Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

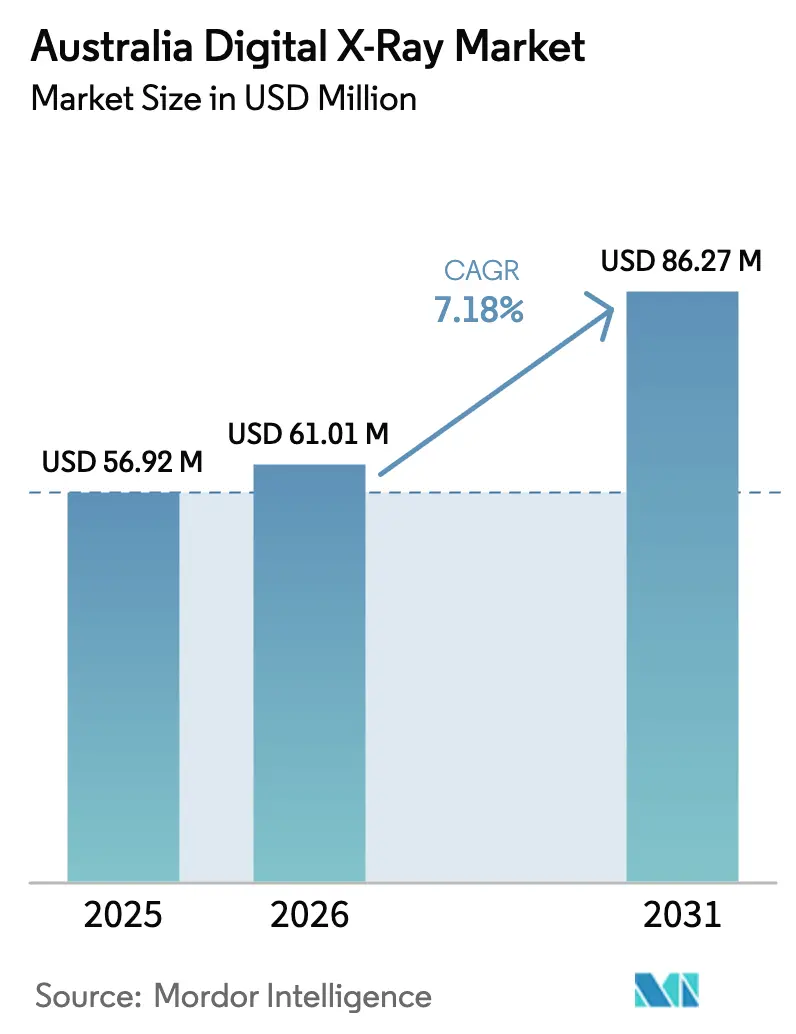

| Base Year Market Size (2025) | USD 56.92 Million |

| Market Size (2026) | USD 61.01 Million |

| Market Size (2031) | USD 86.27 Million |

| Growth Rate (2026 - 2031) | 7.18% CAGR |

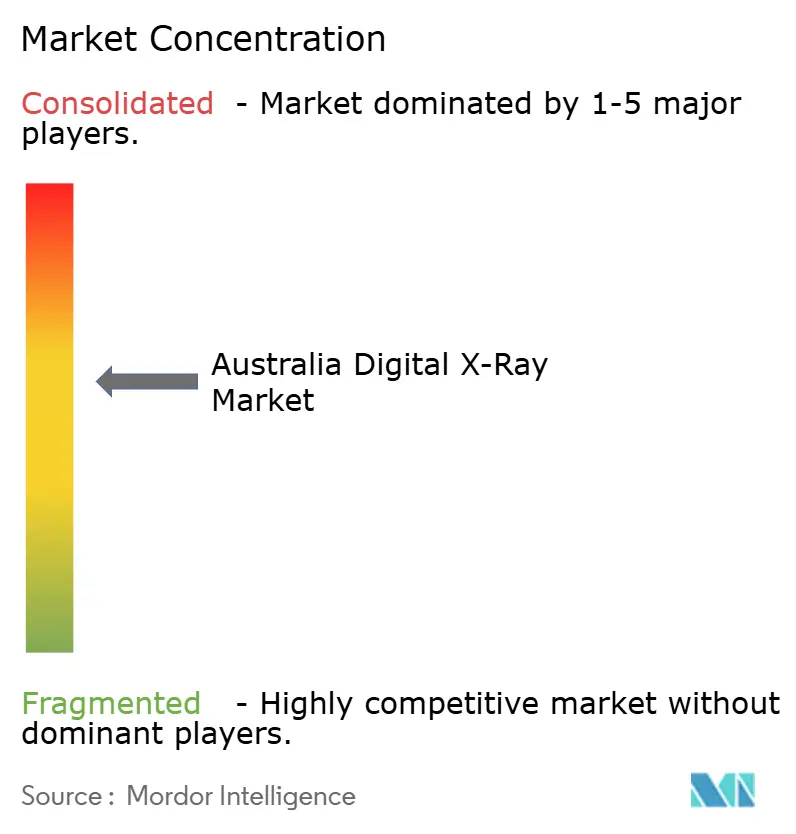

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Digital X-Ray Market Analysis by Mordor Intelligence

Australia digital X-ray market size in 2026 is estimated at USD 61.01 million, growing from 2025 value of USD 56.92 million with 2031 projections showing USD 86.27 million, growing at 7.18% CAGR over 2026-2031. Rising demand for point-of-care imaging, compulsory data-sharing requirements under My Health Record, and fast detector innovation collectively sustain robust revenue momentum across the Australia digital X-ray market. National cybersecurity rules, while adding procurement complexity, accelerate replacement of legacy systems that cannot meet the Therapeutic Goods Administration’s tighter device safeguards. Workforce shortages spur adoption of AI-ready consoles that streamline image acquisition and preliminary triage, giving vendors that bundle software subscriptions with hardware a strategic advantage. Concurrent consolidation among private diagnostic groups increases purchasing power, prompting OEMs to differentiate through mobile ergonomics, flexible detectors, and integrated cloud archiving.

Key Report Takeaways

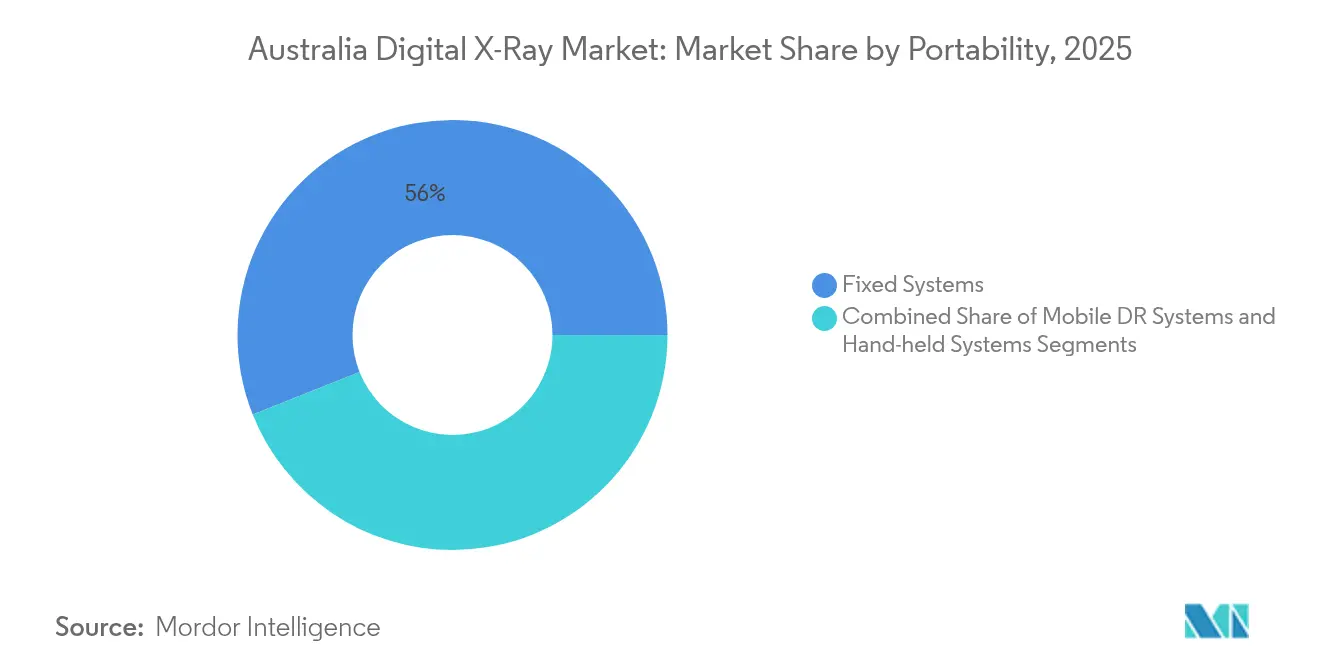

- By portability, fixed systems held 56.02% of the Australia digital X-ray market share in 2025. Mobile DR units are projected to post a 10.05% CAGR through 2031, the fastest of all portability segments.

- By detector panel, amorphous silicon accounted for 45.10% of the Australia digital X-ray market size in 2025. Flexible IGZO panels are forecast to expand at a 10.4% CAGR between 2026 and 2031.

- By application, orthopedic imaging led with 38.25% revenue share in 2025, while dental digital X-ray adoption is advancing at a 9.55% CAGR to 2031.

- By end user, hospitals and multispecialty clinics commanded 46.12% of 2025 revenues; diagnostic imaging centers are growing the quickest at 8.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Digital X-Ray Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ageing population & rising imaging demand | +2.1% | NSW, VIC, QLD | Long term (≥ 4 years) |

| Increasing prevalence of chronic diseases | +1.8% | National; higher in regional areas | Medium term (2-4 years) |

| Rapid detector & AI-based workflow innovations | +1.5% | Urban centers; spreading to regional | Short term (≤ 2 years) |

| Government push to upload images to My Health Record | +1.3% | Nationwide mandate | Medium term (2-4 years) |

| Growing adoption of telehealth and remote diagnostics | +0.8% | Rural and remote zones | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ageing Population & Rising Imaging Demand

The share of Australians aged 65 years and above is projected to reach 4.2 million by 2030, a cohort that historically undergoes 40% more radiography procedures per capita than younger groups[1]Australian Institute of Health and Welfare, “Older Australia at a Glance,” aihw.gov.au. Higher prevalence of musculoskeletal disorders within this demographic sustains orthopedic imaging volumes, ensuring stable throughput for fixed hospital suites and stimulating purchases of bedside systems that reduce patient transfers. The effect is pronounced in regional hubs where elderly residents cluster, encouraging health authorities to procure mobile DR vans that circulate among satellite clinics.

Increasing Prevalence of Chronic Diseases

Half of the adult population lives with at least one chronic condition, and repeated imaging to monitor cardiovascular and diabetic complications strengthens the long-term outlook for the Australia digital X-ray market. Digital radiography’s dose-reduction algorithms and rapid image availability align with preventive strategies outlined in the National Preventive Health Strategy, which promotes frequent community screenings[2]Department of Health, “National Preventive Health Strategy 2025,” health.gov.au. That policy backing, coupled with detector prices that continue to fall, makes large-format mobile units attractive for municipal wellness campaigns.

Rapid Detector & AI-Based Workflow Innovations

Flexible indium gallium zinc oxide (IGZO) panels weigh 30% less than conventional amorphous-silicon plates yet maintain detective quantum efficiency, enhancing the ergonomics of portable rigs favored in emergency departments. Local software leader Pro Medicus secured AUD 40 million in new AI contracts during 2025, showcasing demand for server-side algorithms that auto-prioritize cases and generate structured findings. Simultaneously, Micro-X’s carbon-nanotube cathodes eliminate filament warm-up delays, allowing truly instant-on devices for rural trauma response.

Government Push to Upload Images to My Health Record

All diagnostic imaging providers must transmit reports—and, increasingly, original DICOM images—into My Health Record within defined timeframes. The Australian Digital Health Agency’s FHIR R4 roadmap locks in a 2026 compliance deadline, effectively sidelining analog setups or early digital consoles that lack secure APIs. Vendors able to validate seamless, encrypted image transfer win procurement tenders, particularly among smaller clinics that view interoperability as mandatory rather than optional.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High equipment cost & CAPEX constraints | -1.2% | National; acute in rural regions | Medium term (2-4 years) |

| Shortage of radiographers & service engineers | -0.9% | Nationwide; severe outside metros | Long term (≥ 4 years) |

| TGA cybersecurity compliance delays procurement | -0.7% | National; affects smaller providers | Short term (≤ 2 years) |

| Limited funding and reimbursement | -0.8% | National; private sector most exposed | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Equipment Cost & CAPEX Constraints

Acquiring a floor-mounted digital room can cost AUD 500,000 (USD 320,000) even before construction fit-out, straining budgets at regional hospitals where capital grants favor urgent-care upgrades over imaging suites. Medicare reimbursement has not fully aligned with digital radiography’s higher depreciation profile, dampening ROI calculations for private clinics. As a result, refurbished consoles and detector retrofits comprise a growing slice of the Australia digital X-ray market, though resale units rarely include the cybersecurity modules now required by the TGA.

Shortage of Radiographers & Service Engineers

Vacancy rates for radiographers exceed 15% in several rural health districts, limiting scan capacity even where modern equipment is installed. The shortage extends to on-site engineers, lengthening downtime when detectors malfunction. Providers therefore seek AI features that shorten positioning time and auto-rotate images, enabling junior staff or cross-trained nurses to handle basic acquisitions. Vendors that maintain national parts depots and remote diagnostics portals gain favor because rapid field servicing reduces costly interruptions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Portability: Mobile Systems Drive Point-of-Care Expansion

Fixed suites retained 56.02% of 2025 revenues, underscoring their entrenched role in tertiary hospitals that require ceiling-suspended tubes for complex trauma workflows. Yet the Australia digital X-ray market size for mobile units is projected to climb from USD 20.9 million in 2026 to USD 33.74 million by 2031, marking a double-digit trajectory. Diagnostic centers embrace mobile carts to boost ICU throughput, while the Royal Flying Doctor Service outfits aircraft with lightweight DR sets that can be deployed on dirt airstrips.

Mobile fleets incorporate hot-swap battery packs and 5G routers, allowing images to auto-route to cloud PACS during transit. Manufacturers such as GE Healthcare now bundle ergonomic training and radiation-shielding accessories to mitigate staff fatigue. Even hand-held devices—once relegated to dental clinics—are entering geriatric wards, reducing risky patient transfers. As reimbursement parity for bedside imaging becomes widely accepted, mobile share of the Australia digital X-ray market is likely to surpass 30% by the decade’s close.

By Detector Panel Type: Flexible Panels Enable Mobile Innovation

Amorphous-silicon held 45.10% of detector shipments in 2025 and remains the cost-efficient workhorse for high-volume rooms. However, flexible IGZO plates, currently a modest niche, are forecast to contribute USD 11.1 million in incremental revenue by 2031 inside the Australia digital X-ray market. Their bend-resistant substrates survive bumps in mobile environments and weigh under 2 kg, easing maneuvering around ventilated patients. Fujifilm’s latest model achieved an IP56 ingress rating, assuring safe outdoor use during disaster triage.

Complementing hardware, AI vendors calibrate reconstruction kernels to each panel type, ensuring consistent grayscale across multi-site networks. CMOS detectors, prized for low-dose pediatric protocols, retain a loyal following in specialist children’s hospitals but lag in mainstream adoption due to higher unit costs. Combined, these technology shifts point toward a diversified detector mix wherein facilities select panel chemistries based on durability, quantum efficiency, and workflow compatibility.

By Application: Dental Digitization Accelerates Private Practice Adoption

Orthopedic imaging anchored the Australia digital X-ray market size at USD 23.37 million in 2026, benefiting from 38.25% procedure share driven by degenerative joint disease assessments. Dental radiography, historically film-based, is racing ahead with a 9.55% CAGR as clinics invest in panoramic and cone-beam systems that integrate with chairside CAD/CAM workflows. CMS reimbursement now recognizes digital panoramic codes, shortening payback cycles for small practices.

Chest and cardiovascular applications maintain steady throughput in metropolitan hospitals, yet growth is capped by modality competition from CT and MR. Conversely, veterinary and industrial inspections emerge as adjacent niches. Mining operators in Western Australia deploy ruggedized DR sets to evaluate weld integrity on site, extending vendor revenue streams beyond clinical care. Across categories, AI overlay tools that flag fractures or pulmonary nodules add subscription revenue layers and differentiate premium consoles.

By End User: Diagnostic Centers Expand Market Reach

Hospitals and multispecialty clinics commanded 46.12% of 2025 system outlays, leveraging broad case mixes and 24/7 service footprints to justify ceiling-mounted rooms. Yet diagnostic imaging chains now post the fastest ramp-up, logging a 8.72% CAGR that outpaces inpatient budgets. Their growth follows mergers such as Integral Diagnostics’ tie-up with Capitol Health, generating a 240-site network able to negotiate bulk detector pricing.

Imaging centers also pioneer teleradiology models: exams shot in regional branches upload to cloud PACS for after-hours reading by urban radiologists, leveraging Australia digital X-ray market connectivity strengths. Mobile screening units, often operated by public-private consortia, bolster government objectives to improve indigenous health access, while aged-care facilities adopt mini-carts that navigate tight corridors. Collectively, these diverse deployments illustrate how end-user segmentation drives tailored product roadmaps and service bundles.

Geography Analysis

New South Wales and Victoria generated the bulk of equipment revenue in 2024, supported by dense hospital networks and a high concentration of private imaging suites in Sydney and Melbourne. Both states completed broad My Health Record roll-outs early, so providers now prioritize hardware that proves interoperable during tender evaluations. Queensland is the fastest-growing sub-regional contributor, benefitting from population inflows, tourist-driven trauma volumes, and a vibrant mining sector demanding occupational chest films.

Western Australia and South Australia showcase differentiated purchasing patterns that favor mobile rigs capable of traversing long distances between dispersed communities. In Western Australia, fly-in-fly-out clinic teams favor ultra-portable DR carts backed by satellite connectivity. South Australia, meanwhile, leverages state grants to subsidize detector retrofits in smaller community hospitals, stretching limited capital budgets.

The Northern Territory and Tasmania, though smaller markets, post above-average system turnover rates as state governments deploy AI-ready vans that deliver on-the-spot imaging in indigenous settlements and island districts. Regulatory oversight by the ACCC ensures that consolidation among imaging chains does not stifle competition; approval of the Integral-Capitol merger came with divestiture mandates in high-density suburbs to maintain fair access. Across all regions, consistent enforcement of TGA cybersecurity standards aligns purchasing toward OEMs that maintain in-country firmware support.

Competitive Landscape

Multinational conglomerates dominate, but local specialization shapes go-to-market strategy within the Australia digital X-ray market. Siemens Healthineers, Philips Healthcare, and GE Healthcare leverage global R&D pipelines to deliver detector and AI upgrades on synchronized release cycles, servicing hospital procurement frameworks that demand multi-modality consistency. Canon Medical and Fujifilm position on service responsiveness, using distributor networks such as Allrad Imaging to guarantee spare-part arrival within 48 hours in any state capital.

Competitive intensity increasingly centers on software. Pro Medicus’ Visage platform, embedded inside several GE and Siemens consoles, offers native support for lung-nodule CAD and bone-age analysis. OEMs unable to supply equivalent AI toolsets risk commoditization pressure. Local hardware innovator Micro-X entered strategic supply agreements with U.S. defense agencies for portable trauma scanners, validating export potential for technology born in Adelaide.

Private equity inflows accelerate consolidation among imaging providers themselves, indirectly shaping hardware choices. Affinity Equity Partners acquired Lumus Imaging for USD 657 million, granting the chain negotiating clout to demand fleet-wide pricing, cybersecurity audits, and standardized detector footprints that lower training complexity. As interoperability testing and penetration-test certificates become default RFP line items, smaller foreign entrants find barriers to market entry creeping upward.

Australia Digital X-Ray Industry Leaders

Carestream Health

GE Healthcare

Siemens Healthineers AG

Fujifilm Holdings Corporation

Koninklijke Philips NV

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: CSIRO scientists unveiled a technique that trains AI models to write highly accurate chest X-ray reports by exposing algorithms to the same clinical metadata physicians use.

- June 2024: SK Telecom launched X Caliber, an AI-powered veterinary X-ray analysis platform, into Australia’s animal health sector.

Australia Digital X-Ray Market Report Scope

As per the scope of this report, digital X-ray or digital radiography is a form of X-ray imaging where digital X-ray sensors are used instead of traditional photographic films. This has the added advantage of time efficiency and the ability to transfer images digitally and enhance them for better visibility. This method bypasses the chemical processing of photographic films. Digital X-ray imaging has high demand, as it requires less radiation exposure compared to traditional X-rays. Australia Digital X-Ray Market is Segmented by Application (Orthopedic, Cancer, Dental, Cardiovascular, and Other Applications), Technology (Computed Radiography and Direct Radiography), Portability (Fixed Systems and Portable Systems), and End User (Hospitals, Diagnostic Centers, and Other End Users). The report offers the value (in USD million) for the above segments.

By Portability

| Fixed Systems |

| Mobile DR Systems |

| Hand-held Systems |

By Detector Panel Type

| Amorphous Silicon |

| CMOS |

| IGZO / Flexible Panels |

By Application

| Orthopedic |

| Chest Imaging |

| Cardiovascular |

| Dental |

| Other Applications |

By End User

| Hospitals & Multispecialty Clinics |

| Diagnostic Imaging Centers |

| Mobile Screening Units |

| Other End Users |

| By Portability | Fixed Systems |

| Mobile DR Systems | |

| Hand-held Systems | |

| By Detector Panel Type | Amorphous Silicon |

| CMOS | |

| IGZO / Flexible Panels | |

| By Application | Orthopedic |

| Chest Imaging | |

| Cardiovascular | |

| Dental | |

| Other Applications | |

| By End User | Hospitals & Multispecialty Clinics |

| Diagnostic Imaging Centers | |

| Mobile Screening Units | |

| Other End Users |

Key Questions Answered in the Report

How large is the Australia digital X-ray market in 2026?

It stands at USD 61.01 million, with a projected 7.18% CAGR to 2031.

Which segment is growing fastest within Australian radiography?

Mobile digital X-ray systems, advancing at a 10.05% CAGR on rising point-of-care demand.

Why are flexible detector panels gaining traction?

Their lighter weight and higher durability suit mobile units, pushing a 10.4% CAGR to 2031.

How does My Health Record influence equipment purchases?

Mandatory image uploads compel providers to replace analog gear with compliant digital consoles.

What impact do radiographer shortages have?

Staffing gaps encourage AI-enabled consoles that automate routine tasks and reduce scan times.

Who are the leading suppliers in Australia?

Siemens Healthineers, Philips Healthcare, GE Healthcare, Carestream Health, and Fujifilm together supply over 60% of shipped systems.

Page last updated on: