Asia-Pacific Space Propulsion Market Size and Share

Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2017 - 2023 |

| Market Size (2025) | USD 58.65 Billion |

| Market Size (2030) | USD 95.25 Billion |

| Growth Rate (2025 - 2030) | 10.18% CAGR |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Space Propulsion Market Analysis by Mordor Intelligence

The Asia-Pacific Space Propulsion Market size is estimated at 58.65 billion USD in 2025, and is expected to reach 95.25 billion USD by 2030, growing at a CAGR of 10.18% during the forecast period (2025-2030).

The Asia-Pacific space propulsion industry is experiencing a significant transformation driven by increasing commercial space activities and technological advancements. Major space agencies and private companies are shifting their focus towards developing sustainable and efficient spacecraft propulsion technologies, particularly in the realm of green propulsion systems. This shift is exemplified by China's ambitious SatNet program, which plans to deploy a constellation of up to 13,000 satellites, demonstrating the region's growing appetite for large-scale space projects. The integration of advanced manufacturing techniques and smart materials has enabled the development of more sophisticated space engine systems, while simultaneously reducing production costs and improving operational efficiency.

A notable trend in the industry is the increasing emphasis on environmental sustainability and green propulsion technologies. Space organizations across the region are actively investing in research and development of eco-friendly propulsion systems to reduce the environmental impact of space activities. Companies like SpaceX have demonstrated significant progress in this direction, having successfully deorbited over 200 satellites using sustainable electric propulsion systems. This shift towards green technologies is particularly evident in countries like Japan and India, where research institutions are focusing on developing non-toxic propellants and more efficient propulsion systems.

The industry is witnessing a surge in strategic partnerships and collaborative initiatives between private companies and government space agencies. In February 2023, Thales Alenia Space secured a contract with the Korea Aerospace Research Institute (KARI) to provide integrated electric propulsion for the GEO-KOMPSAT-3 satellite, scheduled for launch in 2027. These collaborations are fostering innovation and accelerating the development of advanced propulsion technologies, while also promoting knowledge transfer and technological expertise across the region.

Government support and increasing investments in space programs are playing a crucial role in shaping the market landscape. Countries across the region are establishing dedicated space agencies and implementing supportive regulatory frameworks to facilitate the growth of their domestic space industries. For instance, the Indian Space Research Organization (ISRO) received a significant funding boost of USD 2 billion in February 2023 for various space-related activities, including the development of satellite propulsion systems. This governmental backing, coupled with private sector investments, is creating a robust ecosystem for the development and deployment of advanced propulsion technologies, particularly in emerging space economies across the Asia-Pacific region.

Asia-Pacific Space Propulsion Market Trends and Insights

Increased spending by China, India, Japan, and South Korea are the growth drivers

- The demand for satellite propulsion systems is driven by increased spending on satellite programs by various countries, such as the manufacture and launch of national satellite internet constellation of up to 13,000 satellites. China's SatNet has been engaging with commercial companies as it develops a blueprint for constructing the "Guowang" constellation. Notably, these and other small satellites require onboard propulsion to reduce the chances of collision and mitigate the issue of debris in low Earth orbit. Several companies in the region are developing space propulsion technologies. In May 2022, a Chinese satellite electric propulsion company named Kongtian Dongli announced that it secured a multi-million yuan angel round financing amid a proliferation of Chinese satellite constellation plans. The company's main products are Hall thrusters and microwave electric propulsion systems, with an on-orbit test of the latter planned before December this year.

- Likewise, in February 2023, the Indian government announced that ISRO is expected to receive USD 2 billion for various space-related activities, including the development of the Liquid Propulsion Systems Centre (LPSC) and the ISRO Propulsion Complex. In March 2021, Japan announced spending USD 4.14 billion on space-related activities. The country mentioned having allocated JPY 18.9 billion for the H3 rocket development. In January 2020, JAXA mentioned that JPY 3.6 billion was allocated to fund the research and development of core engine technologies that significantly improve fuel consumption and reduce environmental burden, as well as the research and development of the silent supersonic aeroplane and emission-free aircraft (electric-powered propulsion systems).

Segment Analysis: PROPULSION TECH

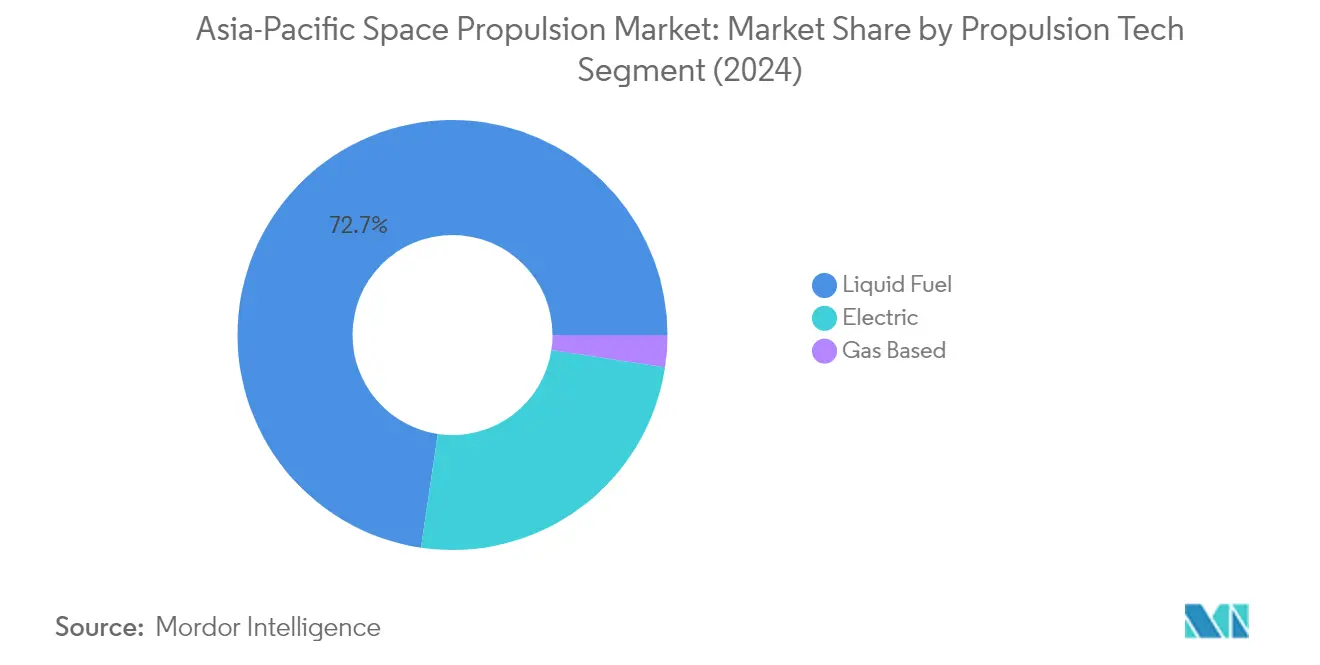

Liquid Fuel Segment in Asia-Pacific Space Propulsion Market

The liquid fuel propulsion technology dominates the Asia-Pacific space propulsion market, commanding approximately 73% market share in 2024. This significant market position is primarily driven by the technology's high efficiency, controllability, reliability, and extended lifespan characteristics, making it an ideal choice for various space missions. The segment's dominance is further strengthened by its versatility in different orbit classes for satellites, from low Earth orbit to geostationary orbit. Major space agencies and private companies in the region are actively investing in liquid propulsion technology development, particularly focusing on reusable liquid propulsion engines and innovative fuel combinations like liquid oxygen & methane (LOX/CH4) and liquid oxygen & kerosene (LOX/KP1). The development of green propellants and advancements in manufacturing technologies are also contributing to the segment's market leadership.

Gas-Based Segment in Asia-Pacific Space Propulsion Market

The gas-based propulsion segment is emerging as the fastest-growing segment in the Asia-Pacific space propulsion market, with a projected growth rate of approximately 15% during 2024-2029. This remarkable growth is driven by the increasing adoption of cold gas propulsion thrusters and green propellants, particularly in small satellites and CubeSats. The segment's growth is further accelerated by its cost-effectiveness, reliability, and suitability for orbital maintenance, maneuvering, and attitude control applications. Space organizations in the region are emphasizing the development of environmentally friendly gas-based propulsion systems, with countries like Japan and India actively researching and implementing green propellant technologies. The segment's expansion is also supported by technological advancements in gas propulsion systems, making them more efficient and suitable for a wider range of space applications.

Remaining Segments in Propulsion Tech

The electric propulsion segment represents a significant portion of the Asia-Pacific space propulsion market, offering unique advantages in terms of specific impulse and efficiency. This technology is particularly valuable for commercial communication satellites and scientific missions, where precise control and long-term operation are essential. The segment has witnessed substantial technological advancements, including the development of Hall-effect thrusters, ion propulsion thrusters, and other innovative electric propulsion solutions. Major space agencies and private companies in the region are increasingly investing in electric propulsion research and development, recognizing its potential for future space exploration and satellite operations. The technology's ability to reduce propellant mass requirements while maintaining high performance makes it an attractive option for various space missions.

Asia-Pacific Space Propulsion Market Geography Segment Analysis

Space Propulsion Market in China

China continues to dominate the Asia-Pacific space propulsion market, commanding approximately 89% of the total market value in 2024. The country's satellite manufacturing industry has experienced remarkable growth, driven by substantial government investments in various satellite systems spanning communication, broadcasting, navigation, weather forecasting, and disaster monitoring applications. The development of electric propulsion technologies has been particularly noteworthy, with significant advancements made by academic institutes and industrial companies, including the Shanghai Spaceflight Power Machinery Institute (SPMI) and the Center for Space Science and Applied Research of the Chinese Academy of Sciences (CSSAR). These institutions have made considerable progress in developing various electric propulsion technologies, including Hall-effect thrusters, ion thrusters, resistors, arcjet, pulsed plasma thrusters, and microwave plasma thrusters. The country's private sector has also demonstrated significant innovation in reusable liquid spacecraft engine propulsion engines, with companies equally divided between developing liquid oxygen & methane (LOX/CH4) and liquid oxygen & kerosene (LOX/KP1) systems.

Space Propulsion Market in India

India's space propulsion market is poised for exceptional growth, with a projected CAGR of approximately 26% from 2024 to 2029. The country's indigenous development capabilities have expanded significantly, particularly in electric propulsion systems and advanced propulsion technologies. The Liquid Propulsion Systems Centre (LPSC) has emerged as a crucial facility for research and development, focusing on high-power electric propulsion systems and various thruster technologies. The organization has successfully developed and tested multiple stationary plasma thrusters with different thrust capabilities, ranging from 18mN to 300mN. The establishment of sophisticated electric propulsion facilities at LPSC has enhanced the country's capacity to develop and qualify various propulsion systems, including stationary plasma thrusters, power processing units, and Xenon feed systems. This infrastructure development has positioned India to support propulsion systems development up to a thrust level of 1N, marking a significant advancement in the country's space propulsion capabilities.

Space Propulsion Market in Japan

Japan's space propulsion industry has established itself as a pioneer in advanced propulsion technologies, with a particular focus on electric propulsion and plasma propulsion systems. The country has made significant strides in developing electric propulsion systems that offer greater efficiency and endurance compared to traditional chemical propulsion systems. Japanese research institutions and companies have demonstrated expertise in plasma propulsion technology, utilizing high-temperature ionized gas for spacecraft propulsion. The solid rocket propulsion sector has also seen considerable advancement, with companies developing sophisticated solid rocket motors for various space applications. These motors are characterized by their high reliability, cost-effectiveness, and long-term storage capabilities. The Japanese space propulsion industry has fostered strong international collaborations, particularly with European and US-based companies, to develop cutting-edge electric propulsion systems and expand their global market presence.

Space Propulsion Market in Australia

Australia's space propulsion sector has undergone significant transformation since the establishment of the Australian Space Agency in 2018. The country's space industry has aligned its development with the Australian Civil Space Strategy (2019-2028), focusing on strengthening Earth observation capabilities, positioning, navigation, and timing systems. Australian companies have made notable progress in developing advanced propulsion technologies, including innovative electric propulsion systems and hybrid rockets that offer improved efficiency and endurance. The industry has particularly emphasized the development of cost-effective and environmentally sustainable propulsion solutions. Australian organizations have fostered strong international partnerships to accelerate technological advancement and expand their market reach, collaborating with established global players in developing sophisticated electric propulsion systems and other space technologies.

Space Propulsion Market in Other Countries

The space propulsion market in other Asia-Pacific countries, including Singapore, South Korea, and New Zealand, demonstrates diverse technological capabilities and growth potential. Singapore has emerged as a notable player in satellite technology and propulsion systems, with several companies actively engaged in developing electric propulsion systems and innovative propulsion technologies. South Korea has made significant advances through the Korea Aerospace Research Institute (KARI), focusing on developing sophisticated satellite systems and propulsion technologies. New Zealand has established itself as an emerging space nation, with companies focusing on sustainable and innovative propulsion solutions. These countries have implemented supportive regulatory frameworks and fostered collaboration between government agencies, research institutions, and private companies to accelerate the development of their space propulsion capabilities.

Competitive Landscape

Top Companies in Asia-Pacific Space Propulsion Market

The competitive landscape is characterized by companies focusing heavily on technological advancement and innovation, particularly in electric propulsion systems and sustainable space propulsion technologies. Major players are investing in research and development to enhance fuel efficiency, reduce environmental impact, and develop reusable propulsion systems. Companies are actively pursuing strategic partnerships and collaborations to strengthen their market presence and expand their technological capabilities. There is a notable trend towards expanding manufacturing facilities and production capacities to meet growing demand, particularly in countries like China and India. Market leaders are also emphasizing the development of complete propulsion solutions, from fuel tanks to thrusters and thrust vector control systems, while simultaneously working on reducing manufacturing costs and improving operational efficiency.

Market Dominated by Global Technology Conglomerates

The Asia-Pacific space propulsion market exhibits a consolidated structure, with major global aerospace and defense conglomerates holding significant market share. These established players leverage their extensive research capabilities, technological expertise, and strong relationships with government space agencies to maintain their market positions. The market is characterized by a mix of international players and emerging regional companies, with Chinese and Indian firms increasingly gaining prominence through government support and indigenous technology development programs.

The competitive dynamics are shaped by high entry barriers due to substantial capital requirements and complex technological expertise needed for developing spacecraft propulsion systems. While mergers and acquisitions activity remains limited, strategic partnerships and joint ventures are becoming increasingly common, particularly between established global players and regional companies looking to expand their capabilities. The market also sees collaboration between private companies and government space agencies, creating a unique ecosystem that combines public sector requirements with private sector innovation.

Innovation and Partnerships Drive Future Success

Success in the satellite propulsion market increasingly depends on companies' ability to develop cost-effective, efficient, and environmentally sustainable propulsion technologies. Market players need to focus on developing modular and scalable propulsion systems that can serve various satellite sizes and mission requirements. Companies must also establish strong relationships with government space agencies and commercial satellite manufacturers while investing in local manufacturing capabilities to comply with regional procurement preferences and regulations.

Future market success will require companies to navigate complex regulatory environments across different countries while maintaining high safety and reliability standards. Players must focus on developing specialized expertise in emerging technologies like electric propulsion and green propellants while building robust supply chains to ensure component availability. Companies also need to consider the growing trend of satellite constellation deployments and develop propulsion solutions specifically tailored for these applications. Additionally, establishing strong after-sales support and maintenance capabilities will become increasingly important as the satellite population grows.

Asia-Pacific Space Propulsion Industry Leaders

Ariane Group

Honeywell International Inc.

Moog Inc.

Northrop Grumman Corporation

Safran SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2023: Thales Alenia Space has contracted with the Korea Aerospace Research Institute (KARI) to provide the integrated electric propulsion on their GEO-KOMPSAT-3 (GK3) satellite.

- December 2022: GKN Aerospace contracted with ArianeGroup to supply the next stage of the Ariane 6 turbine and Vulcain nozzle. The contract covers the manufacturing and supply of units for 14 Ariane 6 launchers, which are expected to go into production by 2025. GKN Aerospace is currently focused on industrializing and integrating novel and innovative technologies into the Ariane 6 product.

- November 2022: Two Northrop Grumman Corporation five-stage solid rocket boosters helped launch the first flight of NASA's Space Launch System "SLS"; as part of the Artemis I mission. This is the first in a series of Artemis missions focused on deep space exploration.

Asia-Pacific Space Propulsion Market Report Scope

Electric, Gas based, Liquid Fuel are covered as segments by Propulsion Tech. Australia, China, India, Japan, New Zealand, Singapore, South Korea are covered as segments by Country.| Electric |

| Gas based |

| Liquid Fuel |

| Australia |

| China |

| India |

| Japan |

| New Zealand |

| Singapore |

| South Korea |

| Propulsion Tech | Electric |

| Gas based | |

| Liquid Fuel | |

| Country | Australia |

| China | |

| India | |

| Japan | |

| New Zealand | |

| Singapore | |

| South Korea |

Market Definition

- Application - Various applications or purposes of the satellites are classified into communication, earth observation, space observation, navigation, and others. The purposes listed are those self-reported by the satellite’s operator.

- End User - The primary users or end users of the satellite is described as civil (academic, amateur), commercial, government (meteorological, scientific, etc.), military. Satellites can be multi-use, for both commercial and military applications.

- Launch Vehicle MTOW - The launch vehicle MTOW (maximum take-off weight) means the maximum weight of the launch vehicle during take-off, including the weight of payload, equipment and fuel.

- Orbit Class - The satellite orbits are divided into three broad classes namely GEO, LEO, and MEO. Satellites in elliptical orbits have apogees and perigees that differ significantly from each other and categorized satellite orbits with eccentricity 0.14 and higher as elliptical.

- Propulsion tech - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Mass - Under this segment, different types of satellite propulsion systems have been classified as electric, liquid-fuel and gas-based propulsion systems.

- Satellite Subsystem - All the components and subsystems which includes propellants, buses, solar panels, other hardware of satellites are included under this segment.

| Keyword | Definition |

|---|---|

| Attitude Control | The orientation of the satellite relative to the Earth and the sun. |

| INTELSAT | The International Telecommunications Satellite Organization operates a network of satellites for international transmission. |

| Geostationary Earth Orbit (GEO) | Geostationary satellites in Earth orbit 35,786 km (22,282 mi) above the equator in the same direction and at the same speed as the earth rotates on its axis, making them appear fixed in the sky. |

| Low Earth Orbit (LEO) | Low Earth Orbit satellites orbit from 160-2000km above the earth, take approximately 1.5 hours for a full orbit and only cover a portion of the earth’s surface. |

| Medium Earth Orbit (MEO) | MEO satellites are located above LEO and below GEO satellites and typically travel in an elliptical orbit over the North and South Pole or in an equatorial orbit. |

| Very Small Aperture Terminal (VSAT) | Very Small Aperture Terminal is an antenna that is typically less than 3 meters in diameter |

| CubeSat | CubeSat is a class of miniature satellites based on a form factor consisting of 10 cm cubes. CubeSats weigh no more than 2 kg per unit and typically use commercially available components for their construction and electronics. |

| Small Satellite Launch Vehicles (SSLVs) | Small Satellite Launch Vehicle (SSLV) is a three-stage Launch Vehicle configured with three Solid Propulsion Stages and a liquid propulsion-based Velocity Trimming Module (VTM) as a terminal stage |

| Space Mining | Asteroid mining is the hypothesis of extracting material from asteroids and other asteroids, including near-Earth objects. |

| Nano Satellites | Nanosatellites are loosely defined as any satellite weighing less than 10 kilograms. |

| Automatic Identification System (AIS) | Automatic identification system (AIS) is an automatic tracking system used to identify and locate ships by exchanging electronic data with other nearby ships, AIS base stations, and satellites. Satellite AIS (S-AIS) is the term used to describe when a satellite is used to detect AIS signatures. |

| Reusable launch vehicles (RLVs) | Reusable launch vehicle (RLV) means a launch vehicle that is designed to return to Earth substantially intact and therefore may be launched more than one time or that contains vehicle stages that may be recovered by a launch operator for future use in the operation of a substantially similar launch vehicle. |

| Apogee | The point in an elliptical satellite orbit which is farthest from the surface of the earth. Geosynchronous satellites which maintain circular orbits around the earth are first launched into highly elliptical orbits with apogees of 22,237 miles. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.