Market Overview

| Study Period | 2017 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 1.71 Billion |

| Market Size (2030) | USD 2.37 Billion |

| Growth Rate (2025 - 2030) | 6.73% CAGR |

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Business Jet Market Analysis by Mordor Intelligence

The Asia-Pacific Business Jet Market size is estimated at 1.71 billion USD in 2025, and is expected to reach 2.37 billion USD by 2030, growing at a CAGR of 6.73% during the forecast period (2025-2030).

The Asia-Pacific business jet aviation landscape is experiencing significant transformation driven by evolving ownership models and fleet modernization initiatives. As of 2022, business jets in the region represent 6% of the active global fleet, with a notable 98% under whole ownership structure rather than fractional ownership arrangements. This ownership pattern reflects the region's preference for direct asset control and highlights the strong financial capability of Asian operators. The business jet market is witnessing substantial consolidation in manufacturing leadership, with the top three manufacturers Gulfstream Aerospace Corporation, Bombardier, and Cessna collectively accounting for 60% of new deliveries, demonstrating the industry's competitive dynamics and quality standards.

The market is experiencing a notable surge in infrastructure development and service capabilities across key aviation hubs. In 2023, significant investments in maintenance, repair, and overhaul (MRO) facilities have been observed, with Bombardier inaugurating the largest OEM business aviation facility in Singapore, while Gulfstream expanded its presence with new service centers. These developments are complemented by the emergence of new private jet terminals and FBO (Fixed-Base Operator) facilities across the region, enhancing operational efficiency and service quality for business jet operators.

The industry is witnessing a remarkable transformation in customer demographics and usage patterns, particularly driven by the substantial growth in the high-net-worth individual (HNWI) population, which increased by 68% between 2017 and 2022. This demographic shift has led to increased demand for private jet aviation services, especially in emerging markets like Southeast Asia, where new charter operators are establishing operations. The market is also seeing a trend toward larger cabin aircraft and longer-range capabilities, reflecting the region's unique geographic requirements and customer preferences.

The business jet market is undergoing significant technological advancement and fleet modernization initiatives. With a projected delivery of 362 new business jets between 2023 and 2030, manufacturers are focusing on incorporating advanced avionics, enhanced fuel efficiency, and superior cabin connectivity features. This modernization drive is accompanied by a growing emphasis on sustainable aviation practices, with operators increasingly considering environmental impact in their fleet decisions. The industry is also witnessing innovation in business models, with the emergence of digital platforms for charter services and the integration of blockchain technology for maintenance tracking and documentation.

Asia-Pacific Business Jet Market Trends and Insights

The HNWI population is booming and is expected to be the biggest growth driver for the market

- HNWIs have over USD 1 million in liquid financial assets, while UHNWIs have a net worth of at least USD 30 million. From 2017 to 2022, there was a surge of around 90% in the HNWI population in the region. In 2022, the number of HNWIs in Asia-Pacific increased by 2% compared to 2020.

- Japan witnessed a growth rate of 15% in 2022. The slow growth of the HNWI population in major countries has affected the overall wealth growth in Asia-Pacific. In China, the increase in average wealth led to more than 70% in the number of millionaires. Asia-Pacific is emerging as the leading destination for wealth management and private banking globally, driven by the growing wealth in the region, the increasing HNWI population, and its need for financial advice.

- Factors such as a change in political leadership and low consumption during the pandemic impacted the Japanese Stock market, Nikkei 225, and hampered the growth of HNWIs in the country. Developing countries such as India, Vietnam, and Thailand witnessed growth in HNWIs compared to the leading Asia-Pacific countries. In 202, India witnessed a growth of over 292% in its HNWI population. Thailand and Vietnam witnessed a growth of around 21% and 13%, respectively. High liquidity support by central banks, supportive domestic policy, and stability in the stock markets aided the growth of HNWIs in these countries. Technology, industrial conglomerates, energy, and real estate were the major sectors that accounted for most of the Asia-Pacific HNWI population.

-By-Country,-Number-of-HNWIs,-Asia-Pacific,-2017---2030.svg)

Understand The Key Trends Shaping This Market

Download PDF

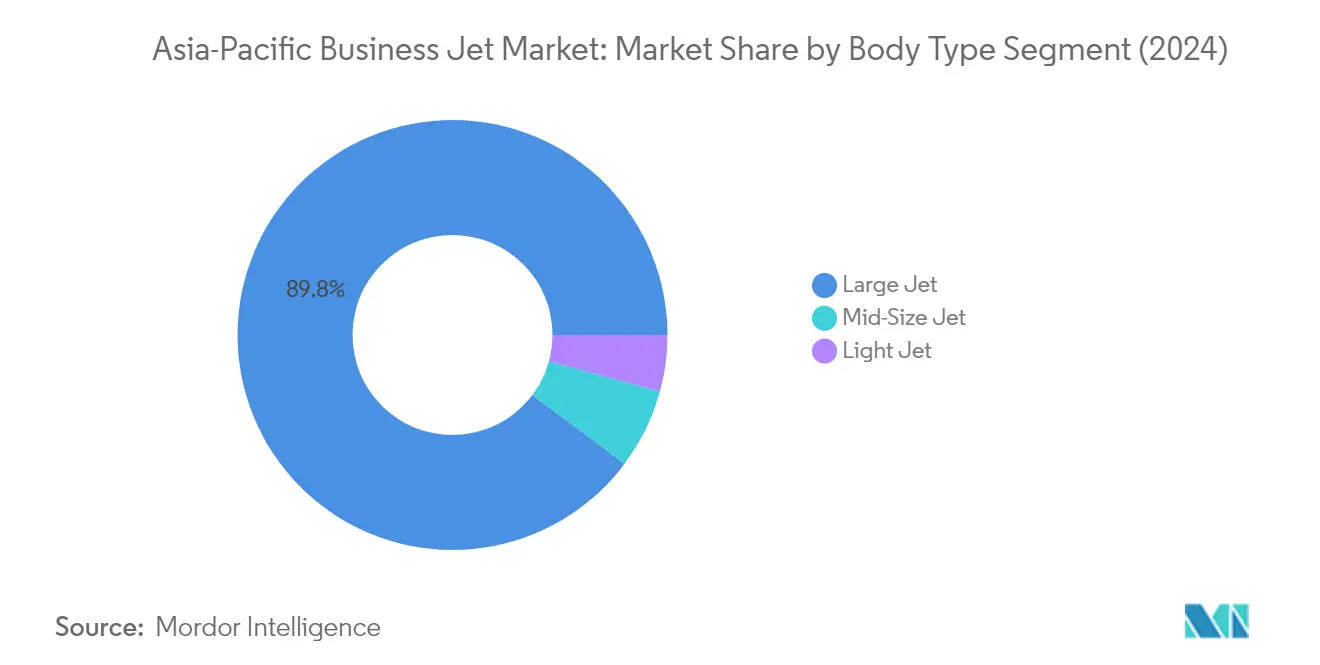

Segment Analysis: Body Type

Large Jet Segment in Asia-Pacific Business Jet Market

The large jet segment dominates the Asia-Pacific business jet market, commanding approximately 90% of the market share in 2024. This substantial market presence is primarily driven by the growing number of high-net-worth individuals (HNWIs) in the region who prefer these aircraft for their superior range, advanced technology, cabin size, and operational efficiency. The segment's dominance is further reinforced by the strong presence of major manufacturers like Gulfstream Aerospace Corporation and Bombardier, who together account for nearly 50% of large jet deliveries in the region. Popular models in this category include the Gulfstream G500/550/650/650ER series, Global 6000/7500 Express, Challenger 604/605/650, and Dassault Aviation's Falcon series, which cater to the sophisticated needs of charter, private, and corporate users in the Asia-Pacific region.

Light Jet Segment in Asia-Pacific Business Jet Market

The light jet segment is emerging as the fastest-growing category in the Asia-Pacific business jet market, projected to grow at approximately 10% CAGR from 2024 to 2029. This remarkable growth is being fueled by increasing demand from new business jet operators and first-time buyers who appreciate the segment's cost-effectiveness and operational flexibility. The segment's expansion is particularly notable in countries like Australia and the Philippines, where light jets are preferred for regional connectivity. Major manufacturers like Cessna, Embraer, and Honda Aircraft Company are actively contributing to this growth through their innovative product offerings and enhanced after-sales support networks. The segment's appeal is further strengthened by the rising trend of shared ownership models and the increasing adoption of these aircraft by air charter companies for short-haul business travel.

Remaining Segments in Body Type

The mid-size jet segment serves as a crucial bridge between light and large jets in the Asia-Pacific jet market. These aircraft offer an optimal balance of range, passenger capacity, and operational costs, making them particularly attractive for medium-range business travel. The segment is particularly strong in markets like Japan and Singapore, where operators value the versatility of mid-size jets for both regional and some international flights. Leading manufacturers in this segment, including Cessna, Bombardier, and Gulfstream Aerospace Corporation, continue to enhance their mid-size jet offerings with advanced technologies and improved comfort features to meet the evolving needs of business aviation customers in the region.

Asia-Pacific Business Jet Market Geography Segment Analysis

Asia-Pacific Business Jet Market in China

China dominates the Asia-Pacific business jet landscape, commanding approximately 22% of the regional market value in 2024. As the largest operator of business jets in Asia-Pacific, China's government considers general aviation to be one of its strategic emerging industries. The Chinese market has witnessed significant infrastructure development, with over 50 general aviation airports added to support private aviation growth. The country's business jet fleet structure is predominantly composed of large jets, which account for about 77% of deliveries, reflecting the preference of Chinese customers for long-range aircraft. The growing number of high-net-worth individuals in the country continues to drive demand for long-range large-cabin jets. The market has also seen the entry of new business jet manufacturers, expanding the available options for Chinese customers. The government's emphasis on supporting general aviation through infrastructure development and regulatory reforms has created a favorable environment for market growth.

Asia-Pacific Business Jet Market in India

India's business jets sector is projected to grow at approximately 11% annually from 2024 to 2029, making it the fastest-growing market in the region. The country's business jet sector is experiencing robust growth alongside its economic expansion and increased utilization of aviation-related services across diverse sectors. The market is characterized by a strong preference for large jets, which account for half of the current operational business jet fleet. The emergence of new charter service providers and the expansion of existing operators have contributed to market dynamism. The country's aviation infrastructure is undergoing significant improvements, particularly in terms of dedicated business aviation facilities and FBO services. The strong economic growth coupled with the rising number of high-net-worth individuals has created a conducive environment for business jet adoption. The market has also witnessed increased interest from international charter operators looking to establish their presence in India.

Asia-Pacific Business Jet Market in Australia

Australia maintains its position as a key player in the Asia-Pacific business jet market, with one of the most mature business aviation sectors in the region. The country's business jet fleet is notably diverse, with light jets dominating the operational fleet, followed by large jets and mid-size jets. The market is characterized by a strong presence of established operators and a well-developed aviation infrastructure. The rise in tourism and increasing demand for private jets has created new opportunities for market expansion. The country's aviation sector benefits from advanced maintenance, repair, and overhaul (MRO) facilities, supporting the operational efficiency of the business jet fleet. The market has shown resilience post-pandemic, with charter operations seeing renewed growth. Australian operators are increasingly focusing on fleet modernization and expansion to meet evolving customer demands.

Asia-Pacific Business Jet Market in Japan

Japan has established itself as a significant force in the Asia-Pacific business jet market, with a sophisticated aviation infrastructure and growing demand for private aviation services. The country's business jet landscape is characterized by a balanced distribution across different aircraft categories, with light jets comprising 37% of the fleet, followed by mid-size jets at 33% and large jets at 30%. The Japanese market benefits from strategic developments in business aviation infrastructure, including dedicated business jet terminals at major airports. The government's focus on deregulation has increased flight activities related to business travel both domestically and internationally. The presence of established maintenance facilities and FBO services enhances the market's operational capabilities. Japanese operators have shown increasing interest in newer, more efficient aircraft models, driving fleet modernization efforts.

Asia-Pacific Business Jet Market in Other Countries

The private jet Asia market in other Asia-Pacific countries, including Malaysia, the Philippines, Singapore, South Korea, Thailand, and Indonesia, demonstrates varying levels of market maturity and growth potential. These markets are characterized by unique regulatory environments and infrastructure development stages. Malaysia and Singapore stand out with their well-developed aviation infrastructure and strategic geographical locations, making them attractive hubs for private jet aviation. The Philippines has emerged as a significant market for light jets due to its archipelagic geography. Indonesia's vast territory and growing economy present substantial opportunities for business aviation growth. South Korea's market is driven by its strong economy and increasing international business connections. Thailand's tourism sector and growing high-net-worth population contribute to its business aviation market development. These countries collectively contribute to the regional market's diversity and growth potential.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

Top Companies in Asia-Pacific Business Jet Market

The leading companies in the business jet market are focusing heavily on product innovation and the development of new aircraft models to maintain their competitive edge. Manufacturers are expanding their service networks and MRO facilities across key markets like Singapore, China, and Australia to strengthen their regional presence. Strategic partnerships with local operators and charter companies have become increasingly common to penetrate emerging markets. Companies are investing in technological advancements like enhanced cabin designs, improved fuel efficiency, and advanced avionics systems to meet evolving customer preferences. The establishment of dedicated training facilities, expansion of parts warehouses, and development of comprehensive aftermarket support networks demonstrate the industry's commitment to operational excellence and customer service. Additionally, manufacturers are adapting their product portfolios to address specific regional requirements while maintaining global quality standards.

Consolidated Market Led By Global Players

The Asia-Pacific business aircraft market exhibits a high level of consolidation with global manufacturers dominating the landscape. These established players leverage their extensive experience, technological capabilities, and worldwide presence to maintain their market positions. The industry is characterized by the presence of large aerospace conglomerates that offer diverse product portfolios ranging from light jets to ultra-long-range aircraft. These companies possess strong financial resources, established distribution networks, and comprehensive after-sales support capabilities that create significant entry barriers for new players. The market has witnessed limited merger and acquisition activity, with companies instead focusing on organic growth through capacity expansion and service network development.

The competitive dynamics are shaped by the presence of both traditional aircraft manufacturers and newer entrants targeting specific market segments. Major players have established strong relationships with regional partners, including maintenance providers, charter operators, and flight training organizations. The industry structure favors companies with integrated operations spanning manufacturing, maintenance, and customer support services. Market participants are increasingly focusing on developing region-specific solutions while maintaining global standards in terms of safety, performance, and reliability.

Innovation and Service Excellence Drive Success

Success in the market increasingly depends on manufacturers' ability to offer comprehensive solutions beyond just aircraft sales. Companies need to develop a strong local presence through service centers, training facilities, and parts distribution networks to effectively serve the growing customer base. The ability to provide customized solutions, flexible ownership models, and comprehensive maintenance packages has become crucial for maintaining private jet market share. Manufacturers must also focus on developing fuel-efficient aircraft with advanced technology features while ensuring compliance with evolving environmental regulations. Building strong relationships with local aviation authorities, understanding regional certification requirements, and establishing efficient supply chains are essential for long-term success.

For new entrants and smaller players, success lies in identifying and serving niche market segments with specialized products or services. Companies must invest in developing innovative financing solutions and ownership models to address the diverse needs of customers across different markets. Understanding local business practices, cultural preferences, and regulatory environments is crucial for establishing a strong market presence. The ability to offer competitive pricing while maintaining high-quality standards and reliable after-sales support will be key differentiators. Additionally, developing partnerships with established players for maintenance support and creating value through specialized services can help companies gain market share in this competitive landscape. Notably, Bombardier's market share in the region is influenced by its strategic partnerships and innovative product offerings.

Asia-Pacific Business Jet Industry Leaders

-

Airbus SE

-

Bombardier Inc.

-

Dassault Aviation

-

General Dynamics Corporation

-

Textron Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- October 2023: Textron Aviation announced that it entered a purchase agreement with Fly Alliance for up to 20 Cessna Citation business jets, four firms with options for 16 additional aircraft. Fly Alliance is expected to use the aircraft for its luxury private jet charter operations and expects to take delivery of the first aircraft, an XLS Gen2, in 2023.

- June 2023: Gulfstream Aerospace Corp. announced today the further expansion of its completions and outfitting operations at St. Louis Downtown Airport. With this latest expansion, Gulfstream is expected to increase completion operations at the site while modernizing its existing spaces by adding new, state-of-the-art equipment and tooling, representing a total capital investment of USD 28.5 million.

- June 2023: Gulfstream Aerospace Corp. announced the super-midsize Gulfstream G280 has been cleared for operations at France’s Airport of the Gulf of Saint-Tropez located in La Môle. The aircraft recently flew several takeoff and landing demonstrations at the short-field airport.

Asia-Pacific Business Jet Market Report Scope

Large Jet, Light Jet, Mid-Size Jet are covered as segments by Body Type. Australia, China, India, Indonesia, Japan, Malaysia, Philippines, Singapore, South Korea, Thailand are covered as segments by Country.

Body Type

| Large Jet |

| Light Jet |

| Mid-Size Jet |

Country

| Australia |

| China |

| India |

| Indonesia |

| Japan |

| Malaysia |

| Philippines |

| Singapore |

| South Korea |

| Thailand |

| Rest of Asia-Pacific |

| Body Type | Large Jet |

| Light Jet | |

| Mid-Size Jet | |

| Country | Australia |

| China | |

| India | |

| Indonesia | |

| Japan | |

| Malaysia | |

| Philippines | |

| Singapore | |

| South Korea | |

| Thailand | |

| Rest of Asia-Pacific |

Need A Different Region or Segment?

Customize Now

Market Definition

- Aircraft Type - General Aviation includes aircraft used for corporate aviation, business aviation and other aerial works.

- Sub-Aircraft Type - Business Jets which are private jets and are designed to carry small groups of people and are used for various roles are included in this study.

- Body Type - Light Jets, Mid-Size Jets, and Large Jets according to their ability to carry passengers and flying distance ranges have been included under this study.

| Keyword | Definition |

|---|---|

| IATA | IATA stands for the International Air Transport Association, a trade organization composed of airlines around the world that has an influence over the commercial aspects of flight. |

| ICAO | ICAO stands for International Civil Aviation Organization, a specialized agency of the United Nations that supports aviation and navigation around the globe. |

| Air Operator Certificate (AOC) | A certificate granted by a National Aviation Authority permitting the conduct of commercial flying activities. |

| Certificate Of Airworthiness (CoA) | A Certificate Of Airworthiness (CoA) is issued for an aircraft by the civil aviation authority in the state in which the aircraft is registered. |

| Gross Domestic Product (GDP) | Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by countries. |

| RPK (Revenue Passenger Kilometres) | The RPK of an airline is the sum of the products obtained by multiplying the number of revenue passengers carried on each flight stage by the stage distance - it is the total number of kilometers traveled by all revenue passengers. |

| Load Factor | The load factor is a metric used in the airline industry that measures the percentage of available seating capacity that has been filled with passengers. |

| Original Equipment Manufacturer (OEM) | An original equipment manufacturer (OEM) traditionally is defined as a company whose goods are used as components in the products of another company, which then sells the finished item to users. |

| International Transportation Safety Association (ITSA) | International Transportation Safety Association (ITSA) is an international network of heads of independent safety investigation authorities (SIA). |

| Available Seats Kilometre (ASK) | This metric is calculated by multiplying Available Seats (AS) in one flight, defined above, multiplied by the distance flown. |

| Gross Weight | The fully-loaded weight of an aircraft, also known as “takeoff weight,” which includes the combined weight of passengers, cargo, and fuel. |

| Airworthiness | The ability of an aircraft, or other airborne equipment or system, to operate in flight and on the ground without significant hazard to aircrew, ground crew, passengers or to other third parties. |

| Airworthiness Standards | Detailed and comprehensive design and safety criteria applicable to the category of aeronautical product (aircraft, engine or propeller). |

| Fixed Base Operator (FBO) | A business or organization that operates at an airport. An FBO provides aircraft operating services like maintenance, fueling, flight training, charter services, hangaring, and parking. |

| High Net worth Individuals (HNWIs) | High Net worth Individuals (HNWIs) are individuals with over USD 1 million in liquid financial assets. |

| Ultra High Net worth Individuals (UHNWIs) | Ultra High Net worth Individuals (UHNWIs) are individuals with over USD 30 million in liquid financial assets. |

| Federal Aviation Administration (FAA) | The division of the Department of Transportation is concerned with aviation. It operates Air Traffic Control and regulates everything from aircraft manufacturing to pilot training to airport operations in the United States. |

| EASA (European Aviation Safety Agency) | The European Aviation Safety Agency is a European Union agency established in 2002 with the task of overseeing civil aviation safety and regulation. |

| Airborne Warning and Control System (AW&C) aircraft | Airborne Warning and Control System (AEW&C) aircraft is equipped with a powerful radar and on-board command and control center to direct the armed forces. |

| The North Atlantic Treaty Organization (NATO) | The North Atlantic Treaty Organization (NATO), also called the North Atlantic Alliance, is an intergovernmental military alliance between 30 member states – 28 European and two North American. |

| Joint Strike Fighter (JSF) | Joint Strike Fighter (JSF) is a development and acquisition program intended to replace a wide range of existing fighter, strike, and ground attack aircraft for the United States, the United Kingdom, Italy, Canada, Australia, the Netherlands, Denmark, Norway, and formerly Turkey. |

| Light Combat Aircraft (LCA) | A light combat aircraft (LCA) is a light, multirole jet/turboprop military aircraft, commonly derived from advanced trainer designs, designed for engaging in light combat. |

| Stockholm International Peace Research Institute (SIPRI) | Stockholm International Peace Research Institute (SIPRI) is an international institute that provides data, analysis, and recommendations for armed conflict, military expenditure, and arms trade as well as disarmament and arms control. |

| Maritime Patrol Aircraft (MPA) | A maritime patrol aircraft (MPA), also known as maritime reconnaissance aircraft is a fixed-wing aircraft designed to operate for long durations over water in maritime patrol roles, in particular, anti-submarine warfare (ASW), anti-ship warfare (AShW), and search and rescue (SAR). |

| Mach Number | The Mach number is defined as the ratio of true airspeed to the speed of sound at the altitude of a given aircraft. |

| Stealth Aircraft | Stealth is a Common term applied to low observable (LO) technology and doctrine, that makes an aircraft near invisible to radar, infrared or visual detection. |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF