Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.20 Billion |

| Market Size (2026) | USD 4.42 Billion |

| Market Size (2031) | USD 5.74 Billion |

| Growth Rate (2026 - 2031) | 5.34% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina Home Appliances Market Analysis by Mordor Intelligence

The Argentina home appliances market size is expected to grow from USD 4.20 billion in 2025 to USD 4.42 billion in 2026 and is forecast to reach USD 5.74 billion by 2031 at 5.34% CAGR over 2026-2031. Economic stabilization following the 2023 presidential election, easing inflation, and the reinstatement of structured retail financing collectively underpin this expansion. Rapid recovery in domestic industrial output, reflected in a 32.3% year-over-year spike in household-appliance production during December 2024, keeps inventories healthy while buffering import volatility. Energy-efficiency labeling, coordinated with bank-subsidized installment plans, continues to steer consumer preferences toward A+ and inverter-based models that reduce lifetime operating costs. Strong demand for premium smart appliances is reshaping competitive strategy, with foreign brands introducing AI-enabled product lines and local manufacturers scaling capacity to protect share. Intensifying online adoption, which is on course to pass 50% penetration in certain categories by 2029, compels brick-and-mortar retailers to emphasize omnichannel convenience, robust after-sales service, and aggressive installment promotions to defend their dominant position.

Key Report Takeaways

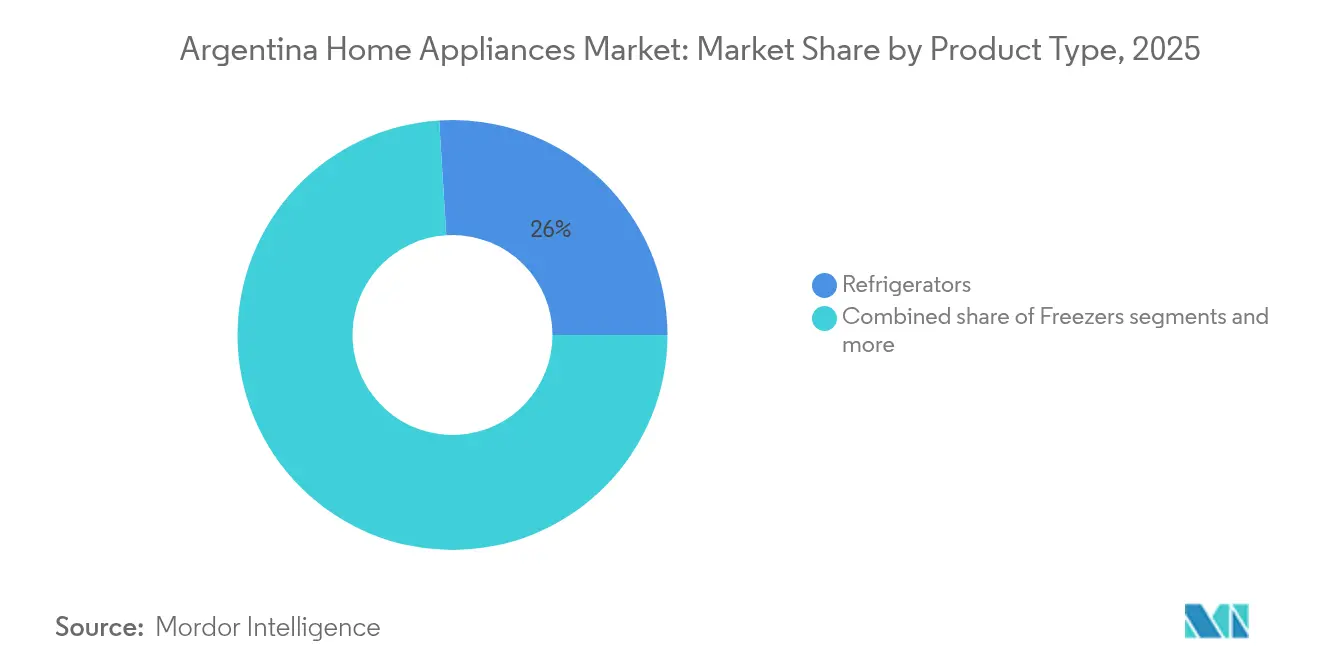

- By product type, refrigerators secured 25.99% of the Argentina home appliances market share in 2025, while ovens led forecast growth at a 5.58% CAGR through 2031.

- By distribution channel, multi-brand stores captured 41.83% of the Argentina home appliances market share in 2025, whereas online platforms are expanding at a 6.02% CAGR to 2031.

- By geography, Buenos Aires Metropolitan Area accounted for 40.64% of the Argentina home appliances market size in 2025, while Patagonia exhibits the fastest projected CAGR at 5.47% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Argentina Home Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Gradual rebound in consumer purchasing power | +1.8% | Nationwide; strongest in Buenos Aires & Córdoba | Medium term (2-4 years) |

| National energy-efficiency labeling program | +1.2% | Nationwide; early gains in Buenos Aires, Córdoba, Mendoza | Long term (≥ 4 years) |

| Retail installment schemes (“Cuota Simple”) | +1.5% | Urban centers nationwide | Short term (≤ 2 years) |

| Urban micro-living demand for compact formats | +0.9% | Buenos Aires Metro, Córdoba, Rosario | Medium term (2-4 years) |

| Import restrictions stimulating local output | +1.1% | Manufacturing hubs in Buenos Aires & Córdoba | Long term (≥ 4 years) |

| Penetration of inverter technology | +1.0% | High-tariff regions nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Gradual Rebound in Consumer Purchasing Power

Sustained moderation in headline inflation from 212% to 117% by April 2025 lifted durable-goods confidence 184%, reigniting replacement cycles for refrigerators and washing machines that households had postponed during the 2022-2023 crisis [1] iProfesional, “Confianza para bienes durables creció 184%,” iprofesional.com. . Industrial production growth of 7.1% year-over-year in January 2025 broadened income stability, allowing consumers to embrace medium-term financing. Whirlpool Brasil designated Argentina an export priority as macro conditions firmed, while domestic firm Mabe injected USD 23 million into new Córdoba capacity to capture the resurgence. Retailers now report double-digit same-store growth in large-appliance tickets, signaling that pent-up demand is translating into confirmed sales. Lower inflation expectations also support more predictable cash-flow planning among families, reinforcing the appeal of 12- to 24-month payment programs. The spending revival, therefore, feeds directly into higher volumes across every major-appliance line.

Retail Installment Schemes

The January 2024 shift from Ahora 12 to Cuota Simple re-energized financing, offering 3- and 6-month plans at 93.5% TNA and preserving retailer liquidity. Multi-brand chains like Cetrogar routinely extend up to 24 interest-free installments through card partnerships, while Whirlpool’s web store promotes bank-backed programs tied to specific SKUs. Such flexibility turns mid-range appliances particularly 340- to 400-liter refrigerators into attainable monthly outlays rather than daunting lump-sum expenses. In inflationary contexts, consumers prize the predictability of fixed payments, so financing terms become a competitive lever on par with sticker price. The upshot is that volume leaders can protect margins by trading longer tenor for price integrity. The continued availability of subsidized credit is therefore pivotal to sustaining momentum in discretionary white-goods spending.

Rising Urban Micro-Living Demand for Compact Formats

Soaring urban real-estate prices in Buenos Aires, Córdoba, and Rosario shrink average dwelling size, elevating the appeal of space-saving appliances. Samsung’s Bespoke AI washer-dryer stack, delivering 22 kg wash and 15 kg dry capacity in a single footprint, epitomizes manufacturers’ response to micro-living [3]Samsung Electronics, “Samsung potencia la eficiencia y la innovación con Bespoke AI,” news.samsung.com.. Local players BGH and Drean have released under-counter refrigerators and built-in convection ovens that align flush with modular cabinetry. For consumers, square-meter efficiency now rivals capacity as a decision trigger, a shift that benefits premium feature bundles capable of maximizing multifunctionality. Developers of new high-rise condos increasingly specify compact, inverter-driven split ACs in tender documents, translating architectural trends into predictable appliance demand. This segment therefore layers incremental growth atop core replacement cycles.

Penetration of Inverter Technology

Escalating residential tariffs in high-consumption provinces incentivize consumers to curb kWh usage through inverter compressors. Split ACs and bottom-mount refrigerator models featuring DC inverters now headline media campaigns, with 10-year warranty offers easing adoption fears. IRAM certification endows compliant units with visible performance badges, reinforcing trust at point-of-sale[4]Whirlpool Argentina, “Planes de financiación 30 cuotas,” whirlpool.com.ar. . The trend lifts average selling prices yet reduces lifetime ownership costs, allowing retailers to upsell efficiency without eroding affordability thanks to financing packages. Independent studies from utility Enarsa show inverter ACs cutting summer peaks by 35%, bolstering policy support. As cumulative installed base climbs, replacement demand will tilt ever further toward high-efficiency technologies.

Restraints Impact Analysis*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency volatility elevating import costs | -1.4% | Nationwide; strongest impact on premium imports | Short term (≤ 2 years) |

| Non-automatic import licenses causing shortages | -0.8% | Premium-segment concentration nationwide | Medium term (2-4 years) |

| Right-to-repair rules lengthening product lifecycles | -1.2% | Nationwide, especially in urban areas | Medium term (2–4 years) |

| Shrinking household size limiting multi-appliance uptake | -0.9% | Nationwide, impacting urban and suburban regions | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Currency Volatility Elevating Import Costs

Sharp peso swings expand landed costs for component-heavy SKUs, squeezing distributors that rely on U.S.-dollar invoices. Although the national trade surplus flipped to USD 18.9 billion in 2024, consumer-goods imports jumped 42.3% year-over-year in February 2025, signaling an expensive resurgence. Premium brands importing finished French-door refrigerators or Wi-Fi modules must either absorb margin hits or transmit higher prices, narrowing their accessible segment. Domestic producers buffer some risk through pesos-denominated wages and local metals, yet they still import compressors and microprocessors whose dollar pricing remains inelastic. Volatility thus distorts planning horizons, forcing cautious inventory holdings that hamper promotional depth. The pass-through effect typically curtails the price-sensitive mid-income tier, cooling sales momentum for high-ticket imports.

Non-Automatic Import Licenses Causing Shortages

The January 2025 tightening of ARCA documentation re-introduced administrative lags of 90-120 days, delaying premium smart-appliance arrivals. Courier channels for large appliances remain prohibited, leaving maritime and formal freight as the sole routes, both subject to customs queueing. Retailers consequently report out-of-stock flags on models like Whirlpool’s 461 L Platinum series. Scarcity inflates price tags, steering consumers toward locally produced substitutes that may lack advanced IoT features. Lengthy approval cycles force import-reliant brands to elongate lead times and hedge currency exposure, eroding agility in a market that favors rapid promotional pivots. Should licensing delays persist, domestic capacity expansions may accelerate, permanently altering competitive balance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Major Appliances Maintain Volume Leadership While Smart Features Command Premiums

Refrigerators retained 25.99% of total Argentina home appliances market share in 2025, supported by a cultural preference for large 340- to 554-liter No Frost units that accommodate extended households. The Argentina home appliances market size for refrigerators is forecast to expand in line with the overall industry at a 5.34% CAGR, benefiting from Banco Nación’s interest-free financing for energy-efficient models. Rising electricity costs elevate the appeal of inverter compressors, prompting both global brands and local manufacturers to relabel mid-tier lines with A+ ratings as standard. Simultaneously, ovens including microwaves and combination units record the fastest forecast CAGR at 5.58%, driven by recipe-sharing social-media trends and smaller apartment kitchens that favor multifunctional cooking solutions.

Washing machines and dishwashers continue to gain incremental traction as households adopt larger 10- to 12-kg capacities that reduce frequency of use, aligning with rising water-cost awareness. Samsung’s Bespoke AI washer-dryer couples 22 kg wash and 15 kg dry cycles within a single drum, illustrating how smart cycles amplify convenience for urban micro-living. Air conditioners capture rising demand amid documented 4.07% year-over-year growth in residential electricity consumption, and inverter split systems outpace window units thanks to 35% energy-savings claims verified by utility studies. Small appliances ranging from coffee makers to air fryers ride e-commerce momentum, evidenced by Cetrogar listing 413 coffee-maker models in April 2025. Stringent IRAM safety norms apply across categories, and local suppliers adept at navigating certification maintain time-to-market edge over import-reliant rivals.

By Distribution Channel: Multi-Brand Chains Defend Dominance Against Digital Ascendancy

Multi-brand stores represented 41.83% of 2025 revenue, their scale allowing nationwide logistics coverage, rich display floors, and service centers that instill post-sale confidence. Attractive financing often stretching to 24 interest-free installments enables these outlets to neutralize price gaps versus online flash deals. In-store POP displays emphasize IRAM labels and demo live smart-voice integrations, enhancing tangible evaluation before purchase. Nevertheless, the Argentina home appliances market is witnessing the online channel clock a 6.02% CAGR well above the store average propelled by manufacturer D2C portals and MercadoLibre brand stores whose real-time pricing and same-day delivery sway digitally savvy buyers. Marketplace algorithms that highlight energy-rating filters and consumer reviews foster informed choices, reducing perceived risk of buying sight-unseen. Exclusive brand outlets cater to premium narratives through immersive showrooms, whereas warehouse clubs and department stores cater to mass-volume promotions tied to holiday events such as Hot Sale and Cyber Monday. The hybridization trend now sees chains launching click-and-collect, thereby merging brick reliability with web convenience.

Geography Analysis

Buenos Aires Metropolitan Area accounted for 40.64% of the Argentina home appliances market share in 2025, leveraging the nation’s highest disposable-income density and proximity to Whirlpool’s Pilar plant. The urban cluster consumes 36% of national electricity, magnifying energy-savings messaging that underpins A+ appliance sales. Retail chains operate dense store networks complemented by same-day e-commerce fulfillment, affording metropolitan shoppers unparalleled assortment breadth. Central Argentina, anchored by Córdoba’s industrial belt, benefits from Mabe’s USD 23 million kitchen-appliance plant that cuts shipping cost and lead time, helping the region secure robust mid-income uptake of mid-range models. Strong automotive exports and agri-business incomes bolster household budgets, translating into steady 5% growth across white-goods lines.

Patagonia, despite sparse population, posts a market-leading 5.47% CAGR forecast as the Vaca Muerta shale expansion fuels residential and commercial construction booms. Appliance distributors ride piggyback on housing completions, although freight surcharges and delivery exclusions particularly to Tierra del Fuego temper stocking breadth. Retailers circumvent this by offering ship-to-store options at mainland depots where consumers arrange private ferry pickup. Cuyo Region’s wine boom and lithium mining in San Juan deliver disposable income gains that filter into appliance upgrades, especially inverter ACs combating summer vineyard heat. Northwest (NOA) and Northeast (NEA) remain income-constrained, and longer replacement cycles persist, yet NGO-backed micro-credit for rural electrification programs seeds future white-goods adoption.

Regional penetration disparity widens as provinces unwind electricity subsidies at varying paces, influencing payback calculations for efficient appliances. Areas with tariff surges such as Neuquén witness accelerated shift to inverter compressors and A+ refrigerators, while subsidy-heavy zones delay upgrade waves. Logistics infrastructure also shapes brand choice; local labels Gafa and BGH gain share in inland provinces due to shorter lead times and lower freight premiums. Conversely, premium import-dependent lines command higher share in Buenos Aires where port adjacency dulls logistics friction. Therefore, geography not only dictates sales volume but also sculpts the competitive landscape of the Argentina home appliances market.

Competitive Landscape

The 2024 market demonstrates moderate concentration, with Whirlpool leading by utilizing dual manufacturing hubs that minimize currency exposure and comply with IRAM protocols, effectively avoiding import delays. Samsung and LG follow closely, focusing on premium differentiation through smart connectivity. Samsung’s March 2025 Bespoke AI campaign highlights this strategy with Family Hub refrigerators featuring 32-inch touch displays integrated into the SmartThings ecosystem. Local brands like BGH and Drean maintain strong positions in the mass market through cost leadership and agile distribution. Meanwhile, Newsan expands its reach with the Atma and Noblex brands via omnichannel rollouts.

Electrolux targets upper-middle households by emphasizing Scandinavian design and quiet inverter technology, appealing to consumers valuing aesthetics and efficiency. Strategic investments highlight ongoing mid-term positioning battles. Mabe’s USD 23 million investment in Córdoba increases annual kitchen appliance production to 200,000 units, reducing landed costs and enhancing domestic content an advantage amid looming import restrictions. Newsan’s July 2024 acquisition of P&G Argentina diversifies its revenue and integrates cross-category loyalty programs, potentially driving appliance trials among Pampers and Gillette customers. Samsung also targets real-estate developers by bundling bulk Bespoke appliance packages into condominium budgets, securing volume ahead of retail launches.

Currency volatility continues to pressure import-dependent brands like Haier, prompting partnerships with local EMS assemblers to qualify for tariff exemptions. The competitive landscape oscillates between premium feature innovation and cost-based market defenses. Success hinges on execution discipline amid Argentina’s unpredictable regulatory environment. Overall, the market remains dynamic, with players balancing innovation, cost-efficiency, and strategic alliances to capture and defend market share. This fluid scenario sets the stage for continued competition and shifting leadership.

Argentina Home Appliances Industry Leaders

Whirlpool Corp.

Samsung Electronics

LG Electronics

Electrolux AB

Mabe

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Mabe invested USD 23 million in a new Córdoba kitchen-appliance plant with 200 000-unit annual capacity, deepening its Argentine footprint.

- March 2025: Samsung Argentina debuted the Bespoke AI line, merging AI cycle optimization with SmartThings integration across washers and refrigerators.

- January 2025: Argentina tightened ARCA import controls, complicating appliance supply chains while favoring local manufacturers.

- January 2025: Argentina's industrial production rose 7.1% year-over-year with domestic appliance production surging 32.3% in December 2024, driven by refrigerators, washing machines, stoves, and water heaters.

Argentina Home Appliances Market Report Scope

Home appliances include electrical or mechanical devices used in a household. They assist in household functions such as cleaning, cooking, and food preservation, among other activities.

The Argentine home appliances market is segmented by major appliances, small appliances, and distribution channels. By major appliances, the market is sub-segmented into refrigerators, freezers, dishwashing machines, washing machines, cooks, and ovens. By small appliances, the market is sub-segmented into vacuum cleaners, small kitchen appliances, hair clippers and hair dryers, irons, toasters, grills and roasters, and other small appliances. By distribution channels, the market is sub-segmented into supermarkets and hypermarkets, specialty stores, e-commerce, and other distribution channels.

The report offers market size and forecasts for the Argentina home appliance market in terms of value (USD) for all the above segments.

By Product

| Major Home Appliances | Refrigerators |

| Freezers | |

| Washing Machines | |

| Dishwashers | |

| Ovens (Incl. Combi & Microwave) | |

| Air Conditioners | |

| Other Major Home Appliances | |

| Small Home Appliances | Coffee Makers |

| Food Processors | |

| Grills & Roasters | |

| Electric Kettles | |

| Juicers & Blenders | |

| Air Fryers | |

| Vacuum Cleaners | |

| Electric Rice Cookers | |

| Toasters | |

| Countertop Ovens | |

| Other Small Home Appliances |

By Distribution Channel

| Multi-Brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

By Geography

| Buenos Aires Metropolitan Area |

| Central Argentina |

| Cuyo Region |

| Northwest (NOA) |

| Northeast (NEA) |

| Patagonia |

| By Product | Major Home Appliances | Refrigerators |

| Freezers | ||

| Washing Machines | ||

| Dishwashers | ||

| Ovens (Incl. Combi & Microwave) | ||

| Air Conditioners | ||

| Other Major Home Appliances | ||

| Small Home Appliances | Coffee Makers | |

| Food Processors | ||

| Grills & Roasters | ||

| Electric Kettles | ||

| Juicers & Blenders | ||

| Air Fryers | ||

| Vacuum Cleaners | ||

| Electric Rice Cookers | ||

| Toasters | ||

| Countertop Ovens | ||

| Other Small Home Appliances | ||

| By Distribution Channel | Multi-Brand Stores | |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| By Geography | Buenos Aires Metropolitan Area | |

| Central Argentina | ||

| Cuyo Region | ||

| Northwest (NOA) | ||

| Northeast (NEA) | ||

| Patagonia | ||

Key Questions Answered in the Report

What is the current value of the Argentina home appliances market?

The market was valued at USD 4.42 billion in 2026, with a projected rise to USD 5.74 billion by 2031.

Which product category leads sales nationwide?

Refrigerators command the highest share at 25.99%, aided by the popularity of large No Frost models with inverter compressors.

Which distribution channel is growing fastest?

Online platforms, including manufacturer D2C websites and MercadoLibre stores, are expanding at a 6.02% CAGR through 2031.

Why is Patagonia’s demand rising quickly?

The Vaca Muerta shale boom is spurring housing and commercial projects, which in turn elevate appliance installations in the region

How is Argentina’s energy-efficiency policy affecting purchases?

Mandatory IRAM labeling and bank-subsidized financing encourage households to upgrade to A+ and inverter models that cut electricity costs.

Which company holds the largest market share?

Whirlpool leads with a 20% share, thanks to its dual domestic manufacturing sites and broad mid-range portfolio.

Page last updated on: