% share in 2024 on the strength of deep e-commerce penetration, robust parcel networks, and early adoption of warehouse robotics. U.S. fulfillment majors integrate auto-boxing with autonomous mobile robots and goods-to-person systems, setting performance benchmarks copied globally. Regulatory focus on packaging landfill diversion in states such as California further accelerates investment in right-sizing. Canada sees rising demand tied to cross-border e-commerce and competitive pressures from U.S. retailers, while Mexico leverages nearshoring to install auto-boxing lines in export-oriented manufacturing parks.

Asia-Pacific is the fastest-growing region, registering a 7.76% CAGR through 2030, mirroring rapid digital shopping adoption and government-backed logistics infrastructure projects. China’s national plan for smart logistics subsidizes automated packaging in bonded warehouses, propelling widespread deployment in the Pearl River Delta. India’s Unified Logistics Interface Platform eases integration of auto-boxing data streams with carrier APIs, lowering technology hurdles for domestic merchants. Southeast Asian marketplaces, led by Indonesia and Vietnam, outsource fulfillment to 3PLs that view carton-on-demand as table stakes for marketplace service-level agreements.

Europe follows similar dynamics but is uniquely shaped by stringent circular-economy policy. Germany’s Packaging Act rewards right-sized boxes via reduced eco-fees, prompting fleet retrofits among multichannel retailers. The United Kingdom, now outside the EU but maintaining voluntary carbon targets, is piloting 100% recycled fanfold across several national distribution centers. Southern European markets lag in adoption but are catching up as apparel exporters seek uniform parcel aesthetics when shipping to Northern Europe. Collectively, geography-specific cost pressures and regulatory frameworks sustain diversified growth corridors across the auto-boxing technology market.

Competitive Landscape

Industry concentration is moderate, with the top five vendors estimated to control roughly 60% of global revenue. Packsize’s April 2025 acquisition of Sparck Technologies created a hardware-software powerhouse capable of single-source solutions from dimensioning to carton sealing. CMC strengthens its moat via partnerships with material distributors such as Antalis, amplifying reach in mid-tier markets that lack direct OEM presence. Multivac leverages its dominance in food packaging to cross-sell auto-boxing into regulated verticals, while Mpac Group integrates end-of-line palletizing to offer turnkey automation cells.

White-space opportunities persist in pharmaceutical compliance and in emerging markets, leading vendors to file patents around temperature-resilient corrugate and onboard quality-assurance modules. Smaller specialists still thrive by targeting niche throughput tiers below 300 packs per hour, though high R&D spend poses sustainability challenges, evidenced by Kolbus’s 2024 exit from the segment. Overall, differentiation hinges on software openness, integrated analytics, and consumable business models rather than pure mechanical speed, reflecting the maturation arc of the auto-boxing technology market.

Strategically, players bundle predictive maintenance to minimize unplanned downtime and harmonize warranty coverage across conveyors, scanners, and glue applicators. Supplier-financed leasing and usage-based pricing lower barriers for small merchants, expanding total addressable demand. The competitive narrative now balances consolidation with ecosystem partnerships, signaling a pivot from equipment sales toward lifetime customer value anchored by fanfold and software subscriptions.

Auto-Boxing Technology Industry Leaders

Packsize International LLC

CMC SpA

Sparck Technologies BV

Kolbus GmbH and Co. KG

Kern AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: WestRock expanded its Box On Demand corrugate-subscription service across all North American fulfillment hubs, bundling predictive inventory forecasting and carbon-footprint dashboards for enterprise customers.

- September 2025: CMC SpA unveiled the CartonWrap X platform at PACK EXPO Las Vegas, boosting throughput to 1,300 packs per hour while introducing a modular mailer-conversion attachment for omnichannel retailers.

- June 2025: Sparck Technologies launched its SmartVision 2.0 suite, adding real-time defect detection and energy-optimization algorithms to the CVP Everest and Impack lines.

- April 2025: Packsize International finalized its acquisition of Sparck Technologies BV, creating a combined portfolio that integrates on-demand box production with AI-enabled dimensioning software.

Global Auto-Boxing Technology Market Report Scope

| Hardware/Machines |

| Software |

| Services |

| Fanfold-Fed Box Makers |

| Sheet-Fed Box Makers |

| Dual-Mode Box and Mailer Systems |

| Integrated Auto-Packaging Lines |

| E-Commerce and Retail |

| Third-Party Logistics Providers |

| Electronics and Consumer Goods |

| Healthcare and Pharmaceuticals |

| Automotive and Industrial |

| Other End-Use Industry |

| High-Speed (Above 800 packs/hr) |

| Medium (300-800 packs/hr) |

| Low (Less than 300 packs/hr) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Component | Hardware/Machines | ||

| Software | |||

| Services | |||

| By Machine Type | Fanfold-Fed Box Makers | ||

| Sheet-Fed Box Makers | |||

| Dual-Mode Box and Mailer Systems | |||

| Integrated Auto-Packaging Lines | |||

| By End-Use Industry | E-Commerce and Retail | ||

| Third-Party Logistics Providers | |||

| Electronics and Consumer Goods | |||

| Healthcare and Pharmaceuticals | |||

| Automotive and Industrial | |||

| Other End-Use Industry | |||

| By Throughput Capacity | High-Speed (Above 800 packs/hr) | ||

| Medium (300-800 packs/hr) | |||

| Low (Less than 300 packs/hr) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the auto-boxing technology market?

The auto-boxing technology market size is USD 2.52 billion in 2025 and is forecast to grow to USD 3.55 billion by 2030.

Which component is growing fastest in automated box-making solutions?

Software is expanding at an 8.67% CAGR thanks to AI dimensioning, predictive analytics, and cloud integration features.

Why are high-speed auto-boxing systems favored in large fulfillment centers?

Lines exceeding 800 packs per hour deliver the quickest labor savings and achieve average payback in under 30 months.

How do sustainability regulations influence adoption in Europe?

EU rules limiting empty space and requiring recycled content compel retailers to deploy right-sized, automated packaging lines to avoid compliance penalties.

Which region shows the highest forecast growth?

Asia-Pacific is projected to register a 7.76% CAGR through 2030, driven by e-commerce expansion and logistics modernization.

What recent corporate action reshaped competitive dynamics?

Packsize’s April 2025 acquisition of Sparck Technologies combined advanced computer vision with on-demand carton production, creating a vertically integrated leader.

Page last updated on: