Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

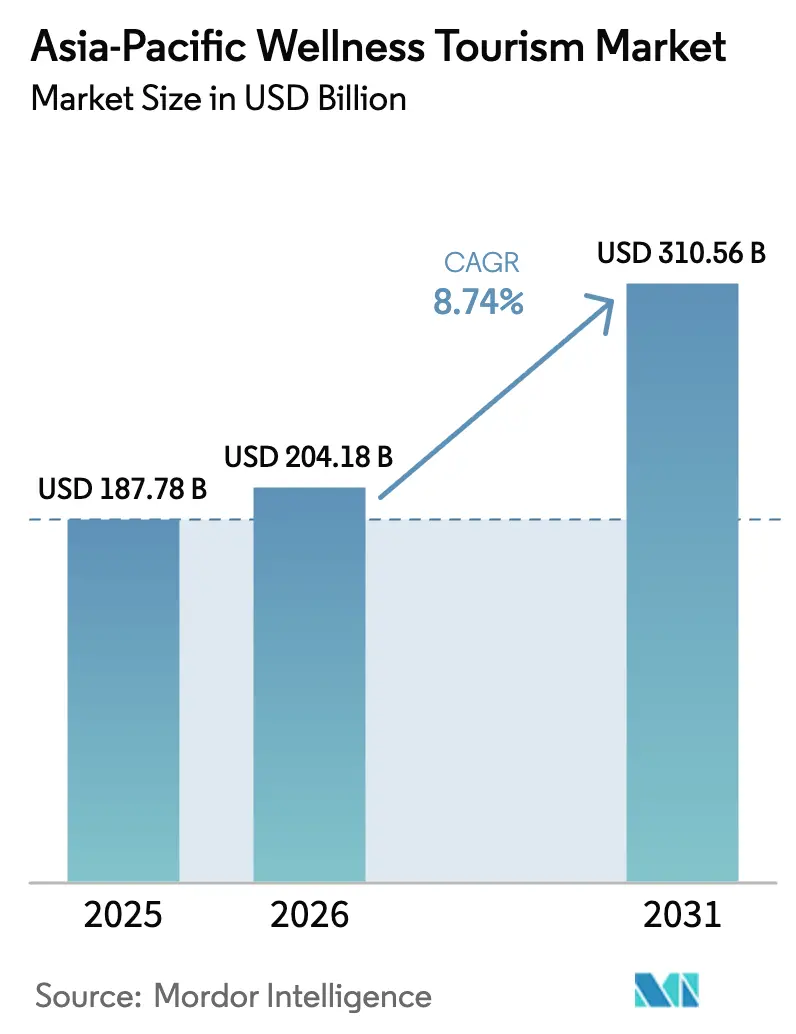

| Base Year Market Size (2025) | USD 187.78 Billion |

| Market Size (2026) | USD 204.18 Billion |

| Market Size (2031) | USD 310.56 Billion |

| Growth Rate (2026 - 2031) | 8.74% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Wellness Tourism Market Analysis by Mordor Intelligence

The Asia-Pacific wellness tourism market size was valued at USD 187.78 billion in 2025 and estimated to grow from USD 204.18 billion in 2026 to reach USD 310.56 billion by 2031, at a CAGR of 8.74% during the forecast period (2026-2031). Government-backed integration of traditional medicine, surging disposable incomes among the region’s expanding middle class, and sustained post-pandemic prioritization of preventive health continue to energize demand for authentic wellness experiences that combine cultural heritage with measurable outcomes[1]Global Wellness Institute, “Global Wellness Economy Monitor 2024,” globalwellnessinstitute.org. . China currently underpins regional performance through a 37.28% Asia-Pacific wellness tourism market share in 2024, yet India’s 11.82% forecast CAGR points to a more geographically balanced growth trajectory during the outlook period. Secondary wellness travel, where wellness activities augment a broader holiday, remains the dominant user behavior, but primary wellness travel is registering stronger expansion as travelers allocate entire trips to transformative health retreats, thereby lifting yields for operators focused on curated long-stay programs. Supply-side fragmentation keeps competitive intensity low; the top five brands command just 25.9% of regional revenue, leaving substantial white-space for specialized retreat developers, eco-lodge owners, and purpose-built medi-wellness facilities that can scale quality capacity faster than incumbents encumbered by standardized hotel operating models.

Key Report Takeaways

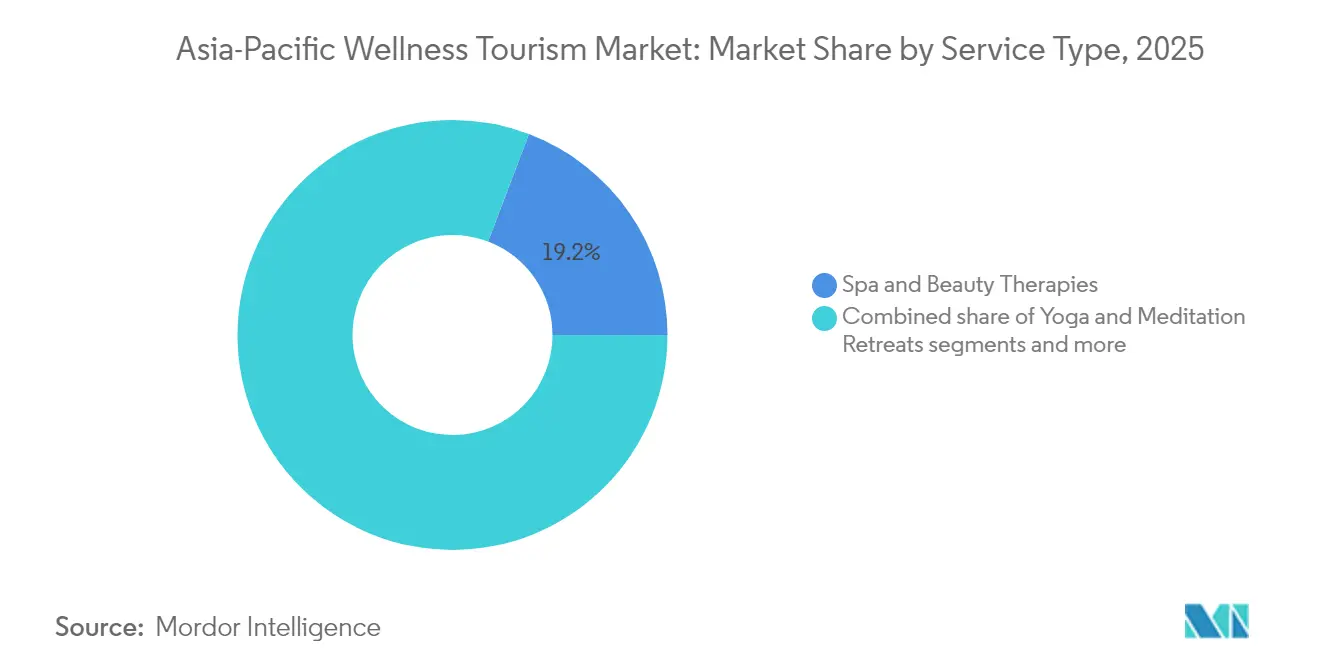

- By service type, spa and beauty therapies led with 19.21% of the Asia-Pacific wellness tourism market share in 2025, while digital-detox escapes are projected to grow at a 11.64% CAGR through 2031.

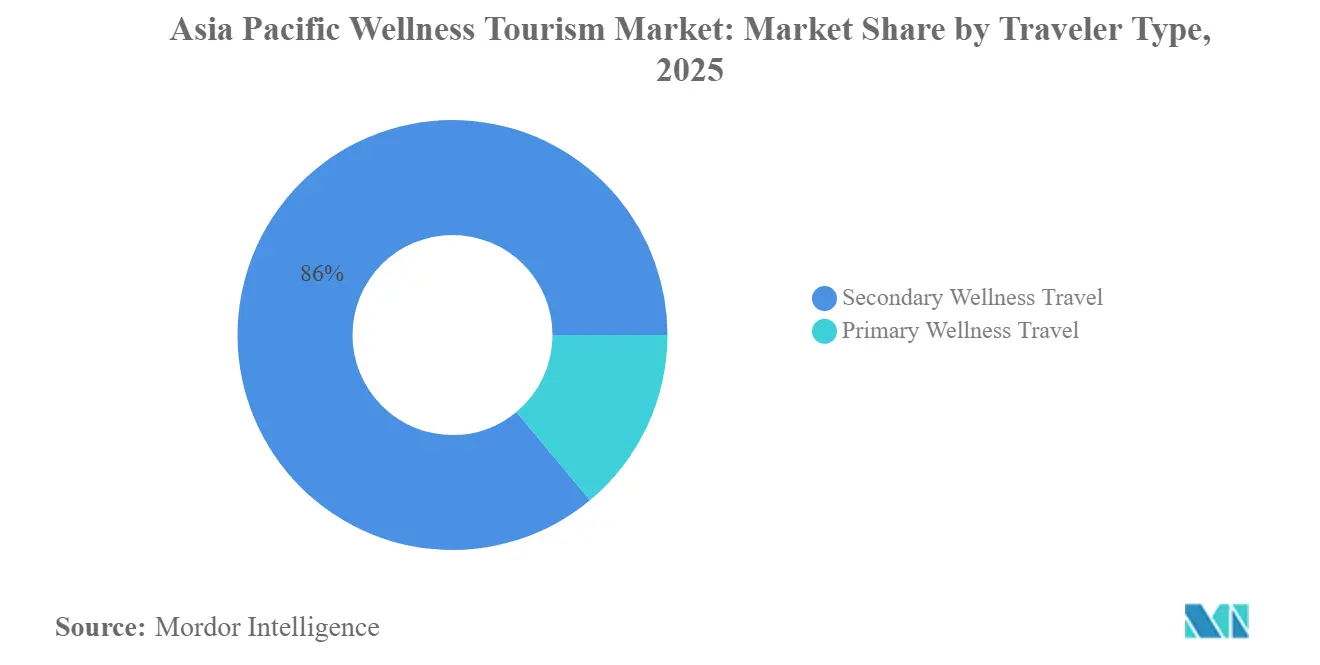

- By traveler type, secondary wellness travel accounted for 86.04% of the Asia-Pacific wellness tourism market size in 2025; primary wellness travel holds the highest projected CAGR at 9.83% for 2026-2031.

- By accommodation type, wellness hotels captured 31.17% of the Asia-Pacific wellness tourism market size in 2025, whereas eco-wellness lodges are forecast to advance at a 12.58% CAGR to 2031.

- By geography, China dominated with a 36.78% Asia-Pacific wellness tourism market share in 2025, while India is positioned as the fastest-growing market at 11.14% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Wellness Tourism Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising middle-class disposable income & intra-regional air-connectivity boom | +2.1% | China, India, Southeast Asia core markets | Medium term (2-4 years) |

| Post-pandemic health consciousness accelerating preventive-care travel | +1.8% | Global, with highest impact in APAC urban centers | Short term (≤ 2 years) |

| Government promotion of AYUSH, TCM & J-Wellness creating demand pull | +1.5% | India, China, Japan with spillover to regional markets | Long term (≥ 4 years) |

| Digital nomad & "work-from-anywhere" visas extending length-of-stay | +0.9% | Thailand, Philippines, Singapore, Malaysia | Medium term (2-4 years) |

| Corporate off-site mental-wellness retreats tackling employee burnout | +0.7% | Urban APAC centers, particularly Japan, South Korea, Singapore | Short term (≤ 2 years) |

| Buy-Now-Pay-Later travel financing unlocking premium retreat affordability | +0.4% | Millennial-heavy markets across APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Middle-Class Disposable Income & Improved Air Links

Surging real wages and favorable demographic profiles have expanded the pool of travelers able to afford dedicated wellness breaks, especially throughout China, India, Indonesia, and Vietnam, where domestic air connectivity has multiplied over the past five years. Low-cost carriers have launched new point-to-point routes that reduce door-to-door travel time and lower fares, enabling weekend wellness escapes that were formerly limited to higher-income groups. Accelerated infrastructure development at secondary airports in Malaysia, Thailand, and the Philippines also lifts access for rural wellness assets, amplifying regional dispersion of visitor flows. Short-haul affordability widens the funnel for first-time wellness travelers, seeding long-term market expansion as repeat visitation boosts average spending on advanced treatments. Destinations able to combine quick flight access with authentic healing modalities consequently achieve stickier demand and favorable RevPAR trends across wellness-centric accommodation. Government incentives that subsidize regional route launches further reinforce the virtuous cycle, suggesting the growth dividend will extend through the medium term.

Post-Pandemic Health Consciousness

The COVID-19 crisis recast health preservation as a lifestyle imperative, vaulting immunity-building, stress reduction, and disease prevention to the heart of travel decision-making. Corporate wellness budgets have swelled as employers seek stress-relief programming to mitigate burnout among remote and hybrid workforces, catalyzing demand for evidence-based retreats that combine diagnostics with coaching. Parallel consumer surveys indicate that affluent Asian millennials value wellness as an “essential” rather than a discretionary purchase, shifting spend from retail to experiential services. Hotels and resorts that swiftly integrated on-site testing, pharmacist consultations, and immunity-focused menus during the reopening phase remain top-of-mind for repeat guests who now expect clinical rigor baked into every itinerary. Marketing narratives grounded in health outcomes rather than pampering experiences resonate widely, creating premium pricing headroom that sustains revenue growth even as traveler cost sensitivity rises elsewhere. The shift appears durable given persistent anxiety over future health shocks, entrenching wellness as a structural, not cyclical, travel driver.

Government Promotion of AYUSH, TCM & J-Wellness

India’s AYUSH visa, launched in 2024, streamlines six- and twelve-month stays for seekers of Ayurveda, yoga, Unani, Siddha, and homeopathy, signaling formal state endorsement of alternative therapies within the inbound tourism strategy. China’s Belt and Road-linked “Health Silk Road” exports Traditional Chinese Medicine clinics across 196 partner countries, elevating global familiarity with TCM and driving inbound flows from patients keen to experience origin-based treatments. Japan positions “J-Wellness” as a core pillar of its Tourism Nation Promotion Basic Plan, integrating forest bathing, onsen therapy, and longevity cuisine into regional destination marketing[2]Ministry of Land, Infrastructure, Transport and Tourism, “Tourism Nation Promotion Basic Plan,” mlit.go.jp.. These policies confer legitimacy on indigenous healing systems, unlock public funding for practitioner training, and subsidize infrastructure that meets modern accreditation standards. Visa facilitation reduces friction for international patients, while bilateral agreements on practitioner licensing spur cross-border referral networks, converting government soft power into measurable visitor arrivals. Over the long term, the alignment between public-sector endorsement and private-sector innovation is expected to elevate service quality, supporting price optimization and margin expansion for certified operators.

Digital-Nomad and Work-From-Anywhere Visas

Thailand, Malaysia, the Philippines, and Indonesia now extend one- to five-year digital-nomad visas that encourage location-independent professionals to combine daily work routines with ongoing wellness regimens. Extended stay permits lengthen the average length of stay well beyond the historical seven-night wellness package, inflating per-visitor revenue across accommodation, treatments, and ancillary spending. Wellness facilities respond by adding co-working zones, high-speed broadband, and flexible scheduling that accommodates mid-day virtual meetings followed by evening detox rituals. Destinations with competitive cost of living and robust digital infrastructure emerge as hubs for “slow wellness,” where guests pursue incremental lifestyle change over multi-month residencies. This paradigm unlocks stable occupancy for low-season months, smoothing revenue volatility and supporting local labor retention. As more APAC governments chase affluent mobile talent, a race to refine nomad-friendly wellness ecosystems may ensue, benefiting early movers with ecosystem depth and brand recognition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price sensitivity among Gen-Z & budget travelers | -1.2% | Indonesia, Vietnam, Philippines | Short term (≤ 2 years) |

| Shortage of licensed therapists & wellness practitioners | -0.8% | Thailand, Indonesia, Malaysia | Medium term (2-4 years) |

| Fragmented accreditation & quality-control frameworks | -0.9% | India, Vietnam, Philippines, and emerging wellness destinations | Medium term (2–4 years) |

| Rising insurance exclusions for non-prescribed wellness services | -0.7% | Developed APAC markets such as Japan, South Korea, and Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Price Sensitivity Among Gen-Z & Budget Travelers

Younger travelers across emerging Southeast Asian economies crave authentic wellness immersion yet remain constrained by modest discretionary income levels and rising inflation. Social media amplifies aspirational demand, but the luxury positioning of many destination spas places packages out of reach, prompting a proliferation of budget operators that often compromise on therapist quality, safety protocols, and hygiene. Price-focused competition can erode brand equity for incumbents if discounting leads to service dilution, while aggressive cost control measures may limit artisan sourcing, thereby diminishing authenticity. Operators that calibrate tiered product lines offering accessibly priced day passes alongside premium multi-day transformations better capture Gen-Z volumes without cannibalizing upscale segments. Innovative financing models such as buy-now-pay-later partnerships can further democratize access, though margin impacts must be weighed against acquisition gains. Over the short term, price friction is likely to restrain growth in lower-income source markets until rising wages or more efficient operating models narrow the affordability gap.

Shortage of Licensed Therapists & Wellness Practitioners

Thailand projects a deficit of 70,000 professional masseurs and therapists over the next four years, with similar gaps emerging in Indonesia and Malaysia as demand accelerates faster than accredited training programs can expand[3]Nation Thailand, “More Massage Therapists to be Trained,” nationthailand.com. . Bottlenecks in practitioner availability constrain capacity, forcing operators to limit occupancy, extend booking windows, or hire under-qualified staff, risking inconsistent service outcomes that deter repeat visitation. Governments have responded with scholarship programs and accelerated certification pathways, yet quality assurance remains a hurdle where training durations shrink. Specialized modalities such as Panchakarma or TCM acupuncture require multi-year apprenticeships, creating lag times before new supply materializes. Wage inflation intensifies as operators bid for scarce talent, squeezing margins for mid-scale resorts and slimming the viability of community-owned wellness start-ups. Over the medium term, partnerships between public vocational institutes and private retreat chains may ease the crunch, but progress will hinge on harmonizing cross-border licensing to enable mobile practitioner pools.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Digital-Detox Escapes Reshape Premium Demand

Digital-detox escapes post a 11.64% CAGR through 2031, eclipsing growth across traditional spa categories even as spa and beauty therapies account for the largest 19.21% revenue slice of the Asia-Pacific wellness tourism market size in 2025. Retreat designers capitalize on employer anxiety over smartphone addiction by mandating tech-free zones, curating nature immersion itineraries, and offering cognitive coaching that restores focus and sleep patterns. Bundling mindfulness workshops with structured silence periods elevates perceived transformation value, helping properties command rates 20%-30% above conventional spa packages while reducing variable cost exposure to imported beauty products. For established resorts, layering digital-detox programs onto existing infrastructure generates incremental yield without extensive capex, encouraging chain-wide rollout despite heterogenous property footprints. Meanwhile, outcome-based modalities such as naturopathy cleanses and longevity monitoring attract health-optimized millennials who value measurable biomarkers over indulgent pampering. Authentic traditional medicine centers in Kerala, Bali, and Chiang Mai integrate centuries-old herbal therapies with clinical diagnostics, drawing repeat guests who track health progression across sequential visits and advocate through social networks, reinforcing organic demand flywheels.

By Traveler Type: Primary Wellness Travel Gains Momentum

Secondary wellness trips and vacations, where wellness services act as add-ons, delivered 86.04% of Asia-Pacific wellness tourism revenue in 2025, yet dedicated primary wellness journeys are accelerating at a 9.83% CAGR to 2031, gradually altering the revenue mix toward higher-spend visitor cohorts. The pivot correlates with rising investor interest in purpose-built medical-wellness facilities that blend diagnostics, IV therapy, and evidence-based nutrition into multi-day protocols tailored to chronic stress, weight management, and hormone balance. Demand elasticity appears favorable; guests enrolling in 7- to 21-day transformative programs spend up to 4.5 times the average secondary wellness ticket, offsetting lower visitor counts during shoulder seasons and reducing marketing cost per booked night. Market education via social media testimonials and third-party physician endorsements accelerates conversion, alleviating initial skepticism among first-time participants wary of medicalized hospitality.

As primary wellness matures, successful operators will differentiate through outcome transparency, publishing aggregated anonymized data on blood markers, sleep quality, and mental health to validate efficacy. Integration with telehealth platforms broadens post-departure support, nurturing brand loyalty that manifests in recurring on-property visits and remote subscription revenue. The shift elevates the strategic importance of therapist-to-guest ratios, cross-disciplinary practitioner teams, and R&D budgets for protocol innovation, reallocating capital away from non-differentiated spa refurbishments toward clinical-grade infrastructure capable of supporting precision wellness.

By Accommodation Type: Eco-Wellness Lodges Lead Sustainability Pivot

Wellness hotels captured 31.17% of the Asia-Pacific wellness tourism market size in 2025, yet eco-wellness lodges command the fastest 12.58% CAGR through 2031 as travelers equate ecological stewardship with holistic well-being. Biophilic architecture that maximizes daylight, airflow, and natural material palettes enhances circadian alignment, elevating sleep scores and guest satisfaction. Operators adopt regenerative agriculture to supply hyper-local cuisine, linking gut-health programming to terroir narratives that enrich cultural authenticity. Off-grid power systems and closed-loop water cycles reduce operating costs over time, counterbalancing upfront capex and resonating with guests willing to pay premiums for carbon-neutral stays. Boutique retreats leverage small footprints to embed within sensitive ecosystems, mangrove forests, tea plantations, and highland rainforests, where immersive nature exposure amplifies therapeutic outcomes.

The surge in eco-wellness uptake also spawns hybrid models combining medical diagnostics with wilderness immersion; for example, luxury tents outfitted with portable cryotherapy chambers or ECG-enabled sleep pods. Certification frameworks such as EarthCheck or WELL Building Standard differentiate early adopters, granting marketing leverage and facilitating inclusion in curated wellness platforms favored by high-net-worth travelers. Over time, mass adoption of eco-centric design may render conventional urban spa hotels less competitive unless they retrofit rooftop gardens, vertical forests, and improved air-filtration technologies that replicate nature’s benefits in dense settings.

Geography Analysis

China retains primacy within the Asia-Pacific wellness tourism market through a 36.78% revenue share in 2025, buoyed by robust domestic demand and state patronage of Traditional Chinese Medicine integration across public healthcare. Rapid expansion of high-speed rail and diversified tourism zones broadens inland access, yet linguistic and regulatory complexities temper inbound penetration among non-Mandarin speakers. Bilateral treatment pathways that bundle medical checkups in Tier-1 cities with recuperative stays in Hainan’s duty-free enclave aim to rectify dispersion challenges and elongate visitor spend cycles. Outbound Chinese travelers, still rebounding from pandemic-related mobility constraints, are progressively opting for short-haul wellness sojourns to Thailand and Indonesia, transferring service expectations back to domestic providers and catalyzing upgrades in facility aesthetics and program rigor.

India’s 11.14% CAGR outperformance stems from synchronized policy actions, including the AYUSH visa and the National Medical and Wellness Tourism Board, that streamline governance across ministries, standardize accreditation, and amplify brand visibility on global stages. Kerala leverages a 5,000-year Ayurvedic heritage, tropical climate, and English-speaking therapist pool to position itself as the “Eastern Riviera of Rejuvenation,” attracting European retirees and Middle Eastern expatriates seeking long-stay preventive care. Investment in dedicated wellness corridors adjoining international airports accelerates private capital inflows, while public-sector incentives for eco-certifications facilitate market entry for boutique clinics without compromising environmental integrity.

Southeast Asia benefits from multilayered destination diversity, with Thailand’s wellness economy reaching THB 1,200 billion and registering 5.58% composite annual growth, supported by public funding to train 7,000 additional massage therapists and medical-wellness clusters in Phuket and Chiang Mai. Vietnam’s Decision 2951/QD-BYT charts a blueprint to transform traditional Vietnamese medicine into a tourism export, targeting double-digit visitor expansion by 2030. Indonesia courts wellness nomads through “second-home” visas and curated eco-retreat investment packages that elevate Bali’s peripheral regencies. Japan’s inbound tourism receipts crossed USD 35.05 billion in 2023, and regional governments channel funds into luxury ryokan renovations and forest-bathing networks to decentralize flows beyond Tokyo and Kyoto . Australia’s positioning leans on pristine nature and high clinical standards, yet currency strength and distance temper price competitiveness, prompting cross-promotion with South Pacific wellness cruises to amplify experiential uniqueness.

Competitive Landscape

The Asia-Pacific wellness tourism market remains structurally fragmented, with the five leading operators, Accor’s Spa & Vitality portfolio, Marriott’s EDITION and Ritz-Carlton Reserve, Banyan Tree’s Wellbeing Sanctuaries, Minor Hotels’ Anantara Wellness, and IHG’s Six Senses, collectively holding a relatively small share of the region’s overall revenue. Brand share diffusion reflects the heavy presence of independent boutique retreats, physician-owned medi-wellness clinics, and community-run eco-lodges that cater to localized heritage therapies. Major chains exploit distribution scale and loyalty ecosystems to maintain visibility across multiple feeder markets, yet homegrown players frequently outperform on guest satisfaction due to deeper cultural immersion and higher therapist-to-guest ratios.

Technology integration has emerged as a decisive differentiator; Anantara’s Layan Life invests in AI-driven body-composition scanners and predictive analytics that personalize detox protocols in real time, delivering quantifiable outcome reports at checkout. Banyan Tree’s Stay for Good initiative layers ESG reporting and guest carbon calculators onto wellness packages, attracting environmentally motivated philanthropists who view travel as an impact investment. Marriott, pursuing asset-light growth, signed 109 new APAC-excluding-China deals in 2024, with 19% of the pipeline dedicated to wellness-oriented luxury formats across Jakarta, Mumbai, and Fukuoka. Chinese conglomerates such as OCT Group expand OCT Yangle hot-spring clusters, leveraging domestic DTC channels to capture pent-up local demand and feeding cross-promotional flows to overseas acquisitions in Guam and Saipan.

Investment banks highlight rising M&A momentum as private-equity firms consolidate fragmented spa chains and aging resort stock ripe for wellness repositioning. Valuation multiples favor operators with proprietary practitioner academies and data-rich patient outcomes, underlining the strategic value of human capital and clinical intellectual property. Looking ahead, convergence of insurance reimbursements, fintech-enabled installment plans, and employer-sponsored retreats could accelerate brand consolidation as capital-intensive diagnostics become table stakes, raising entry barriers for smaller players lacking medical partnerships.

Asia-Pacific Wellness Tourism Industry Leaders

Accor

Marriott International

Banyan Tree Holdings

Hilton Worldwide

Minor International

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Marriott International announced 109 additional management deals across Asia-Pacific (excluding China), adding 21,439 rooms to a wellness-leaning pipeline of 363 properties, with luxury wellness flag EDITION set to debut in Jakarta and Mumbai.

- March 2025: Busan Metropolitan City secured KRW 500 million in national funding after ranking first in South Korea’s 2024 Wellness & Medical Tourism Convergence Cluster Assessment, enabling expansion of ten certified wellness zones that integrate forest therapy and coastal rejuvenation programs.

- January 2025: Anantara Riverside Bangkok Resort launched a 677 sqm Anantara Wellness complex featuring nine treatment suites, on-site TCM consulting rooms, and member packages starting at THB 150,000 that include biometric progress tracking.

- November 2025: TUI Group revealed plans to more than double its Asian hotel portfolio within three years, unveiling 22 wellness-centric properties under TUI Blue and unveiling new luxury brand “The Mora” in Bali.

Asia-Pacific Wellness Tourism Market Report Scope

Wellness tourism is an activity linked to maintaining or enhancing one's health and well-being. A complete background analysis of the Asia-Pacific wellness tourism market, which includes an assessment of the parental market, the report provides an overview of emerging trends in segments, significant changes in market dynamics, and a detailed analysis of the markets. The Asia-Pacific Wellness Tourism Market is segmented by travel type, which includes domestic and international; by activity, which includes in-country transport, lodging, food and beverage, shopping, activities and excursions, and other services; by travel type, which includes primary wellness travelers and secondary wellness travelers; and by geography, which includes China, India, Japan, Australia, Thailand, and other countries. The report offers market size and forecasts for the APAC wellness tourism market in terms of revenue (USD) for all the above segments.

By Service Type

| Yoga & Meditation Retreats |

| Spa & Beauty Therapies |

| Naturopathy & Detox Packages |

| Mental-Wellness Retreats |

| Digital-Detox Escapes |

| Spiritual Healing Journeys |

By Traveler Type

| Primary Wellness Travel |

| Secondary Wellness Travel |

By Accommodation Type

| Yoga Retreats |

| Wellness Hotels (Chain) |

| Boutique Retreats |

| Eco-Wellness Lodges |

| Wellness Clinics with Stay |

By Geography

| India |

| China |

| Japan |

| Australia |

| South Korea |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) |

| Rest of Asia-Pacific |

| By Service Type | Yoga & Meditation Retreats |

| Spa & Beauty Therapies | |

| Naturopathy & Detox Packages | |

| Mental-Wellness Retreats | |

| Digital-Detox Escapes | |

| Spiritual Healing Journeys | |

| By Traveler Type | Primary Wellness Travel |

| Secondary Wellness Travel | |

| By Accommodation Type | Yoga Retreats |

| Wellness Hotels (Chain) | |

| Boutique Retreats | |

| Eco-Wellness Lodges | |

| Wellness Clinics with Stay | |

| By Geography | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines) | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current value of the Asia-Pacific wellness tourism market?

The Asia-Pacific wellness tourism market size is estimated at USD 204.18 billion for 2026.

How fast is the sector expected to grow through 2031?

Market revenue is projected to expand at a 8.74% CAGR, reaching USD 310.56 billion by 2031.

Which service category leads regional revenue?

Spa and beauty therapies currently command the largest 19.21% revenue share in 2025.

Which traveler type offers the highest growth potential?

Primary wellness travel is forecast to grow at a 9.83% CAGR because more visitors dedicate entire trips to transformative health programs.

Which country will witness the fastest growth?

India is projected to record the highest CAGR of 11.14% through 2031, driven by supportive AYUSH visa policies.

Why are eco-wellness lodges gaining popularity?

Travelers increasingly associate environmental stewardship with personal well-being, propelling eco-wellness lodges to a 12.58% forecast CAGR.

Page last updated on: