Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

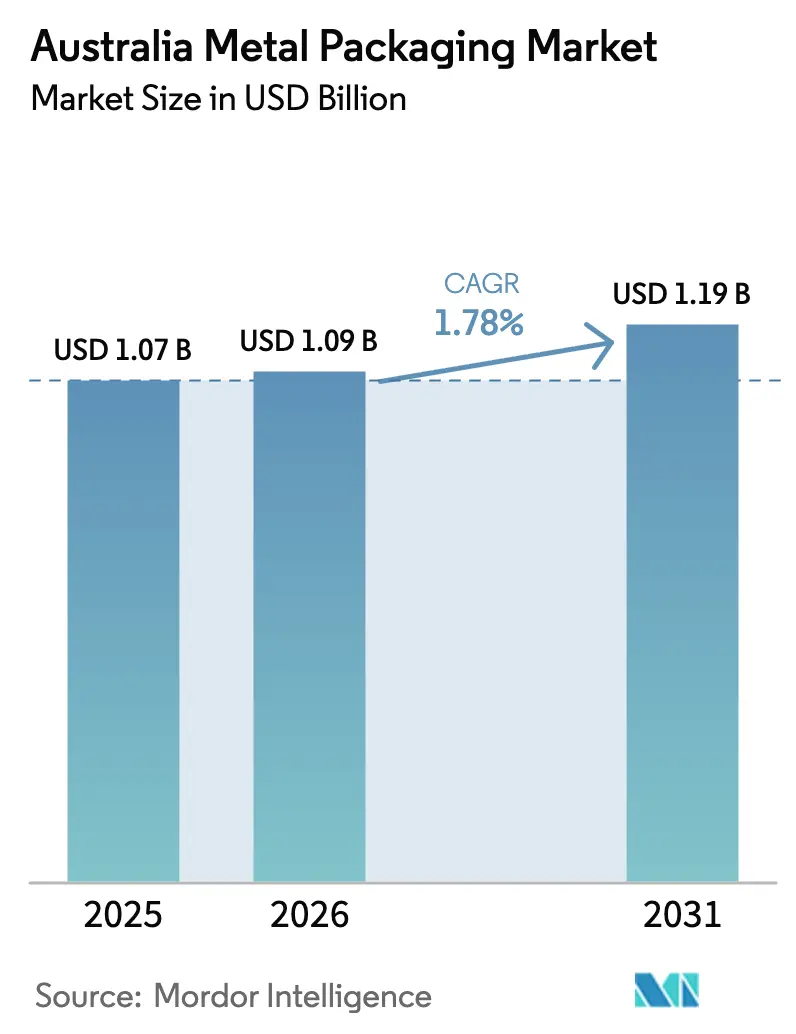

| Base Year Market Size (2025) | USD 1.07 Billion |

| Market Size (2026) | USD 1.09 Billion |

| Market Size (2031) | USD 1.19 Billion |

| Growth Rate (2026 - 2031) | 1.78% CAGR |

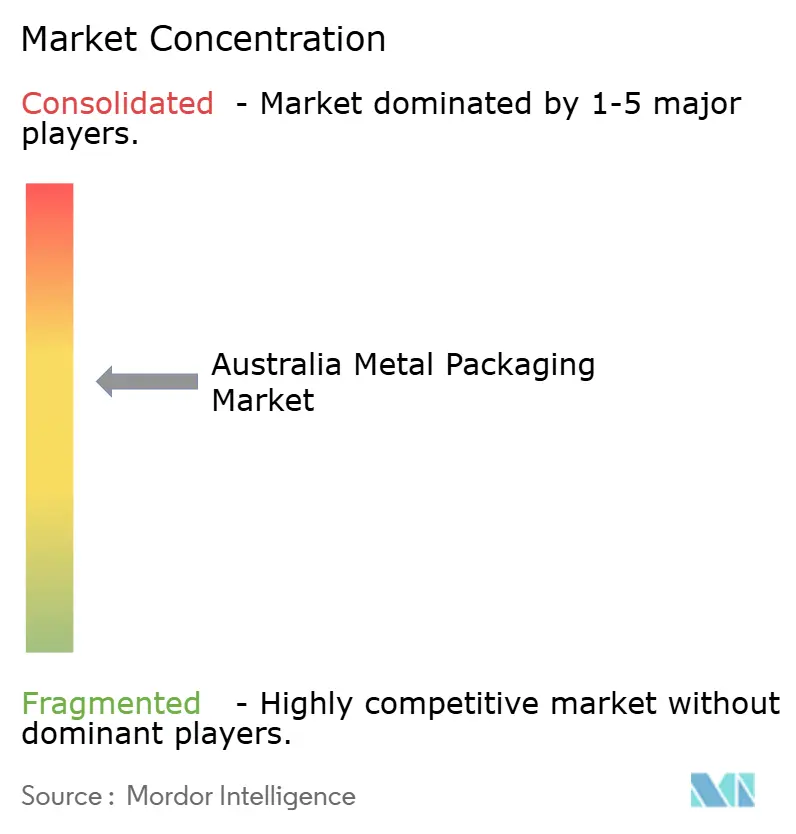

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Metal Packaging Market Analysis by Mordor Intelligence

Australia metal packaging market size in 2026 is estimated at USD 1.09 billion, growing from 2025 value of USD 1.07 billion with 2031 projections showing USD 1.19 billion, growing at 1.78% CAGR over 2026-2031. Expansion remains measured as the sector matures, yet recycling incentives, bans on single-use plastics, and shifting consumer preferences toward circular solutions continue to underpin demand. Elevated aluminum can recovery rates, surpassing 80% after the nationwide Container Deposit Scheme roll-out, dramatically improve scrap availability and lower feedstock costs, tempering raw-material volatility. State bans on plastic takeaway items redirect volume into aluminum and steel formats, particularly in the food service industry, while digital can printing allows breweries and premium brands to rotate artwork without increasing inventories. Capacity additions by Orora, Visy Industries, and Ball Corporation safeguard supply continuity and shorten lead times, reinforcing the competitive position of metal relative to glass and flexible pouches.

Key Report Takeaways

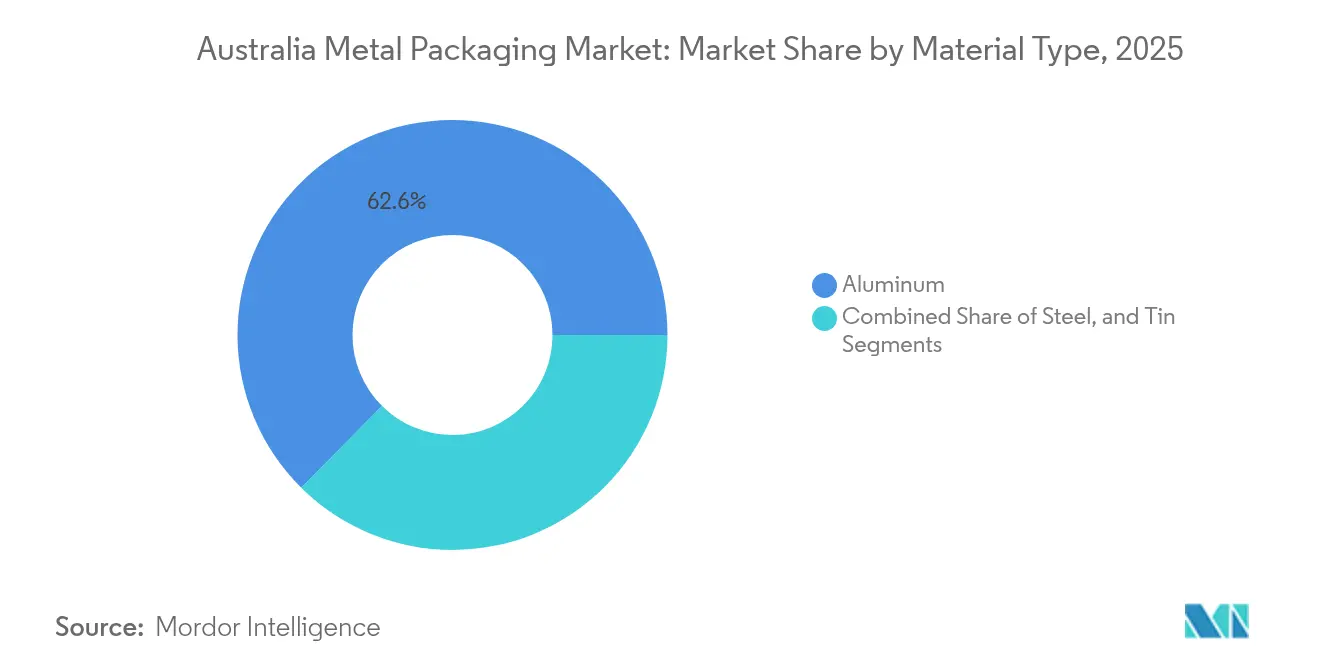

- By material type, aluminum held 62.58% of Australia metal packaging market share in 2025; steel is projected to post the fastest 2.39% CAGR through 2031.

- By product type, cans led with 41.85% revenue share in 2025, whereas bulk containers are poised to expand at a 1.97% CAGR to 2031.

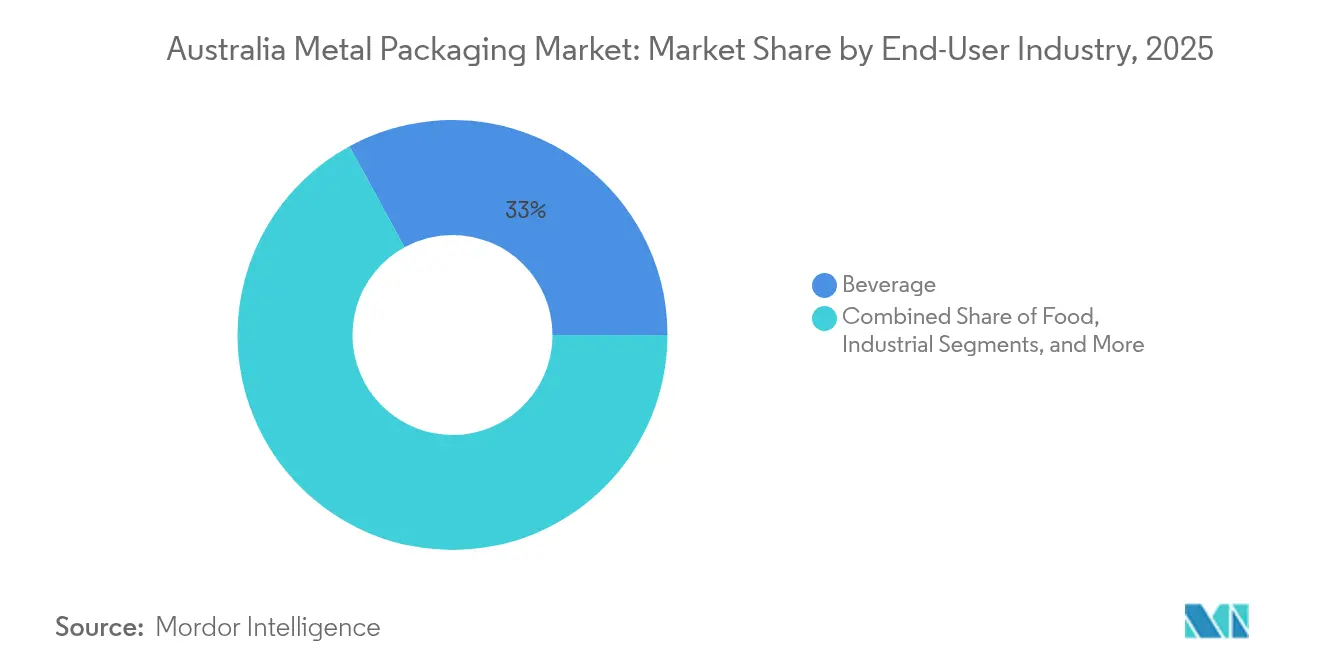

- By end-user industry, beverages accounted for 32.95% of the Australia metal packaging market size in 2025, while industrial users are set to grow at a 2.67% CAGR over the same horizon.

- By coating type, epoxy phenolic commanded 39.12% share of the Australia metal packaging market size in 2025, yet BPA-free systems are advancing at a 2.44% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Metal Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of aluminum beverage can recycling initiatives | +0.4% | National; early gains in NSW, Victoria, Queensland | Medium term (2-4 years) |

| Growing preference for lightweight and shelf-stable packaging | +0.3% | National; concentrated in urban centers | Long term (≥4 years) |

| Stringent Australian regulations on single-use plastic | +0.5% | National; state implementation varies | Short term (≤2 years) |

| Rising demand from craft beer industry for aluminum cans | +0.2% | National; Melbourne, Sydney, Brisbane hubs | Medium term (2-4 years) |

| Surge in demand for metal aerosol cans for insect repellents | +0.1% | National; tropical regions seasonality | Short term (≤2 years) |

| Adoption of digital printing on cans enabling limited-edition marketing | +0.2% | National; premium segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Aluminum Beverage Can Recycling Initiatives

Nationwide deposit refunds now cover every state, lifting aluminum recovery to 80-85%, which is well above plastics, and unlocking an annual AUD 200 million incentive stream that supports closed-loop supply chains. Visy Industries and its partners have demonstrated cans with 83% recycled content, achieving 95% lower energy consumption compared to primary smelting, resulting in substantive emissions offsets that meet the demands of emerging carbon-pricing regimes.[1]Australian Packaging Covenant Organisation, “Recycling and Recovery Report 2024,” packagingcovenant.org.au High scrap flow steadies input costs and supports capacity expansions, encouraging beverage brand owners to specify aluminum over PET. As federal climate rules tighten, the material’s recycling advantage widens compliance gaps versus single-use plastics.

Stringent Australian Regulations on Single-Use Plastic

State bans enforced between 2022 and 2024 have removed roughly 2.7 billion plastic articles from circulation, redirecting demand toward metal formats in takeaway and retail channels. Victoria’s curbs on plastic containers and Queensland’s broader scope covering plates and bowls create immediate substitution wins for aluminum trays and steel cans. Extended Producer Responsibility proposals assign lifecycle fees that favor readily recyclable substrates, narrowing price differentials with plastics and motivating retailers to regroup their assortments around metal pack formats. Compliance levies of AUD 0.15–0.30 (USD 0.097-0.19) per plastic unit further enhance the cost competitiveness of metal packaging.

Growing Preference for Lightweight and Shelf-Stable Packaging

Freight can account for up to 20% of the delivered packaging cost across Australia’s long-haul routes. Aluminum cans offer a 40% weight savings versus glass, reducing emissions and fuel costs for beverage shippers. The mining sector relies on lightweight steel drums to limit backhaul expense from remote sites, while digital decoration supports agile production runs that trim warehousing budgets for craft beverage firms. Durability and long shelf life also underpin resilience during bushfire-related supply disruptions, prompting supermarkets to prioritize canned goods for emergency stocking.

Rising Demand from Craft Beer Industry for Aluminum Cans

Craft beer volumes have increased by 12% annually, and independent brewers now account for 8.2% of national beer output, with cans being favored for blocking oxygen and light, which can degrade hop-forward styles. Asahi’s AUD 60 million (USD 38.97 million) canning upgrade underscores mainstream acknowledgment that canned presentation best supports brand freshness and sustainability targets. Excise advantages and rapid packaging line changeovers allow small brewers to capitalize on seasonal releases, further cementing the shift from glass to metal.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in aluminum and steel commodity prices | -0.3% | National; import-dependent regions | Short term (≤2 years) |

| Increasing shift toward flexible pouches in food packaging | -0.2% | National; processed foods | Medium term (2-4 years) |

| Capacity constraints at domestic can sheet rolling mills | -0.2% | National; seasonal peaks | Medium term (2-4 years) |

| Consumer concerns over BPA alternatives in can coatings | -0.1% | National; health-focused consumers | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatility in Aluminum and Steel Commodity Prices

Spot aluminum swung 15–20% during 2024 as smelters grappled with energy cost spikes, while steel import duties of 15–25% aimed at dumping have tightened domestic availability.[2]Australian Bureau of Statistics, “International Trade: Goods and Services,” abs.gov.au Raw materials account for nearly 70% of the finished can cost, leaving converters vulnerable to price shocks until recycling streams fully stabilize. Currency fluctuations add another layer of risk, given Australia’s reliance on bauxite and specialty steel imports.

Increasing Shift Toward Flexible Pouches in Food Packaging

Lightweight pouches are growing 15–20% each year in processed foods and pet nutrition categories based on cost and shipping benefits. Although multilayer laminates challenge curbside collection systems and remain excluded from deposit schemes, brand owners value the perceived sustainability of reduced transport emissions. Metal packaging suppliers respond by highlighting 90%+ recycling rates and developing peel-seal can ends that mimic the convenience of pouches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Aluminum Leads Amid Steel's Accelerating Growth

Aluminum controlled 62.58% of 2025 revenue, underpinned by its closed-loop advantage under the Container Deposit Scheme and strong adoption in beverages and aerosols. Steel, although still secondary, is forecast to capture the fastest 2.39% CAGR, driven by demand for chemical drums and industrial containers in mining hubs. The Australia metal packaging market relies on Rio Tinto’s scrap partnerships and domestic smelter output to keep aluminum price-competitive, whereas BlueScope backs steel’s resilience through localized supply.

Continual furnace upgrades enable higher recycled inputs, reducing scope 1 emissions and meeting procurement criteria tied to the National Circular Economy Strategy. Despite tinplate’s niche role in premium confectionery, its decorative appeal and barrier traits retain loyal downstream users. Guardrails on carbon intensity implied by state-based procurement add momentum to aluminum’s installed base, signaling sustained leadership even as steel grows in distinct heavy-duty niches.

By Product Type: Cans Dominate While Bulk Containers Surge

Cans generated 41.85% of 2025 turnover and anchor the public’s perception of the Australia metal packaging market, spanning carbonated soft drinks, beer, RTDs, canned meals, and aerosols. Bulk containers, including drums, IBCs, and pails, register the highest 1.97% CAGR, thanks to rising volumes of critical minerals processing fluids and agricultural chemicals. As colorful, digitally printed wraps propel can shelf presence, corrosion-resistant linings and UN ratings elevate bulk metal formats above plastics for hazardous goods.

The Australia metal packaging market size tied to craft brewing alone warranted numerous can line upgrades, yet drums have quietly extended into lithium brine transport where permeation resistance overrides cost. Suppliers now tout life-cycle LCAs that show repeat-use steel IBCs offset initial carbon debt within five cycles, framing the category as an emission-reducing solution for logistics-intensive resources businesses.

By End-User Industry: Beverage Leadership Challenged by Industrial Growth

Beverages accounted for 32.95% of the market in 2025 and remain the emotional core of brand marketing spend. Energy drinks, hard seltzers, and functional RTDs keep aluminum innovation at the forefront, sustaining investment in matte finishes and augmented reality QR codes. However, industrial users are projected to outpace all sectors at a 2.67% CAGR, capitalizing on an expanding pipeline of battery-chemicals, paint, and specialty solvents operations.

The Australia metal packaging market share between beverage and industrial segments thus evolves toward parity by 2030 as miners specify steel and aluminum solutions that satisfy rigorous safety codes issued by Authorities Having Jurisdiction. Food can volume stabilizes under competitive pressure from pouches yet retains strategic relevance for emergency rations and export-oriented produce where dent-resistant steel remains the gold standard.

By Coating Type: Epoxy Phenolic Dominance Faces BPA-Free Challenge

Epoxy phenolic coatings accounted for a 39.12% share in 2025 due to their proven resistance to high-acid conditions. BPA-free options, growing at a 2.44% CAGR, now receive priority R&D budgets by AkzoNobel and PPG. Novel polyester systems claiming equal retort endurance aim to secure beverage approvals by 2026, although converters must adapt their curing profiles and validation protocols.

The Australia metal packaging market size associated with liner upgrades stays modest initially, yet brand commitments to bisphenol-free timelines accelerate volume shift. Regulatory gatekeepers add impetus by evaluating migration from next-generation monomers, guiding formulators to adopt fully disclosed chemistries that enhance consumer trust without sacrificing production rates.

Geography Analysis

New South Wales and Victoria jointly form the economic epicenter, absorbing roughly 60% of metal pack shipments thanks to dense populations, food-processing clusters, and major distribution hubs. NSW topped 85% aluminum can return rates in 2025, driving the lowest feedstock costs nationwide and giving local fillers a material margin edge. Victoria’s manufacturing renaissance fuels a steady demand for steel drums used in the chemical and paint industries, while its metropolitan consumer base drives the production of high-graphic beverage cans.

Queensland’s tropical climate intensifies demand for aerosol insecticides and RTD beverages; its mining hinterland concurrently boosts orders for heavy-gauge drums and IBCs. Western Australia, despite a lower population, accounts for a disproportionate bulk of container volume tied to iron-ore and lithium operations that prefer robust steel over plastic. South Australia benefits from premium wine exports that specify aluminum closures with oxygen-scavenging liners for cellarable vintages.

Tasmania and the Northern Territory remain smaller but strategic. Tasmania’s craft beverage scene sources cans from mainland converters but advertises 100% renewable power, using carbon-neutral can badges for differentiation. The NT’s defense infrastructure calls for MIL-spec metal containers for fuels and munitions, anchoring specialty demand at consistent levels. Finally, the Australian Capital Territory increasingly mandates sustainable packaging in government procurement tenders, functioning as a testbed for high-recycled-content formats that could later scale nationwide.

Interstate freight regulations award a clear advantage to aluminum’s lower weight for transcontinental hauls. Conversely, the cost premium of shipping empty drums from the east coast to Western Australia has triggered localized refurbishment networks, reinforcing circularity and cutting turnaround times. These regional dynamics collectively steer suppliers to diversify footprints and hedge against localized capacity squeezes during summer beverage peaks.

Competitive Landscape

Moderate consolidation defines the Australia metal packaging market, as Orora, Visy Industries, Ball Corporation, Crown Holdings, and Silgan Holdings collectively account for about two-thirds of sales. Orora’s USD 130 million Rocklea expansion can boost output by 40%, underscoring management’s view that localized capacity pays off in freight savings and delivery agility. Visy’s Re-In-Can-Ation initiative, which delivers 83% recycled aluminum cans, elevates its ESG profile and contributes to brewer sustainability scorecards, securing multi-year supply contracts.

International majors pursue scale efficiencies: Ball Corporation’s Ballarat site added two lines with digital printing to tap into the growing craft and energy drink segments, while Crown’s aerosol investment broadens the product mix into high-growth personal-care and insect-repellent niches. Smaller players, such as Onpack and East Coast Canning, compete on service flexibility, leveraging mobile filling and short-run digital graphics to attract microbreweries.

Technological differentiation hinges on inline vision systems, smart-factory analytics, and blockchain-enabled traceability that verifies recycled content. Capital intensity and stringent food-grade accreditation keep entry barriers high, yet niche opportunities remain for startups offering refillable steel keg programs or direct-to-consumer personalized can designs. Overall rivalry stays disciplined, with capacity expansions calibrated to national demand plus limited export potential into New Zealand and the Pacific.

Australia Metal Packaging Industry Leaders

Amcor plc

Orora Limited

Visy Industries Holdings Pty Ltd

Ball Corporation

Crown Holdings, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Visy Industries committed AUD 85 million to AI-driven upgrades at Smithfield, NSW.

- September 2025: The federal government’s National Circular Economy Strategy aims to achieve 90% aluminum recycling by 2028 and secure AUD 150 million (USD 97.43 million) in funding for infrastructure.

- August 2025: Orora and Novelis opened a 50,000-ton closed-loop recycling plant in Melbourne.

- July 2025: Ball Corporation allocated AUD 120 million to double Ballarat output to 1.2 billion cans.

Australia Metal Packaging Market Report Scope

Packaging provides a protective and informative covering to the product and protects the product during handling, storage, and movement. It also provides useful information about the content of the package. Packaging products made using aluminum, tinplate, or steel is termed metal packaging. It comes in various shapes and sizes and can package virtually any product. Metal packaging provides excellent barrier properties and is widely used in food packaging applications. They are used in different package forms and as closures, such as for glass bottles and composite cans.

The study tracks the demand for the metal packaging market through the revenue derived from metal. It also includes the effect of regulations and drivers on market growth. The Australia Metal Packaging Market is Segmented by Materials Type (Aluminum, Steel), Product Type (Cans, Bulk Containers, Shipping Barrels and Drums, Caps and Closures), and End-User (Beverage, Food, Paint & Chemical, Industrial). The market sizes and projections are provided (in USD million) for all the mentioned segments.

By Material Type

| Aluminum |

| Steel |

| Tin |

By Product Type

| Cans | Food Cans |

| Beverage Cans | |

| Aerosol Cans | |

| Decorative Cans | |

| Bulk Containers | |

| Drums and Barrels | |

| Caps and Closures | |

| Other Product Types |

By End-User Industry

| Food |

| Beverage |

| Paints, Coatings and Chemicals |

| Pharmaceuticals and Healthcare |

| Industrial |

| Other End-user Industries |

By Coating Type

| Epoxy Phenolic |

| Acrylic |

| Polyester |

| BPA-Free Alternatives |

| Other Coating Types |

| By Material Type | Aluminum | |

| Steel | ||

| Tin | ||

| By Product Type | Cans | Food Cans |

| Beverage Cans | ||

| Aerosol Cans | ||

| Decorative Cans | ||

| Bulk Containers | ||

| Drums and Barrels | ||

| Caps and Closures | ||

| Other Product Types | ||

| By End-User Industry | Food | |

| Beverage | ||

| Paints, Coatings and Chemicals | ||

| Pharmaceuticals and Healthcare | ||

| Industrial | ||

| Other End-user Industries | ||

| By Coating Type | Epoxy Phenolic | |

| Acrylic | ||

| Polyester | ||

| BPA-Free Alternatives | ||

| Other Coating Types | ||

Key Questions Answered in the Report

How big is the Australia metal packaging market in 2026?

It is valued at USD 1.09 billion, with a forecast to reach USD 1.19 billion by 2031 under a 1.78% CAGR.

Which material dominates metal packaging demand across Australia?

Aluminum leads with 62.58% share thanks to its closed-loop recycling economics and popularity in beverage cans.

What segment is growing fastest within Australia’s metal packaging landscape?

Industrial applications, especially mining and chemicals, are expanding at a 2.67% CAGR as demand rises for corrosion-resistant drums and IBCs.

How are single-use plastic bans affecting packaging choices?

Statewide bans have removed billions of plastic items, shifting food service and retail toward aluminum and steel options that already fit robust recycling systems.

Why are craft brewers choosing cans over bottles?

Aluminum cans shield beer from light and oxygen, align with sustainability messaging, and enable small-batch digital graphics that strengthen brand storytelling.

What technology trend is reshaping can decoration?

Digital printing lets converters produce limited editions without plates, cutting lead times and permitting high-resolution artwork for seasonal promotions.

Page last updated on: