Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2019 - 2024 |

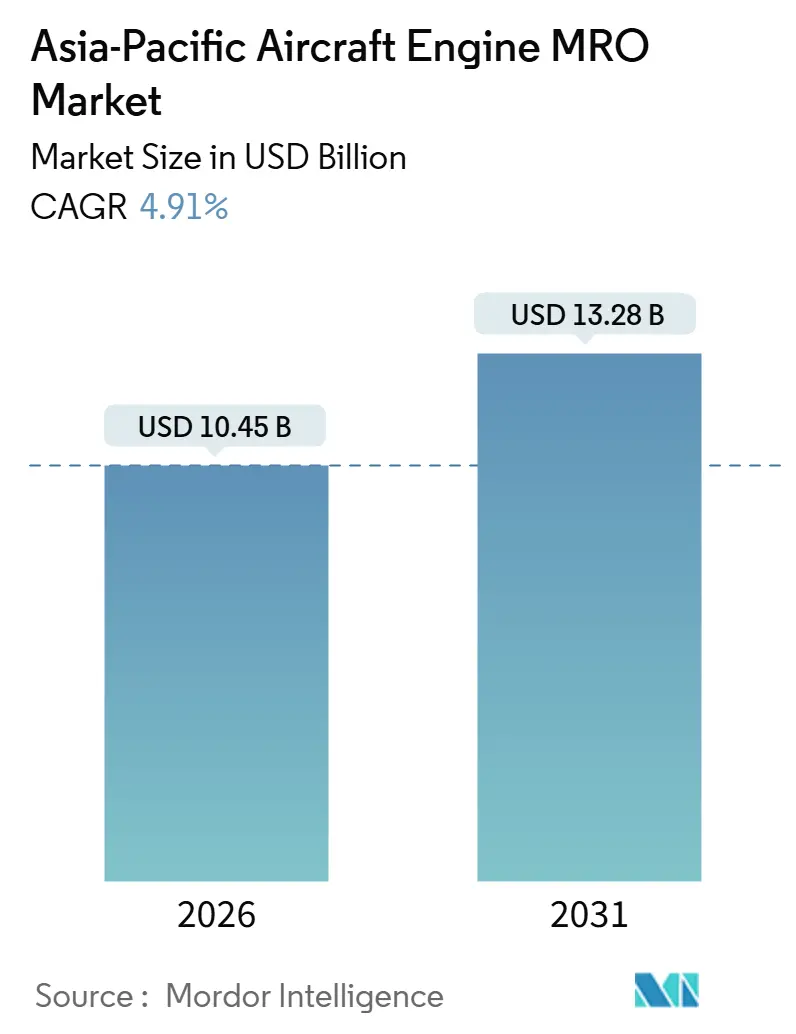

| Market Size (2026) | USD 10.45 Billion |

| Market Size (2031) | USD 13.28 Billion |

| Growth Rate (2026 - 2031) | 4.91% CAGR |

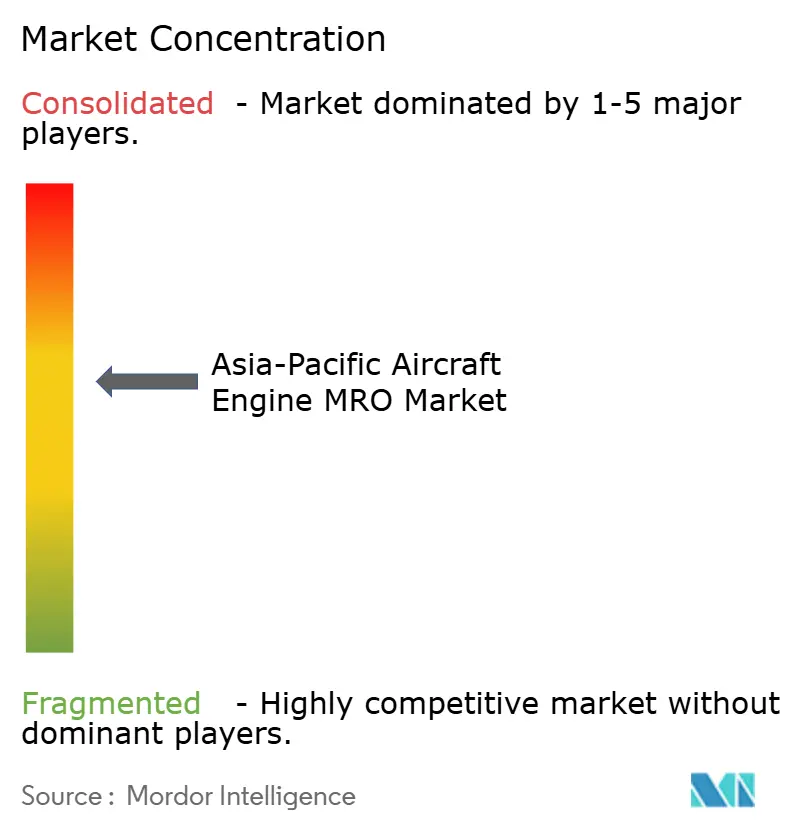

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Aircraft Engine MRO Market Analysis by Mordor Intelligence

The Asia-Pacific aircraft engine MRO market size is USD 10.45 billion in 2026 and is projected to reach USD 13.28 billion by 2031, registering a 4.91% CAGR. This growth reflects sustained fleet expansion, regulatory incentives that encourage localized heavy maintenance, and OEM strategies that co-locate overhaul shops near rapidly growing carriers. Narrowbody deliveries continue to dominate demand, while early-life reliability issues in LEAP and GTF engines intensify short-term shop-visit volumes. OEM-affiliated facilities are widening their lead through proprietary data ecosystems and expertise in hot-section restoration. However, independent providers remain competitive on legacy CFM56 and V2500 platforms by leveraging used, serviceable materials and offering aggressive turnaround-time guarantees. Policymaker support in India, China, and Singapore, combined with investments in advanced coatings and digital twin diagnostics, further underpins the positive outlook for the Asia-Pacific aircraft engine MRO market.

Key Report Takeaways

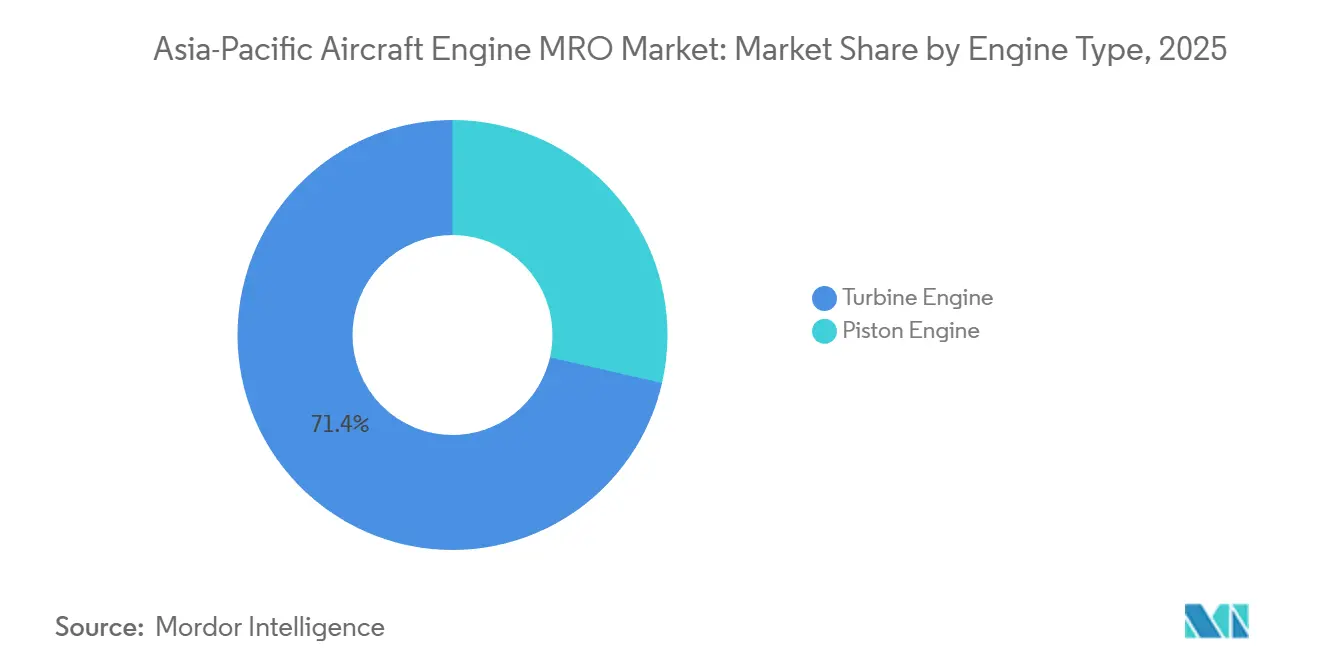

- By engine type, turbine engines held 71.41% of the Asia-Pacific aircraft engine MRO market share in 2025, and the segment is projected to grow at a 5.37% CAGR through 2031.

- By aviation segment, commercial aviation accounted for 63.20% of the Asia-Pacific aircraft engine MRO market size in 2025, while UAV propulsion is expected to advance at a 7.20% CAGR through 2031.

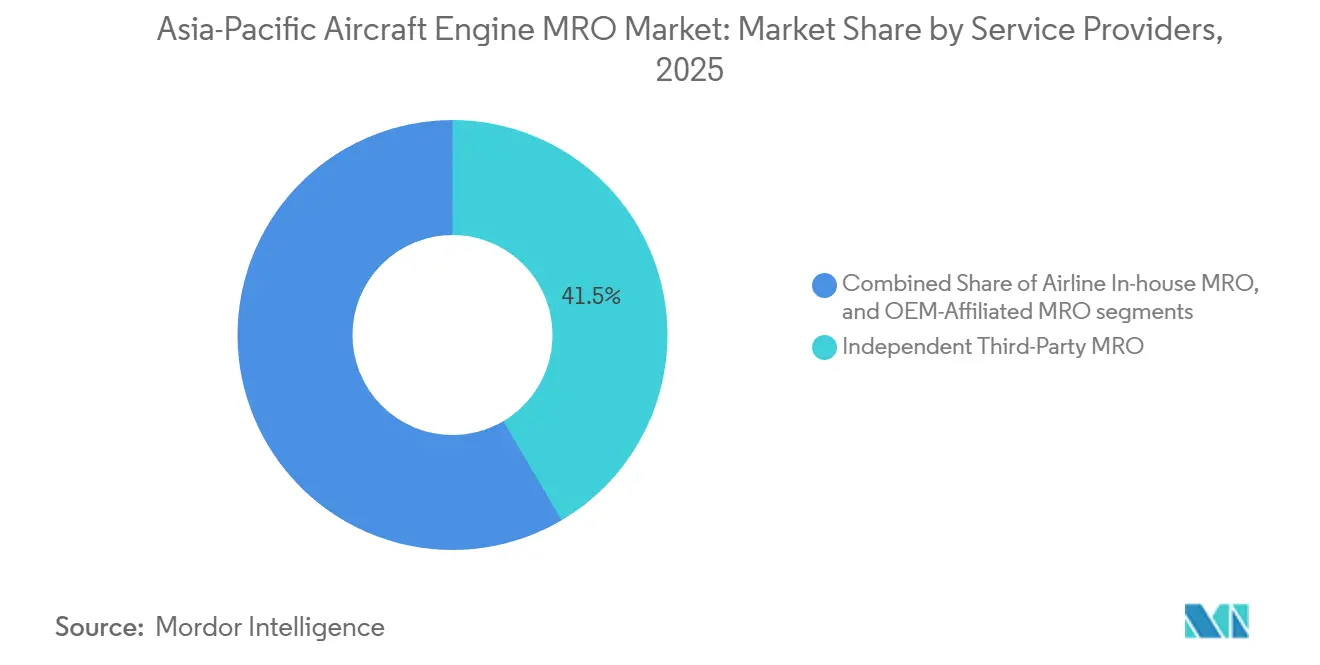

- By service provider, independent MROs controlled 41.52% of the Asia-Pacific aircraft engine MRO market share in 2025; however, OEM-affiliated facilities are expected to expand at a 5.55% CAGR through 2031.

- By geography, China led the Asia-Pacific aircraft engine MRO market, accounting for 48.78% of the market size in 2025. In contrast, India is projected to record the highest CAGR of 6.54% through 2031, following the reduction of GST and the full liberalization of foreign investment.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Aircraft Engine MRO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fleet expansion and new aircraft deliveries | +1.2% | China, India, Southeast Asia; spillover to Japan, Australia | Medium term (2-4 years) |

| Aging narrowbody fleet requiring mid-life shop visits | +0.9% | China, India, Indonesia | Long term (≥ 4 years) |

| OEM and joint-venture capacity investments across APAC hubs | +0.7% | Singapore, Malaysia, China, India | Medium term (2-4 years) |

| Early-life reliability issues in LEAP and GTF engines | +1.1% | India, China, Southeast Asia | Short term (≤ 2 years) |

| Government incentives for indigenous MRO and supply chains | +0.6% | India, China, Singapore | Long term (≥ 4 years) |

| Growing used-serviceable-material trading networks | +0.4% | India, Indonesia, Philippines | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fleet Expansion And New Aircraft Deliveries

Asia-Pacific carriers continue to receive unprecedented numbers of new narrowbody jets, and every delivery seeds a future maintenance event. Between January and September 2025, Airbus and Boeing placed 229 A320neo and B737 MAX aircraft in regional fleets, adding the same number of LEAP powerplants that will age into their first performance-restoration visit around 2032.[1]Source: Airbus, “Orders and Deliveries,” airbus.com Lessors sustain the pipeline: BOC Aviation alone holds orders exceeding 500 aircraft, with six out of every ten units earmarked for China or India, effectively clustering future shop demand in these regions.[2]Source: BOC Aviation, “Annual Report 2024,” bocaviation.com Low-cost airlines such as Vietjet and Akasa already protect margins through long-term power-by-the-hour contracts, sidelining independent overhaulers.

Aging Narrow-Body Fleet Requiring Mid-Life Shop Visits

Asia-Pacific’s vast CFM56 fleet is entering the high-cost middle of its life cycle. Of the region’s 4,200 engines in service, roughly 1,800 exceed fifteen years of operation and are approaching their second or third shop visits, which can cost USD 3 million each. Chinese majors, such as China Southern and Air China, have increased on-wing intervals by 500 flight hours to defer these expenses. Still, this strategy increases the risk of unscheduled removal and reduces the number of available dock slots. Independent shops in Guangzhou and Jakarta exploit the squeeze, promising two-week faster turnarounds and discounting invoices by integrating certified used parts purchased through expanding digital marketplaces across Asia.

OEM And Joint-Venture Capacity Investments Across APAC Hubs

OEMs are doubling down on Asia-Pacific production hubs to secure lucrative aftermarket streams. Rolls-Royce and SIA Engineering have earmarked USD 242 million to increase Singapore Aero Engine Services’ Trent overhaul throughput by 40%, addressing the A350 and A330neo wave. GE Aerospace’s USD 75 million upgrade in Singapore and Malaysia includes laser-coating booths and automated borescopes, which reduce inspection cycles by 30%. Pratt & Whitney followed with a 50-visit annual increase at Eagle Services Asia to tackle GTF backlogs. These investments cement Singapore’s regulatory trifecta approval status, yet India and Indonesia still bear high ferry costs because surplus capacity there remains limited.

Early-Life Reliability Issues In LEAP And GTF Engines

Unexpected reliability shortfalls are causing new-generation engines to be removed from wings sooner than planned. Pratt & Whitney’s powder-metal defect grounded 350 aircraft in 2026, sidelining seventy IndiGo A320neos and forcing expensive wet-leases of older jets. Simultaneously, CFM ordered borescope checks on LEAP engines flown in dusty conditions after three uncontained failures, adding labor hours for Indian and Southeast Asian carriers. Flagship airlines now deploy GE Flight Deck analytics to transition from rigid calendar-based removals to condition-based planning, reducing unnecessary shop visits by approximately 15%. Such digital tools favor OEM-affiliated centers that have complete data access, thereby widening the capability gap with independent centers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skilled-technician shortage and wage inflation | −0.8% | Singapore, India, China urban hubs | Medium term (2-4 years) |

| Supply-chain bottlenecks for critical engine parts | −0.6% | All APAC; severe for titanium forgings | Short term (≤ 2 years) |

| Capacity clustering causing ferry-cost penalties | −0.3% | Indonesia, Philippines, Vietnam, Tier-2 India cities | Long term (≥ 4 years) |

| OEM control over engine-health data limits independents | −0.5% | Independent shops across APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Skilled-Technician Shortage And Wage Inflation

The region’s talent pipeline is drying up just as shop-visit demand accelerates. IATA forecasts that the Asia-Pacific region will need 1.8 million new aviation professionals by 2037, yet the current training output covers barely two-thirds of that requirement.[3]Source: International Air Transport Association, “Workforce Outlook 2025,” iata.org Singapore’s turbine specialists earned SGD 85,000 (USD 66,045) in 2025, a 12% annual jump that squeezed independent shops’ margins while failing to curb attrition. India certified only 1,200 maintenance engineers in 2024, one-third of the forecasted demand, prompting airlines to import expatriate mechanics at a 40% wage premium. Australia’s mining boom siphons technicians with higher pay and more predictable schedules, underscoring how cross-sector competition compounds the labor crunch severely.

Supply-Chain Bottlenecks For Critical Engine Parts

Chronic shortages of critical forgings and castings are lengthening turnaround times despite healthy labor and dock availability. Powder-metal disk output at Pratt & Whitney’s North Carolina plant lags pre-pandemic norms, forcing operators to ground GTF-powered jets for up to three months while waiting for spares. Safran’s six-week strike in France during 2025 delayed 140 LEAP engines, cascading into missed delivery slots at Singapore’s SAESL. Lead times for titanium forgings and single-crystal blades hover around thirty months, compelling shops to carry USD 100 million in inventory to meet performance guarantees. China is investing heavily in domestic forgings, yet it remains 60% dependent on imports.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Engine Type: Turbofan Dominance Anchors Narrow-Body Cycle

Turbine engines held 71.41% of the Asia-Pacific aircraft engine MRO market share in 2025 and are forecasted to achieve a 5.37% CAGR through 2031, sustained by 6,800 CFM56, LEAP, and PW1000G units flying across the region. The Asia-Pacific aircraft engine MRO market size for this segment is expected to grow as 320 LEAP engines are scheduled for their first removals in 2026 and 580 in 2027, testing whether OEM-affiliated capacity can keep pace. Independent providers that secure portable tooling licenses and develop high-pressure turbine refurbishment skills stand to capture overflow demand.

Although widebody powerplants require fewer but more costly events, the installed base of 780 aircraft translates into 110 annual removals, volumes that are most efficiently handled by established hubs in Singapore and Hong Kong. Turboprop and turboshaft engines collectively account for 20% of the Asia-Pacific aircraft engine MRO market. They remain underserved, presenting green-field opportunities in Hyderabad and Surabaya, where regional and helicopter fleets are dense. Piston engines retain a modest share as training fleets migrate toward hybrid and electric propulsion.

By Aviation Segment: UAV Propulsion Emerges As High-Growth Niche

Commercial aviation accounted for 63.20% of the Asia-Pacific aircraft engine MRO market size in 2025, reflecting the dominance of narrowbody passenger operations. UAV propulsion posted the fastest 7.20% CAGR outlook to 2031. China already operates more than 2,000 military drones, such as the Wing Loong II, each of which requires turboprop overhauls every 1,500 hours, a service now supported by AECC at its new Chengdu center.

Narrowbody fleets account for 70% of commercial demand, with LEAP shop-visit intervals averaging around 10 years. In contrast, widebody engines, despite longer intervals, command double the invoice value per visit. Regional jets and military helicopters provide steady niche volumes, sustaining specialized shops in Japan and South Korea. Battery refurbishment for electric logistics drones is emerging outside the scope of traditional turbine MRO but could converge through hybrid-electric models by the early 2030s.

By Service Provider: OEM Affiliates Gain Share Through Data Lock-In

Independent providers captured 41.52% of the Asia-Pacific aircraft engine MRO market share in 2025, maintaining price leadership on legacy engines through 18-day average turnaround times. However, OEM-affiliated shops are growing at a faster rate of 5.55% CAGR by bundling power-by-the-hour contracts that guarantee 95% dispatch reliability and by controlling engine health telemetry. Airline in-house shops such as SIA Engineering and HAECO together account for 32%. They must decide whether to invest USD 100 million or more in next-generation tooling or pivot to component repair.

Access to digital twins and integrated parts supply enables OEM affiliates to reduce shop-visit duration by 20%, a metric that airlines increasingly value. Independents are forming consortia to negotiate collective data access through ICAO, yet progress remains slow. The competitive gap will widen as LEAP and GTF fleets mature, requiring advanced coatings and additive-manufactured spares.

Geography Analysis

China led the Asia-Pacific aircraft engine MRO market with a 48.78% share in 2025, anchored by AMECO and MTU Zhuhai, which completed more than 280 and 200 shop visits, respectively, that year. While China’s scale remains unrivaled, its growth moderates as fleet maturity levels off and regulators push for indigenous support on the CJ-1000A for the C919 aircraft. India is the fastest-growing geography, with a 6.54% CAGR to 2031, fueled by the GST cut to 5%, Air India’s 470-aircraft order, and Safran-Tata’s LEAP module shop, slated for 2027.

Singapore, despite only a 12% share, remains the quality benchmark because SAESL, ST Engineering, and SIA Engineering collectively hold certifications for 18 engine types and all major authority approvals. Japan and South Korea maintain niche specializations in CF34 and CF6 engines, respectively, with IHI and Korean Air Aerospace expanding to accommodate Embraer and GE90 fleets. Indonesia’s GMF AeroAsia is positioning Jakarta as a LEAP-1B hub by 2027, a move that could save LCCs tens of millions in ferry costs. Australia continues to evaluate outsourcing large-engine work to Singapore as rising labor costs challenge domestic economics. Secondary markets in Thailand, Malaysia, the Philippines, and Vietnam collectively generate a 12% share and will likely depend on distributed capacity projects materializing over the next decade.

Competitive Landscape

Innovation and Integration Drive Future Success

The Asia-Pacific aircraft engine MRO market is moderately concentrated, with key players including GE Aerospace, SIA Engineering, ST Engineering, Hong Kong Aircraft Engineering Company Limited, GMF AeroAsia, and SAESL. OEMs deepen vertical integration through equity stakes: Rolls-Royce owns 50% of SAESL, while GE and Safran partner with ST Engineering to secure aftermarket margin. Independents compete through aggressive pricing and turnaround-time guarantees; GMF AeroAsia undercuts OEM affiliates by 40% on CFM56 work by integrating certified USM rotables and focusing on volume.

Data control is the new battleground. GE’s Flight Deck and Rolls-Royce’s Engine Health Management give OEM shops predictive capabilities that independents cannot match without regulatory intervention. Lufthansa Technik’s 2024 purchase of a 26% stake in Air India Engineering marks a likely consolidation wave as OEMs and global MROs acquire stakes in key Asian facilities ahead of the LEAP and GTF shop-visit surge. Blockchain-authenticated USM platforms, such as Aerfin, further disrupt pricing by enabling transparent and traceable part transactions that meet the standards of CAAC and DGCA.

White-space opportunities include Part-145 shops in Tier-2 Indian cities to eliminate ferry costs for IndiGo’s 500-aircraft fleet, as well as dedicated turboprop and turboshaft overhaul lines for the underserved regional and helicopter markets. The interplay of policymaker incentives, OEM data governance, and supply chain fragility will determine whether the Asia-Pacific secures its anticipated 60% share of global engine shop visits by the mid-2030s.

Asia-Pacific Aircraft Engine MRO Industry Leaders

Safran SA

Hong Kong Aircraft Engineering Company Limited

GE Aerospace (General Electric Company)

Singapore Aero Engine Services Private Limited

Singapore Technologies Engineering Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Safran inaugurated the largest LEAP engine MRO center in Hyderabad, initiated its first M88 engine MRO shop outside France, and signed a joint venture with Bharat Electronics Limited to locally produce the “Hammer” air-to-surface weapon. These strategic moves align with India’s “Make in India” initiative, emphasizing localization and defense collaboration.

- September 2025: GE Aerospace's USD 75 million investment in Asia-Pacific MRO facilities reflects a strategic move to address the region's growing aviation maintenance needs. As part of a global USD 1 billion MRO investment plan, this initiative aims to expand capacity, enhance turnaround times, and integrate advanced technologies, including AI-enabled inspection. This development underscores the crucial role of MRO advancements in improving operational efficiency and meeting the evolving needs of the Asia-Pacific aviation market.

Asia-Pacific Aircraft Engine MRO Market Report Scope

Engine maintenance, repair, and overhaul (MRO) is the process of fixing, servicing, or inspecting engines to meet Asia-Pacific safety and airworthiness standards. The study of aircraft engine MRO includes the MRO operations of turbine and piston engine aircraft in the commercial, military, and general aviation sectors in the Asia-Pacific. The market also includes component-level maintenance checks on engines.

The Asia-Pacific aircraft engine MRO market is segmented by engine type, aviation, service providers, and geography. By engine type, the market is segmented into turbine engines and piston engines. By application, the market is segmented into commercial, military, general aviation, and unmanned aerial vehicle (UAV) segments. Service providers segment the market into airline in-house MRO, independent third-party MRO, and OEM-affiliated MRO. The report also covers the market sizes and forecasts for the Asia-Pacific aircraft engine MRO market in seven countries in the region. For each segment, the market size is provided in terms of value (USD).

By Engine Type

| Turbine Engine | Turbofan Engine |

| Turboprop Engine | |

| Turboshaft Engine | |

| Turbojet Engine | |

| Piston Engine |

By Aviation

| Commercial Aviation | Narrowbody |

| Widebody | |

| Regional Jets | |

| Military Aviation | Combat |

| Transport | |

| Special Mission | |

| Helicopters | |

| General Aviation | Business Jets |

| Commercial Helicopters | |

| Unmanned Aerial Vehicles (UAVs) |

By Service Providers

| Airline In-house MRO |

| Independent Third-Party MRO |

| OEM-Affiliated MRO |

By Geography

| China |

| India |

| Japan |

| Singapore |

| Indonesia |

| South Korea |

| Australia |

| Rest of Asia-Pacific |

| By Engine Type | Turbine Engine | Turbofan Engine |

| Turboprop Engine | ||

| Turboshaft Engine | ||

| Turbojet Engine | ||

| Piston Engine | ||

| By Aviation | Commercial Aviation | Narrowbody |

| Widebody | ||

| Regional Jets | ||

| Military Aviation | Combat | |

| Transport | ||

| Special Mission | ||

| Helicopters | ||

| General Aviation | Business Jets | |

| Commercial Helicopters | ||

| Unmanned Aerial Vehicles (UAVs) | ||

| By Service Providers | Airline In-house MRO | |

| Independent Third-Party MRO | ||

| OEM-Affiliated MRO | ||

| By Geography | China | |

| India | ||

| Japan | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

How large is the Asia-Pacific aircraft engine MRO market in 2026?

The Asia-Pacific aircraft engine MRO market size stands at USD 10.45 billion in 2026.

What is the forecast CAGR for Asia-Pacific engine maintenance through 2031?

The market is expected to grow at a 4.91% CAGR to reach USD 13.28 billion by 2031.

Which engine type commands the largest share of shop-visit spending?

Turbine engines, especially CFM56, LEAP, and PW1000G turbofans, held 71.41% of market share in 2025.

Why is India the fastest-growing geography for engine MRO?

Policy reforms that cut GST to 5% and allow 100% foreign investment are attracting new facilities and repatriating work previously sent abroad.

How are OEM-affiliated shops gaining competitive advantage?

They bundle power-by-the-hour contracts with exclusive access to engine-health data and advanced coating technologies, reducing turnaround time by about 20%.

What opportunities exist for new entrants in Asia-Pacific MRO?

Establishing Part-145 shops in Tier-2 Indian cities and setting up dedicated turboprop and turboshaft overhaul lines can tap underserved demand.

Page last updated on: