Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2019 - 2024 |

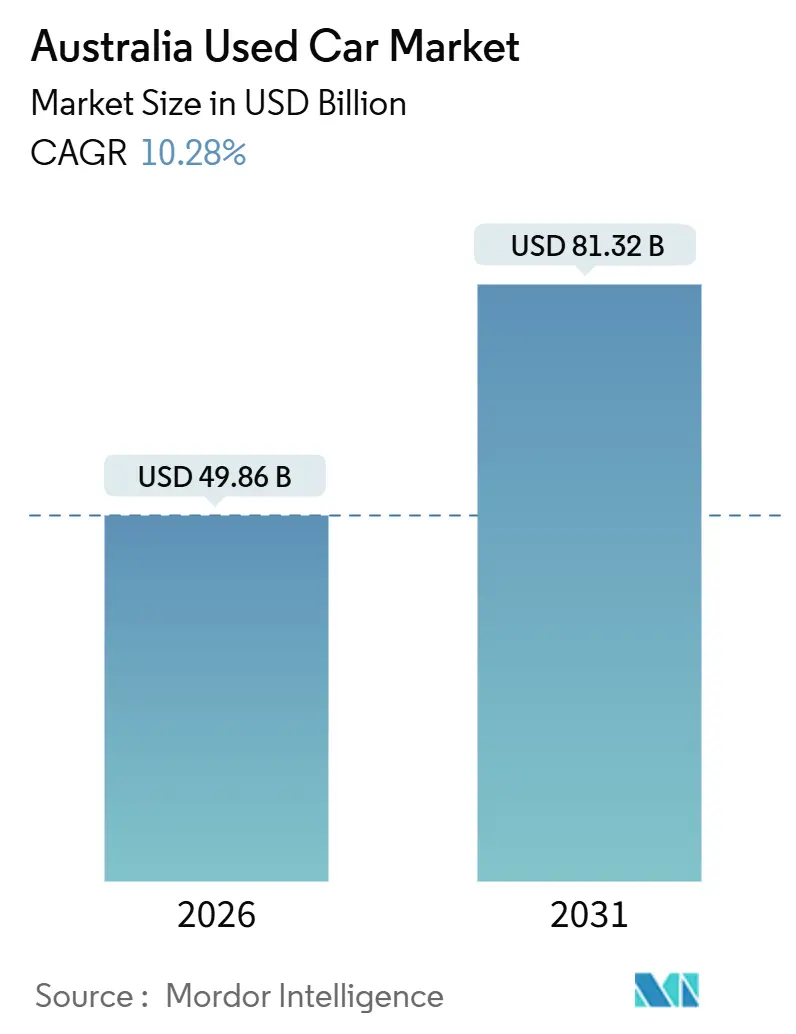

| Market Size (2026) | USD 49.86 Billion |

| Market Size (2031) | USD 81.32 Billion |

| Growth Rate (2026 - 2031) | 10.28% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Used Car Market Analysis by Mordor Intelligence

The Australian used car market size stood at USD 49.86 billion in 2026 and is projected to reach USD 81.32 billion by 2031, reflecting a robust 10.28% CAGR during the forecast window. Rising household migration into outer suburbs, the rapid rollout of certified pre-owned (CPO) programs, and the growing use of algorithm-driven online platforms are collectively increasing transaction velocity and compressing traditional negotiation cycles. Organized vendors are scaling omnichannel storefronts, allowing buyers to secure finance pre-approval and schedule test drives within a single digital journey. Meanwhile, semi-organized independents utilize low-overhead web listings and flexible trade-in terms to close price-sensitive deals. Petrol cars still account for the majority of overall volumes. Still, the current generation of battery-electric vehicles (BEVs) and hybrids is unlocking a new low-emission pool that will enter the secondary market within three to five years. Meanwhile, tightening emissions rules, elevated interstate freight charges, and growing consumer scrutiny of vehicle histories reinforce the premium that verified inventory commands at branded dealerships.

Key Report Takeaways

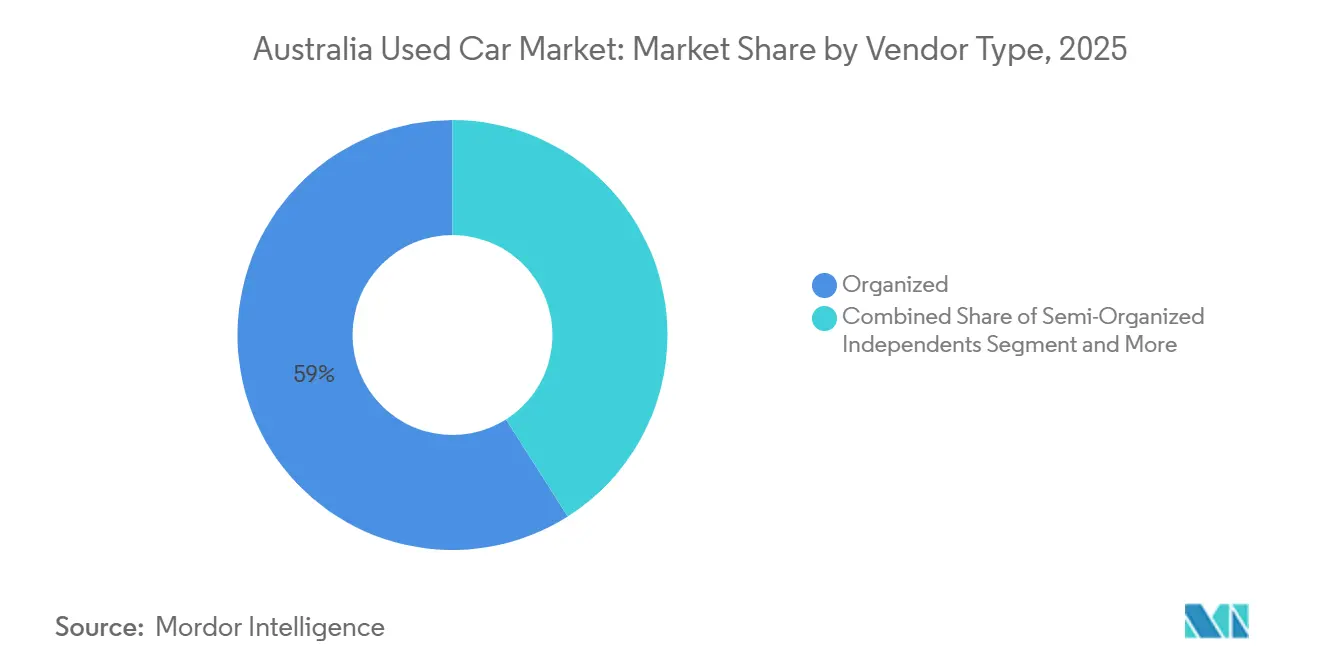

- By vendor type, organized players captured 59.03% of the Australian used car market share in 2025, whereas semi-organized independents are expected to expand at an 11.59% CAGR through 2031.

- By fuel type, petrol cars led with 65.12% of the Australia used car market share in 2025, while electric variants are on course to grow at a 19.12% CAGR to 2031.

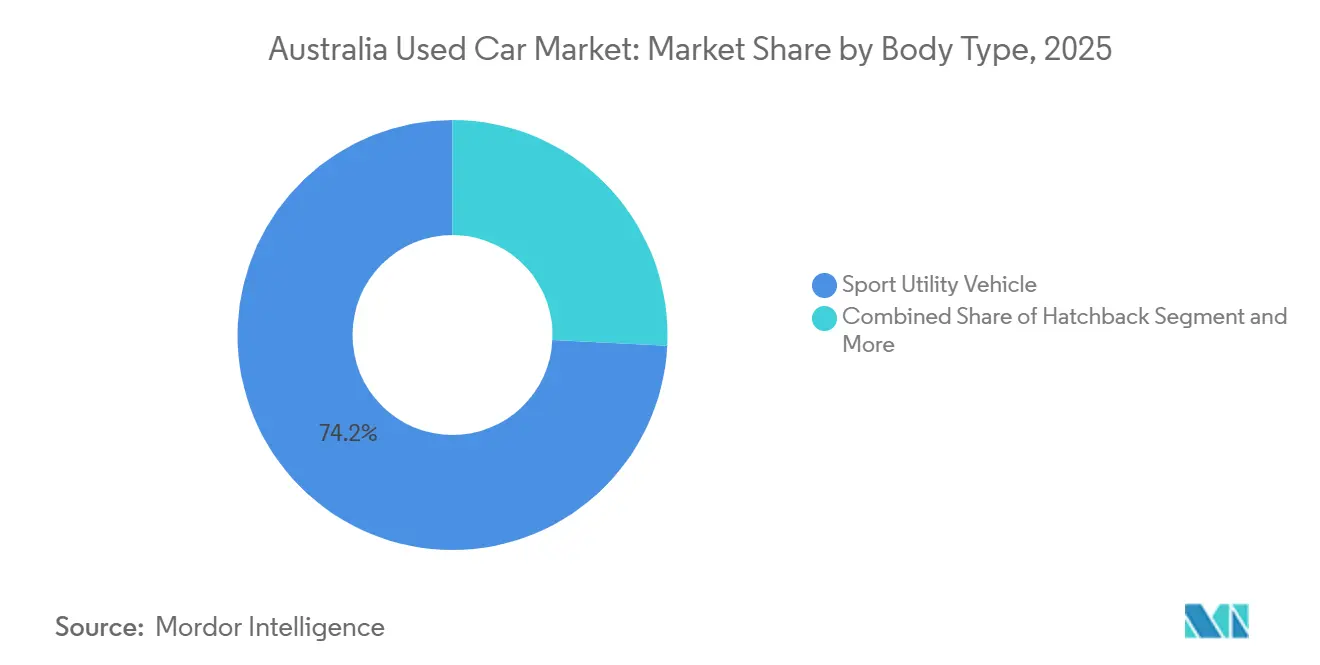

- By body type, sport utility vehicles dominated with 74.18% revenue share in 2025; multi-purpose vehicles and utes are forecast to advance at a 12.03% CAGR during 2026-2031.

- By sales channel, offline formats controlled 75.21% of transactions in 2025, yet online channels are the fastest-growing sub-segment at 14.35% CAGR to 2031.

- By region, New South Wales commanded 32.13% of the Australian used car market size in 2025, whereas Queensland is the quickest-expanding state at an 11.04% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Australia Used Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Online Aggregators Accelerate Metro Sales | +2.1% | NSW, VIC, QLD metro hubs | Short term (≤2 years) |

| State Incentives Enlarge BEV Supply | +2.0% | NSW, VIC, ACT | Medium term (2-4 years) |

| CPO Programs Boost Buyer Trust | +1.8% | NSW and VIC metro corridors | Medium term (2-4 years) |

| SUV Preference Fuels Replacement Demand | +1.5% | Nationwide, with QLD and WA hotspots | Long term (≥4 years) |

| Flexible Finance Attracts Millennial Buyers | +1.3% | Sydney, Melbourne, Brisbane | Medium term (2-4 years) |

| Fleet Renewals Feed Premium Inventory | +1.2% | NSW and VIC metros | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Surge in Online Aggregator Platforms Accelerating Transaction Volumes in Metro Areas

Digital marketplaces are streamlining the journey from car listing to handover, leveraging machine-learning valuations alongside integrated loan offers. Carsales, a prominent player, reported significant revenue for FY 2024 and facilitated a substantial number of trades through its web and app platforms. Gumtree Motors, another key player, attracts a large number of monthly visitors, generating extensive page views, and boasts an inventory supplied by numerous dealer partners across Australia. Australian Automotive Dealer Association (AADA) data show 1.59 million used-car listings in H1 2025, a notable surge above the prior-year period, while completed sales hit 1.13 million, underscoring the efficiency gains of algorithmic matching[1]“Used-Car Retail June 2025 Update,” Australian Automotive Dealer Association, aada.com.au. Cars24, a dedicated operator in the space, secured substantial funding in early 2024. They now offer a unique proposition: after a complimentary inspection, sellers receive their proceeds quickly, bypassing the traditional dealer intermediary. This digital convenience appeals to urban buyers under 35, who often finalize financing via their smartphones. However, drivers in regional areas still prioritize onsite inspections, as inconsistent connectivity and extended travel distances amplify their purchase concerns.

Government EV Incentives Driving Supply of Near-New Electric Used Cars

Expired purchase rebates still influence supply because 2021-2023 incentive cohorts are now hitting their first trade-in cycle. Federal DRIVEN funding of AUD 60 million (~USD 40.2 million) earmarked for dealer chargers lifts range confidence and lowers BEV stock days-to-sell [2]“New Vehicle Efficiency Standard Factsheet,” Department of Climate Change, Energy, the Environment and Water, climatechange.gov.au. In FY 2024-2025, transactions for used electric vehicles (EVs) experienced significant growth. However, listings grew at an even faster pace, creating increased price pressure. As the New Vehicle Efficiency Standard gradually lowers CO₂ targets over the coming years, the policy-driven shift is expected to intensify. This development is likely to drive a greater influx of hybrids and battery electric vehicles (BEVs) into both new-car showrooms and, subsequently, the secondary market.

Rising Penetration of Certified Pre-Owned Programs Enhancing Consumer Confidence

Franchise dealers treat CPO schemes as a margin-defense play because buyers trade price premiums for peace of mind. Hyundai Promise applies a 118-point inspection, a five-year age limit, and a 120,000-kilometer cap, then layers on a 12-month warranty extension. Toyota’s Certified Used Vehicle program matches those standards with several inspection points and a one-year warranty extension, reinforcing Toyota’s residual-value leadership. In the first half of 2025, organized dealers strengthened their presence in the Australian used car market. The impact is heightened by concentrated dealer networks in Sydney and Melbourne, which reduce search distances and lower travel costs for buyers. While independent lots are forming alliances for third-party inspections, risk-averse consumers still prioritize clear brand signals and warranty coverage.

Growing Preference for SUVs and Utes in Replacement Cycle Fuels Secondary Demand

SUVs surpassed passenger cars to become the most popular category for new vehicle sales. By mid-2025, SUVs dominated the market, reflecting a strong consumer preference. This growth ensures a consistent supply of late-model SUVs entering the used car market in the coming years, maintaining high demand and supporting their resale values. Meanwhile, popular ute models continued to perform well, although overall demand for utes showed signs of decline. Buyers are increasingly considering factors such as rising fuel costs and the availability of plug-in alternatives. For instance, newer plug-in models are gaining traction, indicating a shift in powertrain preferences, even in traditionally rural areas.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Certified Battery-Health Data | -1.2% | Nationwide, especially NSW and VIC metros | Medium term (2-4 years) |

| Odometer Rollback and Accident Damage | -0.9% | Highest in the semi-organized and private-party segments | Long term (≥4 years) |

| Vehicle Logistics Costs | -0.8% | NSW-WA and QLD-SA corridors | Medium term (2-4 years) |

| Emissions Standard Uncertainty | -0.6% | ACT and VIC policy hot spots | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Limited Availability of Battery Health Data Damps Confidence in Used EVs

In Australia, buyers are left to depend on informal range tests or proprietary diagnostics, as the country has not yet enacted uniform battery-state-of-health disclosures. This stands in contrast to the proposed protocols in the EU. The high cost of replacement packs can significantly alter the total-cost-of-ownership calculations for five-year-old battery electric vehicles (BEVs). While Tesla's transferable long-term guarantee alleviates some of these concerns, brands outside the premium segment do not offer similar reassurances. Without the establishment of federated standards, high-mileage BEVs will see their residual-value curves trailing behind those of hybrids and petrol cars. This trend is likely to stifle the full potential of electrification in Australia's used car market.

Persistent Transparency Concerns over Odometer Rollback and Accident Histories

New South Wales offers a free three-year odometer lookup, and South Australia enforces fines up to AUD 150,000 (USD 100,500) for tampering, but patchwork regulation still lets fraudulent cases slip through [3]“Motor Vehicle Trading Act Enforcement Summary,” Government of South Australia, sa.gov.au. A national real-time registry comparable to Carfax in the United States remains a policy aspiration. Fraud spikes during supply squeezes, as happened in 2021-2022 when wholesale values soared. The absence of a single-source truth steers risk-averse buyers toward branded dealers and CPO lots, even if prices run significantly higher.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vendor Type: Organized Consolidation Versus Independent Agility

Organized chains commanded 59.03% of the Australian used car market in 2025, with franchise dealers and large independents bundling CPO inspection, instant finance, and same-day settlement. Semi-organized independents register the fastest expansion, at an 11.59% CAGR by 2031, as they leverage low-cost, cloud-based dealer-management systems and partner with fintech lenders for rapid credit scoring. The organized cohort is pursuing acquisition-driven scale; Eagers sold 20% of easyauto123 to Mitsubishi Corporation in October 2025, reinforcing the thesis that global capital seeks high-yield, asset-light retail platforms. Private-party and sole-proprietor lots still dominate regional towns where personal relationships matter. Yet, the compliance burden of warranty law and history reporting is tilting the playing field in favor of branded networks.

In recent years, the organized segment of the Australian used car market has experienced significant growth, fueling expectations of ongoing consolidation. This expansion, combined with group purchasing power, has resulted in reduced reconditioning costs and prioritized access to auctions. In response, independent dealers are virtually pooling their inventories across various yards and leveraging premium listings on Carsales to enhance their professional image. While proposed federal regulations might soon require national vehicle-history disclosures, potentially bridging the assurance gap, buyers are still inclined to invest in the peace of mind offered by Certified Pre-Owned (CPO) banners.

By Fuel Type: Electric Momentum and Hybrid Resilience

Petrol vehicles retained 65.12% of total transactions in 2025, but electric units clocked a 19.12% CAGR by 2031, proving the fastest climb within the Australian used car market. Supply mechanics explain part of the surge: Three-year-old Teslas, MG4s, and Nissan Leafs from 2022 incentive cohorts are now entering trade-in lanes. Monthly sales remain lumpy because uncertainty about battery health deters risk-averse shoppers, yet listing volumes suggest a tipping point is near. Diesel units maintain relevance in rural and mining districts, representing a notable share of March 2025 deals, while hybrids enjoy a sweet spot; Toyota’s hybrid-only passenger range all but guarantees abundant, fuel-sipping stock by 2027. The Australian used car market size for hybrids widened between 2024 and 2025 as residual-value premiums tightened against petrol equivalents.

Looking ahead, the New Vehicle Efficiency Standard will accelerate the shift. Dealers anticipate a two-speed depreciation curve: low-emission cars hold value, whereas high-emission SUVs face steeper markdowns. Lenders already bake lower residual-value risk into loan pricing for hybrids and BEVs, subtly nudging buyer demand toward electrified powertrains.

By Body Type: SUV Supremacy Faces Niche Competition

Sport Utility Vehicles (SUVs) cemented a 74.18% share in 2025, driven by one-car households that require flexibility for school runs and regional trips. March 2025 used-SUV transactions jumped 16.5% month on month to 85,083 units, confirming the depth of demand even in inflationary settings. Still, multi-purpose vehicles and utes are forecast to log a 12.03% CAGR by 2031 as fleets rotate pandemic-era purchases and BYD’s plug-in ute platform enters mainstream awareness. Traditional diesel double-cabs lose shine when weighed against rising fuel and registration costs, yet utes remain irreplaceable for trades where payload ratings outrank economy.

Sedans and hatchbacks, although eclipsed by SUVs, remain the backbone of entry-level budgets. The Corolla, i30, and Mazda 3 models maintain high liquidity, and their relatively low running costs appeal to first-time buyers. Vans and buses benefit from e-commerce expansion and city logistics contracts, but small base volumes cap their market influence. The divergence underlines how the Australian used car market caters to parallel value propositions: lifestyle flexibility, commercial utility, and affordability.

By Sales Channel: Clicks Rise, Bricks Remain Critical

Offline formats accounted for 75.21% of 2025 trades, but online channels booked the strongest growth at 14.35% CAGR by 2031. In FY 2024, Carsales facilitated a significant volume of vehicle transactions, utilizing structured data feeds to help dealers assess lead creditworthiness before the buyer's arrival. However, physical interactions remain crucial: a majority of online consumers demand a test drive before finalizing payment. Auctions play a pivotal role in wholesale clearings, particularly for corporate and finance repossessions with easily documented provenance. Meanwhile, private C2C transactions, once the frontrunner, have declined in major cities, primarily due to increased awareness of warranties.

The hybrid model is set to prevail. Dealers that synchronize digital advertising with in-store service slots convert leads faster and improve accessory attach rates. Conversely, pure-play online entrants such as Cars24 must now establish physical handover hubs to achieve parity with dealer lots in terms of inspection, highlighting convergence rather than displacement within the Australian used car market.

Geography Analysis

New South Wales secured 32.13% of the 2025 transaction value, benefiting from Sydney’s dense dealer networks, auction infrastructure, and headquarters of major aggregators. Listings in the state climbed in January 2025, signaling supply momentum that tempers price inflation. Victoria, buoyed by Melbourne's robust employment landscape and deep-rooted finance sector, recorded significant sales in January 2025. Meanwhile, Western Australia, thanks to its resource-sector payrolls, mitigated the challenges of distance-driven logistics and achieved notable sales in March 2025.

Queensland is the standout for growth, set to expand at a 11.04% CAGR through 2031. Population inflow—125,845 residents in 2023-2024, nearly 60% of whom arrived from overseas—has boosted vehicle demand in the Sunshine Coast, Ipswich, and Logan corridors. Adding to the momentum, a registration-fee rebate introduced in 2024 has made vehicle purchases more affordable. With southeast Queensland's population anticipated to grow steadily in the coming years, the demand trajectory looks promising. Furthermore, as regional migration trends favor SUVs and dual-cab utes for their versatility, the state's vehicle parc is witnessing a diverse range of powertrains.

South Australia and Tasmania, while smaller, present stable markets. Adelaide's initiative of an open-data policy on monthly ownership transfers enhances price transparency. In Hobart, the city's limited geography leads to higher residual values, thanks to constrained supply. The ACT saw a robust surge in sales recently, a testament to the region's public-sector job security and above-average disposable income. The Northern Territory, with its relatively low monthly trades, remains a niche player. Yet, buoyed by elevated mining wages, it boasts high average transaction values. As the New Vehicle Efficiency Standard comes into play, expect a widening geographic divide: urban drivers will likely lean towards low-emission models, while those in remote areas may continue to favor the reliability of diesel.

Competitive Landscape

The market exhibits moderate concentration, with the top five organized players accounting for a notable share of transaction value. Meanwhile, hundreds of semi-organized independents and thousands of private sellers fill the remaining niches. Eagers Automotive, through easyauto123, commands a significant national share and leverages centralized reconditioning hubs to realize scale efficiencies. Its October 2025 capital tie-up with Mitsubishi Corporation provides both expansion bankroll and upstream procurement leverage [4]“Investment in Easyauto123 Press Statement,” Mitsubishi Corporation, mitsubishicorp.com .

Carsales dominates the digital funnel. Its AUD 500 million (USD 329.40 million) rights issue in March 2023 funded a controlling stake in Brazil’s Webmotors, giving it cross-border data leverage and underwriting continued investment in valuation algorithms. Pickles Auctions fulfils the wholesale linchpin role, moving thousands of ex-fleet vehicles and setting pricing benchmarks referenced by lenders.

White-space opportunities center on battery-health certification and last-mile logistics. Cars24’s rapid-payment pledge pressures incumbents to cut settlement windows, amplifying digital warfare on user experience. Independents increasingly partner with fintech firms like Plenti and Stratton Finance to overlay instant credit approvals on Gumtree or Facebook Marketplace listings. Regulatory reforms that mandate national vehicle-history sharing or battery metrics would likely favor well-capitalized chains that can absorb compliance systems, thereby accelerating consolidation inside the Australia used car market.

Australia Used Car Industry Leaders

Cars24

CarsGuide Media Solutions Pty Ltd

Gumtree AU Pty Ltd

Cartopia Pty Ltd

Carsales Australia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Mitsubishi Corporation acquired 20% of Eagers Automotive’s easyauto123 division for AUD 70 million (USD 46.9 million) and injected a further AUD 50 million (USD 33.5 million) into Eagers to co-develop mobility solutions.

- November 2024: Perth-based startup 1Wheel launched a peer-to-peer platform aimed at lowering fees and improving price transparency for private car sellers, targeting the Australian used car market valued at over AUD 100 billion (~USD 66 billion.)

- Mar 2024: The Australian Government announced AUD 76 million (~USD 50 million) to boost EV availability, including a credit line for dealerships and an investment via ARENA to help Europcar add 3,100 battery-electric cars that will flow into the secondary channel after a two-year rental cycle.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Australian used car market as the annual value of passenger cars, SUVs, and utility wagons that have previously been registered, are resold in road-worthy condition, and change legal ownership through any retail, wholesale, or online channel. Vehicles are counted at the final transaction price inclusive of dealer margins, statutory charges, and GST.

Scope exclusion: Heavy commercial trucks, salvage auctions, and informal part-out sales remain outside our scope.

Segmentation Overview

- By Vendor Type

- Organized

- Semi-Organized Independents

- Unorganized

- By Fuel Type

- Petrol

- Diesel

- Hybrid

- Electric

- Others (CNG, Fuel Cell Electric, etc.)

- By Body Type

- Hatchback

- Sedan

- Sport Utility Vehicle

- Multi Purpose Vehicles and Utes

- By Sales Channel

- Online

- Offline

- Franchise Dealer

- Independent Dealer

- Auction

- C2C

- By Region

- New South Wales

- Victoria

- Queensland

- Western Australia

- South Australia

- Tasmania

- Northern Territory

- Australian Capital Territory

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed franchised and independent dealers across New South Wales, Victoria, and Queensland, spoke with auctioneers and online-platform product leads, and polled used-car finance officers. These discussions clarified margin erosion, warranty uptake, and regional demand shifts, enabling us to stress-test secondary inputs and refine scenario assumptions.

Desk Research

We began by extracting foundational data from tier-1 public sources such as the Australian Bureau of Statistics' motor vehicle census, the Department of Infrastructure's registration updates, Australian Automotive Dealer Association sales bulletins, and Reserve Bank household credit releases. Complementary insights on import duties, fuel price trends, and vehicle age mix were gathered from Treasury papers, OECD surface transport tables, and peer-reviewed journals. Our team then mined company filings, dealer presentations, and news archives via D&B Hoovers and Dow Jones Factiva to benchmark pricing spreads and margin structures. These sources are illustrative rather than exhaustive; many other publications informed our desk work.

Multiple datasets were normalized to a single currency year, and outliers were flagged for reconciliation with primary evidence before being loaded into the core model.

Market-Sizing & Forecasting

A top-down build, anchored on Australia's active passenger vehicle parc and annual ownership-change ratios, produced the demand pool. We corroborated totals with bottom-up checks on sampled dealer volumes and average selling prices. Key variables like scrappage rate, online penetration, median disposable income, fuel cost index, and credit availability drive both historical alignment and the multivariate regression that underpins our 2025-2030 forecast. Where dealer roll-ups under-represent private peer-to-peer trades, calibrated adjustment factors bridge the gap.

Data Validation & Update Cycle

Model outputs pass three layers of variance and plausibility checks, after which senior analysts review unusual swings. We refresh every twelve months and trigger ad-hoc updates for policy shifts, macro shocks, or material M&A, ensuring clients receive the latest view.

Why Mordor's Australia Used Car Baseline Commands Reliability

Published estimates often differ because firms adopt distinct scopes, assume varying discount curves, or refresh at dissimilar cadences.

Key gap drivers in our market include whether private C2C exchanges are captured, if light commercials creep into counts, and how list prices are reconciled with actual transaction values. Mordor aligns scope precisely with registered passenger vehicles, applies verified discount factors, and updates annually, delivering a balanced midpoint.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 49.86 B (2025) | Mordor Intelligence | - |

| USD 28.32 B (2024) | Global Consultancy A | Excludes private sales, relies on VAT-exclusive prices |

| USD 71.64 B (2024) | Regional Consultancy B | Adds light commercial vehicles and fleet disposals |

| USD 77.20 B (2024) | Industry Association C | Uses advertised ask prices without negotiated discounts |

These comparisons show that while other publishers skew low or high based on scope or price treatment, our disciplined variable selection and transparent adjustment steps keep Mordor's baseline dependable for strategic decisions.

Key Questions Answered in the Report

How large is the Australia used car market in 2026?

The Australia used car market size reached USD 49.86 billion in 2026 and is projected to grow at a 10.28% CAGR to USD 81.32 billion by 2031.

Which vendor segment is growing the fastest?

Semi-organized independents are growing at 11.59% CAGR through 2031, outpacing all other vendor categories due to digital listing adoption and flexible finance tie-ups.

What body type dominates current used-vehicle sales?

SUVs dominate, holding 74.18% share of 2025 transactions thanks to their versatility and continued popularity among family and lifestyle buyers.

How quickly are electric cars penetrating the secondary market?

Electric vehicles are forecast to register a 19.12% CAGR through 2031.

Which state offers the strongest growth outlook?

Queensland leads with an 11.04% CAGR forecast, powered by interstate migration, infrastructure investment, and targeted registration-fee reductions.

What is the main barrier to used-EV adoption?

Lack of standardized battery-health certification drives range-anxiety concerns and accelerates price depreciation for high-mileage electric models.

Page last updated on: