Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 9.08 Billion |

| Market Size (2026) | USD 9.53 Billion |

| Market Size (2031) | USD 12.55 Billion |

| Growth Rate (2026 - 2031) | 5.66% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific LED Packaging Market Analysis by Mordor Intelligence

The Asia Pacific LED packaging market size is expected to grow from USD 9.08 billion in 2025 to USD 9.53 billion in 2026 and is forecast to reach USD 12.55 billion by 2031 at a 5.66% CAGR over 2026-2031. Demand is pivoting from commodity lighting toward high-density Mini LED and Micro LED packages that support premium televisions, augmented-reality wearables and adaptive-beam headlamps. China remains the volume anchor, yet localized incentive programs in India and Southeast Asia are redistributing new capacity and tightening regional competition. Thermal management, mass-transfer precision and driver integration have become core value drivers, raising capital intensity while creating barriers to entry for smaller firms. Panel makers and tier-one automotive suppliers are vertically integrating packaging activities to lock in supply security, reduce time-to-market and capture component margins.

Key Report Takeaways

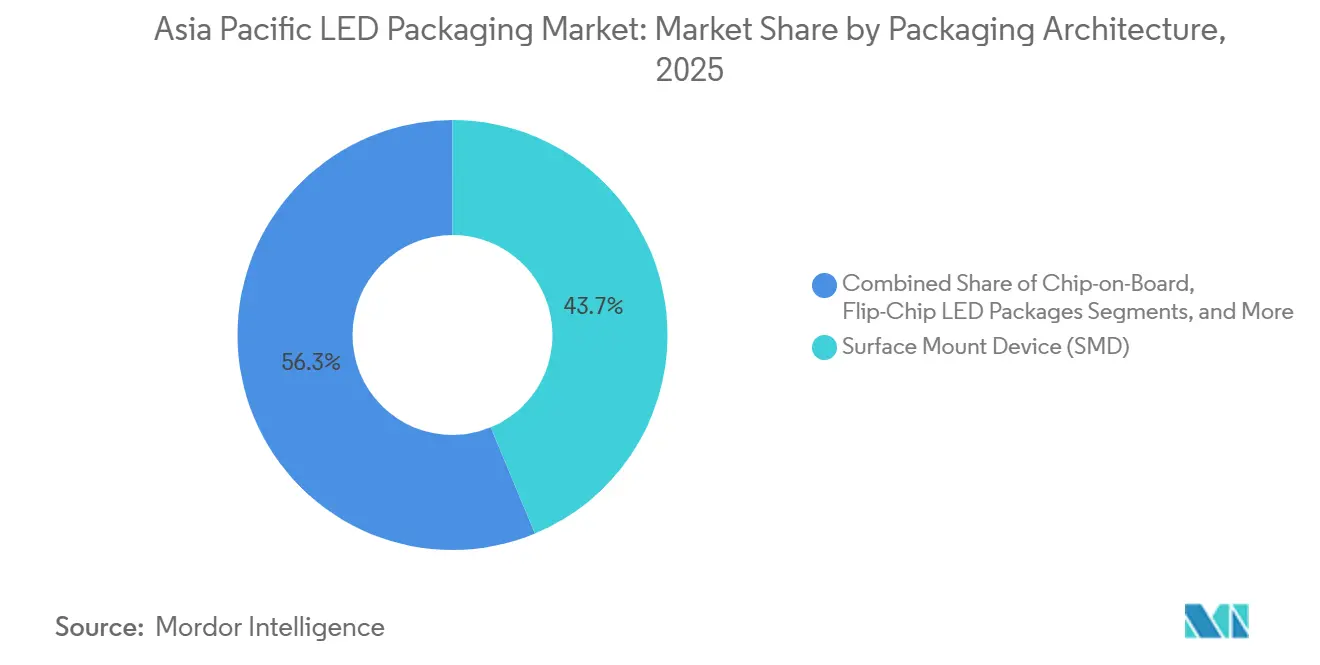

- By packaging architecture, Surface Mount Device packages led with 43.74% revenue share in 2025, while Chip Scale Package solutions are advancing at a 6.28% CAGR to 2031.

- By power class, Mid-power LEDs captured 39.38% of the Asia Pacific LED packaging market share in 2025, whereas high-power devices are projected to expand at a 6.21% CAGR through 2031.

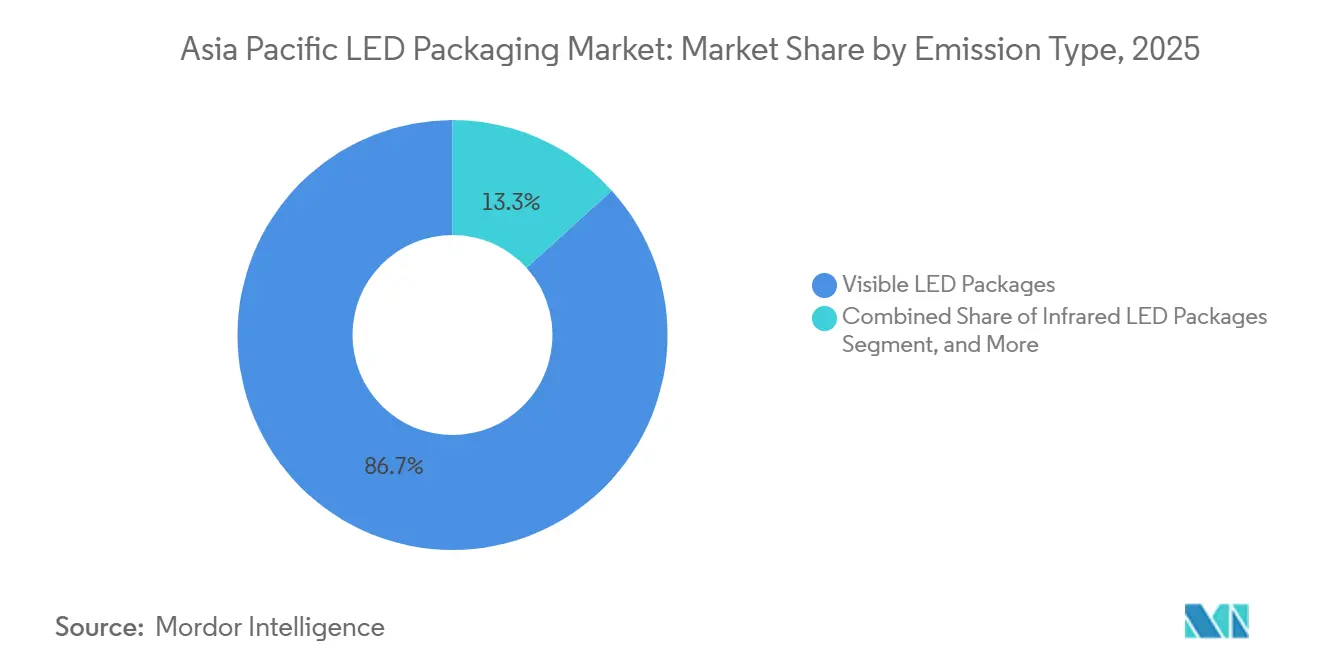

- By emission type, visible LEDs dominated volume with 86.73% in 2025; ultraviolet packages represent the fastest-growing slice at a 6.15% CAGR to 2031.

- By material chemistry, substrates accounted for 34.95% of spending in 2025, yet phosphors and coatings are growing faster at a 5.99% CAGR through 2031.

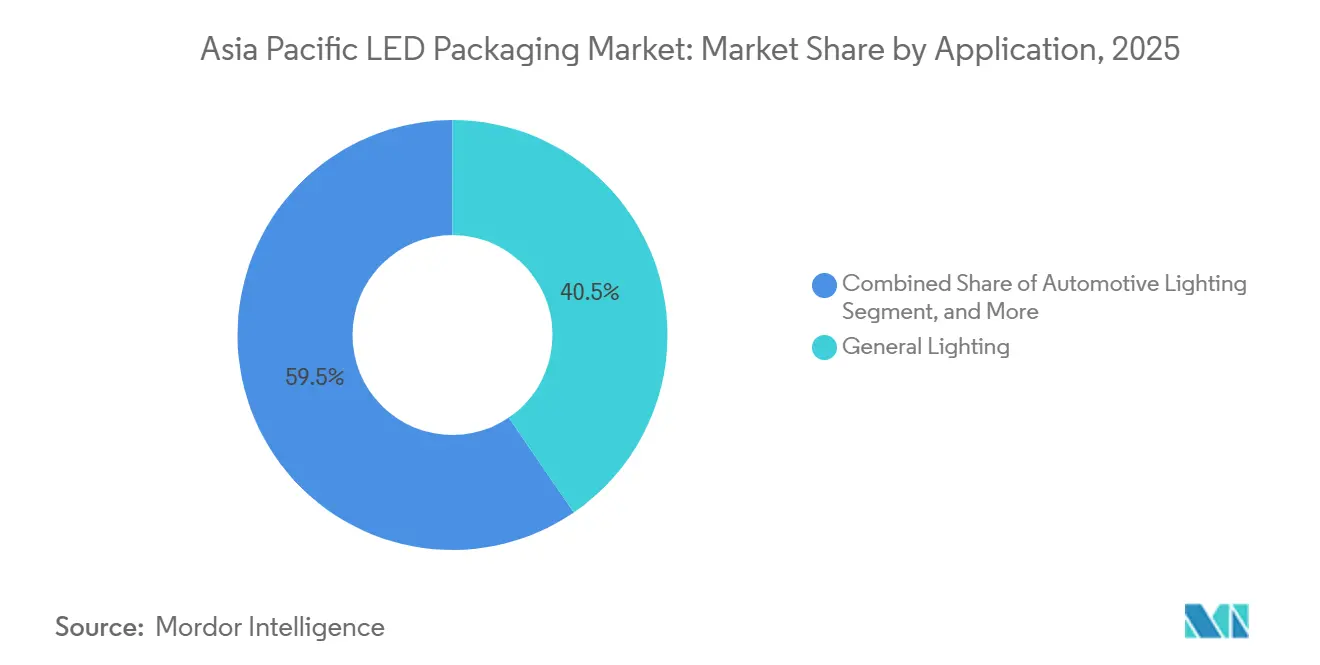

- By application, general lighting held 40.47% share in 2025, and automotive lighting posts the highest projected CAGR at 5.91% over 2026-2031.

- By geography, China held 50.88% share in 2025 and India represents the fastest-growing market at a 5.87% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia Pacific LED Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of Mini-LED and Micro-LED Backlighting | +1.2% | China, South Korea, Japan; spillover to India and Southeast Asia | Medium term (2-4 years) |

| Government Energy-Efficiency Mandates Boosting LED Uptake | +0.9% | China, India, Japan; regulatory harmonization across ASEAN | Short term (≤ 2 years) |

| Declining ASP of LED Packages Through Economies of Scale | +0.7% | Global, with strongest effects in China manufacturing clusters | Long term (≥ 4 years) |

| Rising Automotive LED Penetration in Headlamps and ADAS | +1.3% | China, South Korea, Japan; export-driven gains in Thailand and Vietnam | Medium term (2-4 years) |

| Localization Incentives for Advanced Packaging Lines in China and India | +0.8% | China, India; secondary effects in Malaysia and Vietnam | Medium term (2-4 years) |

| Emergence of Flip-Chip CSP for Horticulture Lighting Customisation | +0.4% | China, Japan, India; niche adoption in Southeast Asia vertical farms | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of Mini-LED and Micro-LED Backlighting

Television makers accelerated Mini LED penetration to roughly 10% of regional shipments in 2026, as energy-efficiency subsidies in China reward Level-1-compliant sets. Samsung introduced six Micro RGB TV sizes that eliminate color filters and deliver full BT.2020 gamut certification, reinforcing the move toward chip-level integration.[1]LEDINSIDE, “Samsung 2026 Micro RGB TV Line-Up,” ledinside.com Automakers from Xiaomi to BMW are committed to Mini LED cockpit displays that exceed 4,000 nits, expanding demand for high-brightness packages that manage elevated junction temperatures. The shift favors chip-on-board and glass-substrate modules, prompting panel makers to internalize packaging and forcing independent vendors to specialize in high-yield mass-transfer equipment. Micro LED revenue doubled to USD 105.4 million in 2026, and near-eye AR shipments are projected at 21 million units by 2030, setting the stage for sustained packaging innovation.

Government Energy-Efficiency Mandates Boosting LED Uptake

China’s March 2026 standard widened coverage to spotlight, high-bay luminaires, and smart products with a 0.5-watt standby limit, tightening efficacy baselines across commercial construction.[2]RCGEOTECH, “China 2026 LED Energy-Efficiency Standard,” rcgeotech.com Japan mandated 100 % LED road lighting on national highways by 2030 to meet decarbonization goals. India’s Production-Linked Incentive scheme unlocked INR 10 478 crore (USD 1.26 billion) for localization, aiming to lift domestic value addition to 75-80%. Divergent testing protocols between Asia and Europe compel exporters to dual-qualify products, spurring demand for chip-on-board packages that surpass 150 lumens-per-watt.

Declining ASP of LED Packages Through Economies of Scale

Bulk procurement under India’s Domestic Efficient Lighting Program once slashed bulb prices by 75%, demonstrating how volume commitments compress upstream package margins.[3]LEDINSIDE, “India LED Bulb Price Drop Analysis,” ledinside.com China’s Zhaochi now ships roughly 12,000 mini-RGB kilopieces monthly while running 1.1 million four-inch wafers, highlighting the scale needed for price leadership. Bridgelux flip-chip CSP parts achieve 209 lm/W at 350 mA, eliminating wire bonds to reduce material costs and improve thermal performance. The squeeze is forcing mid-tier suppliers to either consolidate or pivot toward niche ultraviolet, automotive, or horticulture niches where qualification hurdles temper price erosion.

Rising Automotive LED Penetration in Headlamps and ADAS

Adaptive driving beam revenue reached USD 4.52 billion in 2025 and is growing at 24.5% globally, with Asia Pacific logging the steepest 28.7% climb as Chinese and Korean OEMs deploy pixel arrays to rival European brands. Nichia and Infineon co-developed a 16,384-pixel Micro LED engine that embeds driver ICs, enabling per-pixel dimming and on-chip thermal monitoring. LG Innotek’s ultra-thin pixel module trims thickness to 0.12 inch, opening grille and bumper integration for vehicle-to-everything communication. As yields rise and driver integration lowers bill-of-materials costs, the cost premium over halogen declines, pointing to mainstream adoption in mid-range cars by 2028.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial CapEx for Advanced Packaging Equipment | -0.6% | China, India, Southeast Asia; acute for small and medium enterprises | Short term (≤ 2 years) |

| Thermal Management Challenges in High-Power Packages | -0.5% | Global, with highest impact in automotive and industrial segments | Medium term (2-4 years) |

| Phosphor Supply Constraints from Rare-Earth Bottlenecks | -0.7% | Global, with acute ex-China sourcing challenges | Medium term (2-4 years) |

| Patent Expiry Cliff Creating Pricing Pressures | -0.4% | China, Taiwan, India; less impact in Japan and South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial CapEx for Advanced Packaging Equipment

C Sun invested NT 1.48 billion (USD 46.9 million) in a new Taichung site for AI-driven advanced packaging tools, underlining the steep outlay required for ±1 µm Micro LED placement accuracy. Wuxi NOVO’s Thailand branch supports regional customers with Mini LED backlight automation, yet even contract assembly now demands proprietary robotics that many small companies cannot finance.[4]WUXI NOVO, “Thailand Automation Factory,” wuxinovo.com NationStar plans CNY 970.1 million (USD 116.4 million) in six Mini and Micro LED projects, with payback periods of 7 to 8 years, discouraging late entrants. These economics channel new capacity toward large conglomerates or joint ventures that can amortize tooling over multiple product lines.

Thermal Management Challenges in High-Power Packages

Heat flux in automotive-grade LEDs can exceed 85 W cm⁻², with 70-85% of input power dissipated as heat. Simulations show that adding 9 copper vias in FR-4 reduces junction temperature from 129 °C to about 71 °C, yet gains plateau beyond 16 vias, prompting designers to shift toward aluminum-nitride substrates at higher cost. Chip-on-board on metal-core PCBs reduces package thermal resistance but introduces challenges to optical uniformity during phosphor coating. Automotive pixel arrays pack 16,384 Micro LEDs into compact headlamp footprints, making the co-design of drivers, substrates, and heatsinks mandatory and increasing system costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Architecture: CSP Gains as SMD Matures

Surface Mount Device packages accounted for 43.74% of the Asia Pacific LED packaging market size in 2025, sustaining dominance in general illumination fixtures and edge-lit displays. Chip Scale Package revenue is advancing at a 6.28% CAGR through 2031 as flip-chip designs eliminate ceramic submounts, trim the bill of materials, and reduce thermal resistance. Panel makers in China increasingly deploy chip-on-board Mini LED bars in 75-inch-plus televisions, compressing the supply chain and shifting profit pools away from independent packagers. Japanese and Korean automotive suppliers favor flip-chip layouts that simplify automated optical inspection and support per-LED current sensing, a prerequisite for AEC-qualified headlamps.

Continued CSP cost erosion stems from high wafer-level throughput and fewer assembly steps, yet reliability under sulfur exposure and high humidity remains a concern for outdoor signage. SMD producers are responding with epoxy-mold-compound upgrades and secondary optics, but price gaps persist. The Asia Pacific LED packaging industry now observes a dual-track model: commodity SMD lines run at hyperscale in the Pearl River Delta, whereas CSP lines co-located with driver back-end flow in Jiangsu and Taiwan focus on performance-critical segments. Suppliers lacking advanced mass-transfer or flip-chip expertise face shrinking addressable markets as display and automotive verticals internalize packaging.

By Power Class: High-Power Surges on Automotive Demand

Mid-power parts ranging from 0.5-1 W captured 39.38% of Asia Pacific LED packaging market share in 2025. High-power components above 1 W are growing faster at 6.21% CAGR as adaptive-beam headlamps demand robust lumen density. Thermal-via optimization allows select mid-power footprints to encroach on indoor high-bay niches; however, automotive specifications still require ceramic or metal-core substrates that withstand -40 °C to 125 °C cycles.

Ultra-high-power arrays above 3 W address sports arenas and horticulture greenhouses where fixture count must be minimized. OEMs weigh single high-power emitters against clustered mid-power assemblies: clusters lower thermal hotspots but increase driver channel count and optical alignment complexity. Suppliers that span the full power spectrum hedge against these architecture choices and lock in volume regardless of OEM design selection.

By Emission Type: UV Packages Accelerate on Disinfection Pull

Visible LEDs represented 86.73% of shipments in 2025, underpinned by white phosphor-converted products for general lighting, displays, and mobile flash. Ultraviolet devices, though niche, are climbing at a 6.15% CAGR as mercury-lamp bans under the Minamata Convention accelerate UVC adoption in municipal water systems. Nichia’s 7.4% wall-plug-efficient deep-UV LED at 280 nm signals a step change in germicidal efficacy per watt.

UV package reliability hinges on quartz or glass lenses that resist photon-induced discoloration. Encapsulant shrinkage under high-flux UVC can reduce radiant output by 30% across 10,000 h if not addressed with fluoropolymer coatings. Segment success, therefore, depends on materials innovation as much as chip efficiency. Visible part suppliers with established epoxy supply chains must invest in new chemistries or risk missing the UV opportunity.

By Material Chemistry: Phosphors Outpace Substrates

Substrates consumed 34.95% of material spending in 2025, with sapphire leading blue and UV epitaxy, while silicon carbide and aluminum nitride capture high-power niches. Phosphors and coatings, which are expanding at a 5.99% CAGR, benefit from demand for tunable spectra in human-centric and horticulture lighting. China’s October 2025 export controls on yttrium, europium, and cerium have quadrupled ex-China prices, driving packagers to sign long-term supply contracts or explore rare-earth-lean formulations.

Substrate innovation focuses on silicon platforms enabling monolithic driver integration, yet lattice mismatch with gallium nitride still limits external quantum efficiency. Ceramic boards with thermal conductivity above 170 W m-K command premiums in automotive-grade lighting. Material cost inflation is thus bifurcated, rare-earth scarcity lifts phosphor pricing, while advanced ceramics raise initial bill-of-materials but lower total cost of ownership by improving lumen maintenance.

By Application: Automotive Lighting Outpaces General Lighting

General lighting retained a 40.47% share in 2025, though replacement cycles are lengthening as luminaires rated for 50,000 h saturate mature markets. Automotive lighting is now the fastest-growing segment, with a 5.91% CAGR, propelled by electric-vehicle brand differentiation through adaptive beams and Micro LED cockpit clusters. Display backlighting is transitioning to direct-lit Mini LED grids in premium televisions, aided by China’s energy-efficiency subsidies, whereas smartphone OEMs weigh Mini LED versus OLED on cost and burn-in risk.

Industrial specialties-including UV curing, machine vision, and medical phototherapy-command double-digit gross margins but represent under 10% of package volume. Suppliers balancing high-volume SMD lines with bespoke automotive or UV programs insulate themselves from cyclicality in any single vertical. However, qualification cycles in automotive average 24-30 months, locking in suppliers early and limiting switching opportunities for late entrants.

Geography Analysis

China controlled about half of regional revenue in 2025 on the back of fully integrated players such as Sanan Optoelectronics and NationStar. Sanan scaled its Hubei site to 130,000 × 4-inch LED wafers and 2,000 × 6-inch Micro LED wafers per month, and targets 75,000 more 4-inch and 1,000 additional 6-inch wafers by end-2026, while sustaining yield at 99.99% and ±1 µm placement accuracy. NationStar, second in full-color LEDs domestically, is raising a CNY 970.1 million (USD 116.4 million) war chest for Mini LED capacity, sensing modules and automotive devices. China’s 15th Five-Year Plan emphasizes semiconductor self-reliance, while extended rare-earth export controls tighten foreign dependence on domestic yttrium and europium.

Japan provides high-performance niches anchored by Nichia, Toyoda Gosei and Stanley Electric. Nichia’s Aachen automotive center bridges European OEM proximity with Japanese process know-how, underscoring export-oriented R&D. Government road-lighting mandates require 100% LED adoption on national highways by 2030, further lifting domestic demand. Japanese vendors offshore commodity output to Southeast Asia yet keep ultraviolet and specialty lines at home to safeguard intellectual property.

India is the fastest-growing geography at 5.87% CAGR. The Production-Linked Incentive and Electronics Component Manufacturing Scheme together allocate over INR 239.7 billion (USD 2.98 billion) in benefits, luring multinationals seeking China-plus-one diversification. Calcom Vision’s upgraded INR 25 crore (USD 3 million) investment unlocks higher incentive slabs and broadens its module portfolio. Infrastructure gaps-namely power reliability and raw-material depth-remain bottlenecks, but phased-manufacturing roadmaps target 75-80% local value addition by 2029.

Thailand, Vietnam and Malaysia are evolving from assembly hubs into higher-value testing and module integration. Sunlight Lighting is injecting RMB 324 million (USD 38.9 million) into a BOI-certified Thai plant for tax exemptions and 100% foreign ownership. Seoul Semiconductor’s OMINSU tie-up positions Vietnam to export driverless and natural-spectrum lamps. Yet the region still imports most LED chips and phosphors from China, exposing it to upstream trade risks.

South Korea and Taiwan contribute display-centric innovation. LG Innotek’s KRW 100 billion (USD 67.9 million) expansion in Gwangju backs automotive application processors, while Samsung’s six-size Micro RGB TV lineup validates sub-100 µm chip mass-transfer scalability. Taiwanese packagers consolidate and shift toward Mini and Micro LED but face rising vertical integration by mainland panel makers, pressuring independent houses unless they secure proprietary yield-boosting IP.

Competitive Landscape

The Asia Pacific LED packaging market is moderately fragmented, with the top five suppliers accounting for a high combined share. Sanan Optoelectronics rides hyperscale commodity chips and advanced Micro LED lines, whereas NationStar leverages display and automotive qualifications. Nichia safeguards its dominance in ultraviolet and specialty lighting through an extensive patent portfolio and 70-plus CRI efficacy leadership. Samsung integrates chips into finished Micro LED displays through modules, retaining margins in its value chain. Everlight pivots toward automotive and industrial segments to escape price wars in general lighting.

Panel makers BOE, TCL, CSOT, and Tianma are vertically integrating upstream to seize Mini and Micro LED margins, threatening to disintermediate traditional packagers unless those vendors develop proprietary mass-transfer methods or focus on domains such as UV where panel integration offers limited advantage. Technology capabilities-in-line AI yield analytics, automated optical inspection and per-LED current feedback-constitute the new competitive currency. Nichia-Infineon’s 16,384-pixel engine illustrates how deep electronics collaboration raises the entry bar.

Litigation risk persists as incumbent licensors guard intellectual property. Seoul Semiconductor and Nichia continue to pursue component and end-product injunctions against Chinese and Taiwanese firms that allegedly infringe patents, placing compliance burdens on TV and lamp OEMs. Average selling-price erosion in mainstream SMDs is accelerating consolidation, Sanan recorded its first annual loss since 2008 as subsidies waned, highlighting the urgency for portfolio migration into silicon carbide, integrated circuits and automotive-grade packages. White-space opportunities lie in tunable-spectrum human-centric lighting, ultra-high-power stadium floodlights and integrated driver-in-package IoT modules.

Asia Pacific LED Packaging Industry Leaders

Nichia Corporation

OSRAM Licht AG

Seoul Semiconductor Co. Ltd

Samsung Electronics Co. Ltd

Everlight Electronics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Sanan Optoelectronics scaled Hubei capacity to 130 000 4-inch LED wafers and 2 000 6-inch Micro LED wafers per month, targeting further expansion by year-end.

- March 2026: Sunlight Lighting confirmed RMB 324 million (USD 38.9 million) investment to establish a Thailand factory under BOI incentives.

- February 2026: C Sun acquired a NT 1.48 billion (USD 46.9 million) Taichung site to build AI-enabled advanced packaging equipment lines.

- January 2026: LG Innotek allocated KRW 100 billion (USD 67.9 million) for its Gwangju automotive application-processor module plant, slated for completion in Dec 2026.

Asia Pacific LED Packaging Market Report Scope

The Asia Pacific LED Packaging Market refers to the industry focused on the design, development, and production of LED packaging solutions within the Asia-Pacific region. LED packaging involves encapsulating LED chips to protect them from environmental factors, enhance performance, and enable integration into various applications.

The Asia Pacific LED Packaging Market Report is Segmented by Packaging Architecture (Surface Mount Device, Chip-on-Board, Chip Scale Package, Flip-Chip LED Packages, Dual In-line Package, and Others), Power Class (Low Power, Mid Power, High Power, and Ultra-High Power), Emission Type (Visible LED Packages, Infrared LED Packages, and Ultraviolet LED Packages), Material Chemistry (Substrates, Encapsulation, Bonding and Die-Attach, and Phosphors and Coatings), Application (General Lighting, Automotive Lighting, Display and Backlighting, Consumer Electronics, and Industrial and Specialty), and Geography (China, Japan, India, Southeast Asia, and Rest of Asia-Pacific). The Market Forecasts are Provided in USD.

By Packaging Architecture

| Surface Mount Device (SMD) |

| Chip-on-Board (COB) |

| Chip Scale Package (CSP) |

| Flip-Chip LED Packages |

| Dual In-line Package (DIP / Through-hole) |

| Others, Packaging Architecture |

By Power Class

| Low Power (Less than 0.5 W) |

| Mid Power (0.5-1 W) |

| High Power (1-3 W) |

| Ultra-High Power (More than 3 W) |

By Emission Type

| Visible LED Packages |

| Infrared LED Packages |

| Ultraviolet LED Packages |

By Material Chemistry

| Substrates |

| Encapsulation |

| Bonding / Die-Attach |

| Phosphors / Coatings |

By Application

| General Lighting |

| Automotive Lighting |

| Display and Backlighting |

| Consumer Electronics |

| Industrial and Specialty |

By Geography

| China |

| Japan |

| India |

| Southeast Asia |

| Rest of Asia-Pacific |

| By Packaging Architecture | Surface Mount Device (SMD) |

| Chip-on-Board (COB) | |

| Chip Scale Package (CSP) | |

| Flip-Chip LED Packages | |

| Dual In-line Package (DIP / Through-hole) | |

| Others, Packaging Architecture | |

| By Power Class | Low Power (Less than 0.5 W) |

| Mid Power (0.5-1 W) | |

| High Power (1-3 W) | |

| Ultra-High Power (More than 3 W) | |

| By Emission Type | Visible LED Packages |

| Infrared LED Packages | |

| Ultraviolet LED Packages | |

| By Material Chemistry | Substrates |

| Encapsulation | |

| Bonding / Die-Attach | |

| Phosphors / Coatings | |

| By Application | General Lighting |

| Automotive Lighting | |

| Display and Backlighting | |

| Consumer Electronics | |

| Industrial and Specialty | |

| By Geography | China |

| Japan | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the projected value of Asia Pacific LED packaging by 2031?

It is forecast to reach USD 12.55 billion by 2031, expanding at a 5.66% CAGR from 2026.

Which segment is expanding fastest within regional LED packaging?

Automotive lighting shows the highest 5.91% CAGR, driven by adaptive-beam headlamps and cockpit displays.

How much of the 2025 market did Surface Mount Device packages hold?

SMDs accounted for 43.75% of revenue in 2025.

Why are Chip Scale Packages gaining share?

Flip-chip CSPs remove submounts, lower system cost and improve thermal paths, enabling 6.28% CAGR growth.

Which country is showing the fastest geographic growth rate?

India leads with a projected 5.87% CAGR through 2031, supported by production-linked incentives and localization programs.

Page last updated on: