Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 1.07 Trillion |

| Market Size (2030) | USD 2.29 Trillion |

| Growth Rate (2025 - 2030) | 16.44% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Australia Payments Market Analysis by Mordor Intelligence

The Australia payments market size is USD 1.07 trillion in 2025 and is forecast to reach USD 2.29 trillion by 2030, expanding at a 16.44% CAGR. Fast uptake of real-time infrastructure, contactless proliferation, and regulatory clarity around buy-now-pay-later (BNPL) licensing form the backbone of this growth. Real-time rails delivered by the New Payments Platform (NPP) continue to draw volume away from the Bulk Electronic Clearing System (BECS) as merchants and consumers prioritize speed and data-rich settlement. Tap-to-phone innovation is widening acceptance for micro-merchants, while earned-wage access products improve liquidity for shift workers in hospitality and retail. Interchange reform, rising fraud costs, and scheduled sunsetting of aging rails temper the outlook, but policy consistency and the Reserve Bank’s push toward a cash-lite economy sustain long-term momentum.

Key Report Takeaways

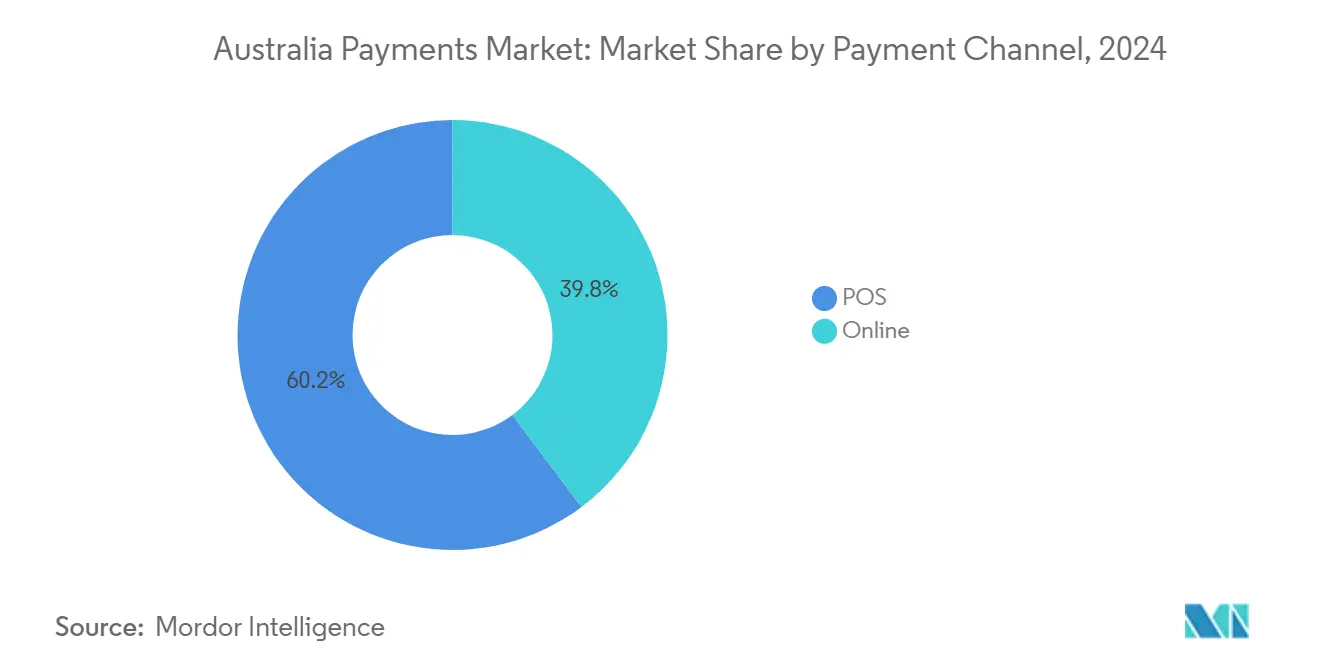

- By payment channel, point-of-sale captured 60.24% of the Australia payments market share in 2024; online payments are projected to grow at a 17.96% CAGR to 2030.

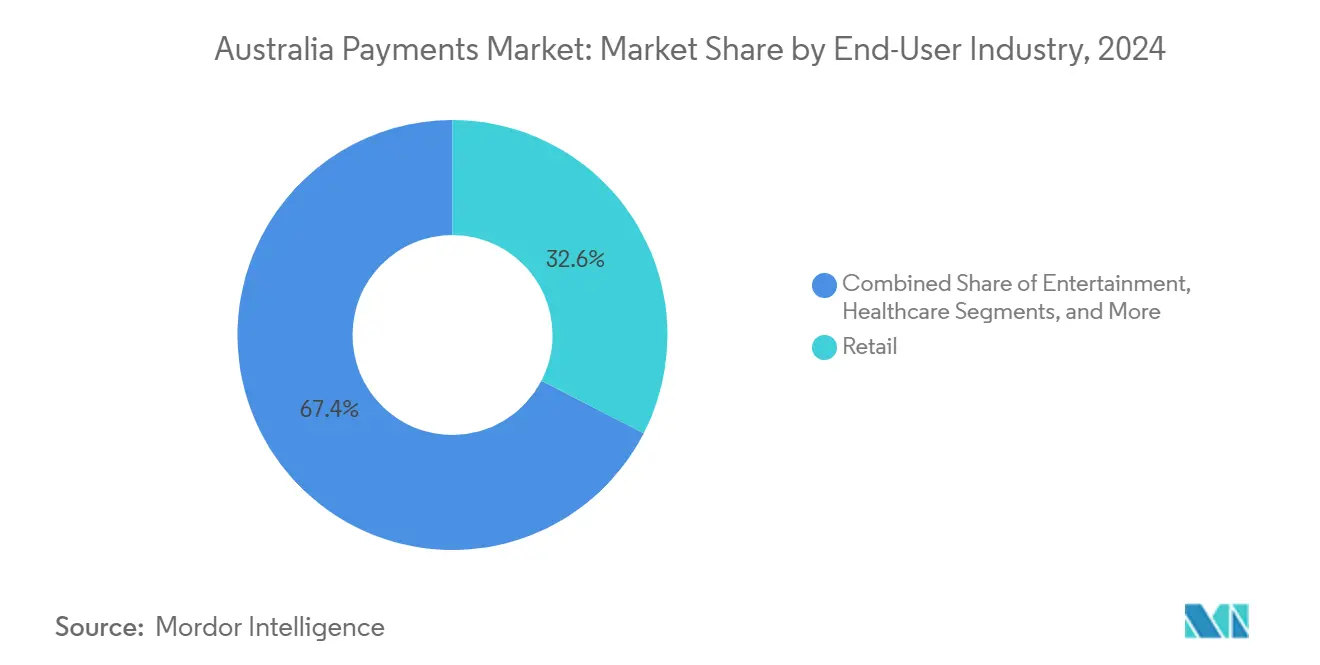

- By end-user industry, retail led with 32.56% of the Australia payments market size in 2024, while entertainment is advancing at a 17.24% CAGR through 2030.

- By geography, New South Wales held 34.67% share of the Australia payments market size in 2024 and Queensland is expanding at a 17.16% CAGR through 2030.

Australia Payments Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in contactless card usage | +3.2% | National; early gains in Sydney, Melbourne, Brisbane | Short term (≤ 2 years) |

| E-commerce expansion post-COVID | +4.1% | National; concentrated in NSW and Victoria | Medium term (2-4 years) |

| Roll-out of New Payments Platform (NPP) | +2.8% | National; phased regional deployment | Long term (≥ 4 years) |

| Instant salary access (earned-wage) services | +1.9% | Metro hubs; hospitality and retail | Medium term (2-4 years) |

| Retail CBDC pilot learnings | +1.5% | National pilot cities | Long term (≥ 4 years) |

| Tap-to-phone enablement among micro-merchants | +2.1% | National; faster uptake in regional areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Growth in Contactless Card Usage

Tap-and-go now accounts for more than 95% of face-to-face card payments, cementing contactless as the de-facto tender for low-ticket transactions.[1]Source: Reserve Bank of Australia, “Consumer Payments Survey 2024,” rba,gov,au Average ticket sizes are declining as consumers abandon cash even for sub-AUD 10 spends. Hardware makers have responded by integrating near-field communication (NFC) readers into inventory and customer-relationship tools, incentivizing merchants to retire mag-stripe and PIN-pad estates. Micro-merchants such as market stalls and food trucks that historically considered terminals cost-prohibitive have migrated to all-in-one readers or tap-to-phone apps, broadening overall acceptance. This infrastructure refresh supports richer data capture per transaction, enabling loyalty and real-time offers that further entrench digital habits. Card schemes gain volume headroom, but interchange compression risk spurs ancillary revenue pursuits in value-added services.

E-commerce Expansion Post-COVID

Domestic online checkouts reached AUD 69 billion in 2024 as digital wallet penetration grew 34% year on year.[2]Australia Post, “eCommerce Industry Report 2024,” aupost.com.au Healthcare, education, and professional services embedded pay-by-link and hosted checkout widgets to replace paper invoicing, trimming debtor days. Within medical practices, on-the-spot Medicare integration cut back-office reconciliation times by 42% according to Commonwealth Bank’s GP Insights dataset. Payment orchestration layers that juggle cards, PayTo mandates, and alternative methods in a single API saw merchant adoption triple, driven by demand for fail-over routing and dynamic currency conversion. Logistics, subscription media, and utility billers now benchmark themselves against the “single-click” retail standard, making frictionless authentication and tokenized storage a baseline rather than a differentiator.

Roll-out of New Payments Platform (NPP)

The NPP processed 1.2 billion transactions in 2024, and PayTo overlay services allow merchants to debit consumer accounts instantly without direct-debit latency.[3]NPP Australia, “NPP Processes Record 1.2 Billion Transactions in 2024,” nppaustralia.com.au Confirmation-of-Payee has lowered mis-directed payments by 23% and slashed fraud losses 15%, strengthening consumer confidence. Amazon Australia’s integration with NAB lets shoppers authorize recurring debits from their banking apps, eliminating storage of card credentials. The next roadmap milestone is straight-through cross-border settlement with Singapore’s PayNow, positioning Australia to trim correspondent costs and daylight lags. Overlay innovation is catalyzing B2B adoption, with invoice-attached, data-rich requests for payment enabling automatic matching in enterprise resource planning (ERP) systems. As BECS retirement approaches, banks invest in ISO 20022 migration to future-proof ancillary platforms.

Instant Salary Access (Earned-Wage) Services

Earned-wage platforms processed AUD 500 million of early pay in 2024, easing liquidity for hourly workers. Hospitality and retail firms report a 15% reduction in staff turnover after deployments as on-demand access offsets paycheck-to-paycheck stress. Banks view these providers as ecosystem complements; Westpac embedded earned-wage APIs into its acquiring gateway for small businesses, extending merchant retention stickiness. Current regulation classifies earned wages as employment benefits rather than credit, enabling rapid scaling without consumer credit license overhead. Family-owned cafes and franchises exploit the model to differentiate in tight labor pools while mitigating over-time disputes through transparent accrual tracking.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interchange fee regulation pressure | -2.1% | National; greater effect in metro merchant clusters | Medium term (2-4 years) |

| Rising fraud and chargeback costs | -1.8% | National; skewed toward high-volume e-commerce corridors | Short term (≤ 2 years) |

| BNPL regulatory tightening | -1.3% | National; driven by consumer-protection mandates | Medium term (2-4 years) |

| Payment-rail outages (NPP/RITS) perceptions | -0.9% | System-wide; latent reputational risk | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Interchange Fee Regulation Pressure

Reserve Bank consultation proposes aligning digital-wallet and BNPL interchange caps with four-party card schemes to level acceptance costs. Retail lobby groups cite EU experiences where caps lowered merchant costs 0.2%-0.3% of transaction value, intensifying advocacy. Processors diversify toward data monetization, subscription billing, and anti-fraud services to offset possible margin squeeze. Some acquirers introduce tiered pricing that rewards merchants for routing transactions to least-cost rails, improving stickiness but thinning blended yields. Long-tail SMEs may benefit from cost relief, yet innovation budgets risk compression if interchange inflows fall faster than value-added uptake.

Rising Fraud and Chargeback Costs

Card-not-present fraud topped AUD 868 million in fiscal 2024, forming 92% of total losses. Synthetic identities leverage data breaches to bypass two-factor authentication, driving issuers to invest in behavioral biometrics and device-fingerprinting. Chargeback ratios climbed as friendly fraud blurred lines between disputes and deliberate abuse. Small gateways lacking machine-learning models struggle to reach mandated false-positive thresholds, pushing them toward white-label fraud-screen partnerships. Merchants bear higher secondary costs in dispute management staff and extended settlement holds, eroding cash-flow benefits of faster payment rails. Scheme mandates such as Secure Customer Authentication add friction that can trigger cart abandonment if poorly implemented.

Segment Analysis

By Mode of Payment: POS Dominance Faces Online Disruption

Point-of-sale (POS) payments controlled 60.24% of the Australia payments market share in 2024, translating into a USD-denominated majority of the transactional Australia payments market size. Debit card contactless usage is displacing credit cards as consumers prioritize fee avoidance, while digital wallets unify online and in-store identities, shrinking checkout divergence. Tap-to-phone and integrated POS tablets bundle loyalty, order-ahead, and pay-at-table functions, raising average spend by 8% for quick-service restaurants. Account-to-account PayTo debits at physical checkouts offer merchants processing fees that run 20-30 basis points below card-present rates, though adoption is nascent. Cash dipped below 7% of over-the-counter spend in 2025 as regional infrastructure gaps closed. Cryptocurrency acceptance remains marginal but provides marketing cachet for tech-savvy merchants.

Online payments accelerated at a 17.96% CAGR through 2030, propelled by subscription models in media and software-as-a-service, and by open-banking data feeds that simplify account verification. Tokenized one-click checkouts cut cart abandonment by 42% for fashion e-tailers, while marketplace escrow solutions diminish seller fraud risk. Cross-border e-commerce leverages multicurrency routing engines that settle in local clearing systems, bypassing card scheme FX spreads. Chargeback liability shifts under scheme rules spur merchants to add 3-D Secure, though friction pushes some to link PayTo as default auto-debit. Combined, hybrid fulfillment models blur the boundary between POS and online, setting the stage for unified commerce dashboards that reconcile inventory across channels in real time.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Mode of Payment: POS Dominance Faces Online Disruption

Retail preserved 32.56% of the Australia payments market size in 2024, underwritten by omnichannel initiatives that provide uniform loyalty accrual regardless of purchase location. Self-checkout, buy-online-pickup-in-store (BOPIS), and dropship partnerships raise transaction counts while compressing basket margins, encouraging data-driven upselling at payment confirmation screens. Large grocers deploy computer-vision checkout that auto-debits stored credentials, eliminating traditional tills.

Entertainment exhibited the highest growth trajectory at 17.24% CAGR, as streaming, in-game purchases, and event ticketing adopt instant settlements to prevent piracy and scalping. Subscription fatigue drives providers to embed “pause or resume” options within account dashboards, enabled by PayTo mandates that merchants can amend without fresh card details. Gaming platforms introduce micro-transactions denominated in sub-AUD 1 increments, viable only with low-cost real-time rails. Live-event organizers embrace token-gated access, issuing NFT-like passes whose resale royalties settle automatically upon wallet transfer.

Healthcare digitization gained prominence as practices integrate Medicare claim lodgment at point of service, boosting first-time claim acceptance to 97%. Earned-wage access resonates in private hospitals for shift coverage incentives. Hospitality leverages QR-code table ordering and auto split-bill features to raise throughput during labor shortages. Professional services migrate from hourly billing to retainer auto-debits using PayTo, reducing debtor days from 42 to 7 on average. Education and government lag but are accelerating through mandated electronic fee collection frameworks.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

New South Wales held 34.67% of national transaction value in 2024, reflecting Sydney’s density of fintech headquarters, venture funding, and advanced consumer adoption curves. The state’s AUD 216 billion government banking contract obliges participating banks to enable PayTo across all public-facing departments, effectively forcing underlying vendor ecosystems to adopt real-time APIs. Merchant preference for multi-acquirer redundancy also emanates from global enterprises basing regional hubs in Sydney, pushing providers to meet international uptime standards. Contactless penetration surpassed 99% of card-present volume, rendering cash almost obsolete for discretionary spend. Biometric authentication pilots at point-of-sale are underway, with early results indicating 18% faster customer throughput.

Queensland registers the fastest CAGR at 17.16% through 2030, buoyed by tourism revival and the state’s Digital Queensland blueprint mandating electronic payment acceptance across public transport and park services. Brisbane’s emerging fintech enclave benefits from lower operating costs and university talent pipelines. Earned-wage providers concentrate marketing on coastal hospitality belts, driving double-digit user adoption among shift workers. Infrastructure upgrades ahead of the 2032 Olympics include NFC ticketing and cash-free precincts, anchoring longer-term behavioral change toward digital.

Victoria sustains growth through Melbourne’s powerhouse retail and hospitality scene. The city’s tram network adopted mobile wallet ticketing in 2025, simplifying fare collection and reducing evasion. Regulatory frameworks prioritize consumer redress and data privacy, enhancing trust in digital credentials. Local tech clusters experiment with receipt-linked loyalty tokens stored in open banking wallets.

Western Australia’s mining corridor creates atypical B2B demands-bulk disbursements to fly-in-fly-out staff and multi-currency supplier settlements. Specialized platforms enable automated approvals tied to production milestones, settling via NPP for domestic suppliers and via Swift gpi for offshore vendors. Internet connectivity upgrades in Pilbara towns support tap-to-phone uptake at remote service outposts.

The Rest of Regions category-South Australia, Tasmania, ACT, and Northern Territory-narrows the digital divide as credit unions partner with cloud processors for instant issuance and open banking PFM apps. The ACCC’s least-cost routing guidelines drove small merchants here to renegotiate acquirer contracts, trimming acceptance fees by up to 18 basis points. Regional tourism boards bundle QR-code payment links in marketing collateral, easing international visitor spend.

Competitive Landscape

Australia’s payments arena is moderately concentrated. The Big Four banks plus Citibank processed 54% of transaction value in 2024, but over 120 licensed non-bank acquirers and 75 active fintech gateways fragment the remaining share. Platform convergence shapes strategy: Commonwealth Bank anchors merchants with ISO 20022-compliant invoicing and BNPL white-label add-ons, whereas NAB embeds accounting-software integrations to defend SME footholds. ANZ’s Suncorp Bank acquisition unlocks Queensland agribusiness payment flows, increasing regional bargaining power with schemes.

Fintech-first processors such as Zeller, Square, and Stripe emphasize transparent fee schedules and same-day settlement. Zeller’s modular stack lets merchants add banking and expense cards, promoting average revenue per user growth without legacy overhead. BNPL incumbents Afterpay and Zip pivot toward omnichannel PayTo subscriptions as ASIC oversight compresses margins.

Fraud mitigation becomes table-stakes; PayPal’s 2025 machine-learning suite reduced false positives by 19% in pilot merchants, sparking industry-wide model benchmarking. Value-added bundles-lending, payroll, and analytics-differentiate providers more than base transaction pricing. Multinational entrants leverage global volume discounts yet must localize for NPP compatibility. Overall competitive tension favors agile, API-native players able to adapt products within quarterly cycles.

Australia Payments Industry Leaders

-

Commonwealth Bank of Australia

-

Westpac Banking Corporation

-

National Australia Bank Ltd

-

Australia and New Zealand Banking Group Ltd

-

PayPal Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- September 2025: ANZ completed its AUD 4.9 billion purchase of Suncorp Bank, broadening its merchant acquiring base in Queensland.

- August 2025: Stripe opened acquisition talks with Tyro Payments at a proposed AUD 1.2 billion valuation, aiming for direct Asia-Pacific scale.

- July 2025: NSW government awarded a AUD 216 billion payment processing contract to Commonwealth Bank, ANZ, NAB, Westpac, and Citibank, mandating PayTo integration.

- June 2025: Amazon Australia and NAB activated PayTo for subscription billing, eliminating stored card credentials.

Australia Payments Market Report Scope

The Australian Payments Market is segmented by Mode of Payment (Point of Sale (Card Payments, Digital Wallet, Cash), Online Sale (Card Payments, Digital Wallet)), and by End-user Industries (Retail, Entertainment, Healthcare, Hospitality).

E-commerce payments include online purchases of goods and services such as purchases made on e-commerce websites and online booking of travel and accommodation. The market scope excludes online purchases of motor vehicles, real estate, utility bill payments (such as water, heating, and electricity), mortgage payments, loans, credit card bills, or purchases of shares and bonds. As for Point-of-Sale, all transactions that occur at the physical point of sale are included in the scope of the market. It includes traditional in-store transactions and all face-to-face transactions regardless of the location of the transaction. Cash is also considered for both cases (cash-on-delivery for e-commerce sales). The study looks at COVID-19's overall influence on the Australian payment ecosystem.

By Mode of Payment

| Point-of-Sale (POS) | Debit Card Payments |

| Credit Card Payments | |

| A2A Payments | |

| Digital Wallet | |

| Cash | |

| Other Points of Sale Payment Modes | |

| Online (E-commerce and In-app) | Debit Card Payments |

| Credit Card Payments | |

| A2A Payments | |

| Digital Wallet | |

| Cash-on-Delivery | |

| Other Online Sales Payment Modes |

By End-User Industry

| Retail |

| Entertainment |

| Healthcare |

| Hospitality |

| Other End-User Industries |

By Geography

| New South Wales |

| Victoria |

| Queensland |

| Western Australia |

| Rest of Regions |

| By Mode of Payment | Point-of-Sale (POS) | Debit Card Payments |

| Credit Card Payments | ||

| A2A Payments | ||

| Digital Wallet | ||

| Cash | ||

| Other Points of Sale Payment Modes | ||

| Online (E-commerce and In-app) | Debit Card Payments | |

| Credit Card Payments | ||

| A2A Payments | ||

| Digital Wallet | ||

| Cash-on-Delivery | ||

| Other Online Sales Payment Modes | ||

| By End-User Industry | Retail | |

| Entertainment | ||

| Healthcare | ||

| Hospitality | ||

| Other End-User Industries | ||

| By Geography | New South Wales | |

| Victoria | ||

| Queensland | ||

| Western Australia | ||

| Rest of Regions | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is the Australia payments market in 2025?

It stands at USD 1.07 trillion with a 16.44% CAGR outlook toward 2030.

Which payment channel is growing fastest in Australia?

Online payments post a 17.96% CAGR thanks to e-commerce and subscription billing uptake.

Why is Queensland a focus area for payment providers?

It records the highest regional CAGR at 17.16% driven by tourism recovery and state digital mandates.

What is driving fraud-prevention investment among acquirers?

Card-not-present fraud rose to AUD 868 million in 2024, pushing providers to deploy machine-learning detection.

How are earned-wage access services affecting businesses?

They lower turnover in hospitality and retail by offering employees real-time access to accrued wages.

Page last updated on: