Switzerland Data Center Storage Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

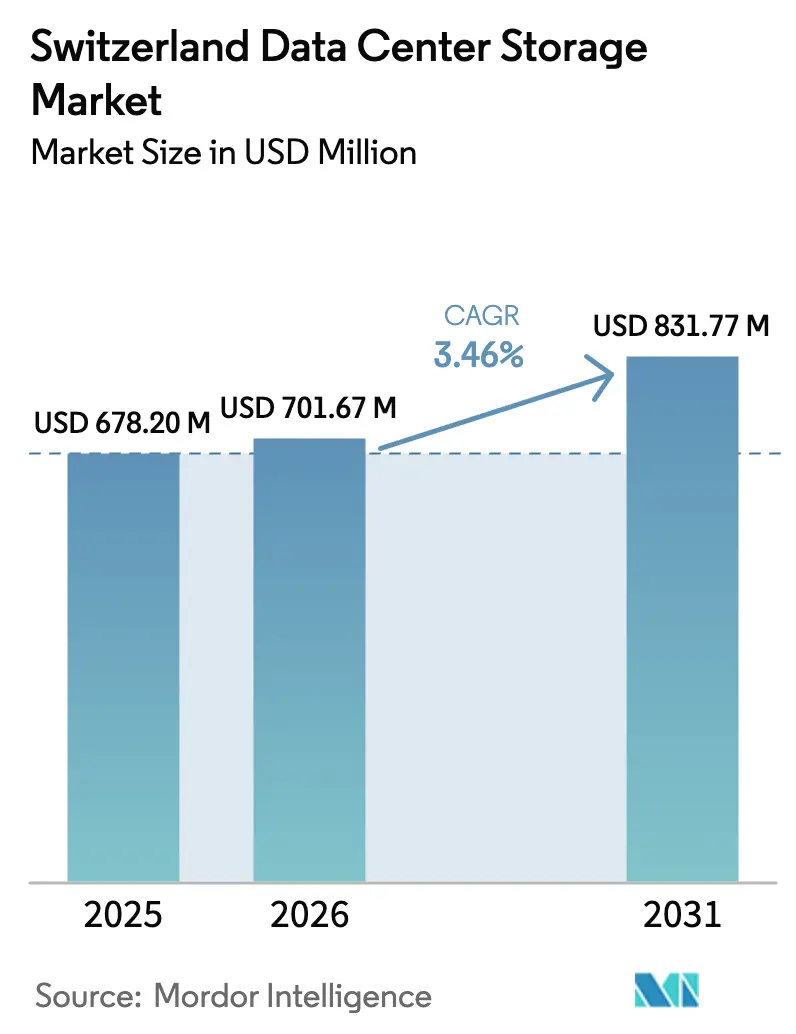

| Base Year Market Size (2025) | USD 678.20 Million |

| Market Size (2026) | USD 701.67 Million |

| Market Size (2031) | USD 831.77 Million |

| Growth Rate (2026 - 2031) | 3.46% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Switzerland Data Center Storage Market Analysis by Mordor Intelligence

Switzerland data center storage market size in 2026 is estimated at USD 701.67 million, growing from 2025 value of USD 678.20 million with 2031 projections showing USD 831.77 million, growing at 3.46% CAGR over 2026-2031. Stable growth arises from enduring demand within financial services, stricter data-sovereignty rules, and a rising preference for sovereign-cloud deployments. Inbound hyperscale capital, most notably Microsoft’s USD 400 million Zurich-Geneva program, amplifies capacity while fueling a shift toward low-latency NVMe architectures. Enterprise buyers weigh escalating electricity tariffs against performance gains, prompting a pivot to all-flash arrays and software-defined designs that fit Switzerland’s high-cost urban footprints. ESG mandates and the revised Federal Act on Data Protection (FADP) further shape procurement, favoring energy-efficient hardware and localized backup services.

Key Report Takeaways

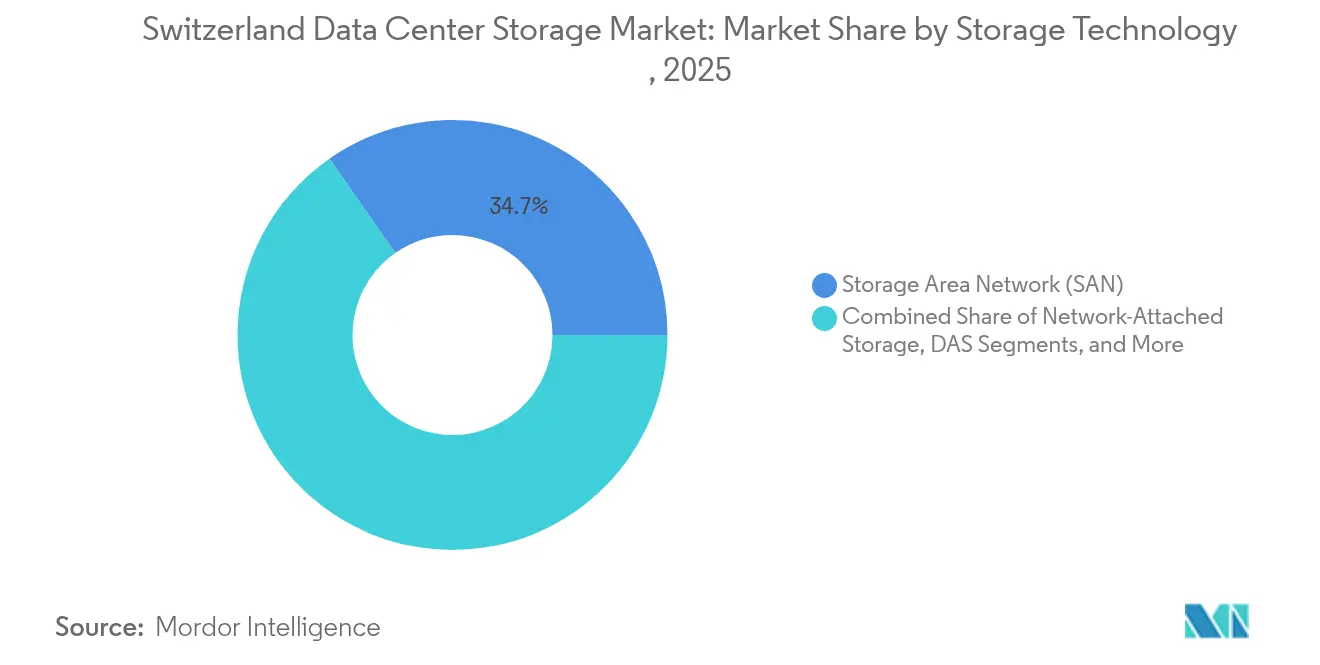

- By storage technology, SAN led with 34.70% of Switzerland's data center storage market share in 2025, whereas NAS is projected to post the fastest 3.62% CAGR through 2031.

- By storage type, traditional HDD arrays accounted for 42.60% of the Switzerland data center storage market size in 2025, while all-flash arrays are set to expand at a 4.05% CAGR to 2031.

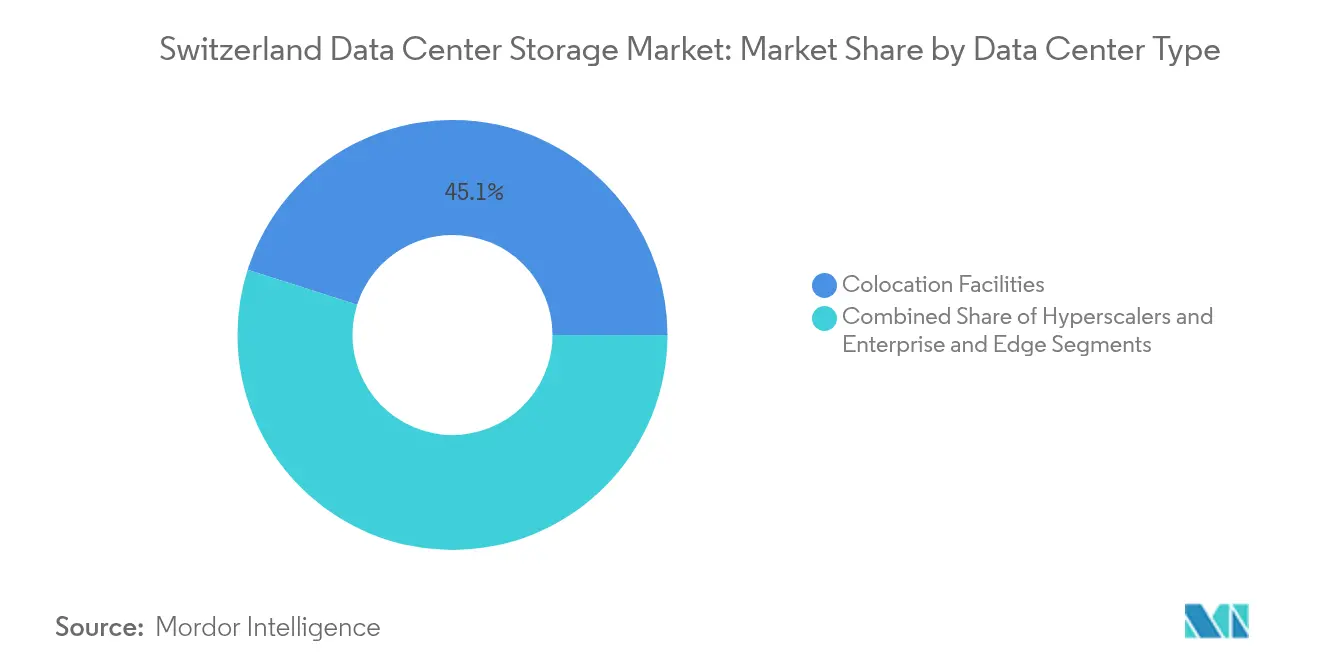

- By data center type, colocation facilities held 45.10% of 2025 revenue, and hyperscalers register the highest 5.18% CAGR over the forecast period.

- By end user, IT & telecommunications controlled 21.05% revenue in 2025, whereas BFSI achieves a leading 5.49% CAGR through 2031.

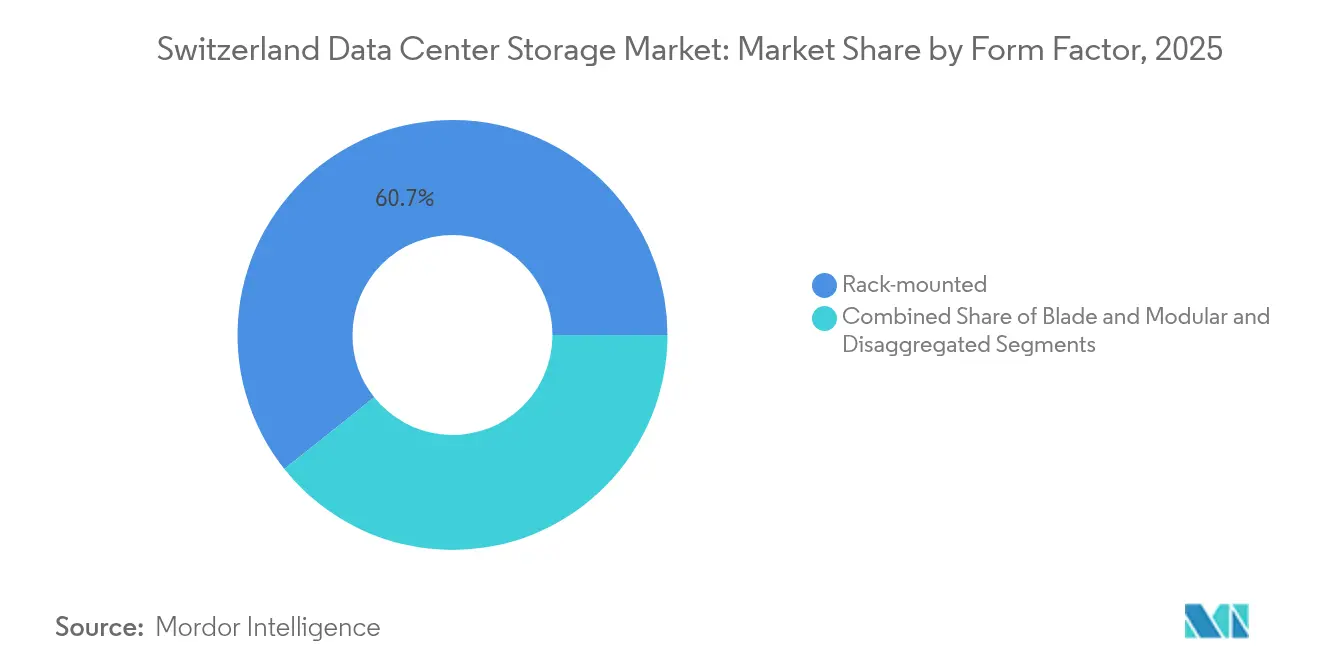

- By form factor, rack-mounted systems captured 60.70% share in 2025, with disaggregated architectures advancing at a 6.05% CAGR.

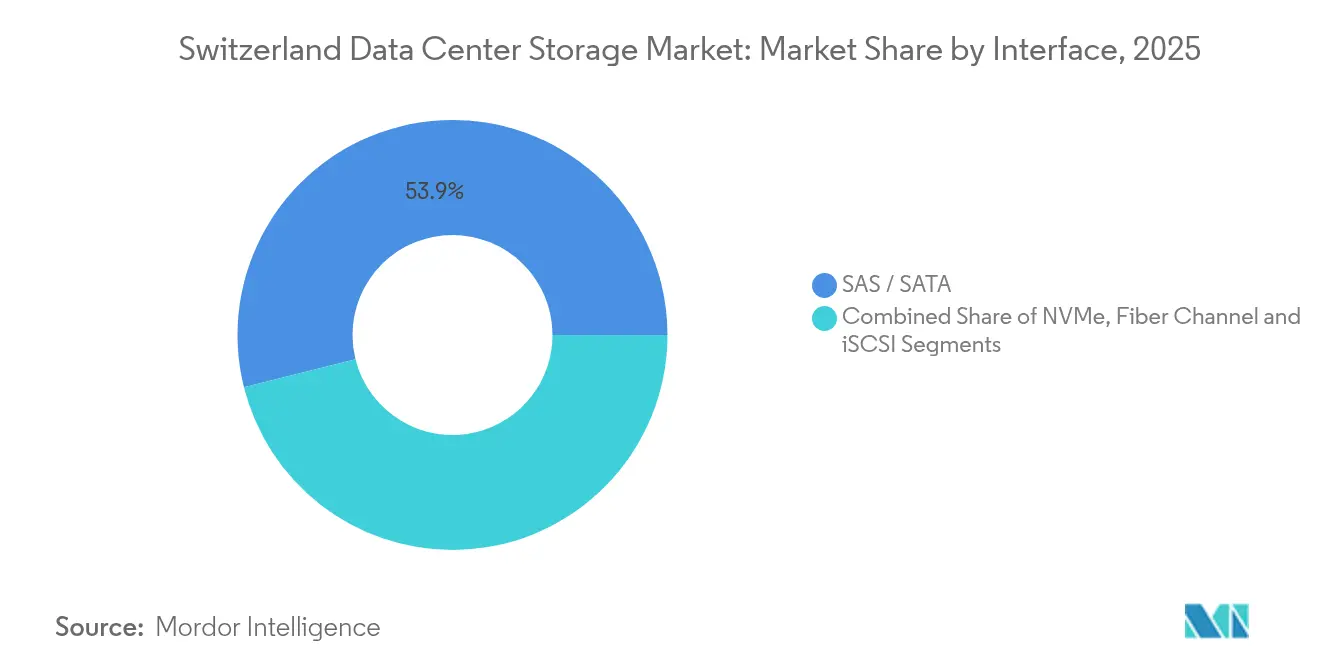

- By interface, SAS/SATA combined for 53.90% revenue in 2025; NVMe rises the quickest at 5.51% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Switzerland Data Center Storage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-first and SaaS adoption surge among Swiss SMEs | +0.8% | National, concentrated in Zurich, Basel, Geneva | Medium term (2-4 years) |

| Edge–data-center build-outs by colocation players | +0.6% | Zurich metro, expanding to Bern, Lausanne | Short term (≤ 2 years) |

| Rapid NVMe-oF roll-outs to reduce latency for fintech workloads | +0.4% | Zurich financial district, Geneva private banking | Short term (≤ 2 years) |

| Favourable data-sovereignty rules attracting hyperscale back-up sites | +0.7% | National, with concentration in Zurich, Geneva | Long term (≥ 4 years) |

| GAIA-X-aligned sovereign-cloud initiative | +0.3% | National, EU cross-border implications | Long term (≥ 4 years) |

| ESG-driven switch to energy-efficient all-flash arrays | +0.5% | National, emphasis on urban centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cloud-First and SaaS Adoption Surge Among Swiss SMEs

Swiss SMEs are migrating workloads to public and hybrid clouds to cut administrative overhead and meet post-pandemic digitization goals. Despite higher public-cloud storage tariffs than private equivalents, firms keep shifting file services and collaboration suites off-premises, driving need for on-premises gateways that synchronize with cloud buckets. The Switzerland data center storage market benefits because hybrid NAS platforms integrate legacy applications while enabling SaaS backup. Analysts note Swiss cloud uptake still trails the United Kingdom and the United States, leaving headroom that sustains infrastructure spend through 2030. Government digitalization programs reinforce the trend by subsidizing SME technology upgrades, stimulating steady demand for modular storage bundles that mesh with SaaS stacks

Edge–Data-Center Build-Outs by Colocation Players

To meet sub-10 ms latency targets in finance and AI inference, colocation vendors are constructing multi-story edge facilities around Zurich’s fiber rings. Green’s 46,000 m² Metro Campus supplies direct on-ramps to 700 global sites, pushing the Switzerland data center storage market toward distributed SSD clusters for edge-to-core data paths.[1]Green Datacenter AG, “Metro Campus Zurich Fact Sheet,” green.chVantage Data Centers’ CHF 370 million Zurich 2 project mirrors this emphasis on proximity and low-latency storage, promising 24 MW for hyperscale tenants. Edge locations stimulate demand for high-density NVMe shelves and erasure-coded object stores that can replicate seamlessly to central campuses.

Rapid NVMe-oF Roll-Outs to Reduce Latency for Fintech Workloads

Banks in Zurich’s Paradeplatz district replace ageing Fibre Channel fabrics with NVMe-over-Fabrics, shrinking read latency tenfold for algorithmic trading. Early pilots at the Swiss National Supercomputing Centre validate microsecond response times, encouraging commercial adoption.[2]Swiss National Supercomputing Centre, “Performance Evaluation of NVMe Systems,” cscs.ch Insurance carrier Suva’s migration to Hitachi VSP 5500 underlines wider enterprise uptake for SAP and analytics acceleration. As real-time risk models mature, the Switzerland data center storage market sees rising attach rates for NVMe shelves, QLC flash, and 100 GbE fabrics

The revised FADP, together with the 2024 Swiss-US Data Privacy Framework, lets certified US firms move data without new contractual safeguards, while retaining stringent local oversight. This regulatory clarity persuaded Microsoft to commit USD 400 million to dual-region expansions that localize AI training datasets for 50,000 Swiss customers. Hyperscale arrivals accelerate the Switzerland data center storage market by buying petabyte-scale object and tape libraries for cold backup tiers and regulatory archives.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited brown-field space in Zurich metro for large scale build-outs | -0.4% | Zurich metropolitan area, spillover to surrounding cantons | Short term (≤ 2 years) |

| Rising electricity tariffs versus neighbouring EU countries | -0.3% | National, acute in urban centers | Medium term (2-4 years) |

| Scarcity of bilingual (DE/FR) storage architects inflates wage bill | -0.2% | National, concentrated in multilingual regions | Long term (≥ 4 years) |

| Stringent Swiss data-privacy rules hindering cross-border replication | -0.3% | National, affecting international operations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Limited Brown-Field Space in Zurich Metro for Large-Scale Build-Outs

Scarce real estate lifts land prices, making new 10 MW-plus footprints economically challenging. Operators respond by stacking data halls vertically and adopting high-density all-flash configurations that squeeze more capacity into smaller floorspace. Green nonetheless broke ground on a 12 MW shell in 2024, accepting higher development costs to remain close to its financial client base. Density constraints steer the Switzerland data center storage market toward software-defined solutions and chassis that reach 25 kW per rack.

Average commercial power now costs 30.49 cents per kWh—well above Germany and France—eroding TCO models for HDD-heavy arrays. The 2024 ‘power-reserve’ levy layered further charges, compelling operators to chase lower PUE values and adopt flash that cuts watt-per-TB ratios. [3]Swisscom AG, “Wankdorf Data Center Sustainability Report,” swisscom.chSwisscom’s Wankdorf site hits a 1.2 PUE and exports waste heat to housing, illustrating the design pivots necessary to control opex. High tariffs temper total capacity growth yet push the Switzerland data center storage market toward premium, energy-efficient gear.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Storage Technology: SAN Dominance Faces NAS Disruption

SAN solutions held 34.70% of the Switzerland data center storage market in 2025, sustained by performance-sensitive banking and ERP stacks. Yet NAS is gaining fastest with a 3.62% CAGR as file-based collaboration and container storage meet hybrid-cloud roadmaps. Enterprises increasingly deploy unified arrays that present block and file services, letting them balance SAN consistency with NAS flexibility across DevOps pipelines.

SAN’s deep integration with Fibre Channel keeps it entrenched in mission-critical cores, but new deployments layer NVMe-oF front-ends to cut latency. Meanwhile, AI training and media workflows fuel NAS clusters that scale linearly and integrate with S3 gateways. The Switzerland data center storage market thus pivots toward platforms capable of switching protocol personality without forklift upgrades, protecting legacy spend while embracing cloud-native growth.

By Storage Type: All-Flash Arrays Challenge HDD Supremacy

Traditional HDD arrays captured 42.60% of Switzerland data center storage market share in 2025, catering to cost-per-TB driven backup and video archives. However, all-flash arrays expand at 4.05% CAGR as ESG rules and power prices elevate watt efficiency as a purchase trigger. Flash’s reliability and inline compression further shrink rack needs, a boon in space-constrained Zurich cages.

Hybrid arrays straddle the divide, blending SSD tiers with capacity SATA drives so operators can phase migrations gradually. Flash penetration deepens as NAND prices soften and quad-level-cell density rises, letting CFOs justify flash for mainstream workloads. The Switzerland data center storage market size for flash is projected to exceed HDD revenue by the late 2020s as operators prioritize TCO over acquisition cost.

By Data Center Type: Hyperscalers Accelerate Past Colocation

Colocation captured 45.10% revenue in 2025, reflecting enterprises’ preference to retain server ownership while offloading facility management. Hyperscalers now post a 5.18% CAGR, enabled by regulatory certainty and enterprise demand for sovereign cloud landing zones. Colos counterbalance by adding build-to-suit halls that let cloud providers park edge nodes within carrier-dense campuses.

Edge facilities proliferate along Zurich fiber loops and satellite cities, allowing fintech, gaming, and Industry 4.0 data to stay within 10 km of users. This distributed pattern pushes the Switzerland data center storage market toward tiered replication, where hot datasets sit at the edge and colder pools live in suburban halls. Vendors selling policy-based movement engines and immutable snapshots see rising traction across both segments.

By End User: BFSI Leads Digital Transformation

IT and telecom providers made up 21.05% of 2025 revenue, supplying hosting and managed services to downstream industries. BFSI, though smaller in base, grows at 5.49% as algorithmic trading, AML analytics, and PSD 2 compliance lift storage IOPS and retention windows. Healthcare follows with rising genomic workloads, and manufacturing expands IoT telemetry capture for predictive maintenance.

Financial institutions push NVMe flash and synchronous metro mirroring to guarantee zero-data-loss. Their governance appetite for on-shore replicas accelerates colocation demand in Zürich and Geneva. Across sectors, the Switzerland data center storage market rewards vendors able to map tier-1 latency expectations to multi-site regulatory constraints.

By Form Factor: Disaggregated Architecture Gains Traction

Rack-mount units dominated 60.70% of deployments in 2025 because they fit standard 19-inch cabinets and allow incremental upgrades. Disaggregated and composable frames, though nascent, clock a 6.05% CAGR, prized for letting operators grow storage independently of compute. Start-ups ship NVMe-oF JBOF (just a bunch of flash) sleds that pool capacity over 100 GbE fabrics, shrinking stranded resources.

As modular adoption rises, procurement tilts toward software-defined controllers running on x86 nodes, decoupling vendor lock-in. Blade and fully integrated boxes still service branch IT rooms, yet the Switzerland data center storage market increasingly favors Lego-style disaggregation that extracts maximum kilowatts per rack footprint in Zurich data halls.

By Interface: NVMe Disrupts Traditional Connectivity

SAS/SATA continued at 53.90% revenue in 2025, buoyed by backward compatibility and affordable drives. NVMe, however, expands 5.51% annually as flash-specific PCIe signalling slashes queue latency, critical for risk-model recalculations. Fibre Channel remains entrenched in heavily audited transaction environments, while iSCSI retains a role for secondary workloads and SMB backups.

Transition paths often involve front-ending existing arrays with NVMe caching or adopting dual-port U.3 drives in new servers. This coexistence demands flexible HBAs and multiprotocol switches. Consequently, the Switzerland data center storage market favors suppliers that bundle NVMe and legacy protocol support within a unified license stack, easing migration anxiety.

Geography Analysis

Zurich remains the epicenter of the Switzerland data center storage market, underpinned by deep capital markets, dense fiber, and an ecosystem of more than 180 carrier points-of-presence. Colocation and cloud operators exploit the city’s proximity to banking clients, positioning low-latency storage clusters within 5 km of core exchanges. Yet limited land and stringent zoning inflate build costs, inviting stacked data-hall designs and premium rack pricing.

Bern, Basel, and Geneva now attract spill-over investments. Swisscom’s CHF 60 million Tier IV Bern site illustrates how secondary hubs cater to government and pharma, harnessing district heating links to reach a 1.2 PUE. Basel’s life-sciences corridor needs petabyte-scale research archives, while Geneva’s concentration of NGOs and private banks demands tamper-proof vaults that align with multi-language compliance.

Cross-border fiber into France, Germany, and Italy positions Swiss facilities as pan-European disaster-recovery refuges. The GAIA-X alliance and federal digital-sovereignty initiatives channel grants toward sovereign-cloud pilots, spurring distributed micro-edge nodes in Lausanne, Lucerne, and St. Gallen. This network diversity encourages tiered data placement strategies—hot datasets near user clusters, colder replicas in hydro-powered Alpine regions—expanding the Switzerland data center storage market footprint beyond Zurich’s urban core.

Competitive Landscape

Competition is moderate, with global majors holding scale advantages while niche specialists address vertical or architectural gaps. Digital Realty’s three CO2-neutral Zurich facilities, totaling 25,100 m², serve 180 customers and 115 carriers, leveraging FINMA RS-18/3 certification to deepen finance penetration. Green and Vantage court the same tenant base but differentiate by offering shell-and-core leases that allow hyperscalers to deploy custom racks.

Sustainability credentials now rank alongside latency and uptime in RFP scoring. Operators advertise waste-heat reuse, hydro power guarantees, and ISO 50001 energy management to win ESG-oriented clients. Vendors consequently emphasize flash arrays that trim kilowatts, and software that powers down idle drives. The Switzerland data center storage market therefore, rewards suppliers linking performance gains with carbon-reduction metrics.

Strategic moves center on ecosystem partnerships. Microsoft binds its sovereign cloud zones to local telecoms for low-latency connectivity, while Dell Technologies teams with Swiss integrators to wrap managed services around PowerStore clusters. Meanwhile, Hitachi and NetApp embed compliance toolkits, simplifying cross-border audits under FADP. Boutique firms specialize in NVMe-oF fabrics, targeting algorithmic-trading enclaves inside Zürich’s banking towers.

Switzerland Data Center Storage Industry Leaders

Dell Technologies

Hewlett Packard Enterprise (HPE)

NetApp Inc.

Huawei Technologies Co. Ltd.

Hitachi Vantara LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Microsoft confirms a USD 400 million expansion for AI-ready data centers near Zurich and Geneva, adding sovereign zones tailored to finance and health.

- December 2024: The Data Protection Commissioner issues fresh FADP cross-border guidance, clarifying contractual clauses for Swiss firms.

- September 2024: The Federal Council rolls out the Swiss-US Data Privacy Framework, streamlining compliant data transfers for certified US entities.

- August 2024: Green starts a 12 MW build within Zurich despite land scarcity, aligning with client demands for metro-proximate racks.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Switzerland data center storage market as the yearly value of on-premise and colocation storage hardware, firmware, and embedded management software, including SAN, NAS, DAS, object, and tape systems, deployed inside Swiss data center facilities. Solutions powering edge-tier pods that are physically hosted within the country are also covered, provided the workload is managed through a Swiss data hall.

Scope exclusion: Household NAS appliances, removable media sold through retail, and storage capacity bundled only as a public-cloud service are not counted.

Segmentation Overview

- By Storage Technology

- Network Attached Storage (NAS)

- Storage Area Network (SAN)

- Direct Attached Storage (DAS)

- Object and Tape Storage

- By Storage Type

- Traditional HDD Arrays

- All-Flash Arrays (AFA)

- Hybrid Storage

- By Data Center Type

- Colocation Facilities

- Hyperscalers/Cloud Service Providers

- Enterprise and Edge

- By End User

- IT and Telecommunication

- BFSI

- Government and Public Sector

- Media and Entertainment

- Healthcare and Life Sciences

- Manufacturing

- By Form Factor

- Rack-mounted

- Blade and Modular

- Disaggregated / Composable

- By Interface

- SAS / SATA

- NVMe

- Fibre Channel and iSCSI

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts held structured calls and short surveys with Swiss colocation operators, IT buyers in banking and pharma, and regional channel distributors; these conversations validated capacity utilization, migration cycles, and discount ladders that are rarely public. Feedback from European storage architects refined our forecast assumptions on NVMe penetration and hybrid-flash refresh rates.

Desk Research

We began with public macro-series from Switzerland's Federal Statistical Office, Comtrade shipment codes 8471-70 and 8471-80, and customs releases that track inbound enterprise storage arrays. Trade association briefs from Digital Switzerland and SNIA Europe, patent trends pulled via Questel, and procurement notices on Tenders Info clarified technology shifts. Company 10-Ks and investor decks supplied ASP hints, while Dow Jones Factiva helped us trace quarterly installation news.

The sources listed above illustrate, not exhaust, the wider pool we leveraged for fact-checking and historical baselining.

Market-Sizing & Forecasting

A top-down demand pool, constructed from data-center floor space, rack density norms, and median GB-per-rack ratios, yielded our initial 2024 spend. Select bottom-up spot checks, such as supplier roll-ups and blended ASP multiplied by sampled unit imports, tempered over- or under-shoots before finalization. Key variables include Switzerland's raised-floor additions, flash-to-HDD mix shift, BFSI data-retention rules after the revised FADP, all-flash average selling price erosion, and energy-linked TCO gains. Multivariate regression, anchored on GDP-deflator-adjusted IT spend and regulated data-sovereignty indices, underpins the 2025-2030 forecast path. Gaps in granular shipment data were bridged using three-point triangulation from distributor volumes, customs tallies, and expert range-checks.

Data Validation & Update Cycle

Every draft model passes an anomaly screen, peer review, and a sign-off from a senior analyst. We refresh figures annually and issue interim tweaks when material events, such as hyperscale investments or sudden tariff shifts, alter fundamentals. A final validation run occurs just before report release so clients receive the most up-to-date baseline.

Why Our Switzerland Data Center Storage Baseline Commands Reliability

Published estimates naturally diverge; scope breadth, refresh cadence, and conversion choices often vary.

According to Mordor Intelligence, clarity on what is and is not counted is the first guardrail against confusion.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 678 M (2025) | Mordor Intelligence | - |

| USD 674 M (2024) | Regional Consultancy A | Uses 2024 as terminal year and excludes object storage refresh, limiting forward comparability |

| USD 1.02 B (2024) | Global Consultancy B | Blends servers, network, and storage into a single IT-infrastructure figure, inflating value versus storage-only scope |

Taken together, the comparison shows that when definitions tighten and local price differentials are applied, our balanced 2025 figure becomes a dependable midpoint clients can trace back to clear variables and reproducible steps.

Key Questions Answered in the Report

What is the current value of the Switzerland data center storage market?

It stands at USD 701.67 million in 2026 and is forecast to reach USD 831.77 million by 2031.

Which segment is growing fastest within the Switzerland data center storage market?

Hyperscalers and cloud service providers expand at a 5.18% CAGR, outpacing other data-center types.

Why are all-flash arrays gaining momentum in Switzerland?

ESG mandates and high power prices push operators toward energy-efficient flash that lowers Watt-per-terabyte costs while boosting performance.

How do Swiss data-sovereignty laws influence storage demand?

The revised FADP and Swiss-US framework compel enterprises to keep sensitive data onshore, creating sustained need for local backup and disaster-recovery capacity.

Page last updated on: