Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

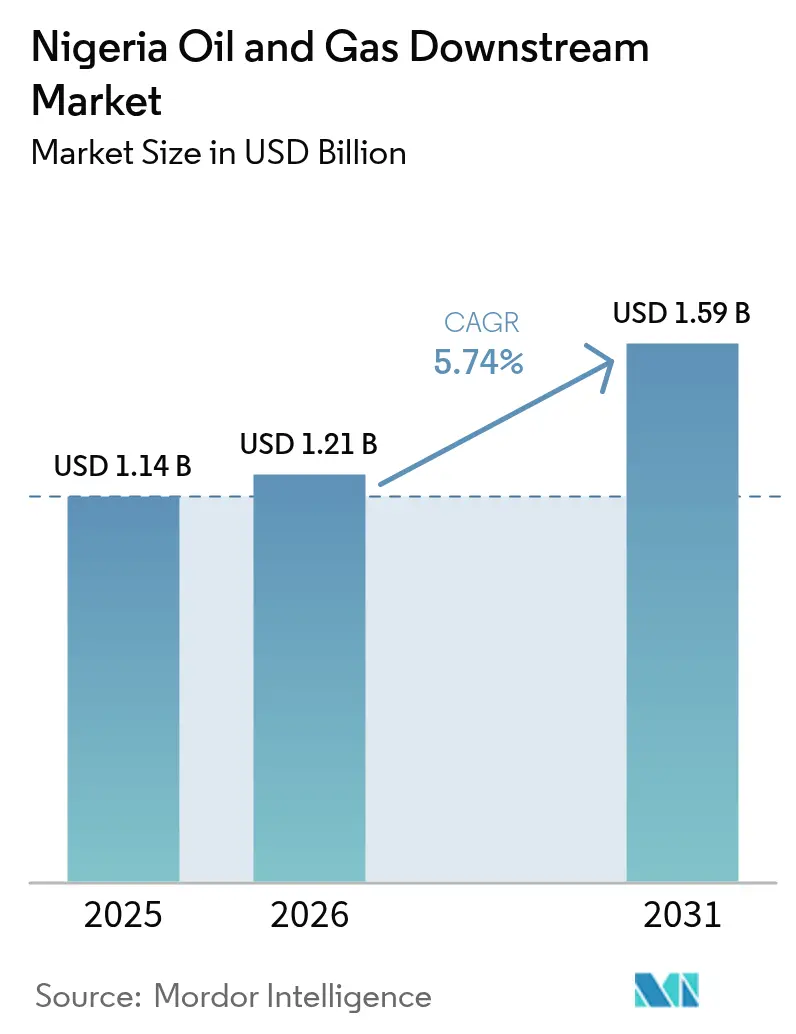

| Base Year Market Size (2025) | USD 1.14 Billion |

| Market Size (2026) | USD 1.21 Billion |

| Market Size (2031) | USD 1.59 Billion |

| Growth Rate (2026 - 2031) | 5.74% CAGR |

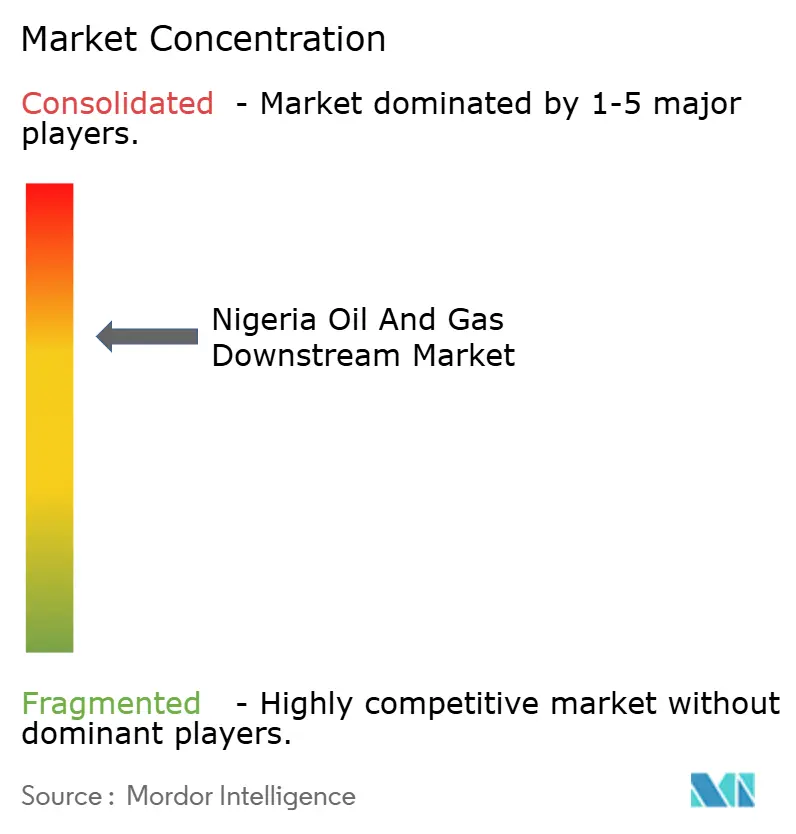

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Nigeria Oil And Gas Downstream Market Analysis by Mordor Intelligence

The Nigeria Oil And Gas Downstream market size is expected to grow from USD 1.14 billion in 2025 to USD 1.21 billion in 2026 and is forecast to reach USD 1.59 billion by 2031 at 5.74% CAGR over 2026-2031.

Rising local refining capacity, policy deregulation, and growing urban fuel demand anchor this expansion. The commissioning of the 650,000 barrels-per-day Dangote Refinery sharply reduces import dependence and pushes domestic output toward regional export surpluses. Flexible pricing after subsidy removal improves margins for private operators, while modular projects unlock participation for indigenous firms. Accelerated security operations in the Niger Delta further stabilize crude supply and boost investor confidence.

Key Report Takeaways

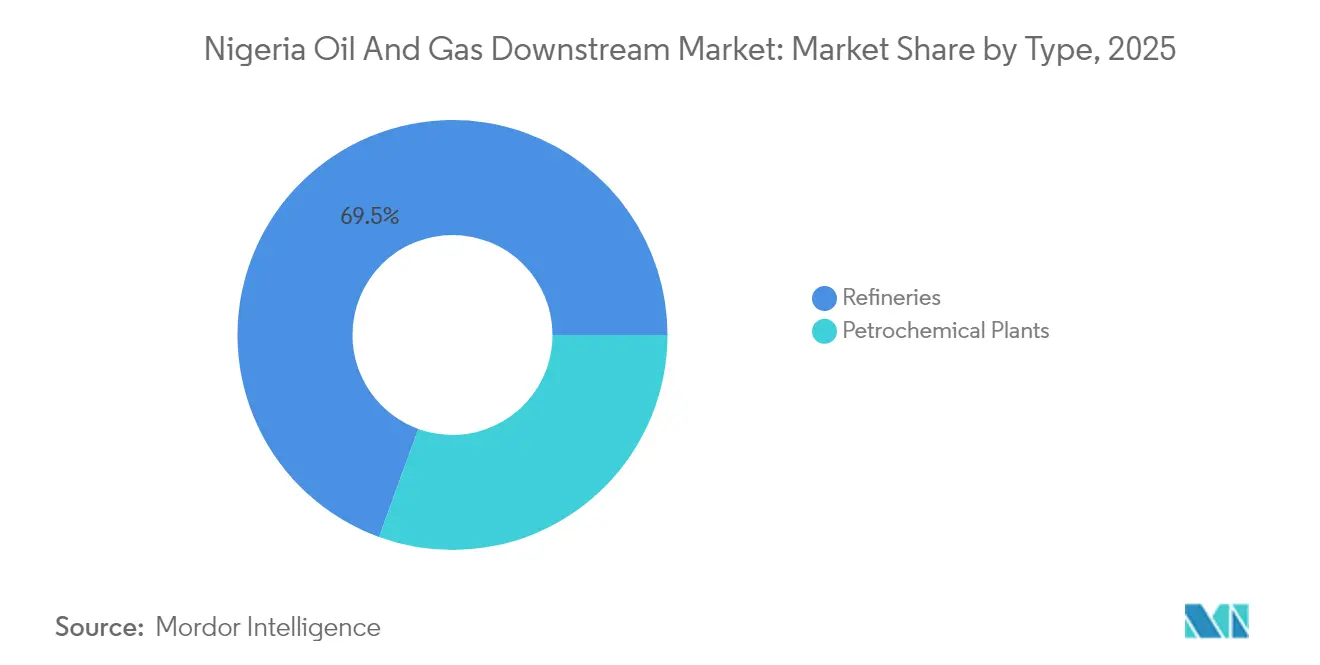

- By type, refineries led with 69.45% of Nigeria's oil & gas downstream market share in 2025; petrochemical plants are poised to expand at a 7.12% CAGR through 2031.

- By product type, refined petroleum products commanded a 74.15% share of the Nigeria oil & gas downstream market size in 2025, whereas petrochemicals recorded the fastest 6.86% CAGR to 2031.

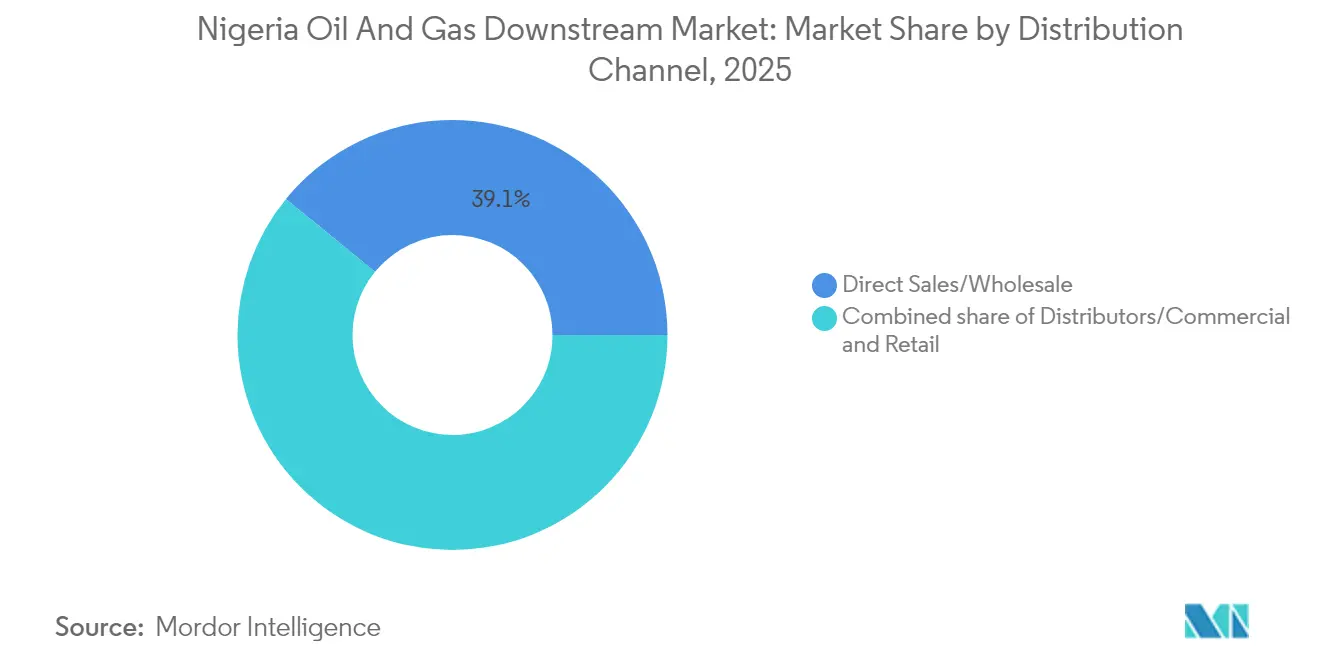

- By distribution channel, direct sales and wholesale accounted for a 39.10% revenue share in 2025, while retail distribution is projected to grow at a 6.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Nigeria Oil And Gas Downstream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid growth in domestic fuel demand | 1.2% | National, concentrated in Lagos, Abuja, Port Harcourt | Medium term (2-4 years) |

| Commissioning of Dangote Refinery boosting local supply | 1.8% | National, with export spillover to West Africa | Short term (≤ 2 years) |

| Government deregulation & subsidy removal policies | 1.0% | National, early implementation in major cities | Medium term (2-4 years) |

| Expansion of modular refinery projects in Niger Delta | 0.8% | Niger Delta states, primarily Rivers, Bayelsa, Delta | Long term (≥ 4 years) |

| Local-content law fostering indigenous participation | 0.6% | National, strongest in upstream-downstream integration | Long term (≥ 4 years) |

| Export potential to West Africa's short-supply markets | 0.7% | Regional, targeting Ghana, Benin, Togo markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Commissioning of Dangote Refinery Boosting Local Supply

The start-up of full gasoline runs at Dangote’s 650,000 barrels-per-day complex in September 2024 instantly raised domestic supply and freed USD 9 billion in annual import spending. NNPC initially acquires all gasoline output, smoothing distribution while the plant ramps to nameplate capacity. A dedicated 1,100 km subsea pipeline delivers Niger Delta crude directly to the facility, cutting historic transport penalties. Co-located petrochemical and fertilizer units deepen value capture and open export channels into West Africa. A 10-year gas-supply agreement from Shell’s Iseni field guarantees 100 million scf/d of feedstock to the polypropylene and methanol trains.[1]Natural Gas World, “Shell Inks Gas Supply Deal for Dangote Plant,” naturalgasworld.com

Government Deregulation and Subsidy Removal Policies

Executive orders issued in 2024 ended pump-price caps and transferred price setting to open market dynamics. This shift restored refinery economics, attracting USD 4.2 billion in private equity commitments within twelve months.[2]Nigerian National Petroleum Company Limited, “Corporate Presentation 2025,” nnpcgroup.com The Petroleum Industry Act 2021 now provides stable fiscal terms, while local-content directives mandate minimum indigenous equity, driving skills transfer. Although a temporary 3.3% of GDP subsidy reappeared during the 2024 election cycle, authorities reconfirmed a full rollback in early 2025, reinforcing investor confidence.

Expansion of Modular Refinery Projects in Niger Delta

Eighteen licensed modular plants, each sized 5,000-20,000 barrels per day, collectively add 215,000 barrels per day of incremental capacity by 2027. Lower capital expenditures, proximity to feedstock, and phased debottlenecking make the model attractive to local entrepreneurs. The Nigerian Content Development and Monitoring Board reports that 37,400 direct jobs have been generated to date, with an additional 72,000 anticipated during the expansion phases. State-funded gunboat patrols reduce vandalism on feeder pipelines, improving plant uptime.

Export Potential to West Africa’s Short-Supply Markets

Regional demand outstrips supply by 450,000 barrels per day, and Nigerian refiners target Ghana, Benin, and Togo, where import parities exceed domestic ex-gate prices by 12-18%. ECOWAS protocols eliminate most tariffs, while Lagos-Tema sailings average only three days, outperforming European cargoes in terms of freight cost and delivery time. Long-term offtake contracts signed in Q1 2025 secure Dangote's 5 million barrels of annual gasoline exports.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-price volatility affecting refinery margins | -0.9% | National, affecting all refineries | Short term (≤ 2 years) |

| Persistent pipeline vandalism & oil theft | -1.1% | Niger Delta region, onshore operations | Medium term (2-4 years) |

| Foreign-exchange scarcity for feedstock imports | -0.7% | National, import-dependent facilities | Short term (≤ 2 years) |

| ESG-driven funding constraints for fossil projects | -0.5% | International financing, major projects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Pipeline Vandalism and Oil Theft

Illicit taps on trunk lines siphon off 200,000 barrels per day, equal to USD 10 billion per year in lost revenues and deferred taxes. Multi-agency Operation Delta Safe deployed armed drones and attack helicopters in late 2024, achieving a 16.7% lift in national crude output within twelve months. Yet analysts note that dismantling the financial networks behind theft rings remains crucial for durable gains. The environmental liabilities from illegal “Kpo-fire” distillation add remediation costs that erode refinery cash flows.

Foreign-Exchange Scarcity for Feedstock Imports

Although the Nigeria oil & gas downstream market increasingly relies on local crude, legacy plants still import specialty grades. Declines in Brent prices from USD 82 to USD 65 per barrel in 2025 complicated a proposed USD 5 billion oil-backed loan, delaying cargo purchases and swelling demurrage bills. Foreign-currency regulations that require environmental bonds and license fees in USD tighten liquidity, illustrated by the aborted USD 860 million TotalEnergies asset sale when bank guarantees failed to clear.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Refineries Dominate Infrastructure Investment

Refineries captured 69.45% of Nigeria's oil & gas downstream market share in 2025 as the state prioritized energy security through domestic processing. The Nigeria oil & gas downstream market size attributable to refineries is projected to climb at a 5.45% CAGR, supported by the USD 18.5 billion Dangote complex and the December 2024 restart of Warri Refinery. Integrated operators secure feedstock via joint-venture upstream stakes, buffering margin volatility. Modern process units, such as continuous catalytic regenerators, raise gasoline yields and lower sulfur, aligning products with ECOWAS specifications.

Petrochemical plants, although currently smaller, are projected to grow at the fastest 7.12% CAGR through 2031. Indorama Eleme's latest debottlenecking initiative increases urea output to 3.8 million tonnes per year, while Shell-supported propane dehydrogenation units supply polypropylene lines. Modular refineries offer a learning curve for local investors, with quick payback periods that recycle cash into second-phase expansions.

By Product Type: Petrochemicals Drive Value Addition

Refined fuels held a 74.15% share of Nigeria's oil & gas downstream market size in 2025 as gasoline, diesel, and kerosene met transport and power demand. However, petrochemicals are expected to accelerate at a 6.86% CAGR on the back of Dangote's 900,000-tonne polypropylene train and a co-located 3 million-tonne ammonia-urea facility. Domestic fertilizer self-sufficiency reached 65% in 2025, resulting in USD 1.1 billion in savings on import costs.

Lubricants and specialty products occupy niche positions yet benefit from automotive fleet growth. International brands partner with local blenders to meet the rising demand for OEM quality grades, and synthetic lubricant penetration reaches 14% in urban centers. Government policy is increasingly rewarding value-added production through tax credits for chemical derivatives over basic fuels.

By Distribution Channel: Retail Networks Expand Market Access

Direct sales and wholesale retained 39.10% of revenue in 2025, anchored by bulk contracts with power plants and heavy industry. The Nigerian oil & gas downstream market size booked under retail outlets is forecast to rise at a 6.72% CAGR through 2031, as private station ownership increases following the removal of subsidies.

Urban roll-outs feature multi-service stations offering convenience retail, quick-service restaurants, and EV charging bays. The Midstream and Downstream Petroleum Regulatory Authority streamlined licensing in 2024, reducing the average permit time from 90 to 35 days. Digital payment platforms reduce cash leakage and provide real-time inventory visibility, enabling operators to optimize truck dispatches and minimize stockouts.

Geography Analysis

Lagos State anchors the Nigeria oil & gas downstream market as home to the Lekki Free Zone, where Dangote’s 2,635-hectare complex operates. The region handles 60% of national refined-product sea imports and now channels rising export volumes to neighboring states. Proximity to deep-draft jetties reduces freight costs and facilitates the handling of petrochemical bulk.

The Niger Delta remains the crude heartland, driving feedstock availability for both mega and modular plants. Security operations have reduced reported vandalism incidents by 28% year-over-year, yet insurance premiums remain elevated. Warri and Port Harcourt refineries benefit from pipeline interconnections that feed both domestic and export tanks.

Northern demand centers such as Abuja and Kano rely on overland trucking and emerging rail corridors that extend 1,200 km from southern terminals. Transport margins add USD 40 per m³ on average, underpinning the economic case for a proposed 50,000 barrels-per-day Kaduna modular plant, slated for commissioning in 2027. Regional pipelines under discussion would relieve road congestion and cut product losses.

West Africa offers a natural outlet for surplus gasoline and chemicals. Ghana imported USD 48.6 million worth of Nigerian petroleum in 2022 and signed a framework agreement in 2025 for a long-term supply of 35,000 barrels per day at Tema. Benin and Togo seek similar deals under ECOWAS rules that waive import levies, giving Nigerian exporters a 4-cent-per-liter landed cost advantage over European cargoes.

Competitive Landscape

The Nigeria oil & gas downstream market contains a blend of state-owned incumbents, international majors, and agile local independents. NNPC Limited retains pivotal influence through equity stakes in three legacy refineries and a 20% share in Dangote. Its trading arm markets one-third of national fuel demand and administers strategic stockpiles.

The Dangote Group commands a significant capacity but opts for a range of 5,000 to 20,000 barrels per day, serving proximate markets and catering to marine bunkering needs through an export-led model that diversifies its revenue. The integrated complex covers refining, petrochemicals, and fertilizer, capturing value across the hydrocarbon chain. Shell, TotalEnergies, and ExxonMobil are repositioning toward offshore production while maintaining branded fuel retail and LPG distribution networks. Shell’s USD 2.4 billion sale of SPDC to Renaissance Group finalizes a multi-year divestment from onshore blocks, yet keeps the company invested in the high-margin Bonga North deep-water project.[4]Shell Plc, “Transaction Completion: SPDC Sale,” shell.com

Indigenous firms such as Waltersmith, Azikel, and Niger Delta Petroleum refine 5,000-20,000 barrels per day, serving proximate markets and catering to marine bunkering. Competitive focus centers on supply chain integration, digital asset monitoring, and ESG compliance to unlock more affordable financing. Operators deploying fiber-optic pipeline surveillance report 45% fewer leak incidents within the first year of installation. Retail segment rivalry intensifies as Mobil, Oando, and Ardova expand premium forecourts that bundle non-fuel services.

Nigeria Oil And Gas Downstream Industry Leaders

NDEP plc

Nigerian National Petroleum Corporation

Indorama Eleme Petrochemicals Limited.

KBR Inc.

Midoil Refining & Petrochemicals Company Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Shell completed the USD 2.4 billion divestment of Shell Petroleum Development Company of Nigeria Limited to Renaissance Group, offering up to USD 2.5 billion in transition funding.

- December 2024: Shell reached a final investment decision on the Bonga North deep-water project, comprising 16 wells, with first oil targeted for 2027.

- December 2024: Federal approval confirmed Shell’s onshore asset sale after initial regulatory reservations about Renaissance’s technical capacity.

- December 2024: Rivers State donated six military-grade gunboats to the Nigerian Navy, strengthening the protection of critical pipelines.

Nigeria Oil And Gas Downstream Market Report Scope

Downstream operations are oil and gas processes that occur after the production phase to the point of sale. They are the final step in extracting the oil and gas from the ground and delivering them to the end user.

The Nigerian oil and gas downstream market is segmented by sector. By sector, the market is segmented into refining, petrochemical plants, and retail sales. The market sizing and forecasts have been done based on refining capacity (million barrels per day).

By Type

| Refineries |

| Petrochemical Plants |

By Product Type

| Refined Petroleum Products |

| Petrochemicals |

| Lubricants |

By Distribution Channel

| Direct Sales/Wholesale |

| Distributors/Commercial |

| Retail |

| By Type | Refineries |

| Petrochemical Plants | |

| By Product Type | Refined Petroleum Products |

| Petrochemicals | |

| Lubricants | |

| By Distribution Channel | Direct Sales/Wholesale |

| Distributors/Commercial | |

| Retail |

Key Questions Answered in the Report

What is the forecast value of the Nigeria oil & gas downstream market by 2031?

The sector is projected to reach USD 1.59 billion by 2031, expanding at a 5.74% CAGR.

How much capacity does the Dangote Refinery add to Nigeria’s system?

The plant introduces 650,000 barrels-per-day of refining capacity plus integrated petrochemical and fertilizer units.

Which product segment is growing fastest within Nigeria’s downstream sector?

Petrochemicals, driven by new integrated complexes, are forecast to grow at 6.86% CAGR through 2031.

How is subsidy removal affecting retail fuel distribution?

Market-based pricing has spurred private investment, with retail networks expected to grow at 6.72% CAGR.

What security measures are in place to curb pipeline vandalism?

Operation Delta Safe deploys drones, naval patrols, and community engagement, reducing incidents by 28% over the past year.

Which West African markets are key targets for Nigerian refined-product exports?

Ghana, Benin, and Togo are primary destinations due to close proximity and existing trade agreements.

Page last updated on: