Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

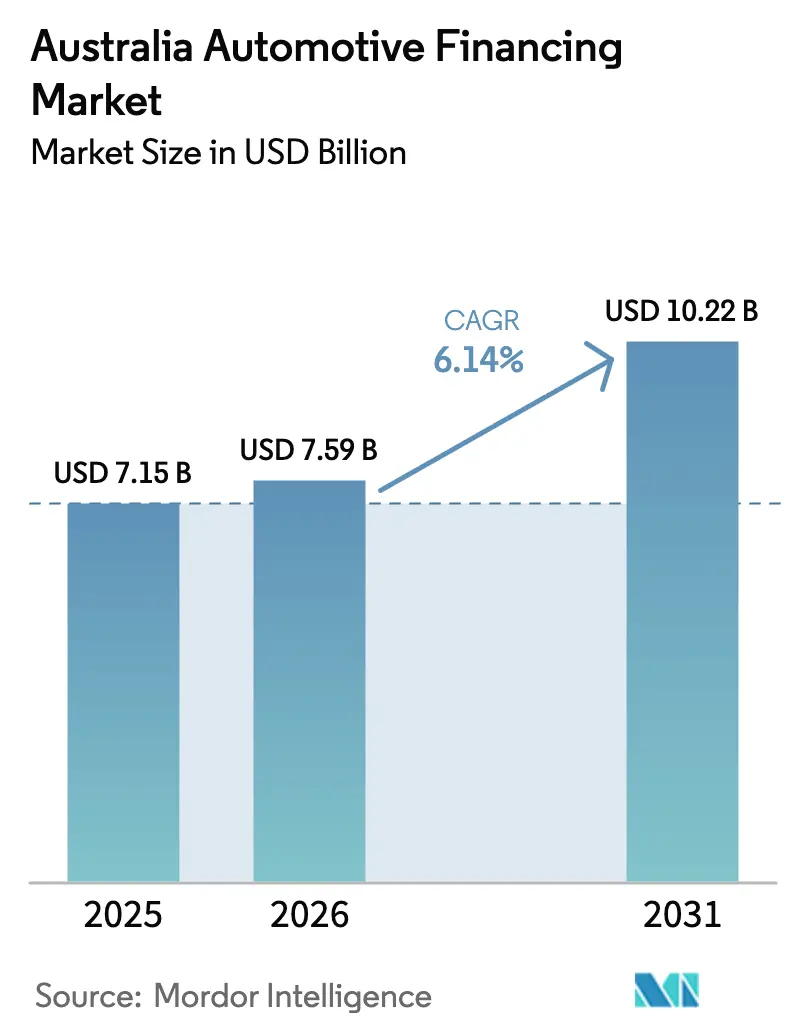

| Base Year Market Size (2025) | USD 7.15 Billion |

| Market Size (2026) | USD 7.59 Billion |

| Market Size (2031) | USD 10.22 Billion |

| Growth Rate (2026 - 2031) | 6.14% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Automotive Financing Market Analysis by Mordor Intelligence

The Australia automotive financing market size is expected to grow from USD 7.15 billion in 2025 to USD 7.59 billion in 2026 and is forecast to reach USD 10.22 billion by 2031 at 6.14% CAGR over 2026-2031. Growth persists despite the Reserve Bank of Australia’s 4.35% cash rate, underpinned by rising electric-vehicle penetration, digital-first lending, and new products such as guaranteed future value loans [1]“Statement on Monetary Policy,” Reserve Bank of Australia, rba.gov.au. Structural shifts include OEM captives scaling embedded finance, fintech-bank partnerships widening credit access, and subscription models meeting demand for flexible mobility. Competitive intensity is rising as banks defend share against OEM captives and specialized non-banks through AI-enabled underwriting and omnichannel origination. Geographic divergence is evident: New South Wales remains volume leader, yet Western Australia posts the fastest gains on mining-driven prosperity. Regulation remains a pivotal force, with ASIC’s ban on flex commissions compressing dealer spreads and open-banking mandates adding compliance costs.

Key Report Takeaways

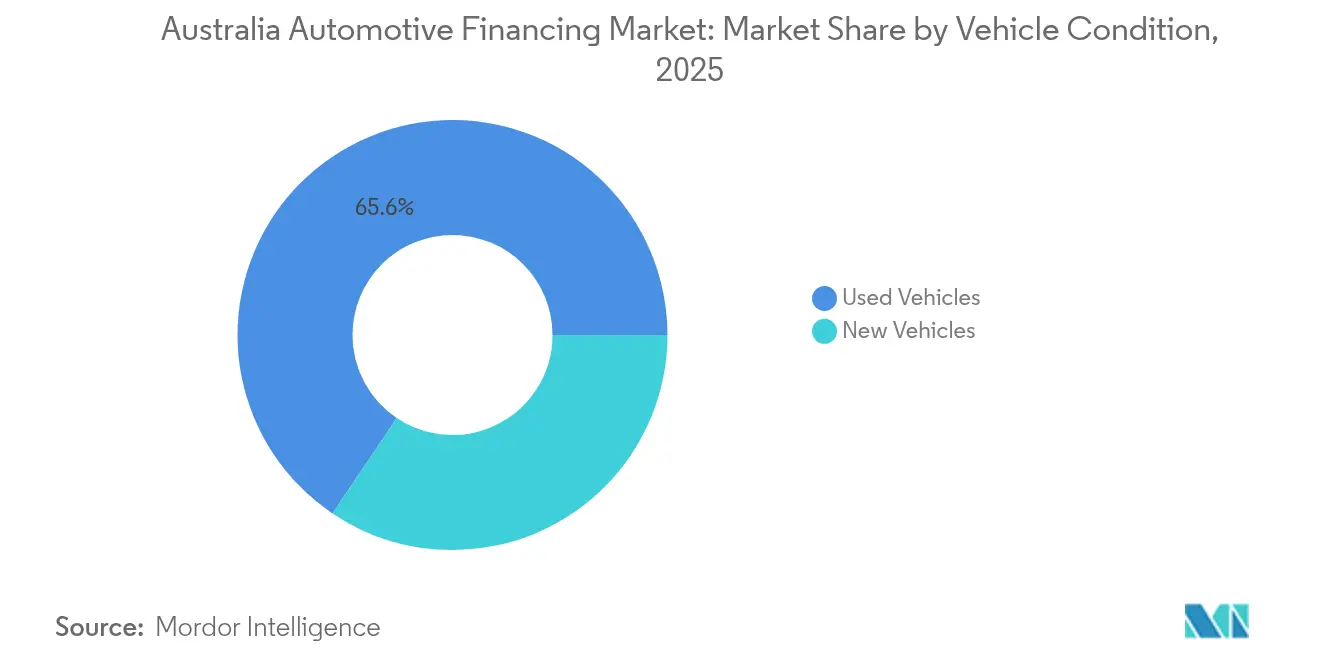

- By vehicle condition, used cars held 65.58% of the Australia automotive financing market share in 2025, whereas new-car loans are projected to advance at a 6.98% CAGR to 2031.

- By financing source, banks led with 53.78% share of the Australia automotive financing market size in 2025, while OEM captive lenders are set to grow fastest at 7.86% CAGR through 2031.

- By financing product, secured auto loans held 48.76% of the Australia automotive financing market share in 2025, whereas subscription and pay-per-use is projected to advance at a 7.28% CAGR to 2031.

- By vehicle type, passenger cars accounted for a 72.63% of the Australia automotive financing market share in 2025 and will grow with a 6.71% CAGR by 2031.

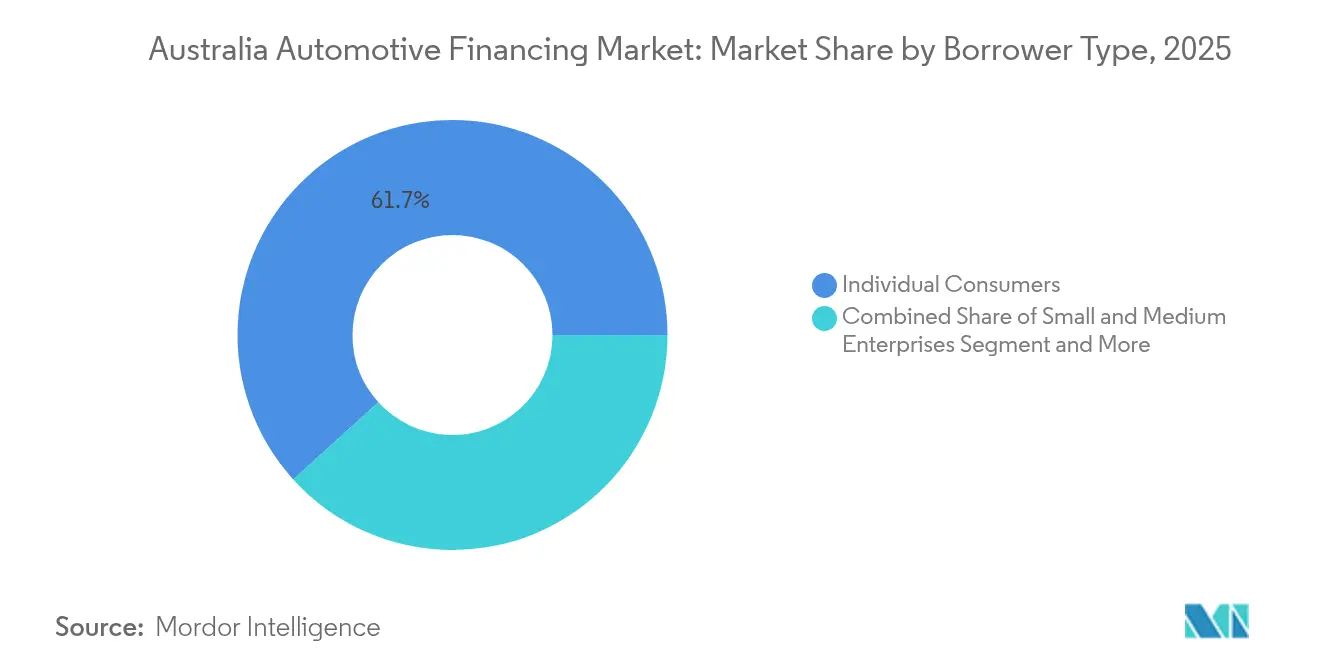

- By borrower type, individual consumers held 61.72% of the Australia automotive financing market in 2025, while small and medium enterprises are expected to grow with an 8.09% CAGR through 2031.

- By channel, dealer-integrated finance captured 56.71% of the Australia automotive financing market in 2025, while direct-to-consumer online model is expected to grow with an 8.52% CAGR through 2031.

- By state/territory, New South Wales captured 34.12% of the Australia automotive financing market in 2025; Western Australia shows the highest projected CAGR at 7.78% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Automotive Financing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV and Hybrid Adoption | +1.8% | National, concentrated in ACT, NSW and Victoria | Medium term (2-4 years) |

| Accelerating Digital Loan Origination | +1.2% | National, early adoption in NSW and Victoria | Short term (≤ 2 years) |

| Dealer-led GFV Programs | +1.1% | National, metro uptake | Short term (≤ 2 years) |

| Fintech–Bank Partnerships for Borrowers | +0.9% | National, regional focus | Medium term (2-4 years) |

| Incentives for Subscription and Lease | +0.7% | Urban high-income centers | Long term (≥ 4 years) |

| Residual-Value Insurance and Higher LTVs | +0.5% | Major cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Soaring BEV and Hybrid Adoption Supported by EV-specific Loan Products

Battery-electric and hybrid uptake is accelerating loan demand thanks to government rebates, Fringe Benefits Tax exemptions on novated leases, and low-rate green loans from Bank Australia and RACV. July 2025 BEV deliveries rose 7.1% year on year, providing lenders with a segment growing. OEM captives bundle charging credits and insurance, boosting uptake in ACT, New South Wales, and Victoria. As the New Vehicle Efficiency Standard begins in 2025, manufacturers face fleet CO₂ caps that will steer borrowers toward electrified models.

Digital-first Loan Origination and e-KYC Acceleration

Digital-first loan origination and e-KYC compress approval times from days to minutes, resetting consumer expectations nationwide. Pepper Money’s instant offers and Ausloans’ two-minute Zink approvals show how real-time bank feeds, AI credit scoring, and open-banking APIs replace paper statements and manual verifications. Dealers gain higher conversion rates and reduced fall-out, while online portals can fund customers within a browsing session. The efficiency savings lower acquisition cost, widen credit access for regional borrowers, and lift loan volumes despite higher interest rates.

Dealer-led Guaranteed Future Value (GFV) Programs Boosting Affordability

Guaranteed Future Value programs transfer residual-value risk from drivers to lenders, lowering monthly payments and unlocking new-car affordability. The structure generated a significant loan surge as OEM captives, backed by detailed resale data, promote fixed buy-back prices at term-end. Australian Taxation Office minimum residual tables add regulatory clarity, while insurers package coverage that protects lenders against market swings. Uptake is strongest in metro areas where predictable depreciation and high secondary-market liquidity reduce risk premiums for financiers.

Fintech-bank Partnerships Expanding Credit Access to Thin-file Borrowers

Fintech–bank alliances widen credit access for thin-file borrowers by combining real-time bank feeds with alternative data scoring. Plenti’s integration with NAB PayTo enables instant repayments, while Westpac and Rich Data Co deploy AI cash-flow predictions to refine serviceability tests. Marketplace lenders such as SocietyOne still approve only about 11% of applicants, yet their models push incumbents toward inclusive analytics. ASIC’s focus on Indigenous and regional consumers supports this shift, and forthcoming BNPL licensing embeds responsible-lending rules across emerging channels.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interest Rate and Debt Pressure | -1.4% | National; acute in NSW and Victoria | Short term (≤ 2 years) |

| ASIC Cracks Down on Commissions | -0.8% | National | Medium term (2-4 years) |

| Rapid BEV Depreciation Risk | -0.6% | Early-adoption states | Long term (≥ 4 years) |

| Open-Banking Compliance Costs | -0.3% | National; small lenders | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Interest-rate Volatility and Household Debt-servicing Pressure

Since May 2022, the Reserve Bank of Australia has lifted the cash rate from 0.10% to 4.35%, pushing the average variable mortgage rate above 6.0% and the average fixed three-year car-loan rate to 8.1%. Treasury modelling indicates that every 100-basis-point rise in mortgage rates cuts household consumption growth by 0.35 percentage points, curbing discretionary outlays such as vehicle upgrades. Economists see a significant recession probability, heightening employment uncertainty and prompting lenders to tighten scorecards and shorten loan terms.

ASIC Clamp-down on Dealer “Flex-commissions” Lowering Margins

The 2018 ban removed mark-ups that once inflated rates, culminating in an AUD 85 million ANZ settlement [2]“Flex-Commission Ban Impact,” ASIC Media Release, asic.gov.au. The practice’s removal compresses dealer margins, lowering incentives to upsell finance and shifting negotiation power to well-informed borrowers. Some dealers respond by raising vehicle prices or pushing add-on insurance to recover lost profit, but these steps risk greater regulatory scrutiny. Banks and captives must redesign compensation models to keep showroom finance attractive.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Condition: Used-car scale meets new-car EV momentum

Used cars dominated the Australia automotive financing market with a 65.58% share in 2025 as average loan amounts of AUD 28,116 undercut new-car equivalents. Online classifieds integrating escrow payments enhance trust in pre-owned transactions. New-car loans grow at 6.98% CAGR, propelled by EV subsidies and GFV programs lowering monthly outlays. 2024 achieved record sales, which reinforces lender appetite for prime-credit new-car customers.

Digital-first underwriting benefits both segments, yet risk models differ. Used loans face wider condition variance, driving higher provisioning. New-car portfolios gain from warranty coverage and predictable depreciation, especially for OEM-captive paper. ASIC scrutiny remains tighter on second-hand finance to guard vulnerable borrowers.

By Financing Source: Banks anchor, OEM captives climb

Banks held 53.78% of the Australia automotive financing market in 2025, leveraging deposit funding and national branch networks to maintain pricing power. Their Big Four status secures a notable share of banking assets, but OEM captives are expanding at 7.86% CAGR by bundling sub-vented rates, service packages, and GFV guarantees that streamline showroom sales. Customer-owned banks add community-focused competition in loans, growing over time.

Non-bank lenders such as Taurus Auto Finance securitize retail pools to fund AUD 550 million in originations, showing how agile underwriting captures niche cohorts. Portfolio reshuffles—Westpac’s divestiture to Resimac and Macquarie’s sale to Allied Credit—highlight capital-efficiency priorities amid tightening Basel capital buffers. Intensifying competition narrows pricing spreads but widens product choice.

By Financing Product: Secured loans prevail, subscriptions surge

Secured loans accounted for 48.76% of the Australia automotive financing market in 2025, benefiting from vehicle collateral that supports median interest rates and five-year terms. Unsecured personal loans cater to buyers of older vehicles but price in higher credit risk with double-digit rates. Tax-advantaged novated leases flourish for salaried EV buyers under Fringe Benefits Tax exemptions, while GFV structures move residual risk to lenders and fuel a volume spike.

Subscription and pay-per-use models grow 7.28% CAGR, bundling insurance, registration, and maintenance into fixed monthly fees that appeal to urban professionals seeking flexibility. Residual-value insurance enables lenders to stretch loan-to-value ratios, particularly on electric models with uncertain resale curves, without materially elevating capital provisions. Compliance frameworks demand transparent terms to mitigate consumer misunderstanding of balloon obligations .

By Vehicle Type: Passenger cars dominate, LCVs and BEVs follow

Passenger cars retained 72.63% of the Australian automotive financing market in 2025 and are projected to expand at a 6.71% CAGR through 2031 as households prioritize personal mobility and lenders favor predictable depreciation. The Toyota HiLux and Ford Ranger dominate registrations, illustrating the blurred line between passenger and utility use. Light commercial vehicles benefit from instant-asset write-offs that let SMEs depreciate, stimulating fleet renewals. Medium and heavy trucks rely on longer tenors aligned with operational life cycles, requiring specialized underwriting.

Electrification gathers pace in passenger segments, with Tesla Model Y climbing the leader board, whereas commercial EV uptake hinges on payload and range economics. New Vehicle Efficiency Standards starting in 2025 accelerate overall fleet decarbonization and add compliance cost factors to leasing models.

By Propulsion Type: ICE still heavy, BEV grows quickest

Internal-combustion vehicles commanded 74.95% of the Australian automotive financing market in 2025, supported by entrenched refueling infrastructure and lower upfront prices. Battery-electric vehicles, however, show a 8.89% CAGR outlook as charger rollouts and loan discounts narrow cost gaps.

Hybrid sales increased in 2024, providing a transitional pathway. Green loans at 6.95% (Bank Australia) and RACV’s 5.09% offers trim finance expense, while novated-lease FBT relief amplifies paycheck savings. Financing structures reward low-emission borrowers through rate cuts and novated-lease tax breaks. Residual-value uncertainty for BEVs remains a restraint; lenders increasingly price shorter terms and lower balloon residuals. Insurance wrappers offset volatility, sustaining loan appetite even as rapid tech cycles compress depreciation curves.

By Borrower Type: Consumers lead, SMEs accelerate

Individuals comprised 61.72% of the Australian automotive financing market in 2025, with credit scores slightly below the national average yet within prime bands. Household mobility requirements sustain steady demand even amid cost-of-living pressure. Australia's automotive financing market size for SMEs grows 8.09% CAGR as electrified fleets and instant asset write-offs drive uptake. Corporate fleet finance relies on volume rebates and multi-year maintenance packages, often funneled through OEM captives.

Corporate fleet financing emphasizes bulk discounts, operating-lease structures, and total-cost-of-ownership analytics, frequently managed by OEM captives with telematics-based monitoring. Fintech scoring models broaden access for thin-file applicants such as gig-economy drivers, while ASIC oversight safeguards vulnerable cohorts, including Indigenous borrowers, through responsible-lending audits and breach actions. AI-driven income verification accelerates approvals, but lenders still flag higher provisioning for unsecured SME exposures.

By Channel: Dealer finance leads, direct-to-consumer scales

Dealer-integrated finance accounted for 56.71% of the Australian automotive financing market in 2025, leveraging point-of-sale convenience and manufacturer incentives despite ASIC’s flex-commission ban, trimming margins. GFV offers and low-rate captive loans remain persuasive at showrooms, but online direct-to-consumer channels are climbing 8.52% CAGR as digital natives demand transparent pricing and instant decisions.

Brokers aggregate options across 60+ lenders, while Ausloans’ Zink approves in two minutes, illustrating UX as a competitive lever. Open-banking APIs enable real-time income checks, though cybersecurity compliance raises costs for smaller lenders. Marketplace safeguards—such as Carsales–Monoova escrow—boost trust in peer-to-peer deals. As mobile origination apps evolve, lenders blend omnichannel journeys, allowing a borrower to start online, finalize at a dealership, and service the loan via smartphone portals.

Geography Analysis

New South Wales commands 34.12% of the Australia automotive financing market, generating a significant share of loan applications and spearheading EV charging rollouts. New South Wales blends scale and policy support, hosting the largest dealership footprints and concentrated fintech clusters that streamline originations. High urban density favors BEV adoption, and state rebates complement federal incentives. Victoria leverages legacy manufacturing ecosystems and charging corridors along the Melbourne-Sydney route. Queensland benefits from population inflows and tourism, which sustain light-commercial lending.

Western Australia records the fastest CAGR at 7.78%, fueled by mining wealth and infrastructure upgrades. Western Australia’s commodity-backed prosperity buffers cyclical downturns and lifts disposable incomes, with Pilbara infrastructure projects necessitating high-value utility vehicles. South Australia, Tasmania, and the ACT are smaller in volume yet punch above their weight in EV adoption and novated-lease penetration. Northern Territory’s sparse population skews toward larger 4×4 loans, while Tasmania’s lower average loan size signals heightened price sensitivity.

Cross-state regulatory harmony under ASIC ensures uniform consumer safeguards, though varying stamp-duty concessions and registration discounts add complexity to loan pricing. Charging-infrastructure rollout, especially in highway corridors, remains a determinant of BEV loan growth trajectories.

Competitive Landscape

The Australia automotive financing market exhibits moderate concentration. Banks guard incumbency with funding cost advantages and brand trust, yet OEM captives exploit bundled offerings and superior residual-value insights. Non-bank lenders and fintechs differentiate through speed and user experience; Pepper Money’s instant approvals and Taurus Auto Finance’s securitized funding spotlight these advantages.

Regulatory shifts spur strategic recalibration. Westpac exited direct auto lending via a AUD 1.5 billion book sale to Resimac in March 2025, redeploying capital toward core segments. Macquarie’s offload of vehicle loans to Allied Credit in July 2025 underscores an asset-light trend among banks. Technology remains the defining competitive weapon: AI and open-banking data streams lower default rates and unlock underserved niches, while cybersecurity spend rises to protect real-time APIs.

Emergent models include subscription finance and GFV residual insurance, offering annuity-style revenue that offsets margin compression from rate competition. Partnerships—such as NAB’s PayTo integration with Plenti—demonstrate symbiotic bank-fintech plays that expand market coverage without bloating balance sheets.

Australia Automotive Financing Industry Leaders

Toyota Finance Australia

ANZ Banking Group

National Australia Bank (NAB)

Macquarie Leasing & Asset Finance

Commonwealth Bank (CommBank)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Macquarie’s Banking and Financial Services unit agreed to transfer a USD 1.0 billion (AUD 1.5 billion) auto-loan portfolio to Allied Credit, realigning capital toward advisory services.

- March 2025: Resimac Group finalized the purchase of Westpac’s auto-finance assets, raising AUM to AUD 15.7 billion and cementing its non-bank scale.

- March 2025: Bank Australia announced it will cease funding new fossil-fuel vehicles from 2025 to accelerate the national EV transition.

Australia Automotive Financing Market Report Scope

Automotive financing is the service that offers new vehicles to consumers at much-lowered prices at affordable EMI installments. These installments are divided based on the loan amount, and tenure with some fixed rate of interest.

The Automotive financing market is segmented on the basis of type, source type, and vehicle type. On the basis of type, the market has been segmented into new vehicles and used vehicles. On the basis of source type, the market has been segmented into OEMs, banks, credit unions, and financial institutions, and on the basis of vehicle type, the market has been segmented into passenger cars and commercial vehicles. The report covers the market size in value (USD billion) for all the above-mentioned segments

By Vehicle Condition

| New Vehicles |

| Used Vehicles |

By Financing Source

| Banks |

| OEM Captive Finance |

| Credit Unions and Mutuals |

| Non-bank Lenders and Fintechs |

By Financing Product

| Secured Auto Loans |

| Unsecured Personal Loans |

| Lease and Novated Lease |

| GFV / Balloon-Payment Finance |

| Subscription and Pay-per-use |

By Vehicle Type

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

By Propulsion Type

| Internal-Combustion Engine (ICE) |

| Hybrid Electric Vehicle (HEV) |

| Battery Electric Vehicle (BEV) |

By Borrower Type

| Individual Consumers |

| Small and Medium Enterprises |

| Corporate and Fleet |

By Channel

| Dealer-integrated Finance |

| Direct-to-Consumer Online |

| Broker and Aggregator Platforms |

By State / Territory

| New South Wales |

| Victoria |

| Queensland |

| Western Australia |

| South Australia |

| Tasmania |

| Australian Capital Territory |

| Northern Territory |

| By Vehicle Condition | New Vehicles |

| Used Vehicles | |

| By Financing Source | Banks |

| OEM Captive Finance | |

| Credit Unions and Mutuals | |

| Non-bank Lenders and Fintechs | |

| By Financing Product | Secured Auto Loans |

| Unsecured Personal Loans | |

| Lease and Novated Lease | |

| GFV / Balloon-Payment Finance | |

| Subscription and Pay-per-use | |

| By Vehicle Type | Passenger Cars |

| Light Commercial Vehicles | |

| Medium and Heavy Commercial Vehicles | |

| By Propulsion Type | Internal-Combustion Engine (ICE) |

| Hybrid Electric Vehicle (HEV) | |

| Battery Electric Vehicle (BEV) | |

| By Borrower Type | Individual Consumers |

| Small and Medium Enterprises | |

| Corporate and Fleet | |

| By Channel | Dealer-integrated Finance |

| Direct-to-Consumer Online | |

| Broker and Aggregator Platforms | |

| By State / Territory | New South Wales |

| Victoria | |

| Queensland | |

| Western Australia | |

| South Australia | |

| Tasmania | |

| Australian Capital Territory | |

| Northern Territory |

Key Questions Answered in the Report

What is the projected size of the Australia automotive financing market by 2031?

The Australia automotive financing market size is forecast to reach USD 10.22 billion by 2031, supported by a 6.14% CAGR.

Which vehicle condition segment currently leads loan volumes?

Used-car financing commands 65.58% of total volume, driven by affordability advantages over new-car purchases.

Why are OEM captive finance companies growing faster than banks?

OEM captives bundle low-rate loans with vehicles and leverage superior residual-value data, enabling an 7.86% CAGR through 2031.

Which Australian state is expected to post the fastest financing growth?

Western Australia is projected to expand at 7.78% CAGR, buoyed by mining-driven income growth and vehicle replacement demand.

Page last updated on: