Argentina Grains Market Analysis by Mordor Intelligence

The Argentina grains market size was valued at USD 17.56 billion in 2025 and estimated to grow from USD 18.24 billion in 2026 to reach USD 22.10 billion by 2031, at a CAGR of 3.91% during the forecast period (2026-2031). Similarly, the volume was recorded at 104.45 million metric tons in 2025 and is projected to grow to 107.06 million metric tons in 2026. It is projected to reach 123.0 million metric tons by 2031, registering a CAGR of 2.81%. The country maintains its position as a global agricultural leader with an output of 125 million metric tons and represents 15% of world grain trade[1]Australian Export Grains Innovation Centre, “Argentina Grain Export Overview,” aegic.org.au. Argentina remains one of the world's major maize exporters, playing a crucial role in global food security and trade. According to the FAOSTAT, in 2023, the country's maize production reached 41.4 million metric tons despite experiencing a 29.8% reduction from the previous year due to severe drought. The maize generated USD 6.55 billion in export revenues in 2024, according to the ITC Trade Map, serving as a significant source of foreign exchange and rural employment. The market faces both opportunities and challenges, with biofuel mandates, precision agriculture adoption, and domestic feed industry growth driving demand toward higher-value segments, while climate variability, port infrastructure limitations, and foreign exchange restrictions impact market operations.

Key Report Takeaways

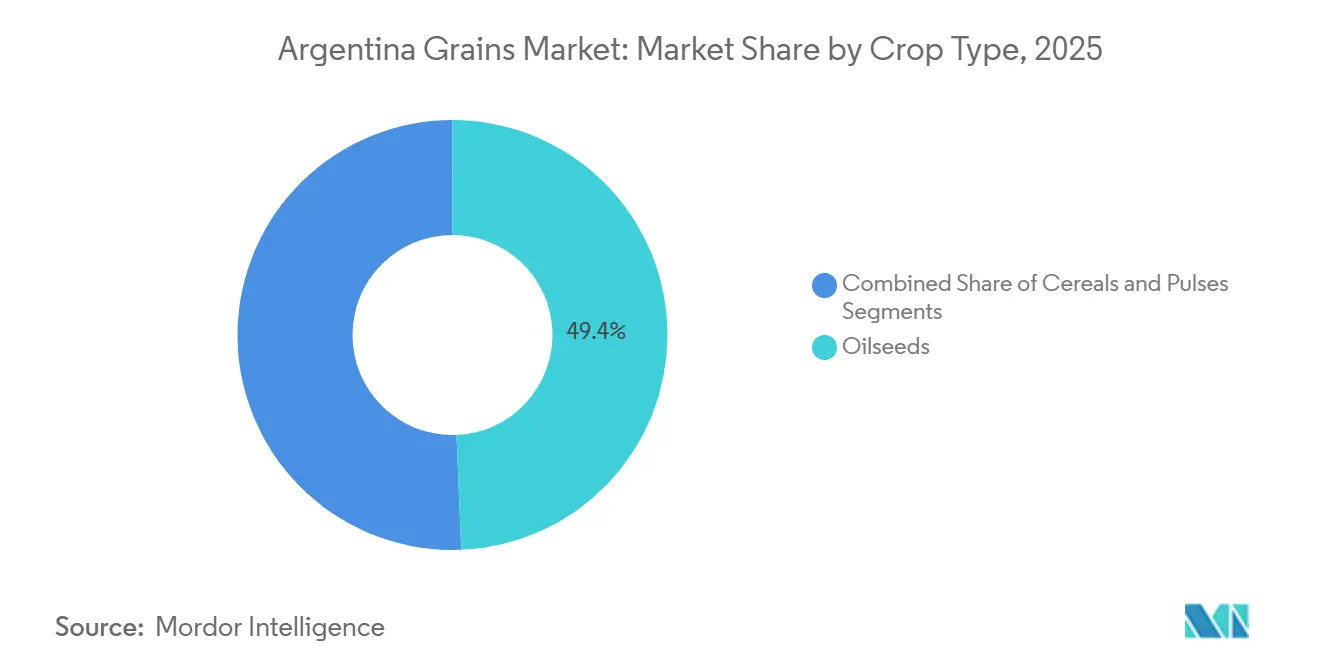

- By crop type, oilseeds held 49.35% of the Argentina grains market size in 2025, while the cereals segment is projected to grow at a CAGR of 4.03% during the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Argentina Grains Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Robust biofuel blending mandates | +1.2% | National, soybean and corn belts | Medium term (2-4 years) |

| Adoption of Precision Ag-tech on mega farms | +0.8% | Pampas region, spreading north | Medium term (2-4 years) |

| Expansion of grain-based animal feed capacity | +0.7% | National, corn-producing clusters | Short term (≤ 2 years) |

| Government support drives growth in grain production | +0.6% | Export-oriented provinces | Short term (≤ 2 years) |

| Capital-funded regenerative grain purchase agreements | +0.4% | Pampas | Medium term (2-4 years) |

| Organic and sustainable farming trends | +0.3% | Scattered, near urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Robust Biofuel Blending Mandates

Argentina's biodiesel and bioethanol consumption is rising, driven primarily by increased gasoline demand in the agricultural sector for farm machinery. The country's biodiesel production is currently operating at 38% capacity utilization, highlighting the potential for higher soybean oil demand, irrespective of export performance. According to the Secretaría de Energía (Argentina), biodiesel production grew by 40% in 2024 compared to 2023, reaching 1.16 million metric tons. Additionally, the USDA reported that bioethanol consumption reached 1.12 billion liters in 2024, with 60% derived from corn-based production. Higher blending mandates are ensuring steady domestic demand, reducing exposure to global price fluctuations, and creating long-term feedstock premiums in Argentina's grain market. This stability in corn and soybean prices is further reinforced by refiners securing volumes under the increased mandates, leading to stronger prices for farmers.

Adoption of Precision Ag-Tech on Mega Farms

Large-scale row-crop operations in Argentina are implementing precision agriculture technologies, including drones, sensors, and AI-driven prescription maps, to reduce input waste and increase yields. As of 2024, Vuelagro srpays 250 to 370 acres per day, achieving 80-90% reductions in water and chemical usage through targeted applications. The Aapresid Congress 2024 showcased agricultural technology companies, including DeepAgro for AI-based herbicide application, Ucropit for field-level traceability, and Silo Real for humidity monitoring, highlighting the increasing adoption of digital solutions. With soybean receiving suboptimal fertilization, precision agriculture tools present opportunities for yield improvement. These technologies reduce fuel consumption by 27%, decreasing carbon emissions and supporting decarbonization initiatives of major exporters. The implementation of connected agricultural machinery expands the Argentina grains market by improving productivity while controlling operational costs.

Expansion of Grain-Based Animal Feed Capacity

Argentina's livestock integrators are expanding their feed-milling operations, increasing domestic demand for corn and soybean meal. The USDA projects Argentina's corn production to reach 49 million metric tons in 2024/25, with domestic consumption increasing due to growth in poultry and pork feedlot operations [2]U.S. Department of Agriculture, “Argentina Grain and Feed Update,” usda.gov. Processing facilities now handle storage, crushing, and pelleting operations on-site, retaining margins previously captured by international buyers. This vertical integration helps protect operators from export premium volatility, and drives increased cultivation of animal feed-specific corn hybrids. The enhanced feed processing capacity strengthens the Argentina grains market by securing a significant portion of harvest volumes for domestic use.

Government Support Drives Growth in Grain Production

The reduction in export duties on soybeans to 26% and further to 24% by late 2025 and corn and wheat to 9.5% has enhanced the profitability of various planting plans. The USD 100 million loan from the Inter-American Development Bank in 2023 for climate-smart agro-industry improvements will benefit 25,000 rural producers. The fiscal reforms have generated the first primary surplus since 2010, with real GDP projected to grow by 5.5% in 2025[3] International Monetary Fund, “Argentina: Request for Extended Fund Facility Arrangement,” imf.org. These developments facilitate machinery investments and the adoption of high-yield crop varieties, strengthening the Argentina grain market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in grain prices | -0.7% | Global, export-dependent heartlands | Short term (≤ 2 years) |

| Rising climatic shocks | -0.6% | Nationwide, drought-prone tracts | Long term (≥ 4 years) |

| Infrastructure constraints at ports and railways | -0.5% | Rosario corridor, northern rail | Medium term (2-4 years) |

| Foreign exchange control risks impacting export opportunities | -0.3% | National, exporters relying on hard-currency inflows | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatility in Grain Prices

Price volatility affects input budgeting, hedging strategies, and debt management. A Farmdoc survey of 475 agricultural producers across the Pampas, US Midwest, and southern Brazil revealed that Argentine farmers consider price volatility their primary risk. Argentina's food inflation reached 293% year on year in May 2024, increasing working capital requirements[4]World Bank, “Transformational Economic Corridors in Northwest Argentina,” worldbank.org. Global market conditions intensify this volatility, as demonstrated when Chicago corn futures reached an 18-month high following unfavorable South American weather conditions. These market disruptions impact forward-sales contracts, requiring sophisticated price-risk management tools in Argentina's grain market, which smaller producers often struggle to access.

Rising Climatic Shocks

The Buenos Aires Grain Exchange reduced its 2024/25 corn forecast by 1 million metric tons, with only 30% of plantings in good or excellent condition compared to 40% in the previous year[5]Agriculture and Horticulture Development Board, “Argentina Corn Outlook January 2025,” ahdb.org.uk. Climate change impacts could reduce global staple crop production by 2050, particularly affecting water-scarce regions. Drought conditions have already decreased soybean oil production due to the decline in potential yields by 22% in 2025 according to the Buenos Aires Grain Exchange. The Argentina grains market faces constraints on long-term growth as producers invest in drought-resistant seeds and irrigation systems, increasing operational costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Crop Type: Oilseeds Dominate While Cereals Accelerate

Oilseeds dominated the Argentina grain market with a 49.35% share in 2025. The soybean harvest reached 50.3 million metric tons in 2025. Argentina retained its position as the leading exporter of soybean oil in 2024, with exports valued at USD 5.2 billion according to the ITC Trade Map. However, the segment's growth rate remains below the overall market growth. This slower growth stems from increased competition from Brazilian acreage, changing dietary preferences toward alternative oils, and domestic biodiesel consumption. The segment maintains stability through improved local crush margins and new regenerative purchase premiums.

Cereals represent fastest growing segment at a 4.03% CAGR. According to USDA projections, corn production will reach 49 million metric tons in 2024/25, with exports anticipated at 34 million metric tons. Wheat production is projected to achieve 21 million metric tons by 2025, with export potential of 14-15 million metric tons. The segment benefits from increased domestic feed demand, higher ethanol blending requirements, and favorable rainfall patterns improving wheat yields. The reduction in export taxes on corn and wheat to 9.5% has enhanced profit margins, positioning cereals as the fastest-growing segment in the Argentina grain market.

Geography Analysis

The Pampas region remains the primary production center, contributing the majority of oilseed and cereal output due to its deep-topsoil loams, mechanized farming practices, and proximity to Rosario's crushing and port facilities. However, land limitations and climate variability are driving expansion northward into Santiago del Estero and Salta provinces, where adapted crop varieties and no-till farming methods enable the cultivation of new areas. World Bank corridor analyses identify Salta as the primary grain hub in the Northwest region, with potential for increased throughput once rail and road infrastructure improve. The integration of feed mills and crushing plants near livestock centers is increasing, expanding domestic trade flows within the Argentina grain market.

Argentina has recorded substantial growth in grain consumption, particularly wheat, barley, and corn, driven by increased demand in the food and feed sectors. Corn is essential to Argentina's livestock industry, which accounts for 70% of national corn production in 2023, according to USDA data. The growth in livestock production has driven increased maize cultivation, as corn serves as a primary feed component for cattle, poultry, and swine. Domestic feed requirements and ethanol blending consume an increasing portion of corn production, while favorable rainfall has improved the wheat outlook.

The Parana River and Rosario complex remain crucial for Argentina's export logistics, handling most bulk vessel shipments. Low river levels have imposed draft restrictions, reducing loading capacity by up to 12.5% and increasing per-metric ton shipping costs in 2022. The April 2025 strike disrupted grain loading during peak soybean season, highlighting the vulnerability of this transportation corridor. In response, traders are developing alternative transport routes, including trans-Andean truck lanes, and increased shipments through the Bahia Blanca port despite its limited capacity. Climate changes are affecting agricultural geography, with irrigated wheat production moving southward following rainfall patterns, while shorter-cycle corn hybrids improve crop reliability in northern regions. Precision agriculture technology, initially concentrated in the Pampas region, is expanding northward, supported by drone service providers seeking new markets. These changes are reshaping regional growth patterns and diversifying export routes in the Argentina grain market.

Recent Industry Developments

- May 2025: The Argentine government reduced export taxes on soybeans from 33% to 26% and lowered taxes on wheat and corn to 9.5%. These changes remain effective until June 2025.

- April 2025: Louis Dreyfus Company acquired a 22,000-metric tons grain and oilseed site in Santa Elena with river-barge capacity of 450 metric tons per hour.

- April 2025: IMF approved a USD 20 billion Extended Fund Facility aimed at stabilizing macro fundamentals and sustaining 5.5% real GDP growth in 2025.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Argentina grains market as the total annual value, in US dollars, of domestically produced plus directly imported cereals, pulses, and oilseeds that are traded in bulk prior to any industrial processing or retail packaging. The covered crops include corn, wheat, barley, sorghum, rice, soybeans, sunflower seed, chickpeas, and related minor grains.

Scope exclusion: processed derivatives such as flour, animal feed, biofuels, and edible oils are not counted.

Segmentation Overview

- By Commodity Type

- Cereals

- Production Analysis (Volume)

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Overview

- Key Supplying Markets

- Export Market Analysis

- Overview

- Key Destinations Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis (Volume)

- Pulses

- Production Analysis (Volume)

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Overview

- Key Supplying Markets

- Export Market Analysis

- Overview

- Key Destinations Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis (Volume)

- Oilseeds

- Production Analysis (Volume)

- Overview

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Overview

- Key Supplying Markets

- Export Market Analysis

- Overview

- Key Destinations Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Seasonality Analysis

- Production Analysis (Volume)

- Cereals

Detailed Research Methodology and Data Validation

Primary Research

Multiple touchpoints with growers' cooperatives, grain elevator operators, port inspection agents, and input suppliers across the Pampas, NOA, and NEA regions validated harvested volumes, average farm-gate prices, and informal storage losses. Follow-up calls with traders in Rosario and Bahía Blanca helped fine-tune domestic versus export channel splits and typical payment lags, which shaped our working capital assumptions.

Desk Research

Mordor analysts began with authoritative public data sets such as the Ministry of Agriculture's "Estimaciones Agrícolas," USDA-FAS PSD reports, and the Buenos Aires Grain Exchange seasonal bulletins, which together map area planted, yields, and export volumes. Trade and FOB price trends were tracked through the International Grains Council, FAOSTAT, and customs shipment statistics, while weather anomalies were checked against INTA agro-meteorology dashboards. Subscription feeds from D&B Hoovers and Dow Jones Factiva supplied company revenue splits and news that helped align price assumptions with on-farm realities.

Regulatory insights on export taxes and currency policy were gathered from Official Gazette decrees and World Bank macro notes, giving context for margin swings that influence sowing decisions. The sources listed illustrate the mix; many additional government circulars, exchange circulars, and scholarly articles were reviewed to cross-check figures and definitions.

Market-Sizing & Forecasting

The top-down build starts with harvested tonnage by crop and multiplies it by annualized farm-gate prices, adjusted for quality discounts and on-farm retention. Results are sense-checked with a bottom-up roll-up of sampled elevator receipts and processor intake to avoid overstatement. Key model drivers include planted area trends released weekly by BAGE, average yield gains from precision seeding adoption rates, Up River FOB price series, export tax differentials, rainfall deviations from the 30-year mean, and domestic feed demand indexed to hog and poultry inventories. A multivariate ARIMA model projects each driver to 2030, and scenario stress tests are run for currency shocks and tariff shifts. Gaps in primary volumes are infilled using three-year moving averages before final triangulation.

Data Validation & Update Cycle

Outputs pass variance checks against independent crop export tallies and Statista trade values. Senior reviewers run anomaly screens, and models refresh every twelve months, with interim updates triggered by policy changes or extreme weather. A fresh review is completed just before report release so buyers see the most current view.

Why Mordor's Argentina Grains Baseline Inspires Confidence

Published estimates often diverge because firms choose different crop baskets, pricing points, and update rhythms. By anchoring values to audited production data and current farm-gate prices, Mordor minimizes scope drift and inflation mismatches that inflate or depress totals elsewhere.

Key gap drivers include some publishers bundling downstream milling and oil extraction revenue, others reporting only cereals, and several applying constant 2022 prices without currency re-indexing. Mordor reports the core grain pool, updates annually, and converts at the mid-year market exchange rate, giving planners a stable, transparent anchor.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 16.90 B (2025) | Mordor Intelligence | - |

| USD 30.10 B (2030) | Global Consultancy A | Adds flour, feed, and crushing revenues and keeps constant 2022 prices |

| USD 3.12 B (2024) | Industry Association B | Counts cereals only and limits scope to Buenos Aires production |

These comparisons show that while totals can swing widely, Mordor's disciplined scope selection, variable tracking, and annual refresh cadence deliver a balanced baseline that decision-makers can trace and replicate with public data.

Key Questions Answered in the Report

What is the current Argentina grain market size?

The Argentina grain market size is USD 18.24 billion in 2026 and is projected to reach USD 22.1 billion by 2031.

Which crop segment is growing fastest in Argentina’s grain market?

Cereals, led by corn and wheat, expand at a 4.03% CAGR, outpacing oilseeds and pulses.

How are biofuel policies influencing grain demand?

A higher biodiesel blend mandate of 7.5% and potential rise to 15% are redirecting more soybeans and corn into domestic fuel production, strengthening internal demand and price floors.

How significant are climate risks to Argentina’s grain output?

Persistent droughts have already reduced corn and soybean yields, and forecasts warn production could fall further without substantial investment in resilient seeds and water management.

What infrastructure projects may ease export bottlenecks?

The Capricorn Bioceanic Corridor, scheduled for completion in 2026–2027, could cut logistics costs by up to 40% and remove 15 days from transit times.

Page last updated on: