Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

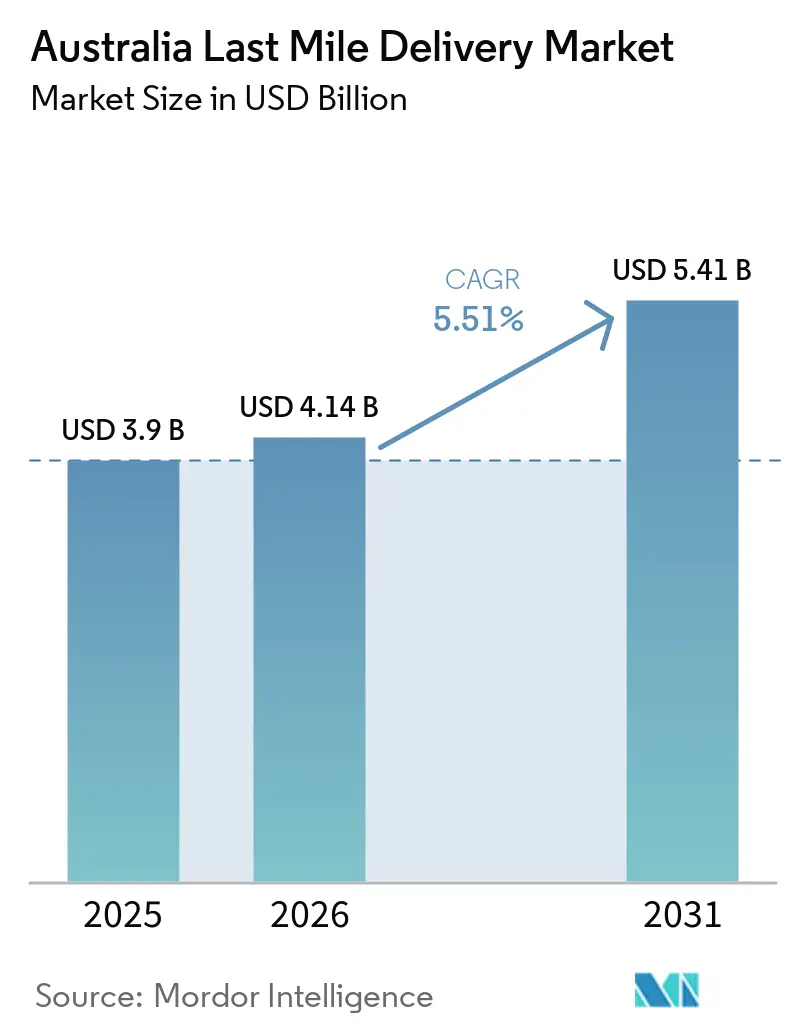

| Base Year Market Size (2025) | USD 3.9 Billion |

| Market Size (2026) | USD 4.14 Billion |

| Market Size (2031) | USD 5.41 Billion |

| Growth Rate (2026 - 2031) | 5.51% CAGR |

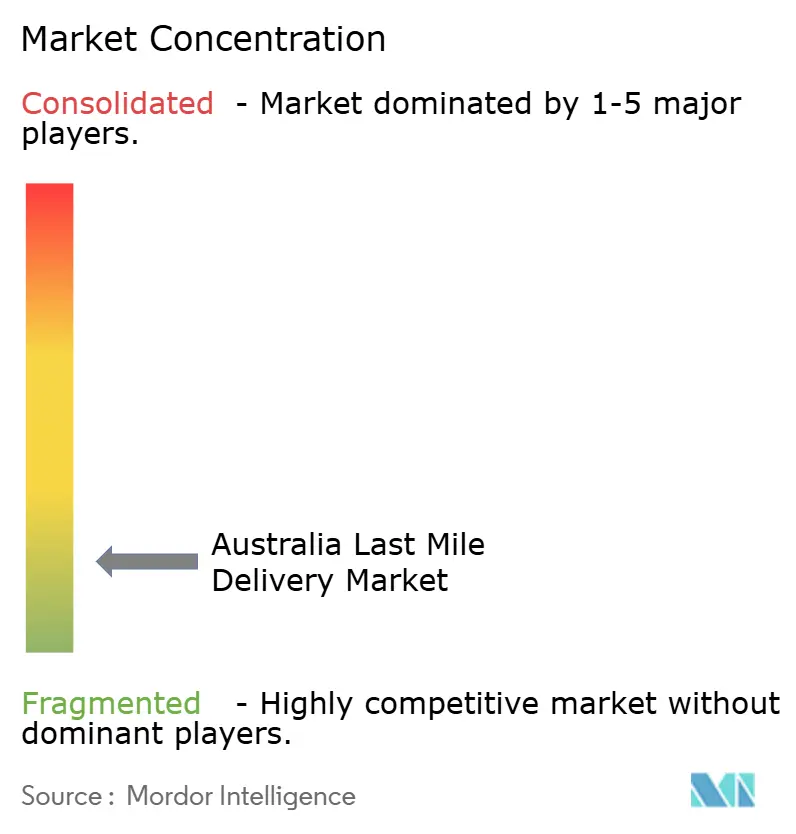

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Last Mile Delivery Market Analysis by Mordor Intelligence

The Australia last mile delivery market size is expected to grow from USD 3.90 billion in 2025 to USD 4.14 billion in 2026 and is forecasted to reach USD 5.41 billion by 2031 at 5.51% CAGR over 2026-2031.

Long-run growth remains steady, yet the underlying structure is being reordered by rapid-fulfillment grocery models that require dense urban micro-fulfillment, by postal-network reforms that unlock rural capacity, and by subscription services that smooth demand volatility. Regulatory support for Beyond Visual Line of Sight (BVLOS) drones is opening new peri-urban corridors, while corporate net-zero mandates are accelerating fleet electrification. Driver shortages, rising cybersecurity threats, and costlier insurance for gig couriers constrain pure capacity additions, so competitive advantage is shifting toward technology-enabled productivity gains.

Key Report Takeaways

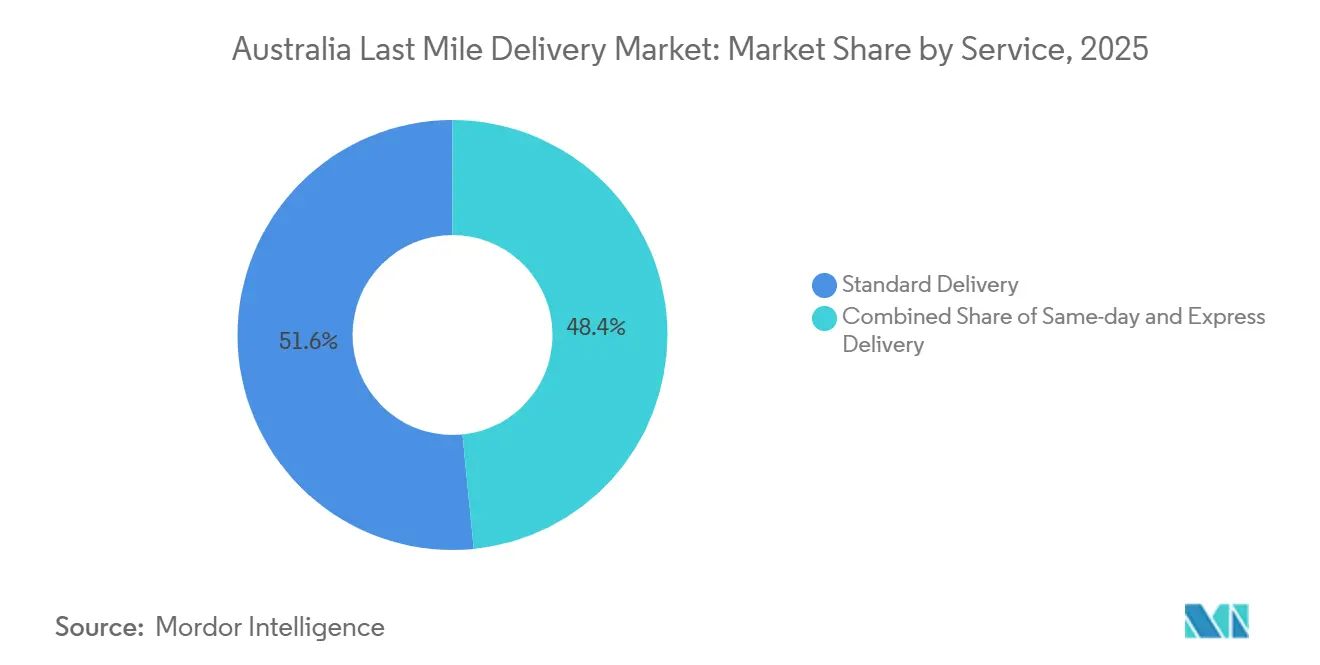

- By service, standard delivery held 51.58% of the Australia last mile delivery market share in 2025, while same-day delivery is advancing at a 6.06% CAGR through 2031.

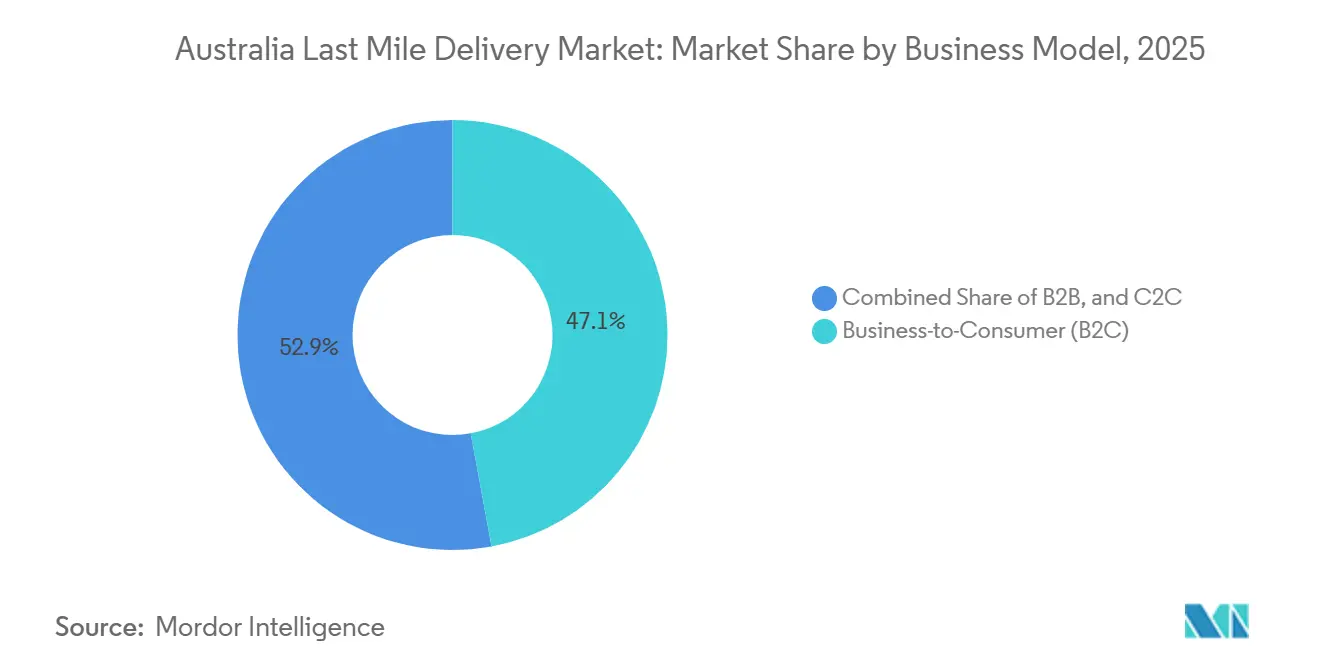

- By business model, business-to-consumer transactions commanded 47.09% share of the Australia last mile delivery market size in 2025 and are growing fastest at 6.18% CAGR to 2031.

- By end-user, e-commerce retail accounted for 26.11% of 2025 demand, whereas Fashion & Lifestyle posts the strongest expansion at 6.24% CAGR over 2026-2031.

- By region, New South Wales contributed 30.90% of 2025 value, but Queensland leads growth with a 5.92% CAGR during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Last Mile Delivery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of "quick-commerce" grocery & convenience ecosystems | +1.4% | Metro areas: Sydney, Melbourne, Brisbane, Perth | Short term (≤ 2 years) |

| Post26 postal-reform efficiencies unlocking new parcel capacity | +1.1% | National, regional Australia priority | Medium term (2-4 years) |

| Subscription-based delivery models for meal-kits & consumables boosting volume predictability | +0.8% | National, urban concentration | Medium term (2-4 years) |

| Corporate net-zero supply-chain mandates driving carrier partnerships | +0.7% | National, multinational corporations | Long term (≥ 4 years) |

| On-demand B2B spare-parts & field-service logistics enabled by additive manufacturing | +0.6% | Industrial hubs: NSW, VIC, WA | Medium term (2-4 years) |

| Regulatory green-light for BVLOS drone corridors in peri-urban zones | +0.4% | Peri-urban: Logan QLD, Canberra ACT | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of "Quick-Commerce" Grocery & Convenience Ecosystems

Quick-commerce grocery chains are redefining urban fulfillment economics by situating stock within micro-fulfillment hubs inside existing supermarkets, enabling sub-60-minute delivery windows demanded by affluent urban shoppers. Woolworths rolled out Metro60 across 50-plus stores in 2024, recording 86% of Business-to-Consumer orders delivered within 24 hours. Coles On Demand scaled to 400 stores and delivered 30.1% e-commerce revenue growth to AUD 3.295 billion (USD 2.10 billion) Dense order clustering raises drop density and yields higher revenue per route, yet limits roll-out to catchments where spending power offsets premium delivery fees. The model therefore amplifies a two-tier market: metropolitan zones secure lightning-fast options while regional communities remain on next-day schedules. Operators responding fastest with distributed inventory, analytics-driven demand forecasting, and dedicated rider fleets gain the most share. Capital flows accordingly into automated dark stores, e-bike fleets, and dynamic routing software[1]HelloFresh, “HelloFresh Australia Operations,” hellofresh.com.au.

Post26 Postal-Reform Efficiencies Unlocking New Parcel Capacity

Australia Post’s modernization agenda, fully in force by late 2025, raised allowable parcel volumes per postal round and upgraded sorting automation to push more freight through existing headcount. During 1H 2025 the operator handled 262 million parcels and lifted revenue 6.3% year-on-year to AUD 5.01 billion (USD 3.20 billion) while improving profitability, confirming that the reforms deliver both scale and margin upside. Resulting efficiencies particularly benefit lower-density regions where historical economics prevented frequent service. By consolidating letters into fewer rounds and layering additional parcels onto each route, the universal service provider essentially subsidizes rural e-commerce, giving it a structural cost edge against private carriers in sparsely populated corridors. Competitors must either match delivery frequency at higher cost or restrict coverage, reinforcing Australia Post’s incumbent advantage outside major cities.

Subscription-Based Delivery Models for Meal-Kits & Consumables Boosting Volume Predictability

Weekly meal-kit shipments from HelloFresh and Marley Spoon create steady, forecastable volumes that logistics partners can slot into fixed capacity, reducing the cost volatility inherent in ad-hoc parcel flows. Predictability enables tighter route design, earlier labor scheduling, and higher truck fill rates, producing margin uplift for carriers and cheaper shipping for platforms. The concept is proliferating into pet supplies, personal-care refills, and consumable home goods, extending a growing baseline of routine deliveries. Operators blending these smooth flows with peak-hour on-demand volumes see better asset utilization across the week. Technology that allocates subscription boxes first, then overlays variable demand, is becoming a core differentiator for fleet owners seeking resilience against fuel and wage inflation.

Corporate Net-Zero Supply-Chain Mandates Driving Carrier Partnerships

Large multinationals now benchmark logistics vendors on Scope 3 emissions performance, turning sustainability into bid-qualification criteria. DHL operates 39,100 electric pick-up and delivery vehicles worldwide, already achieving 37.6% electrification, while FedEx targets carbon neutrality by 2040. Domestically, Team Global Express secured AUD 20.1 million (USD 12.86 million) in ARENA funding to trial 60 electric trucks in Sydney, pairing renewable charging with telematics to verify carbon reductions. Carriers that invest in zero-emission fleets, renewable depots, and granular emissions reporting unlock procurement preference with enterprise shippers. Smaller couriers lacking capital to retrofit fleets risk exclusion from high-value corporate lanes, accelerating consolidation toward operators capable of meeting environmental scorecard thresholds.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter local-council night-time delivery curfews limiting delivery windows | -0.9% | Urban centers: Sydney, Melbourne, Brisbane | Short term (≤ 2 years) |

| Worsening professional-driver shortage amid ageing workforce & licence-cost hikes | -1.2% | National, acute in regional areas | Medium term (2-4 years) |

| Escalating cyber-attacks on delivery-management platforms causing service disruption | -0.7% | National, technology-dependent operators | Short term (≤ 2 years) |

| Soaring insurance premiums for gig-economy couriers, e-bikes & drone fleets | -0.6% | Metro areas, platform operators | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stricter Local-Council Night-Time Delivery Curfews Limiting Delivery Windows

Municipal noise controls introduced in Melbourne, Sydney, and Brisbane compress deliveries into daytime slots already congested with commuter traffic. Operators lose the off-peak efficiency that once enabled three extra nightly routes, pushing fleet utilization lower and raising cost per drop. Quick-commerce players face direct conflict because their value proposition hinges on late-night availability. Route-planning software must now embed council-by-council time-window logic, increasing complexity and mileage. Carriers offering electric vans and e-bikes can lobby for exemptions on the basis of low-noise operation, but rule fragmentation across 500-plus local governments makes blanket solutions elusive[2]Australian Cyber Security Centre, “Cyber Threat Report 2024-2025,” cyber.gov.au.

Worsening Professional-Driver Shortage Amid Ageing Workforce & Licence-Cost Hikes

Aging demographics and costly licence training are eroding Australia’s pool of qualified drivers, especially in regional towns where population density is thin. Average hourly wages of AUD 24.53 (USD 15.70) for delivery drivers trail mining or construction roles, making recruitment harder. Carriers therefore raise wages or shift to gig platforms, yet both inflate operating costs. Autonomous vans and delivery robots remain multiple regulatory stages away from broad deployment. Until they scale, operators must stretch existing labor through dynamic routing, parcel lockers, and shift-sharing none of which fully offset the structural workforce gap[3]Fair Work Australia, “Wage and Salary Information 2025,” fairwork.gov.au.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Same-Day Acceleration Redefines the Mix

Standard Delivery retained 51.58% of Australia last mile delivery market due to its cost advantage on non-urgent items, but Same-day is on track for a 6.06% CAGR that will steadily dilute that dominance. The Australia last mile delivery market for Same-day offerings is projected to expand faster than any other tier as quick-commerce retailers promise groceries in under two hours. Standard networks respond by automating mega-hubs such as Australia Post’s USD 33 million Brisbane plant, which sorts 176,000 parcels daily, trimming process time to remain competitive.

Investments in micro-fulfillment and real-time routing algorithms compress pick-pack-deliver cycles, allowing grocery and pharmacy chains to migrate repeat customers into paid rapid-delivery memberships. Express Delivery occupies a middle ground; its next-day promise sustains relevance for mid-value goods, yet it faces squeeze from cheaper Standard and faster Same-day tiers. Over time, operators blending cross-docking, in-store picking, and crowdsourced couriers can flex capacity across tiers, preserving margins despite rising service expectations. The Australia last mile delivery market therefore pivots toward differentiated service levels where speed and reliability, not just price, dictate customer loyalty.

By Business Model: Consumer Parcels Power Network Economics

Business-to-Consumer consignments supplied 47.09% of Australia last mile delivery market size turnover and outpace overall growth with a 6.18% CAGR to 2031. The B2C segment of Australia last mile delivery market should widen because supermarket, fashion, and electronics retailers keep migrating in-store purchases online. Higher volume per suburb enables tighter route density, pulling down unit costs even as service levels rise.

Business-to-Business traffic remains essential where predictable weekday schedules and specialized requirements fetch premium yields. Medical, industrial, and office-supply shippers value punctuality and compliance more than raw speed. Customer-to-Consumer flows peer-to-peer resale and social-commerce parcels demand ad-hoc pick-ups from residential addresses and are less profitable, yet carriers integrate them to boost off-peak backhauls. The Australia last mile delivery industry continues to orient fleet investment toward B2C because that segment drives scale, technology funding, and strategic partnerships with major retailers.

By End-User Industry: Fashion Gains Momentum Beyond General Retail

E-commerce Retail contributed 26.11% of Australia last mile delivery market share, anchoring the network’s baseline. Fashion & Lifestyle, however, is advancing 6.24% CAGR, becoming the fastest enlarging vertical as return-friendly policies and social-media marketing normalize online apparel buys. This creates demand for reverse-logistics sophistication, size-swap automation, and eco-friendly packaging.

Beauty & Wellness shipments require temperature stability and compliance with ingredient regulations, while Consumer Electronics parcels command high security standards. Home & Furniture orders involve bulky, high-touch deliveries with assembly services, pulling some couriers into white-glove territory. Healthcare & Medical volumes, fueled by the Sigma-Chemist Warehouse merger and Toll’s AUD 100 million (USD 64 million) regional investment, require GDP-compliant cold chains. The Australia last mile delivery market therefore fragments along industry lines, each with distinct handling, speed, and compliance thresholds that reward carriers able to tailor service bundles.

Geography Analysis

Queensland’s 5.92% CAGR crowns it the quickest-growing state market through 2031, buoyed by population inflows, tourism rebound, and intensive e-commerce adoption along the Gold Coast-Brisbane-Sunshine Coast corridor. Australia Post’s AUD 12 million (USD 7.68 million) Gold Coast facility and Wing’s BVLOS drone trials in Logan showcase the state’s embrace of both traditional and emergent capacity solutions. Enhanced highway and rail funding under the Queensland Government’s AUD 37.4 billion (USD 23.94 billion) transport plan further shrinks transit times, positioning carriers to capture rural and regional volumes that once defaulted to slower services[4]Queensland Treasury, “Queensland Budget 2024-25,” budget.qld.gov.au.

New South Wales remains the largest prize with 30.90% of the 2025 value. Sydney’s density delivers unmatched route productivity, yet congestion, kerb-access restrictions, and night-time curfews pressure cost-to-serve. Federal spending of AUD 17.1 billion (USD 10.94 billion) on Western Sydney road upgrades and Team Global Express’s AUD 1.8 billion (USD 1.15 billion) rail freight pact with Aurizon aim to relieve bottlenecks and decarbonize line-haul legs. Service innovation, therefore, balances volume opportunity against intensifying regulatory complexity.

Victoria leverages Melbourne’s retail and tech ecosystems, with Coles investing AUD 400 million (USD 256 million) in robot-rich customer fulfillment centers, solidifying the state as a hub for automated last-mile experimentation. Western Australia’s resource economy sustains premium B2B demand across remote mining towns, justifying air charters and heavy-duty 4×4 fleets. South Australia and Tasmania showed growth as infrastructure expansions made premium delivery economically feasible. Geographic diversification across states insulates national networks from localized shocks but necessitates flexible asset deployment and state-by-state regulatory compliance.

Competitive Landscape

The Australia last mile delivery market is low concentrated. Australia Post and subsidiary StarTrack dominate Standard Delivery, underpinned by a nationwide mandate and continuous automation. DHL Express, FedEx Express, and Toll Group anchor the Express tier, leveraging global networks for inbound cross-border flows. Retail titans Woolworths and Coles internalize a growing share of grocery parcels via Metro60, Direct-to-Boot, and automated dark stores, blurring lines between retailer and carrier.

Technology-enabled challengers such as Sherpa, and CouriersPlease exploit platform economics to aggregate SME demand and dynamically allocate to gig fleets. CouriersPlease’s 2024 merger with FMH Group and Australia Post’s 2025 stake in Shiperoo display a tilt toward digital marketplaces that match parcel attributes to optimal fleets. Drone operator Wing and electric-fleet pioneer Team Global Express carve early leadership in autonomous and low-carbon niches, each betting regulatory tailwinds will thin the field to capital-heavy players.

Strategic levers revolve around fleet electrification, integrated cyber-resilience, and subscription-volume partnerships. Players unable to finance battery trucks, install secure IT, or provide granular emissions data may lose enterprise bids. M&A activity remains likely as incumbents absorb specialist tech providers to accelerate those capabilities. The Australia last mile delivery market therefore tilts toward firms blending physical scale with software and sustainability prowess.

Australia Last Mile Delivery Industry Leaders

DHL Express

FedEx Express

Toll Group

Aramex Australia

Australia Post (StarTrack)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: DHL (broader business including Australia) planned to adjust fuel surcharge practices to weekly reviews due to volatile fuel prices from global geopolitical uncertainty.

- February 2026: Aramex (global) reported its full year 2025 financial performance in Feb 2026, noting stable revenue and improved performance trends in Oceania (including Australia) as part of its broader strategic transformation program.

- February 2025: Sigma Healthcare completed its merger with Chemist Warehouse, creating a combined AUD 30 billion (USD 19.2 billion) entity to strengthen pharmaceutical distribution.

- January 2025: Myer-Apparel Brands merger received approval, combining operations with over AUD 4 billion (USD 2.56 billion) sales and reshaping fashion-delivery demand.

Australia Last Mile Delivery Market Report Scope

By Service

| Standard Delivery |

| Same-day |

| Express Delivery |

By Business Model

| Business-to-Business (B2B) |

| Business-to-Consumer (B2C) |

| Customer-to-Consumer (C2C) |

By End-user Industry

| E-commerce Retail |

| Fashion and Lifestyle |

| Beauty, Wellness and Personal Care |

| Home and Furniture |

| Consumer Electronics and Appliances |

| Healthcare and Medical Supplies |

| Others |

By Region

| New South Wales |

| Victoria |

| Queensland |

| Western Australia |

| South Australia |

| Tasmania |

| Others |

| By Service | Standard Delivery |

| Same-day | |

| Express Delivery | |

| By Business Model | Business-to-Business (B2B) |

| Business-to-Consumer (B2C) | |

| Customer-to-Consumer (C2C) | |

| By End-user Industry | E-commerce Retail |

| Fashion and Lifestyle | |

| Beauty, Wellness and Personal Care | |

| Home and Furniture | |

| Consumer Electronics and Appliances | |

| Healthcare and Medical Supplies | |

| Others | |

| By Region | New South Wales |

| Victoria | |

| Queensland | |

| Western Australia | |

| South Australia | |

| Tasmania | |

| Others |

Key Questions Answered in the Report

How fast is the Australia last mile delivery market expected to grow by 2031?

Value is projected to rise to USD 5.41 billion by 2031, reflecting a 5.51% CAGR over 2026-2031.

Which service tier is expanding quickest across Australian metros?

Same-day delivery is advancing at a 6.06% CAGR as quick-commerce grocers drive sub-two-hour commitments.

Why are corporate net-zero targets influencing carrier selection?

Large shippers now score vendors on emissions, giving fleet-electrified carriers like DHL and Team Global Express a procurement edge.

How are sustainability targets influencing fleet choices?

Federal and state incentives drive the adoption of electric vans and trucks, with trials such as Team Global Express’ 60-truck deployment in Sydney.

Which state presents the highest five-year growth opportunity?

Queensland leads with a 5.92% CAGR thanks to population influx, tourism rebound, and infrastructure investment.

How are postal reforms affecting rural capacity?

Post26 changes let postal workers carry more parcels per round, boosting rural service frequency without proportional labor cost hikes.

Page last updated on: