Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

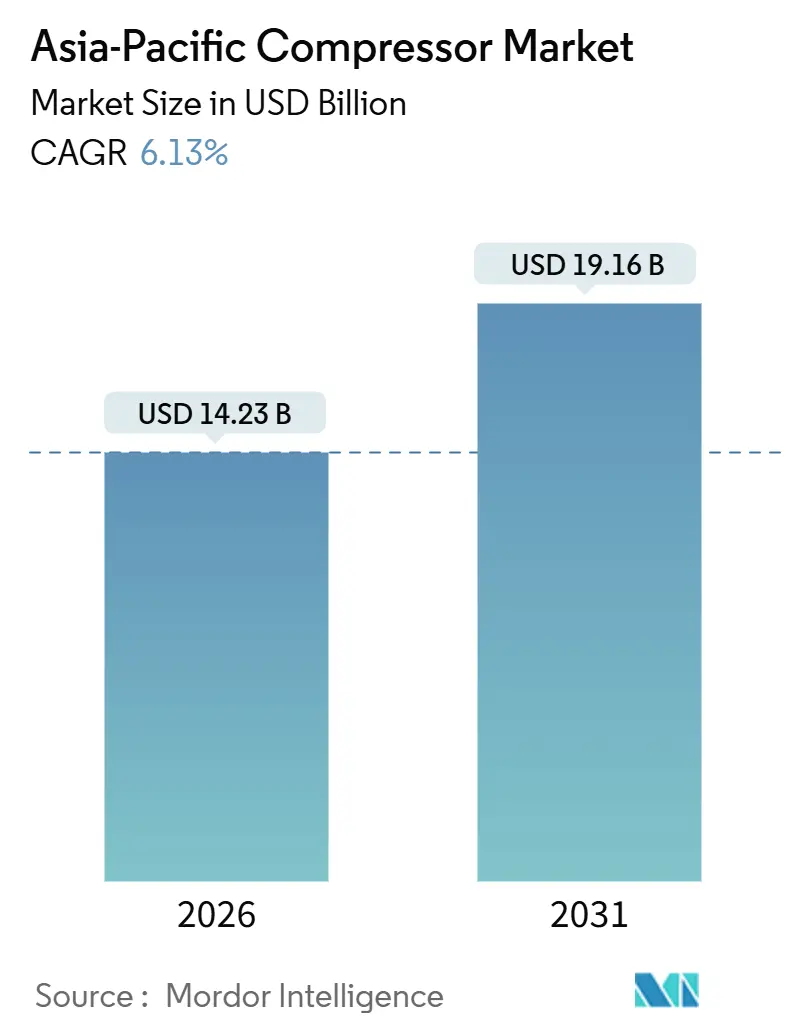

| Market Size (2026) | USD 14.23 Billion |

| Market Size (2031) | USD 19.16 Billion |

| Growth Rate (2026 - 2031) | 6.13% CAGR |

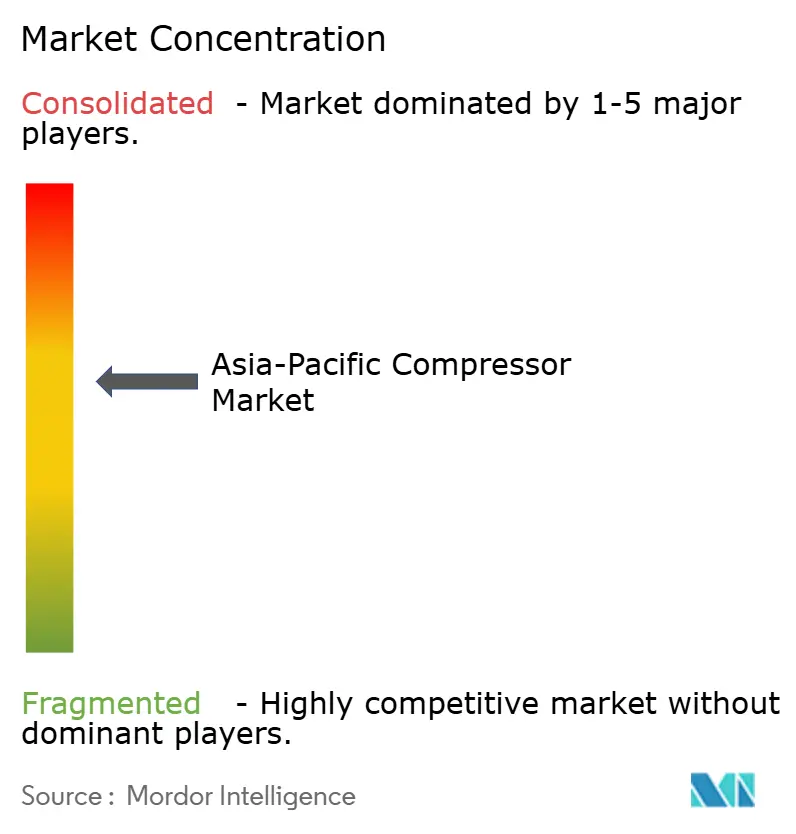

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Compressor Market Analysis by Mordor Intelligence

The Asia-Pacific Compressor Market size is estimated at USD 14.23 billion in 2026, and is expected to reach USD 19.16 billion by 2031, at a CAGR of 6.13% during the forecast period (2026-2031).

Demand is rising on the back of rapid industrialization, increasingly stringent energy-efficiency mandates, and a wave of LNG, hydrogen, and cold-chain infrastructure projects. The Asia-Pacific compressor market is also benefiting from policy-linked manufacturing corridors in India, Belt and Road construction in China, and a region-wide push toward variable-speed-drive (VSD) technologies that curb electricity consumption. Meanwhile, European and North American original-equipment manufacturers (OEMs) are localizing assembly and service footprints to counter tariff headwinds, while domestic champions exploit cost advantages in price-sensitive niches. Medium-pressure systems dominate day-to-day industrial loads, yet low-pressure compressors tied to HVAC-R and cold-chain growth are advancing fastest, mirroring the region’s rising middle-class spending power.

Key Report Takeaways

- By type, positive displacement captured 67.8% revenue share in 2025, while dynamic units are forecast to expand at a 6.5% CAGR through 2031.

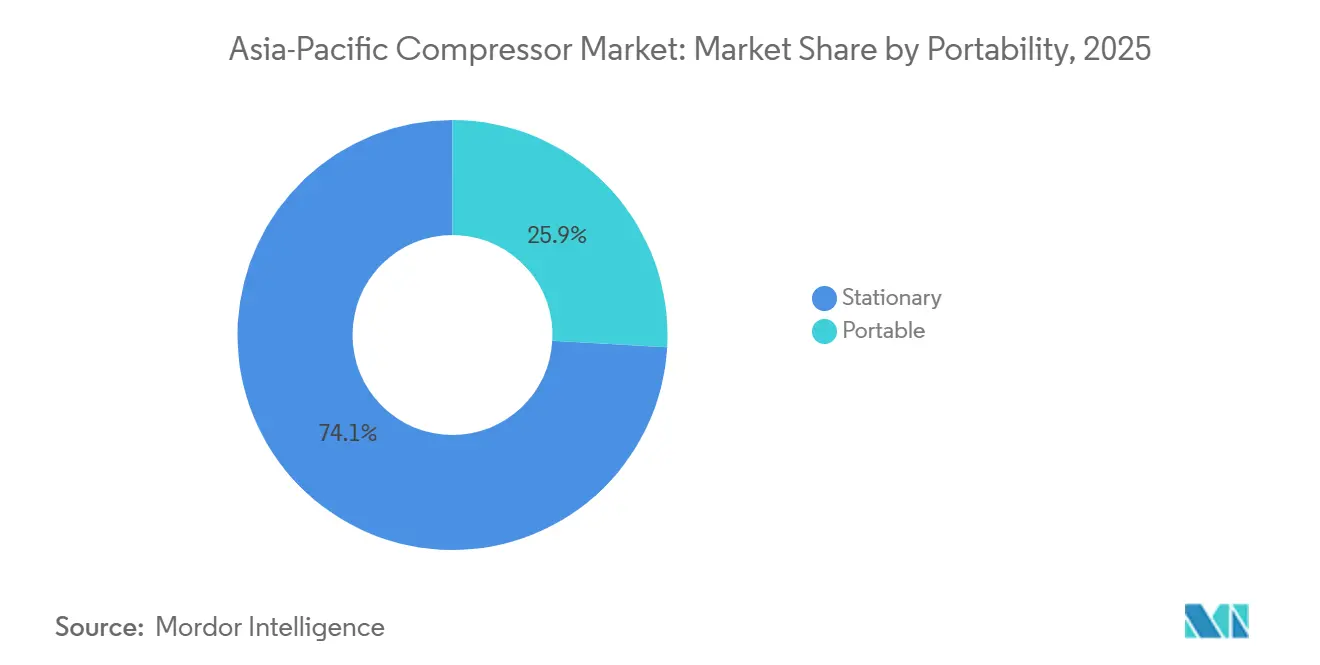

- By portability, stationary installations held 74.1% of demand in 2025; portable counterparts are growing at a 7.2% CAGR, led by infrastructure and mining projects.

- By pressure rating, medium-pressure systems accounted for 49.5% of the Asia-Pacific compressor market size in 2025; low-pressure units are advancing at an 8.0% CAGR to 2031.

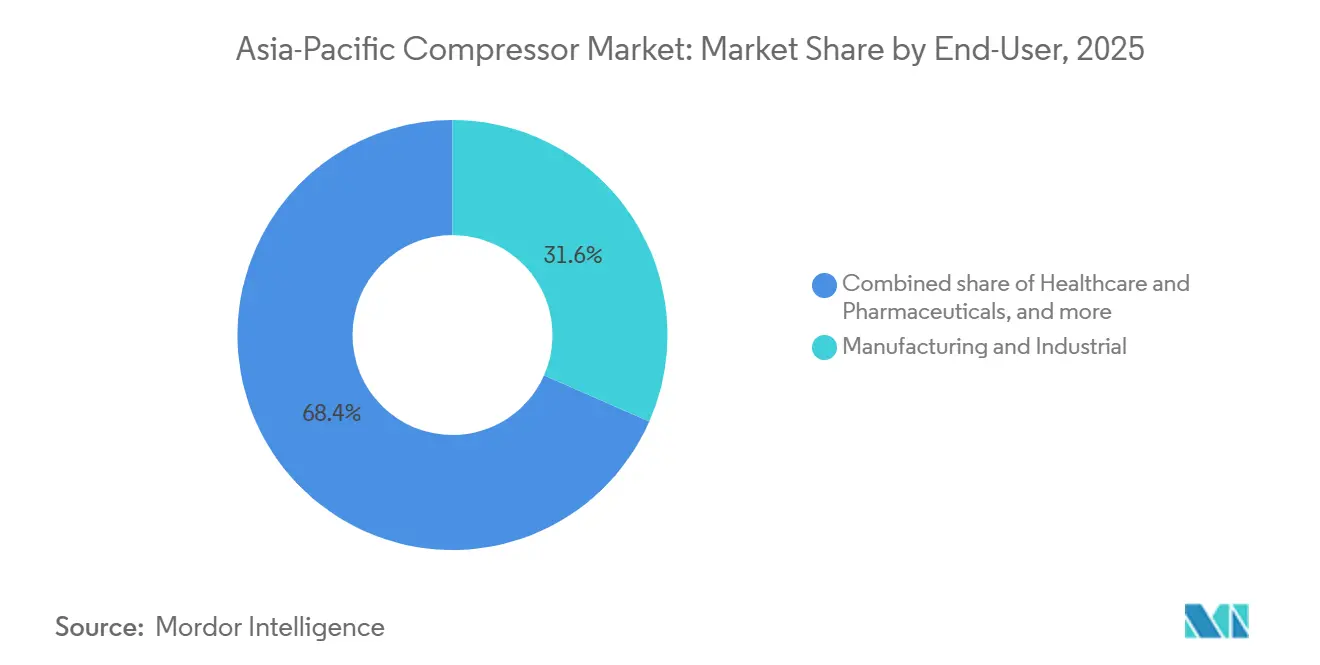

- By end-user, manufacturing led end-user adoption with 31.6% of the Asia-Pacific compressor market share in 2025, but healthcare and pharmaceuticals are rising at an 8.8% CAGR.

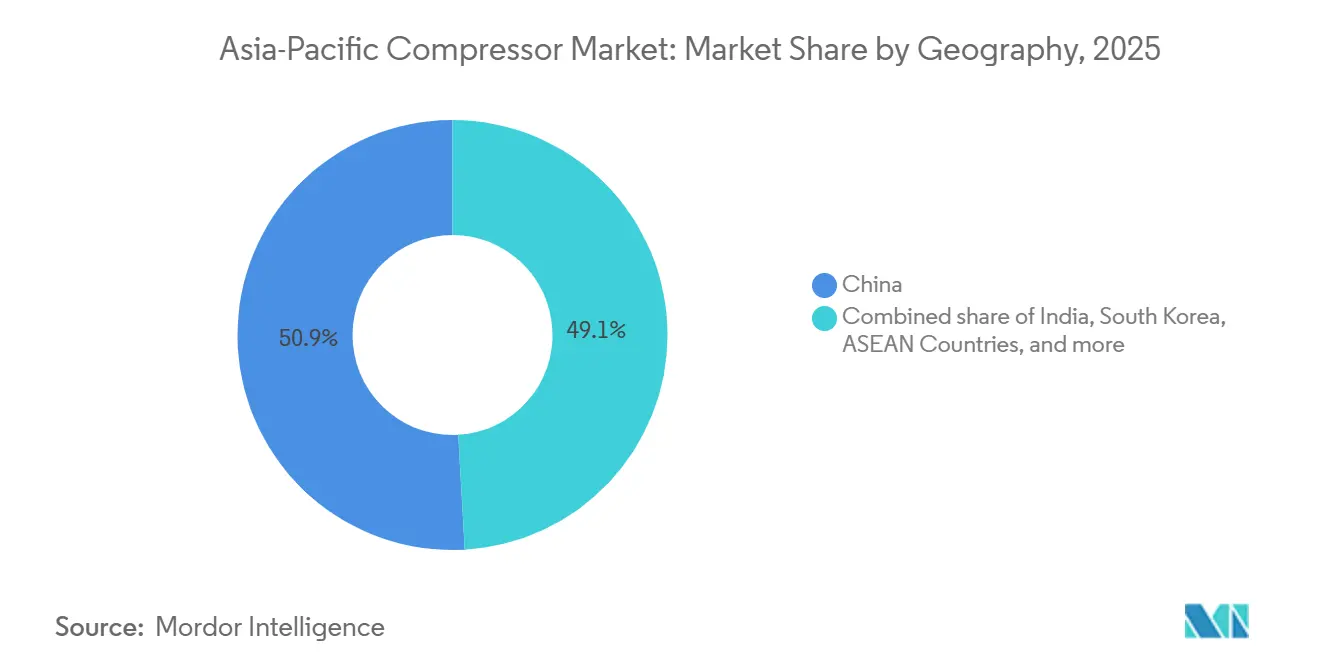

- By geography, China commanded a 50.9% share in 2025; India is the fastest-growing geography at a 6.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Compressor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid industrialization & manufacturing expansion | +1.8% | China, India, ASEAN (Vietnam, Thailand, Indonesia) | Medium term (2-4 years) |

| Stringent energy-efficiency regulations favouring rotary-screw & VSD units | +1.2% | Singapore, Australia, Japan, South Korea, with spillover to Malaysia and Vietnam | Long term (≥4 years) |

| LNG & gas-pipeline build-out boosting high-pressure gas compressors | +1.0% | China, India, Indonesia, Australia | Medium term (2-4 years) |

| Hydrogen infrastructure roll-out requiring specialty H₂ compressors | +0.6% | Japan, South Korea, Australia, Singapore | Long term (≥4 years) |

| Digital service contracts & predictive-maintenance platforms | +0.5% | Global, with early adoption in Japan, South Korea, Australia | Medium term (2-4 years) |

| Surging HVAC & cold-chain demand among APAC middle class | +0.9% | India, ASEAN, China tier-2 and tier-3 cities | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rapid Industrialization & Manufacturing Expansion

China delivered about 30% of global manufacturing value-added in 2025, while India’s production-linked incentive program earmarked INR 6,940 crore (USD 830 million) for air-conditioner and LED lines, spurring orders for rotary-screw and reciprocating units.[1] Press Information Bureau, “PLI Scheme for White Goods,” pib.gov.in ASEAN economies attracted USD 224 billion in foreign direct investment in 2024, with Vietnam and Thailand commissioning new electronics and automotive parks that require compressed-air networks.[2]Asian Development Bank, “ASEAN FDI Statistics,” adb.org India’s Delhi–Mumbai and Chennai–Bengaluru corridors embed VSD standards that trigger a replacement cycle away from fixed-speed machines. Higher-value manufacturing, semiconductors, EV batteries, and biologics demand oil-free and centrifugal designs with tighter tolerances. Stabilizing steel output but rising aluminum and copper smelting in Indonesia and India further lift multi-megawatt centrifugal demand.

Stringent Energy-Efficiency Regulations Favouring Rotary-Screw & VSD Units

Singapore enforced Minimum Energy Performance Standards for industrial compressors in 2024, mandating efficiency labels and phasing out low-performance models. Vietnam’s 2025 building-code revision requires heat-recovery HVAC systems built around VSD compressors. Australia’s Safeguard Mechanism penalizes high-emission facilities, accelerating rotary-screw upgrades that cut electricity use 20–30%. Japan’s Top Runner program and South Korea’s Green New Deal keep tightening benchmarks, while Malaysia’s energy-efficiency plan targets a 10% cut in industrial intensity by 2030. Across the Asia-Pacific compressor market, payback periods of 18–24 months for VSD retrofits are catalyzing small- and mid-size enterprise adoption.

LNG & Gas-Pipeline Build-Out Boosting High-Pressure Gas Compressors

Indonesia’s PLN brought the Arun LNG terminal online in 2024, installing high-pressure reciprocating packages to boost regasified gas into pipelines. Vietnam’s PetroVietnam Gas ordered centrifugal boil-off units above 100 bar for two floating regasification vessels in 2025. South Korea’s Incheon expansion and India’s 15% pipeline extension both relied on fresh high-pressure trains. The IEA projects an 80 million-tonne jump in regional LNG import capacity by 2030, translating into roughly 200 new compressor installations.[3] International Energy Agency, “Gas 2025,” iea.org

Hydrogen Infrastructure Roll-Out Requiring Specialty H₂ Compressors

Kawasaki Heavy Industries commissioned a 700-bar pilot compressor in 2025, while Hyundai deployed multi-stage hydrogen stations across Seoul and Busan. Australia’s Woodside H2Perth and Fortescue Pilbara projects will require ultra-high-pressure systems above 300 bar. Singapore’s Jurong Island hydrogen import terminal plan includes cryogenic and high-pressure compression trains. Japan’s NEDO committed USD 500 million to hydrogen supply-chain pilots, identifying compressor reliability as a bottleneck. These ventures create a premium, high-margin niche within the Asia-Pacific compressor market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront cost of oil-free & VSD compressors | -0.7% | India, ASEAN, China tier-2 and tier-3 cities | Short term (≤2 years) |

| Raw-material price volatility squeezing OEM margins | -0.5% | Global, with acute impact on China and India manufacturing hubs | Medium term (2-4 years) |

| Shortage of skilled technicians for advanced systems | -0.4% | India, ASEAN, Australia regional centers | Medium term (2-4 years) |

| Rising rental penetration dampening new-unit sales | -0.3% | Australia, New Zealand, ASEAN construction corridors | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Upfront Cost of Oil-Free & VSD Compressors

Oil-free rotary-screw machines command a 40–60% premium over lubricated alternatives, while VSD packages add 15–25%, deterring small enterprises in India, Indonesia, and Vietnam. Total cost of ownership favors premium units in contamination-sensitive settings, yet many users defer upgrades until failures occur. Kirloskar Pneumatic reported that 60% of oil-free inquiries did not convert within 12 months, citing budget constraints. Entry-level oil-free 50-hp screws list at USD 25,000 against USD 15,000 for lubricated peers, a delta many small workshops struggle to justify. “Air-as-a-service” leasing softens capex but remains under 10% penetration across the Asia-Pacific compressor market.

Raw-Material Price Volatility Squeezing OEM Margins

Copper oscillated between USD 8,500 and USD 10,200 per tonne in 2024, and hot-rolled coil swung from USD 550 to USD 720, cutting gross margins 200–300 basis points. Aluminum premiums stayed elevated because of energy costs, and nickel prices remained volatile amid Indonesian export curbs, inflating stainless-steel input costs. Atlas Copco disclosed a 1.2-point margin hit in its 2024 Asia-Pacific business, driving a pivot toward material-light modular designs.[4]Atlas Copco, “Annual Report 2024,” atlascopco.com Smaller regional producers lack hedging capacity, leaving them doubly exposed to spikes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Positive Displacement Dominates, Dynamic Gains in Large-Scale Projects

Positive displacement machines controlled 67.8% of the Asia-Pacific compressor market in 2025, buoyed by rotary-screw and reciprocating uptake across factory floors and gas-gathering fields. Dynamic compressors, led by centrifugal designs, are forecast to grow at a 6.5% CAGR as petrochemical and LNG investments proliferate. The Asia-Pacific compressor market size for dynamic units is projected to widen alongside ethylene crackers and ammonia loops that favor multi-megawatt centrifugal trains. Magnetic-bearing systems from Mitsubishi Heavy Industries and Siemens trim operating costs up to 40% over two decades. Variable-speed screws are narrowing the efficiency gap with dynamics, while rotary-vane machines find cleanroom niches where ISO 8573-1 Class 0 purity is mandatory.

Digital twins lengthen service intervals for reciprocating models, and Hitachi’s hybrid screw with embedded sensors cuts automotive paint-shop energy by 15%. Collectively, these innovations underscore how the Asia-Pacific compressor market continues to blur traditional boundaries between displacement and dynamic classes.

By Portability: Stationary Units Anchor Industrial Base, Portable Grows with Infrastructure Boom

Stationary equipment represented 74.1% of 2025 demand, integrated into centralized factory and refinery grids. Portable units, however, are expanding at a 7.2% CAGR, leveraged by expressways, rail, and mining sites across India, Vietnam, and Australia. Contractors increasingly rent compressors to avoid capex, accelerating fleet turnover at rental houses and lifting service-parts revenue. The Asia-Pacific compressor market share for stationary units will remain dominant, yet incremental gains accrue to battery-electric portables, which address urban noise and emission curbs. Kaeser’s lithium-ion model, launched in 2024, targets CBD projects in Singapore and Hong Kong with 4–6 hours of runtime.

By Pressure Rating: Medium Pressure Leads, Low Pressure Surges with HVAC Demand

Medium-pressure compressors (20–100 bar) held a 49.5% share in 2025, serving mainstream industrial pneumatics, assembly lines, and moderate oil-and-gas tasks. Low-pressure systems, however, are slated to post an 8.0% CAGR through 2031, reflecting triple-digit growth in residential and commercial cooling loads as air-conditioner ownership multiplies. The Asia-Pacific compressor market size for low-pressure applications is swelling within cold-chain logistics, where refrigerated warehouse space rose by 2.5 million m² in 2024. High-pressure and ultra-high-pressure tiers remain smaller but are essential to CNG and hydrogen refueling networks.

By End-User: Manufacturing Dominates, Healthcare Accelerates with Cleanroom Expansions

Manufacturing contributed 31.6% of 2025 revenue, anchored by automotive, electronics, and metal-working plants. Healthcare and pharmaceuticals stand out as the fastest-growing adopters, expanding at an 8.8% CAGR as biologics and sterile-injectable facilities multiply across India, China, and Singapore. The Asia-Pacific compressor industry is witnessing a pivot toward ISO 8573-1 Class 0 oil-free solutions that eliminate contamination risk in GMP suites. Meanwhile, oil-and-gas, power generation, and chemicals maintain steady demand for bespoke, high-horsepower packages.

Geography Analysis

China anchored 50.9% of 2025 sales, underwritten by Belt and Road construction and state automation drives. The Asia-Pacific compressor market size in India is expanding at a 6.9% CAGR, catalyzed by production-linked incentives and a 15% city-gas pipeline extension. Japan and South Korea exhibit lower growth yet spearhead hydrogen compression research, exporting magnetic-bearing centrifugal know-how into ASEAN.

Vietnam, Thailand, and Indonesia pulled USD 224 billion of FDI in 2024, funneling rotary-screw and oil-free demand into new electronics, automotive, and food-processing plants. Australia and New Zealand revolve around replacement cycles, but the lithium-mining surge and green-hydrogen pilots in Western Australia are creating premium orders for ultra-high-pressure systems.

Elsewhere, Pakistan, Bangladesh, and Sri Lanka inch forward as textile exporters modernize compressed-air installations to satisfy sustainability audits. Collectively, the Asia-Pacific compressor market remains a tapestry of mature, high-value hubs and frontier growth pockets that command differentiated product and service strategies.

Competitive Landscape

The top five suppliers, Atlas Copco, Ingersoll Rand, Mitsubishi Heavy Industries, Siemens, and Hitachi, control roughly 40-45% of sales, indicating moderate concentration. Local assembly lines, such as Atlas Copco’s 2024 Pune plant, mitigate tariffs and compress lead times. ELGi’s Melbourne service hub trims downtime for Australian mining fleets by delivering parts within 48 hours. Domestic entrants like Kirloskar Pneumatic and Kaishan leverage cost advantages but wrestle with limited access to high-end VSD and IoT modules.

White-space opportunities orbit hydrogen, oil-free retrofits, and digital twins. Burckhardt Compression and Ariel have carved 50-70% price-premium hydrogen niches, while Siemens and Hitachi monetize edge-analytics platforms that slash unplanned downtime 15-20%. SAP’s partnership with Hoerbiger embeds valve diagnostics into its asset network, signaling how data services could eclipse hardware revenue over a 15-year lifecycle. Competitive intensity in the Asia-Pacific compressor market is poised to sharpen as software ecosystems and specialty gases redefine differentiation.

Asia-Pacific Compressor Industry Leaders

Atlas Copco AB

Ingersoll Rand Inc.

Mitsubishi Heavy Industries Ltd

Siemens AG

Hitachi Industrial Equipment Systems Co Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Ingersoll Rand (India) Ltd, a key player in the compressed air and industrial solutions sector, has unveiled its RSbn Nirvana Series Screw Air Compressors in India. Aimed at helping industries cut operating costs and boost energy efficiency, the RSbn Nirvana Series spans from 7 kW to 250 kW.

- January 2026: Horizon Oil Limited has greenlit the final investment for the Nam Phong Booster Compressor Project in onshore Thailand. This strategic upgrade, designed to enhance gas recovery from the newly acquired Nam Phong field, comes at a low cost.

- October 2025: Hitachi Industrial Equipment Systems Co., Ltd. is set to launch its "G Series" oil-free scroll air compressor, featuring models with 1.5kW, 2.2kW, and 3.7kW capacities. These compressors can operate in high ambient temperatures, up to 45°C.

- December 2024: Assam Gas Company Ltd. has awarded Asian Energy Services Ltd. (AEL) a 3-year contract to supply compressor stations. AEL, known for its comprehensive services across the upstream value chain, will operate on a build, own, operate, and transfer (BOOT) basis.

Asia-Pacific Compressor Market Report Scope

A compressor is a mechanical device that increases the pressure of a gas by reducing its volume. Compressors are used throughout the industry to provide instrument air; power air tools, paint sprayers, and abrasive blast equipment; phase shift refrigerants for air conditioning and refrigeration; propel gas through pipelines, etc.

The Asia-Pacific compressor market is segmented by type, portability, pressure rating, end-user, and geography. By type, the market is segmented into positive displacement (reciprocating, rotary screw, rotary vane) and dynamic (centrifugal, axial). By portability, the market is segmented into stationary and portable. By pressure rating, the market is segmented into low, medium, high, and ultra-high. By end-user, the market is segmented into oil and gas, power generation, manufacturing and industrial, chemicals and petrochemicals, HVAC-R and building services, automotive and transportation, food and beverage, and healthcare and pharmaceuticals. The report also covers the market size and forecasts for the Asia-Pacific compressor market across the major countries. For each segment, the market size and forecasts have been done based on revenue (USD).

By Type

| Positive Displacement | Reciprocating |

| Rotary Screw | |

| Rotary Vane | |

| Dynamic | Centrifugal |

| Axial |

By Portability

| Stationary |

| Portable |

By Pressure Rating

| Low (Up to 20 bar) |

| Medium (20 to 100 bar) |

| High (100 to 300 bar) |

| Ultra-High (Above 300 bar) |

By End-User

| Oil and Gas |

| Power Generation |

| Manufacturing and Industrial |

| Chemicals and Petrochemicals |

| HVAC-R and Building Services |

| Automotive and Transportation |

| Food and Beverage |

| Healthcare and Pharmaceuticals |

By Geography

| China |

| India |

| Japan |

| South Korea |

| ASEAN Countries |

| Australia and New Zealand |

| Rest of Asia-Pacific |

| By Type | Positive Displacement | Reciprocating |

| Rotary Screw | ||

| Rotary Vane | ||

| Dynamic | Centrifugal | |

| Axial | ||

| By Portability | Stationary | |

| Portable | ||

| By Pressure Rating | Low (Up to 20 bar) | |

| Medium (20 to 100 bar) | ||

| High (100 to 300 bar) | ||

| Ultra-High (Above 300 bar) | ||

| By End-User | Oil and Gas | |

| Power Generation | ||

| Manufacturing and Industrial | ||

| Chemicals and Petrochemicals | ||

| HVAC-R and Building Services | ||

| Automotive and Transportation | ||

| Food and Beverage | ||

| Healthcare and Pharmaceuticals | ||

| By Geography | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

How large is the Asia-Pacific compressor market in 2026?

The market stood at USD 14.23 billion in 2026 and is projected to reach USD 19.16 billion by 2031, registering a 6.13% CAGR for the period 2026-2031.

Which segment is expanding fastest within the region?

Low-pressure compressors tied to HVAC-R and cold-chain demand are growing at an 8.0% CAGR through 2031.

Why are portable compressors gaining popularity?

Infrastructure, mining, and rental-fleet operators prefer mobile units that eliminate capex and accelerate project timelines.

What drives investment in hydrogen compression?

National hydrogen roadmaps in Japan, South Korea, and Australia require 300-bar-plus systems for refueling and export pipelines.

How are OEMs countering margin pressure from volatile metals prices?

Leading suppliers are adopting modular, material-light designs and localizing assembly to reduce input costs and shipping expenses.

Which countries enforce the strictest efficiency rules?

Singapore, Australia, Japan, and South Korea lead with minimum-performance standards and emissions penalties that favor VSD upgrades.

Page last updated on: