Market Overview

| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

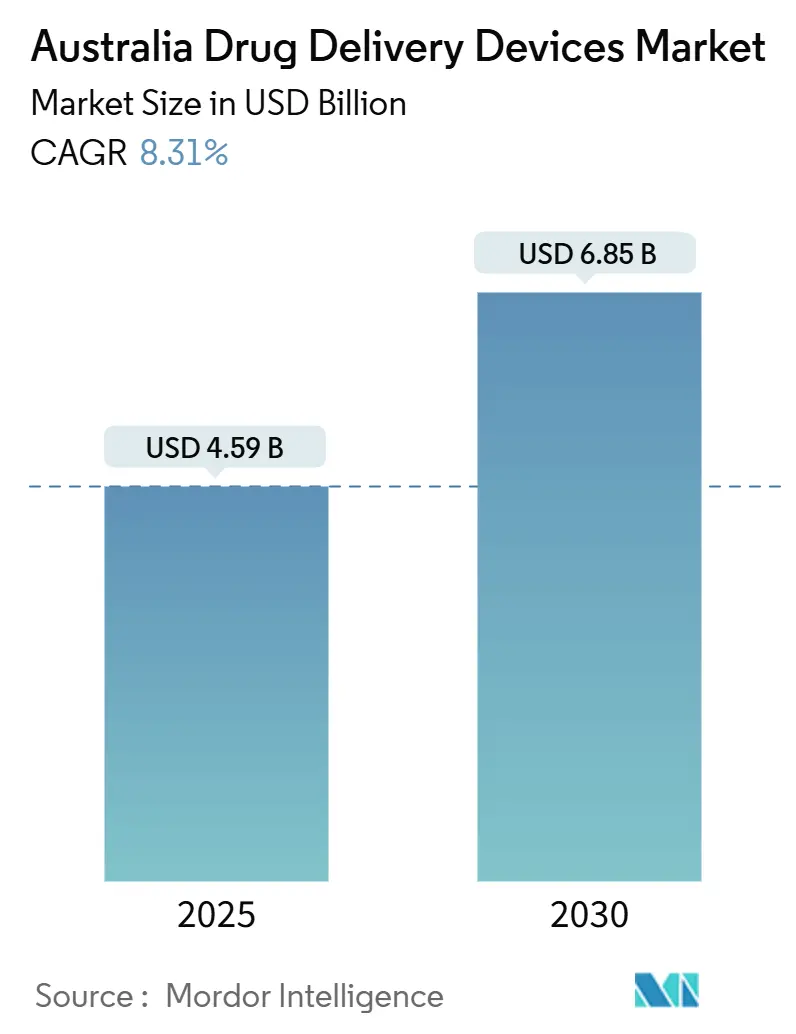

| Market Size (2025) | USD 4.59 Billion |

| Market Size (2030) | USD 6.85 Billion |

| Growth Rate (2025 - 2030) | 8.31% CAGR |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Australia Drug Delivery Devices Market Analysis by Mordor Intelligence

The Australia drug delivery devices market is valued at USD 4.59 billion in 2025 and is forecast to climb to USD 6.85 billion by 2030, registering an 8.31% CAGR over the period. Growth is underpinned by an aging population, a rising chronic-disease burden, and widespread use of the Pharmaceutical Benefits Scheme (PBS), which dispensed medicines to nearly 70% of residents during 2022.[1]Australian Bureau of Statistics, “Health Conditions and Risks,” abs.gov.au Government programs that shift care from hospitals to homes, such as Victoria’s Better at Home initiative, further expand demand for user-friendly devices.[2]Victorian Department of Health, “Better at Home Initiative,” health.vic.gov.auIntensifying R&D around microneedle patches, connected injectors, and orally delivered biologics is driving product innovation, while digital health investments are improving data flow and remote monitoring capability. Against this backdrop, manufacturers face higher Therapeutic Goods Administration (TGA) fees and strict combination-product rules that lift compliance costs.

Key Report Takeaways

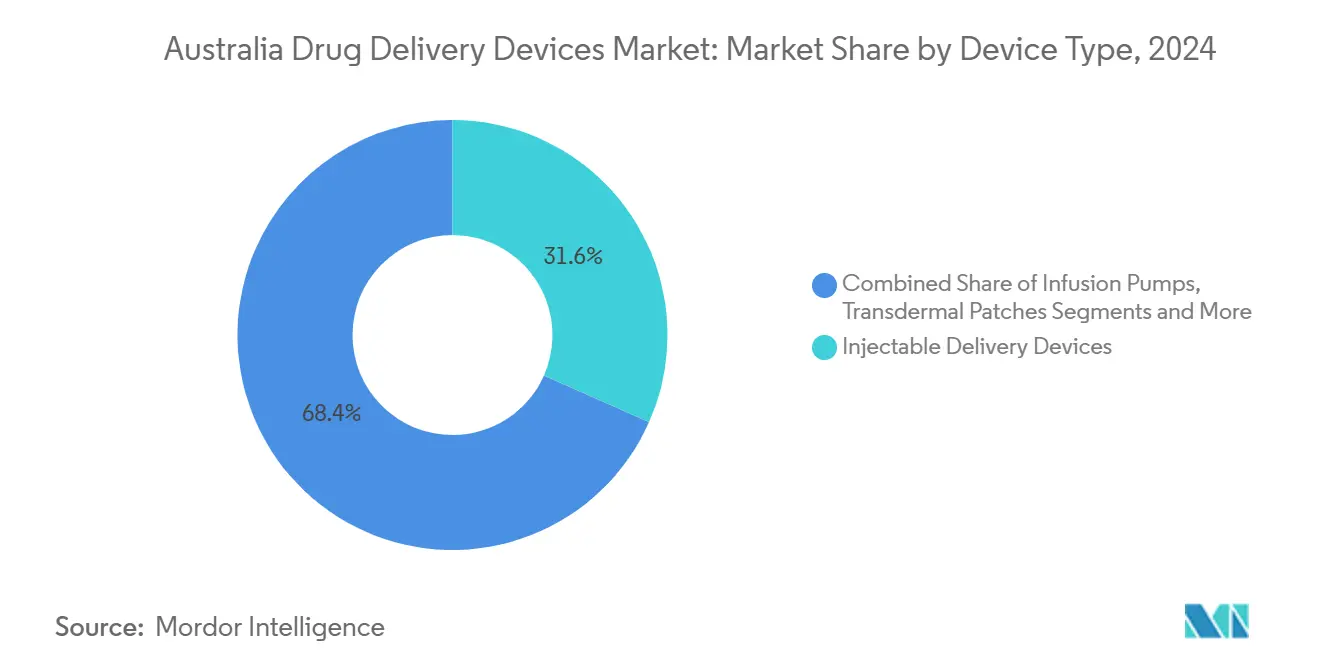

- By device type, injectable delivery devices led with 31.63% of the Australia drug delivery devices market share in 2024; transdermal patches are projected to expand at a 12.29% CAGR through 2030.

- By route of administration, injectables captured 44.57% of the Australia drug delivery devices market share in 2024, whereas oral mucosal systems are set to grow at a 10.23% CAGR during 2025-2030.

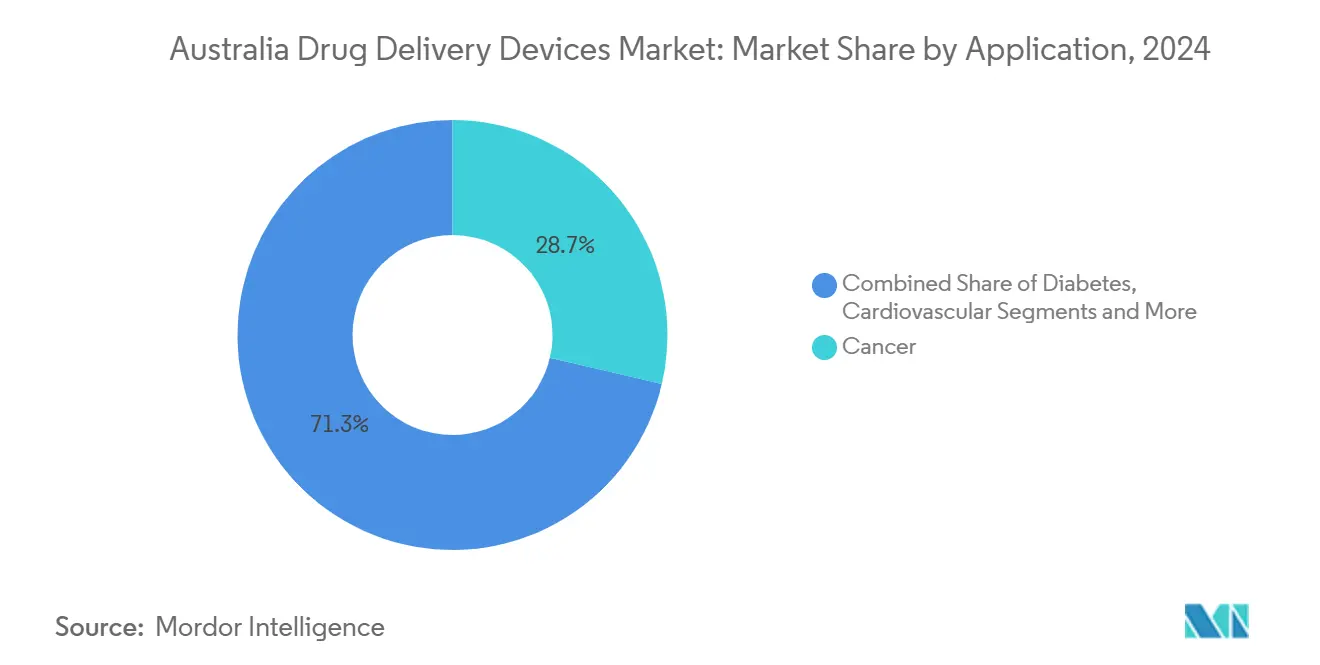

- By application, cancer therapy accounted for a 28.67% share of the Australia drug delivery devices market size in 2024, while diabetes therapies record the highest expected CAGR at 10.74% to 2030.

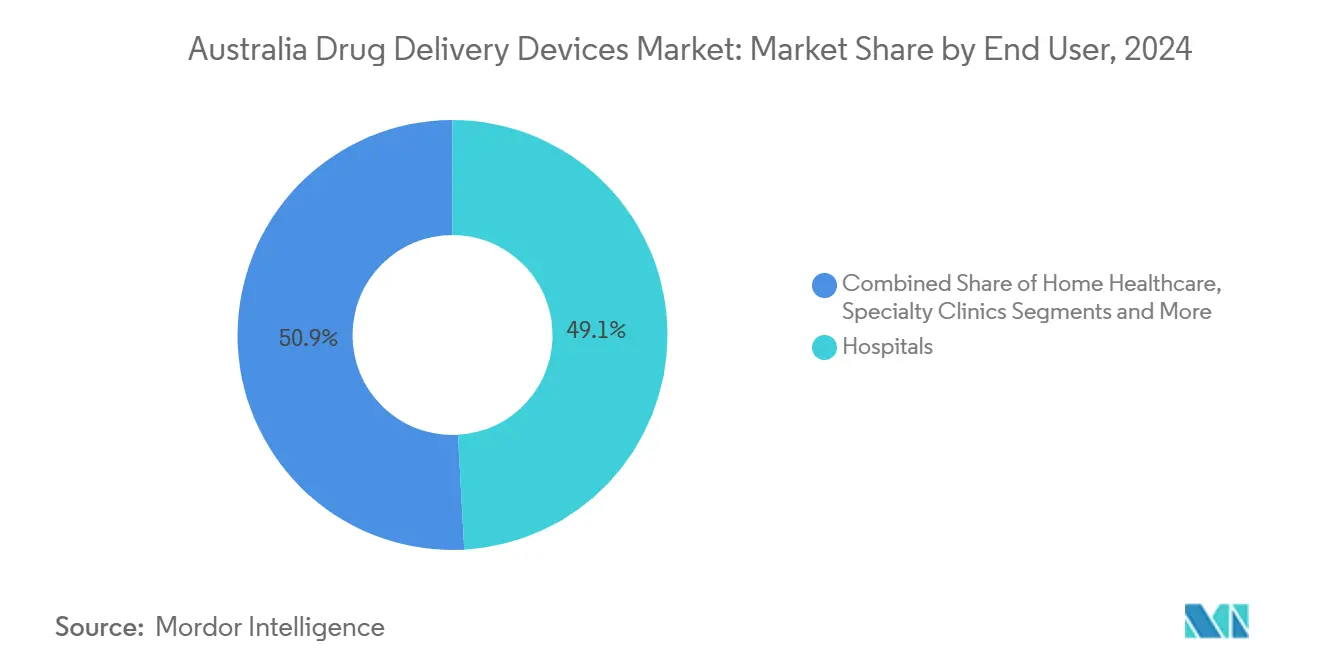

- By end user, hospitals commanded 49.13% of the Australia drug delivery devices market size in 2024; home healthcare settings are on track for an 11.51% CAGR over 2025-2030.

Australia Drug Delivery Devices Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High burden of chronic diseases and ageing population | +2.8% | National; strongest in Victoria and New South Wales | Long term (≥ 4 years) |

| Government & industry support for at-home care and remote drug delivery | +2.1% | National; early adoption in Victoria and Queensland | Medium term (2-4 years) |

| Rising penetration of biosimilars and targeted therapies | +1.5% | National; concentrated in metro areas | Medium term (2-4 years) |

| Digital health integration with connected injectors and pumps | +1.2% | National; early uptake in urban centres | Short term (≤ 2 years) |

| Community-pharmacy vaccination programs that foster self-injection | +1.0% | National; higher penetration in cities | Medium term (2-4 years) |

| Accelerated pipeline drugs and TGA fast-track pathways | +0.8% | National | Short term (≤ 2 years) |

Source: Mordor Intelligence

High Burden of Chronic Diseases and Ageing Population

Australia’s 1.3 million people living with diabetes in 2024 generated AUD 3.9 billion in direct health spending aihw.gov.au. Three-quarters of adults were dispensed at least one PBS medicine, and more than 85% of those with chronic conditions required ongoing pharmacotherapy.[1]Australian Bureau of Statistics, “Health Conditions and Risks,” abs.gov.auAge-related physiological changes alter drug absorption and clearance, heightening demand for delivery formats that optimise dosing precision and safety. Manufacturers that tailor devices to geriatric needs—larger buttons, audible cues, and connected adherence alerts—stand to gain as the senior cohort expands.

Government and Market Players Support for At-home Care & Remote Drug Delivery

Victoria’s Better at Home program channels AUD 698 million into virtual and in-home healthcare, serving more than 15,000 people a year.[2]Victorian Department of Health, “Better at Home Initiative,” health.vic.gov.au Queensland added AUD 27 million for similar services in its 2024-25 budget. Hospital-at-home models have lowered care costs by 30% while maintaining or improving outcomes, leading payers to reimburse home episodes at inpatient rates commonwealthfund.org. These policies create fertile ground for self-use injectors, wearable pumps, and connected inhalers that help patients manage therapy outside acute facilities.

Rising Penetration of Biosimilars and Targeted Therapies Requiring Novel Delivery Formats

Novartis opened a dedicated radioligand-therapy plant in 2024, underscoring demand for precise oncology delivery technologies. Researchers at the University of Sydney advanced an oral insulin tablet that releases drug only in response to blood-glucose changes, potentially displacing subcutaneous injections for many patients.[3]University of Sydney, “Nanotech Opens Door to Future of Insulin Medication,” sydney.edu.au As biologics and conjugated molecules enter late-stage pipelines, innovators are redesigning delivery platforms to maintain molecule stability, handle high viscosity, and improve patient acceptance.

Digital Health Integration with Connected Injectors & Pumps

The National Digital Health Strategy (2023-2028) prioritises FHIR-based data standards and pledges AUD 325.7 million to upgrade e-prescribing, medication management, and device interoperability. Wider use of My Health Record supports real-time adherence tracking and remotely managed dose titration. Technology forums such as the 2025 C3.0 summit place connectivity, cybersecurity, and clinical governance at the centre of drug-device innovation.

Stringent TGA Combination-Product Compliance Costs

Application fees for new chemical entities included in a device run to AUD 18,872, with evaluation charges of AUD 76,055 and annual levies topping AUD 1,500 for Class III devices. These rising costs weigh heavily on start-ups and academic spin-outs, delaying market entry and, in some cases, redirecting R&D overseas.

Needlestick Injury Litigation and Risks Associated with Various Devices

Despite falling numbers of people injecting drugs, incidence of blood-borne infections linked to reused needles has risen, driving higher liability risk for device manufacturers. Government guidelines now demand stricter infection-control protocols and reporting, increasing compliance overhead for hospitals and aged-care facilities.

Segment Analysis

By Device Type: Injectable Devices Lead While Transdermal Patches Surge

Injectable systems held 31.63% of the Australia drug delivery devices market share in 2024, a position cemented by growing biologics use and rising chronic-disease prevalence. Connected pen injectors that transmit dosage logs to clinician dashboards are gaining traction among endocrinologists and rheumatologists. The Australia drug delivery devices market size attached to transdermal patches is projected to grow at 12.29% CAGR between 2025 and 2030, spurred by microneedle breakthroughs that improve payload capacity without compromising comfort. Collaboration between the Transdermal and Transmucosal Drug Delivery Research Group and Bionyeri Pty Ltd created a microneedle patch for acute pain episodes, illustrating domestic innovation.

Infusion-pump makers are integrating Bluetooth and closed-loop algorithms in anticipation of a national subsidy for insulin pumps proposed to begin mid-2025. Implantables, ocular inserts, and nasal devices round out the portfolio, each targeting niche clinical requirements. A recent health-technology assessment found intrathecal pumps improve quality of life for refractory cancer pain, though upfront costs remain high.

Note: Segment shares of all individual segments available upon report purchase

By Route of Administration: Injectables Dominate While Oral Mucosal Delivery Accelerates

Injectables delivered 44.57% of 2024 revenue within the Australia drug delivery devices market. High therapy adherence rates and predictable pharmacokinetics keep parenteral administration the default for many biologics. Inhalation devices account for a sizeable fraction, supported by ongoing upgrades to dry-powder carriers for obstructive-airway disease. The oral-mucosal channel is forecast to post a 10.23% CAGR as developers exploit sublingual routes to bypass first-pass metabolism.

Transdermal technologies continue to benefit from work on novel permeation enhancers and herbal patches that reduce gastrointestinal side effects. Nasal formulations appeal to neurologists for rapid central-nervous-system access; nanoparticle-gel hybrids recently showed 86%–96% encapsulation efficiency, signalling commercial promise.

By Application: Cancer Leads While Diabetes Shows Strongest Growth

Cancer uses generated 28.67% of 2024 revenue, reflecting a need for precise, often multi-modality dosing. Bacterial nanotechnology that steers chemotherapeutics to tumours exemplifies next-generation targeting approaches. The Australia drug delivery devices market size attributed to diabetes therapies is on track for a 10.74% CAGR, driven by automated insulin delivery and continuous-glucose-monitoring integration. Atmospheric-pressure studies confirm device durability during air travel, an important consideration for Australia’s mobile population. Cardiovascular, infectious-disease, and paediatric segments also add incremental demand, with RSV preventives already lowering hospitalisations in pilot states.

Note: Segment shares of all individual segments available upon report purchase

By End User: Hospitals Dominate While Home Healthcare Expands Rapidly

Hospitals absorbed 49.13% of total 2024 sales, buoyed by AUD 9.3 billion in fresh state-level hospital funding and nine new facilities slated to open by 2026. Ambulatory surgical centres, known for day-case procedures, are quick to adopt fast-onset anaesthetic patches and programmable infusion pumps to keep discharge times low.

Homecare remains the fastest-growing channel with an 11.51% projected CAGR. The Better at Home program and equivalent telehealth funding streams promote self-managed therapy using connected devices that alert nurses to out-of-range metrics. Victoria’s hospital-at-home scheme demonstrated 30% cost reductions and equal or better outcomes compared with inpatient stays. Specialty clinics and field-based nursing services leverage similar technologies when treating rheumatology and oncology patients outside tertiary centres.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Urban states dominate demand for sophisticated platforms, yet regional areas increasingly benefit from digital-health advances. Victoria’s AUD 698 million commitment to remotely delivered care places the state at the forefront of connected treatment models, driving higher per-capita adoption of wearable injectors. Queensland’s AUD 28.9 billion health budget, including AUD 27 million for virtual-care initiatives, underlines northern states’ pursuit of similar tools.

Nationwide, the Australia drug delivery devices market benefits from FHIR-compliant data exchange that enables tele-consultations even in sparsely populated areas. The strategy’s focus on secure pharmacovigilance systems means new devices must integrate seamlessly with My Health Record, a requirement shaping supplier selection criteria for rural pharmacies.

Western Australia and Queensland’s infant RSV programs highlight the growing role of state vaccination policies in shaping device adoption. Long-acting monoclonal injections administered through community clinics reduced hospital admissions costing as much as AUD 17,120 per child. As similar preventive measures roll out nationwide, demand for paediatric-friendly autoinjectors and low-dead-space syringes is rising.

Competitive Landscape

The Australia drug delivery devices market comprises multinational pharmaceutical-device hybrids, med-tech specialists, and nimble start-ups. Strategic alliances dominate: Aptar Digital Health’s 2024 tie-up with SHL Medical marries platform software with wearable injectors to streamline self-administration workflows. Domestic universities frequently license nanoformulation breakthroughs to industry partners, shortening the bench-to-bedside pathway.

Nanotechnology for oral biologics, exemplified by the University of Sydney’s glucose-responsive insulin tablet, offers disruptive potential that could erode the long-established injectable segment. At the same time, incumbents defend share by launching smaller, more discreet pumps; Tandem Diabetes Care plans to file for Australian approval of its tubeless Mobi system after successful US debut, banking on CGM integration to sway endocrinologists.

White-space remains in implantables for site-specific chemotherapy and in aerosolised formulations to treat systemic disease via the lung. Companies exploring AI-driven dose timing and patient-behaviour analytics aim to shift competition from hardware attributes toward predictive-care ecosystems, signalling continued evolution of the competitive matrix.

Australia Drug Delivery Devices Industry Leaders

-

Novartis AG

-

GlaxoSmithKline Plc

-

Becton, Dickinson and Company

-

CSL Limited

-

Novo Nordisk A/S

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- February 2025: Nutriband Inc. and Kindeva Drug Delivery amended their agreement to expand commercial supply of Aversa Fentanyl transdermal products in Australia.

- February 2025: TGA advised prescribers that Ozempic (semaglutide) shortages will persist through 2025 and encouraged consideration of alternatives. treatment option for patients with ophthalmic disorders. The device is available in Australia.

- October 2024: Tonik launched sleep- and stress-relief transdermal patches in Asia and announced four new SKUs for early 2025.

- August 2024: Monash University secured AUD 750,000 to advance a next-generation insulin formulation.

Australia Drug Delivery Devices Market Report Scope

As per the scope, drug delivery devices or systems are the tools that are used to deliver the drug through a specific route of administration. It enables the introduction of therapeutic substances into the body.

The Australian Drug Delivery Devices Market is segmented by route of administration (injectable, topical, ocular, and other routes of administration), application (cancer, cardiovascular, diabetes, infectious diseases, and other applications),, and end user (hospitals, ambulatory surgical centers, and other end users). The report offers the value (in USD million) for the above segments.

| By Device Type | Injectable Delivery Devices |

| Inhalation Delivery Devices | |

| Infusion Pumps | |

| Transdermal Patches | |

| Implantable Drug Delivery Systems | |

| Ocular Inserts & Delivery Implants | |

| Nasal & Buccal Delivery Devices | |

| By Route of Administration | Injectable |

| Inhalation | |

| Transdermal | |

| Oral Mucosal (Buccal & Sublingual) | |

| Ocular | |

| Nasal | |

| By Application | Cancer |

| Cardiovascular | |

| Diabetes | |

| Infectious Diseases | |

| Other Applications | |

| By End User | Hospitals |

| Ambulatory Surgical Centres | |

| Home Healthcare Settings | |

| Specialty Clinics | |

| Other End Users |

By Device Type

| Injectable Delivery Devices |

| Inhalation Delivery Devices |

| Infusion Pumps |

| Transdermal Patches |

| Implantable Drug Delivery Systems |

| Ocular Inserts & Delivery Implants |

| Nasal & Buccal Delivery Devices |

By Route of Administration

| Injectable |

| Inhalation |

| Transdermal |

| Oral Mucosal (Buccal & Sublingual) |

| Ocular |

| Nasal |

By Application

| Cancer |

| Cardiovascular |

| Diabetes |

| Infectious Diseases |

| Other Applications |

By End User

| Hospitals |

| Ambulatory Surgical Centres |

| Home Healthcare Settings |

| Specialty Clinics |

| Other End Users |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

1. What is the current size of the Australia drug delivery devices market?

The market is worth USD 4.59 billion in 2025 and is forecast to reach USD 6.85 billion by 2030.

2. Which device category leads in Australia?

Injectable delivery systems hold 31.63% of 2024 revenue, reflecting their pivotal role in chronic-disease management.

3. How fast is home healthcare demand growing?

Home-use settings are projected to grow at an 11.51% CAGR between 2025 and 2030, supported by programs such as Better at Home.

4. What is the fastest-growing application?

Diabetes therapies, especially automated insulin-delivery solutions, are expanding at a 10.74% CAGR.

5. How are digital health policies affecting the market?

National FHIR standards and AUD 325.7 million in federal funding are accelerating adoption of connected injectors, pumps, and remote-monitoring tools.

6. What regulatory hurdles do suppliers face?

TGA fees and evaluation charges for combination products exceed AUD 95,000 per submission, elevating cost and time-to-market for innovators.

Page last updated on: June 9, 2025