Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

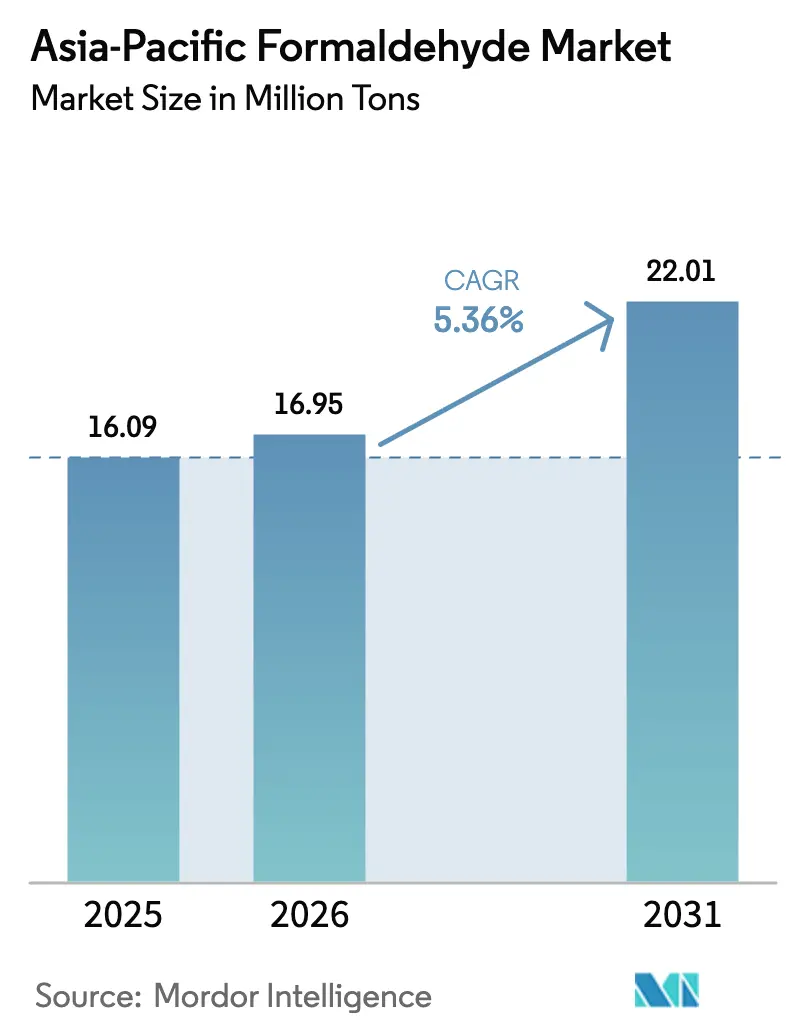

| Base Year Market Size (2025) | 16.09 Million tons |

| Market Volume (2026) | 16.95 Million tons |

| Market Volume (2031) | 22.01 Million tons |

| Growth Rate (2026 - 2031) | 5.36% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Formaldehyde Market Analysis by Mordor Intelligence

The Asia-Pacific Formaldehyde Market size is expected to grow from 16.09 Million tons in 2025 to 16.95 Million tons in 2026 and is forecast to reach 22.01 Million tons by 2031 at 5.36% CAGR over 2026-2031. Robust panel-board production, sustained residential and infrastructure spending, and the steady electrification of vehicle platforms keep demand on an expansionary path, even as regulators tighten emission ceilings. Capacity additions in China and India continue, yet feedstock volatility linked to methanol-to-olefins integration inflates raw-material costs and compresses margins for non-integrated producers. Automotive applications, especially polyoxymethylene (POM) used in precision gears and interior trim, are growing faster than construction, while phenolic resins gain ground in fire-retardant laminates that satisfy stricter building codes. Competitive intensity remains moderate because global majors rely on technology leadership and integrated supply chains, whereas smaller regional players differentiate on cost and proximity to panel clusters. Evolving procurement policies that require renewable electricity and low-emission resins present both a compliance burden and a route to secure premium contracts.

Key Report Takeaways

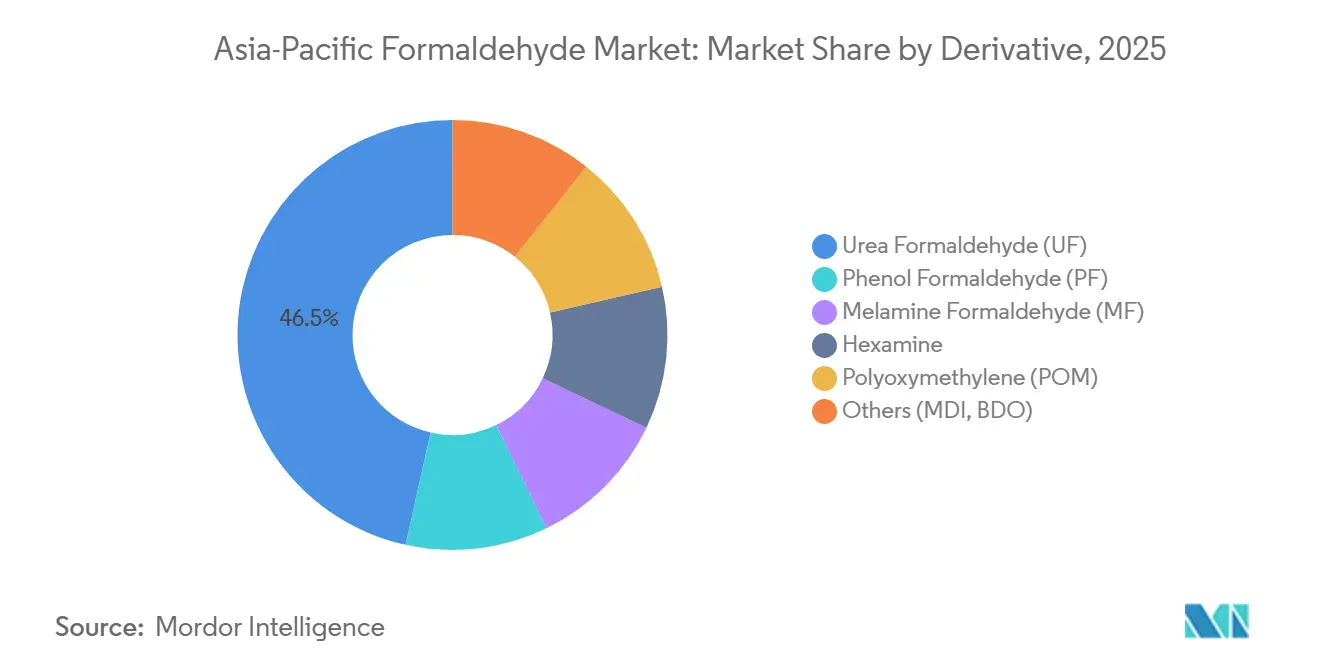

- By derivative, urea formaldehyde led with 46.50% Asia-Pacific formaldehyde market share in 2025, while polyoxymethylene is advancing at a 6.9% CAGR through 2031.

- By end-user industry, construction accounted for 38.47% of the Asia-Pacific formaldehyde market size in 2025; automotive is projected to expand at a 6.18% CAGR between 2026–2031.

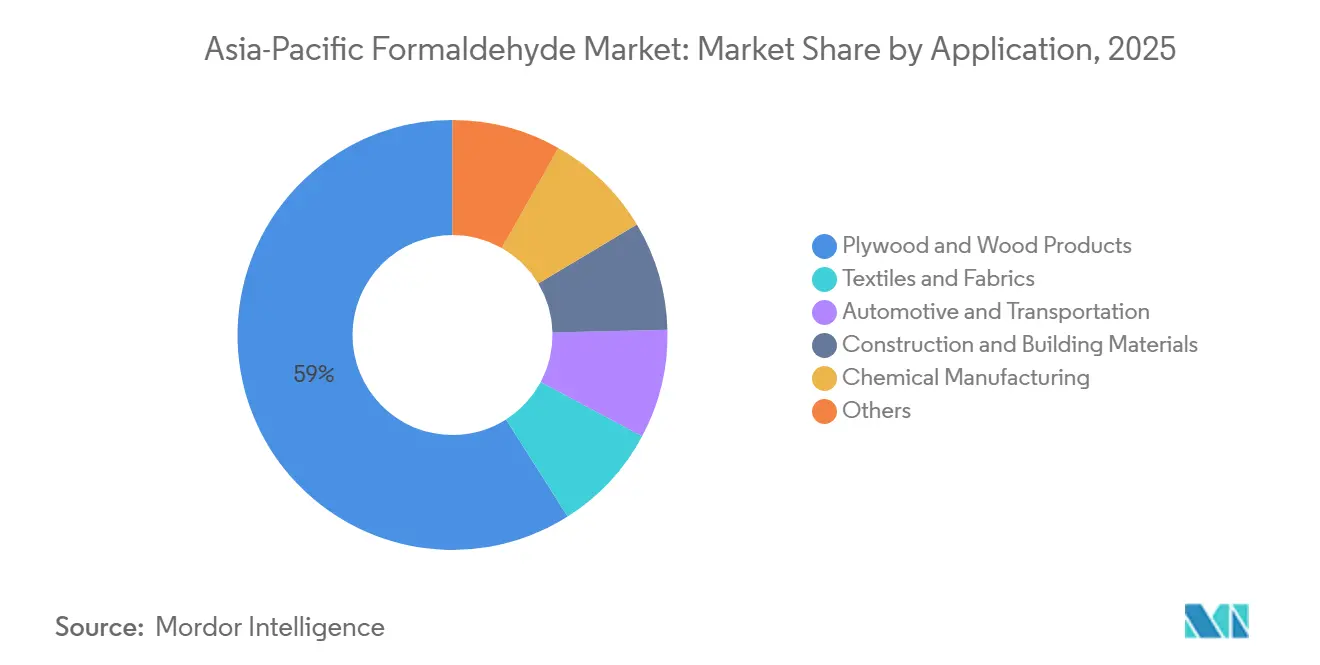

- By application, plywood and wood products captured 58.99% of the Asia-Pacific formaldehyde market size in 2025 and are forecast to grow at 6.05% annually to 2031.

- By geography, China retained 52.41% of the Asia-Pacific formaldehyde market share in 2025, whereas India is set to log the fastest 6.27% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Formaldehyde Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand from construction composites | +1.2% | China, India, Southeast Asia | Medium term (2-4 years) |

| Expanding automotive plastics and coatings adoption | +0.8% | China, Japan, South Korea, India | Long term (≥4 years) |

| Surge in engineered-wood (MDF/particleboard) output | +1.5% | China, India, Vietnam, Malaysia, Thailand | Short term (≤2 years) |

| Growth of UF/PF resin usage in furniture adhesives | +1.0% | Core APAC, Middle East spill-over | Medium term (2-4 years) |

| Methanol-to-olefins integration boosting captive demand | +0.6% | China, limited India | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Demand From Construction Composites

India and China continue to channel infrastructure capex into bridges, metro corridors, and data centers. Formaldehyde-based phenol resins dominate plywood used for exterior cladding because they tolerate monsoon humidity and seismic stress. India’s plywood output rose 6.71% year-on-year in FY 2024, underpinned by a five-year 6.00% CAGR, yet MDF and particleboard still hold only 20% domestic share, leaving headroom for resin consumption growth[1]Indian Brand Equity Foundation, “Wood Panel Industry Trends,” ibef.org. Luxury housing transactions in India climbed 37.8% between January–September 2024, lifting demand for low-emission laminates that comply with emerging indoor-air standards. China produced more than 250 million m³ of wood-based panels in 2023, locking in sustained adhesive demand, while public-housing specifications already require ENF-grade products.

Expanding Automotive Plastics And Coatings Adoption

Electric-vehicle (EV) assembly is redirecting derivatives toward POM and phenolic composites that satisfy stringent cabin-air protocols. BASF raised Asia-Pacific Ultraform POM prices by USD 350/t in March 2025 to offset energy and freight inflation and continued compliance spending. Japan Automobile Manufacturers Association limits cabin formaldehyde to 100 µg m⁻³, a threshold now mirrored across ASEAN sourcing contracts. Hybrid powertrains also accelerate phenolic resin uptake in brake pads and clutch facings that require heat stability.

Surge In Engineered-Wood Output

Regional MDF capacity outpaces near-term demand, trimming resin prices but consolidating long-run formaldehyde volumes. India lifted MDF nameplate capacity to 4.5 million m³ by FY 2025 and expects oversupply until FY 2027 when modular-furniture exports scale. Vietnam launched an anti-dumping probe into Thai and Chinese fiberboard, favoring local mills that purchase domestic UF resin grades. Malaysia’s MS 2750:2021 forces mills to retrofit scavengers or buy low-emission UF grades, intensifying near-term resin demand.

Growth Of UF/PF Resin Usage In Furniture Adhesives

UF maintains cost leadership in interior-grade boards, while PF garners a share in moisture-resistant outdoor furniture. UF represents roughly 70% of global wood-panel adhesives, and Asia-Pacific exceeds 60% of global melamine-formaldehyde consumption due to laminate exports. Hexion introduced ENF-compliant UF systems in March 2023 and expanded MF capacity to serve Chinese laminate lines. Biomass-balanced amino resins developed by BASF and SWISS KRONO trim cradle-to-gate carbon footprints 30%, giving producers an ESG premium.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Toxic and carcinogenic classification tightening exposure limits | -0.4% | Global, stricter in Japan, Singapore, EU exports | Short term (≤2 years) |

| Stringent APAC environmental regulations and emission caps | -0.5% | China, Singapore, Malaysia, Vietnam | Medium term (2-4 years) |

| Shift toward formaldehyde-free resins in wood panels | -0.3% | China, India, Japan, export-oriented ASEAN | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Toxic And Carcinogenic Classification Tightening Exposure Limits

Singapore bans formaldehyde in interior paints from 2026, capping content at 0.01 wt%, which pushes formulators toward acrylic and silicone binders[2]Singapore Statutes Online, “Environmental Protection and Management Act,” sso.agc.gov.sg. Japan’s Building Standard Law demands F4 board ratings of ≤0.04 mg m⁻³, while vehicle makers limit cabin exposure to 100 µg m⁻³, forcing resin upgrades. China’s GB/T 39600-2021 added an ENF tier at ≤0.025 mg m⁻³, and typical adhesive retrofits cost USD 1.2 million per panel plant. Compliance erodes smaller mills’ margins and accelerates substitution by melamine-urea or phenolic alternatives.

Stringent APAC Environmental Regulations And Emission Caps

The Chinese Air Pollution Prevention and Control Law allows winter output curbs for non-compliant aldehyde facilities, throttling supply during peak heating seasons. Malaysia’s MS 2750:2021 harmonizes emission thresholds with CARB and ENF norms, reshaping procurement toward low-emission UF. Vietnam’s anti-dumping probe on imported fiberboards indirectly compels domestic mills to upgrade their environmental footprints to remain competitive.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Derivative: UF Dominance Masks POM And Hexamine Upside

Urea formaldehyde contributed 46.50% of Asia-Pacific formaldehyde market share in 2025, reflecting its low unit cost in particleboard and MDF lines. The sub-segment is forecast to advance at a 5.97% CAGR through 2031, keeping absolute volume leadership despite regulatory headwinds. Polyoxymethylene demand is propelled by EV interior and precision gear demand that tracks a near 7% CAGR. Phenol formaldehyde gains niche adoption in fire-resistant plywood favored in metro and data-center builds, while melamine formaldehyde caters to decorative laminates where scratch resistance commands a price premium.

Technological upgrades in UF enable ENF-grade panels without sacrificing press throughput, mitigating substitution risk. Hexamine retains importance in explosives and veterinary applications but faces gradual displacement in fuel tablets. BASF’s 2025 renewable-powered Zhanjiang unit and Hexion’s ENF-compliant UF lines illustrate how global suppliers pivot toward low-emission chemistries aligned with China’s standards. Concurrently, in-house formaldehyde capacity integrated into MDI routes anchors captive demand obscured from headline statistics.

By End-User Industry: Automotive Outpaces Construction In Growth

Construction absorbed 38.47% of regional formaldehyde volume in 2025 and still lifts aggregate demand as India and ASEAN deploy infrastructure stimulus. Yet automotive is set to grow faster at 6.18% CAGR, driven by POM’s penetration in battery-electric vehicle (BEV) coolant blocks and autonomous-driving sensor housings. India’s formaldehyde-based laminate uptake rises with modular kitchen installations, while Japan’s cabin-air limits accelerate low-emission resin migration into supply contracts. Agriculture’s share contracts as propionic-acid preservatives displace hexamine, and healthcare remains a niche consumer amid rising non-aldehyde sterilant usage.

Beyond OEM demand, aftermarket brake components and clutch facings increasingly specify phenolic resins for thermal stability, an opportunity regional compounders exploit by expanding PF production in South Korea. Formaldehyde-based chemical intermediates such as pentaerythritol and methylenedianiline keep the petrochemical segment relevant, especially where integrated players leverage steam and waste-heat networks to minimize variable costs.

By Application: Plywood And Wood Products Sustain Volume Leadership

Plywood and wood products represented 58.99% of Asia-Pacific formaldehyde market size in 2025 and could grow 6.05% annually to 2031 on the back of sustained panel exports. Overcapacity dampens resin pricing but secures long-term volume as India, Vietnam, and Thailand scale production. Automotive and transportation applications clock above-average growth because BEV designs rely on lightweight POM rails and phenolic brake pads to offset battery mass. Textiles gradually migrate toward citric-acid cross-linkers, but melamine formaldehyde persists in wrinkle-free finishes for workwear exported from Bangladesh and Indonesia.

Construction and building materials outside the wood domain - phenolic foam boards, fire-retardant coatings - show mid-single-digit growth, benefiting from green-building codes. Chemical manufacturing demand remains steady as Celanese’s Acetyl Chain division reported 11% volume gains in Q1 2024, anchored in Asia-Pacific clients. Remaining end-uses such as disinfectants and agricultural additives hold below-10% share and face substitution headwinds.

Geography Analysis

China retained 52.41% share of Asia-Pacific formaldehyde market volume in 2025, anchored in its 250 million m³ wood-panel output and 30.58 million tons per year propane-dehydrogenation capacity that tightens methanol supply. Policy dictates, such as GB/T 39600-2021 and winter smog controls, drive resin reformulations and capex for scrubbers, favoring large integrated sites that achieve compliance economies. Wanhua Chemical’s 240 kt/y Ningbo formaldehyde block aligns with downstream MDI units to capture heat integration and feedstock flexibility.

India, expected to post a 6.27% CAGR through 2031, leverages public housing, fast-growing modular furniture, and aggressive road building to soak up UF and PF volumes. Kanoria Chemicals’ 345 tons per day expansion and ARCL Organics’ 44.8% formaldehyde revenue share highlight domestic capacity additions. Draft emission standards under the Ministry of Chemicals and Fertilizers will harmonize with CARB norms, encouraging investments in low-emission resin technologies.

Japan, South Korea, Malaysia, Thailand, Indonesia, and Vietnam collectively fill the balance. Japan’s F4 rating and JAMA cabin-air guidelines make it a premium low-emission market; Mitsubishi Gas Chemical labels formalin as “business requiring intensive management,” hinting at potential restructuring. South Korea’s mature construction sector caps panel growth but bolsters POM usage in advanced drivetrains. Malaysia’s MS 2750 and downstream guidelines spur resin upgrades, while Vietnam’s anti-dumping probe may redirect fiberboard demand to domestic adhesive suppliers. Smaller South Asian markets remain import-reliant yet show sporadic demand spikes tied to industrial estate rollout.

Competitive Landscape

The Asia-Pacific formaldehyde market remains moderately fragmented. Strategic levers include backward integration into methanol, forward linkages to derivatives, and geographical expansion toward India and Southeast Asia, where infrastructure drives resin uptake. Wanhua Chemical’s Ningbo complex exemplifies end-to-end integration, lowering unit costs 8–12% via waste-heat recovery. White-space opportunities span CO₂-derived methanol routes, lignin-based adhesives, and ENF-grade UF variants with no cure-cycle penalty. Compliance technology, such as real-time emission monitors and catalytic oxidizers, differentiates top-tier producers, whereas smaller mills rely on dilution tactics that risk shutdown under tighter air-quality rules.

Asia-Pacific Formaldehyde Industry Leaders

BASF SE

Hexion

Mitsubishi Gas Chemical Company, Inc.

Perstorp

Kanoria Chemicals & Industries Ltd (KCI)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Kanoria Chemicals unveiled a 345 t d formaldehyde expansion worth INR 56.06 crore (~USD 6.7 million) using Metal Oxide technology aimed at India’s impending composite-wood standards.

- March 2023: Hexion introduced low-emission UF resins engineered for China’s ENF tier and enlarged melamine-formaldehyde capacity across Asia to serve laminate exporters.

Asia-Pacific Formaldehyde Market Report Scope

Formaldehyde, a colorless and highly reactive gas with a pungent odor, is produced through the catalytic oxidation of methanol. This flammable gas is a crucial precursor for various materials and chemical compounds. Its versatile and advantageous properties have led to its widespread use across numerous applications.

The Asia-Pacific formaldehyde market is segmented by derivative, end-user industry, application, and geography. By derivative, the market is segmented into urea formaldehyde, phenol formaldehyde, melamine formaldehyde, hexamine, polyoxymethylene, and others. By end-user industry, the market is segmented into construction, automotive, agriculture, healthcare, chemical and petrochemical, and other end-user industries (paints and textiles). By application, the market is segmented into plywood and wood products, textiles and fabrics, automotive and transportation, construction and building materials, chemical manufacturing, and others. The report also covers the market size and forecasts for the formaldehyde market in eight major countries across the Asia-Pacific. For each segment, the market sizing and forecasts have been done on the basis of volume (Tons).

By Derivative

| Urea Formaldehyde (UF) |

| Phenol Formaldehyde (PF) |

| Melamine Formaldehyde (MF) |

| Hexamine |

| Polyoxymethylene (POM) |

| Others (MDI, BDO) |

By End-user Industry

| Construction |

| Automotive |

| Agriculture |

| Healthcare |

| Chemical and Petrochemical |

| Other End-User Industries (Paints and Textiles) |

By Application

| Plywood and Wood Products |

| Textiles and Fabrics |

| Automotive and Transportation |

| Construction and Building Materials |

| Chemical Manufacturing |

| Others |

By Geography

| China |

| India |

| Japan |

| South Korea |

| Malaysia |

| Thailand |

| Indonesia |

| Vietnam |

| Rest of Asia-Pacific |

| By Derivative | Urea Formaldehyde (UF) |

| Phenol Formaldehyde (PF) | |

| Melamine Formaldehyde (MF) | |

| Hexamine | |

| Polyoxymethylene (POM) | |

| Others (MDI, BDO) | |

| By End-user Industry | Construction |

| Automotive | |

| Agriculture | |

| Healthcare | |

| Chemical and Petrochemical | |

| Other End-User Industries (Paints and Textiles) | |

| By Application | Plywood and Wood Products |

| Textiles and Fabrics | |

| Automotive and Transportation | |

| Construction and Building Materials | |

| Chemical Manufacturing | |

| Others | |

| By Geography | China |

| India | |

| Japan | |

| South Korea | |

| Malaysia | |

| Thailand | |

| Indonesia | |

| Vietnam | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the projected demand for formaldehyde in the Asia-Pacific by 2031?

Formaldehyde consumption in the Asia-Pacific is forecast to reach 22.01 million tons by 2031, reflecting a 5.36% CAGR over 2026–2031.

Which derivative will dominate volume through 2031?

Urea formaldehyde will remain the largest derivative, retaining close to half of regional volume on cost advantages in MDF and particleboard lines.

Why is automotive the fastest-growing end-user segment?

Electric-vehicle production boosts polyoxymethylene and phenolic resin usage for lightweight, low-VOC components, driving a 6.18% CAGR in automotive consumption.

How are regulations shaping product development?

Standards such as China’s GB/T 39600-2021 ENF tier and Japan’s F☆☆☆☆ board rating compel producers to invest in low-emission UF and PF technologies.

Which country offers the highest growth potential?

India is forecast to expand at a 6.27% CAGR to 2031, supported by infrastructure spending, formal housing initiatives, and new resin capacity additions.

Page last updated on: