Ambient Assisted Living Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 13.48 Billion |

| Market Size (2031) | USD 35.84 Billion |

| Growth Rate (2026 - 2031) | 21.60% CAGR |

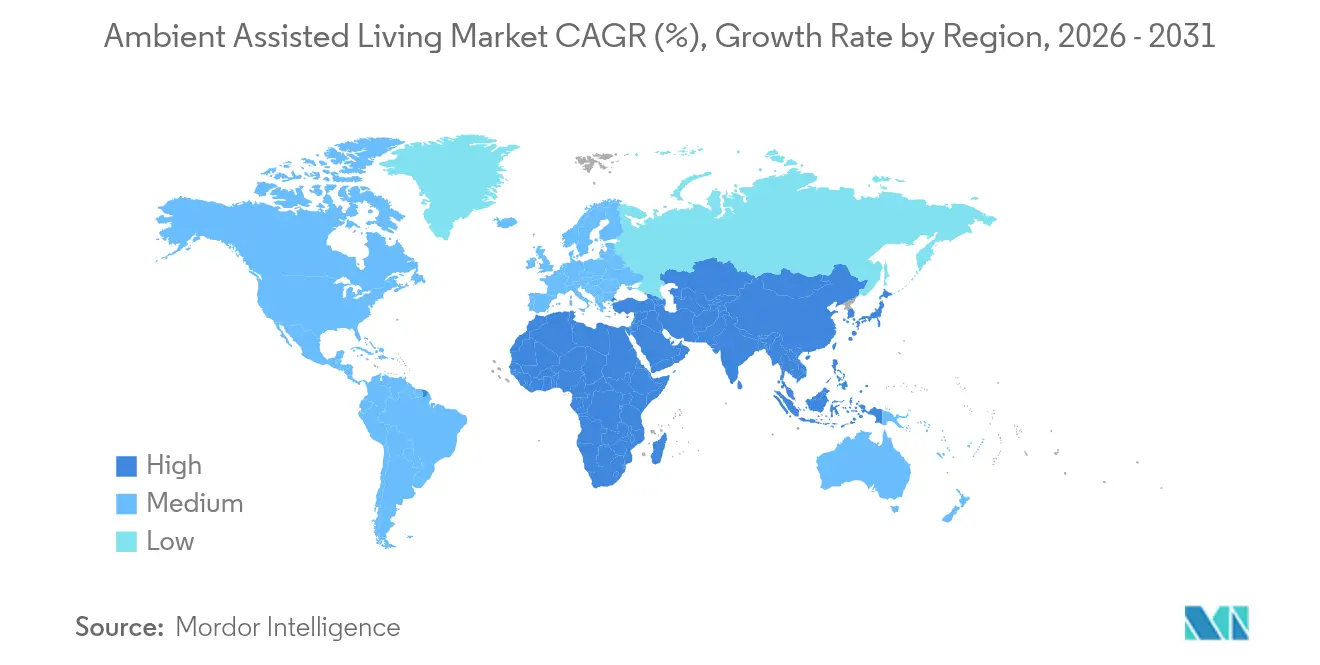

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

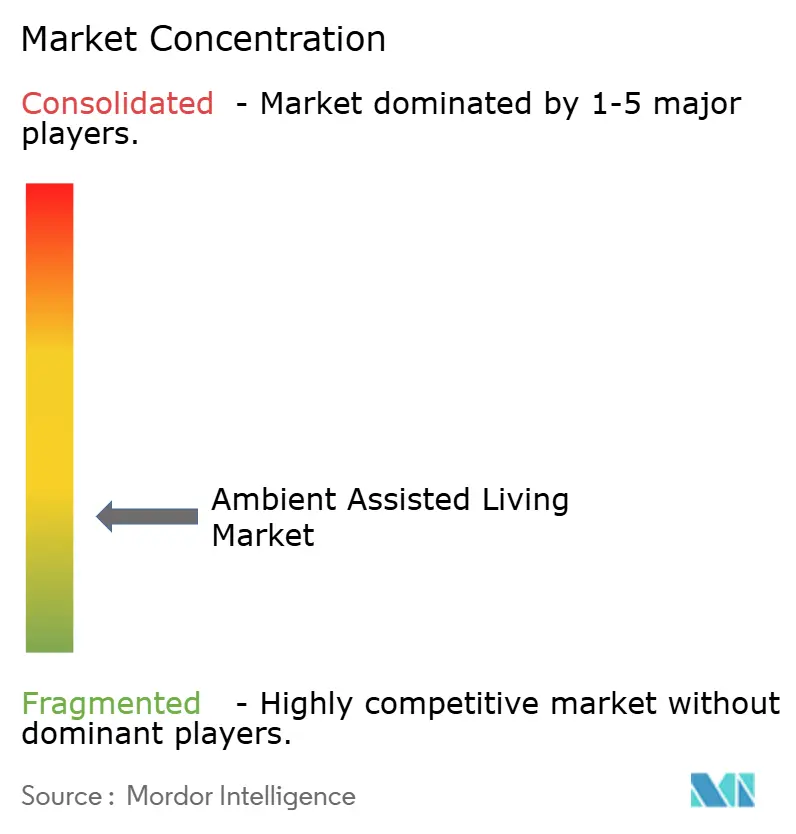

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ambient Assisted Living Market Analysis by Mordor Intelligence

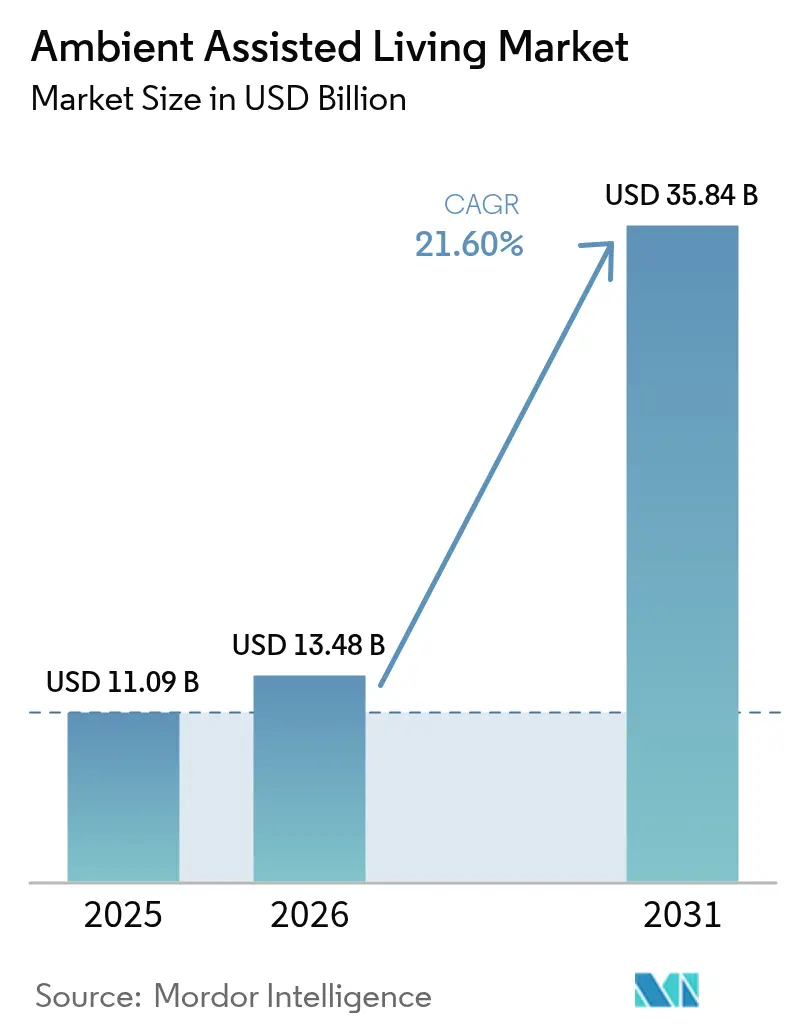

The Ambient Assisted Living market size was valued at USD 11.09 billion in 2025 and estimated to grow from USD 13.48 billion in 2026 to reach USD 35.84 billion by 2031, at a CAGR of 21.6% during the forecast period (2026-2031). Growth reflects the collision of demographic aging, supportive reimbursement reforms, and the steady commercialization of AI-driven home health technologies. Policy makers now view technology-enabled aging in place as critical national infrastructure, while payers recognize that proactive digital monitoring curbs hospital readmissions and long-term care costs. As sensor costs fall and edge computing matures, vendors are integrating predictive analytics, robotics, and voice assistants into unified platforms that extend independent living and alleviate caregiver shortages. Incumbents and start-ups alike are scaling partnerships to bundle hardware, software, and managed services for both residential and institutional buyers, positioning the Ambient Assisted Living market for sustained double-digit expansion through the decade.

Key Report Takeaways

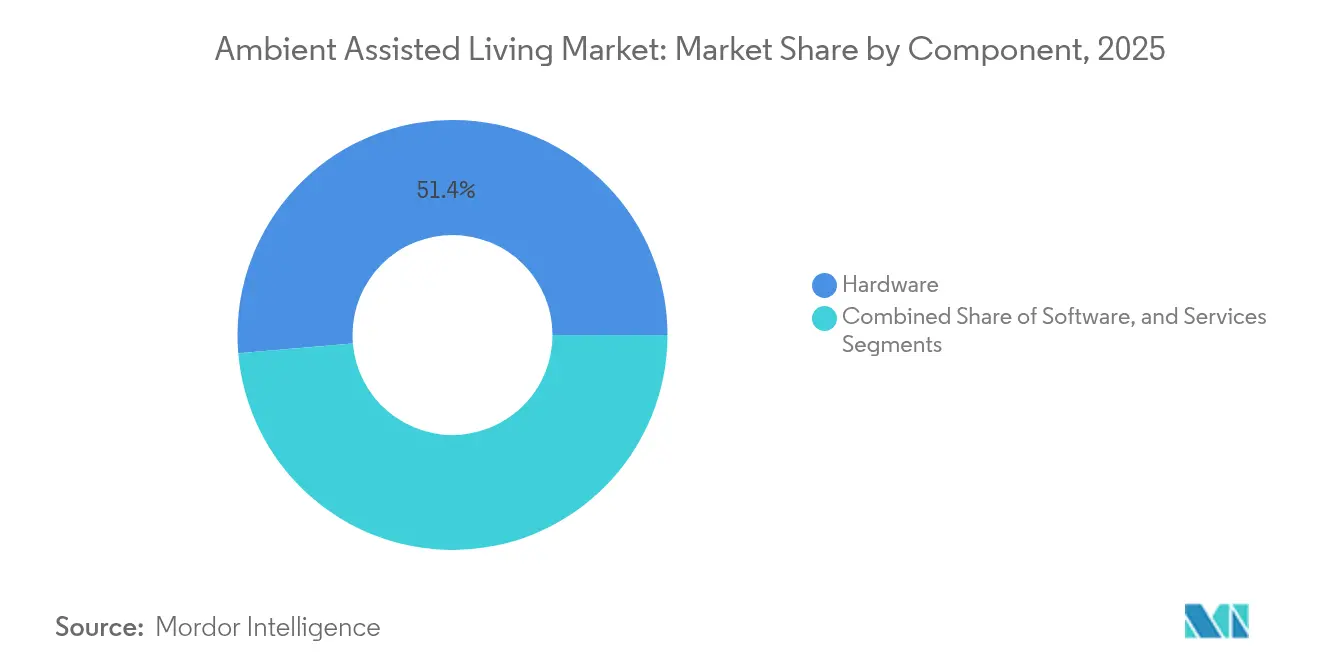

- By component, hardware led with 51.35% revenue share in 2025; services are projected to grow at a 23.9% CAGR to 2031.

- By technology, smart-home automation commanded 47.85% of the Ambient Assisted Living market share in 2025, while social and companion robotics are forecast to expand at 22.85% CAGR.

- By system function, safety and security accounted for a 29.75% share of the Ambient Assisted Living market size in 2025; vitality and wellness is advancing at 22.75% CAGR through 2031.

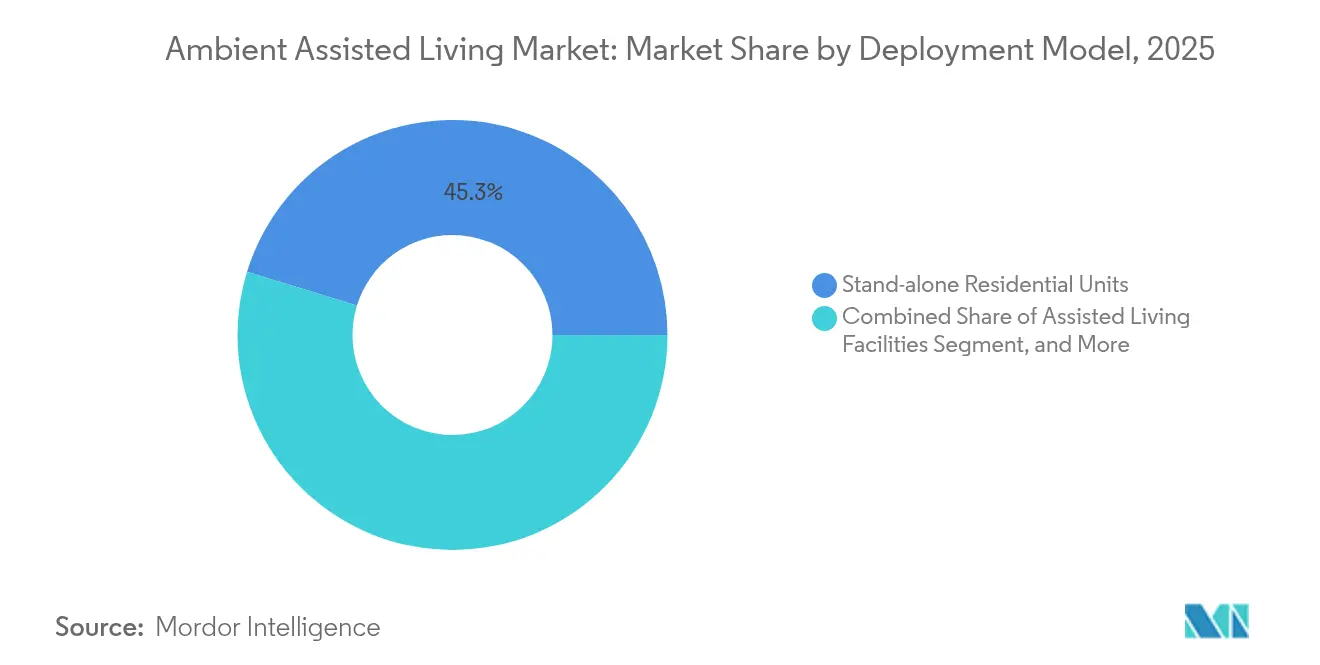

- By deployment model, stand-alone residential units held 45.25% of 2025 revenue, whereas senior-care homes will post the fastest 23.5% CAGR.

- By age group, adults aged 70-79 represented 44.20% of 2025 revenue; the 80+ cohort is slated for 22.7% CAGR.

- By geography, Europe led with 33.65% revenue share in 2025, but Asia-Pacific will deliver the highest 23.1% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ambient Assisted Living Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid policy shifts toward ageing-in-place reimbursement models in OECD economies | +4.20% | North America and Europe | Medium term (2-4 years) |

| Surge in smart-home penetration among 65+ households in North America and Europe | +3.80% | North America and Europe | Short term (≤ 2 years) |

| AI-driven predictive analytics lowering false-alarm rates in emergency response | +3.50% | Global | Medium term (2-4 years) |

| 5G / fibre roll-outs enabling low-latency remote care services across Asia | +3.10% | Asia-Pacific | Long term (≥ 4 years) |

| EU Horizon Europe and AAL-Programme grants accelerating start-up adoption | +2.90% | Europe | Short term (≤ 2 years) |

| Declining costs of edge sensors and wearables | +2.70% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Policy Shifts Toward Aging-in-Place Reimbursement Models

Medicare Advantage began covering non-medical home supports in 2024, converting formerly out-of-pocket services into reimbursable benefits that directly fund Ambient Assisted Living solutions [1]OECD, “Is Care Affordable for Older People?” oecd.org. Similar parity is emerging in Medicaid Home and Community-Based Services, allowing payers to substitute costly institutional beds with sensor-enhanced home care. Across OECD economies, long-term care budgets are projected to rise sharply by 2050, reinforcing legislative momentum to subsidize proactive digital monitoring. These reforms reposition Ambient Assisted Living technologies from discretionary purchases to reimbursable care, enlarging the total addressable market and lowering adoption friction for health-system buyers.

Surge in Smart-Home Penetration Among 65+ Households

Older adults accelerated smart-device adoption during the pandemic, and by 2024 smartphone usage exceeded 80% among 55- to 65-year-olds in multiple high-income countries. Voice interfaces, ambient sensors, and connected appliances now integrate easily into the domestic environment, allowing providers to bundle fall detection, medication reminders, and social-engagement tools in one installation. Pilot programs funded through EU initiatives such as PHArA-ON demonstrated that passive ambient sensors achieved higher acceptance than wearables among frail seniors, supporting hardware strategies that minimize lifestyle disruption while collecting richer datasets for clinicians.

AI-Driven Predictive Analytics Lowering False-Alarm Rates

Machine-learning models trained on multimodal sensor streams detect health deterioration up to two weeks in advance and achieve over 96% accuracy in anomaly recognition [2]Springer, “Smart Education and e-Learning,” link.springer.com. This improvement mitigates the “alarm fatigue” that once plagued tele-care and encourages payers to reimburse continuous monitoring. Vendors embedding edge AI chips reduce latency to sub-second response times, enabling closed-loop safety interventions such as automatic lighting and caregiver call-outs. Hospitals piloting these platforms report measurable declines in emergency admissions and overnight observation costs, adding ROI evidence that further fuels Ambient Assisted Living market adoption.

5G / Fibre Roll-outs Enabling Low-Latency Remote Care Services Across Asia

Asia-Pacific governments are fast-tracking 5G coverage to extend telehealth to urban and rural populations. Japan’s National Broadband Plan and China’s smart-senior-care guidelines fund high-bandwidth networks capable of supporting 4K video and real-time vital-sign streaming. Pilot deployments across South Korea’s multiresident facilities show reliable sub-20-millisecond latency, allowing clinicians to supervise rehabilitation exercises remotely and invoke robotics for bedside assistance. As connectivity barriers fade, the Ambient Assisted Living market expands from simple home alarms to sophisticated mixed-reality physical-therapy and social-robotics programs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented interoperability standards hindering unified caregiver dashboards | -2.80% | Global | Medium term (2-4 years) |

| Privacy and data-sovereignty rules (GDPR, HIPAA) limiting cross-border monitoring | -2.10% | Global, particularly EU and US | Long term (≥ 4 years) |

| Low digital literacy among 75+ cohort in rural regions | -1.90% | Global, particularly rural areas | Medium term (2-4 years) |

| Reimbursement gaps for non-clinical AAL services in emerging markets | -1.60% | Emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented Interoperability Standards Hindering Unified Caregiver Dashboards

Residential and institutional buyers still juggle multiple proprietary portals because device makers interpret health-data templates differently. Despite progress in initiatives such as the United States Core Data for Interoperability and Europe’s EEHRxF, implementation remains uneven [3]Office of Disease Prevention and Health Promotion, “United States Core Data for Interoperability,” odphp.health.gov. Integration costs suppress volume deployments, particularly in small home-care agencies that lack IT budgets. The absence of plug-and-play semantics delays cross-vendor analytics, limits predictive-model accuracy, and forces procurement teams to lock in single-brand ecosystems, creating switching frictions that mute near-term market acceleration.

Privacy and Data-Sovereignty Rules Limiting Cross-Border Monitoring

GDPR classifies ambient sensor data as health information, triggering strict transfer constraints that complicate cloud architectures. HIPAA introduces additional encryption and audit requirements that lift compliance spend for multinational providers. These overlapping mandates discourage global tele-care roll-outs and compel vendors to maintain region-specific data centers, capping economies of scale. While regulatory clarity is improving, risk-averse hospital systems often delay purchase decisions until legal frameworks mature, shaving incremental points from the global Ambient Assisted Living market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Dominance Meets Service Innovation

Hardware captured a 51.35% revenue share in 2025, underpinned by volume shipments of passive infrared sensors, door contacts, and wearables that anchor most installations. Unit prices dropped below USD 10 for basic motion sensors in 2025, widening access for mid-income households. Demand is shifting from single-function devices to multi-sensor modules that integrate environmental, biometric, and location data feeds. Vendors benefit from silicon advances that squeeze AI inference engines onto battery-powered tags, prolonging field life and trimming maintenance.

Services are scaling faster, projected at 23.9% CAGR to 2031 as providers monetize managed monitoring, AI-based alert triage, and 24/7 virtual call centers. Payers favor subscription bundles that combine hardware amortization, software licenses, and professional response teams under one capitated fee. The Ambient Assisted Living market size for service offerings is set to more than triple within five years, creating acquisition targets for telecom operators seeking recurring revenue diversification. Software layers add stickiness; platforms offering open APIs and remote firmware management reduce truck rolls and improve gross margins.

By Technology: Smart Homes Lead, Robotics Accelerate

Smart-home automation retained 47.85% revenue in 2025 by piggybacking on mature consumer ecosystems such as Zigbee, Z-Wave, and Wi-Fi. Voice assistants now integrate medication reminders, lighting cues, and caregiver check-ins without custom wiring, cutting installation times by 30%. Interoperability with mainstream devices positions vendors to upsell health services alongside entertainment subscriptions, broadening household reach.

Social and companion robotics, forecast to grow 22.85% CAGR, is transitioning from pilot novelty to scalable product line as natural-language processing and haptic feedback humanize interactions. Japan’s government injected more than USD 300 million into care-robot RandD programs, enabling rapid commercialization and export of turnkey robotic aides. Modular designs facilitate cost-effective customization for cultural context, and case studies report statistically significant reductions in loneliness metrics among isolated seniors. Vendors integrating robotics with telehealth portals enable seamless continuity of care, raising switching barriers and fueling the next leg of Ambient Assisted Living market expansion.

By System Function: Safety Foundation Enables Wellness Innovation

Safety and security applications accounted for 29.75% of 2025 revenue, reflecting universal demand for fall detection, door egress alerts, and emergency call buttons. Hospitals discharge planners increasingly prescribe home-monitoring kits at the point of exit to cut readmissions, bolstering volume growth. Legal mandates in several EU states require alarm systems in care homes, cementing baseline demand.

Vitality and wellness solutions are scaling at a 22.75% CAGR, propelled by AI models that flag declining mobility, dehydration, or cognitive impairment before acute events occur. Insurers pilot premium discounts tied to adherence metrics captured by ambient sensors, creating behavioral nudges with immediate economic incentives. The Ambient Assisted Living market size for wellness tools is expanding rapidly as evidence mounts that continuous behavioral coaching reduces long-term expenditure on chronic-disease management. Bundling safety and wellness under one dashboard accelerates cross-sell penetration and underpins long-run platform stickiness.

By Deployment Model: Residential Independence Drives Institutional Innovation

Stand-alone residential models retained 45.25% revenue share in 2025 as policy trends and family preferences converge on aging in place. Telecom operators bundle LTE routers, cloud storage, and emergency call services on single bills, lowering adoption friction for mass-market consumers. Integration with consumer voice assistants further simplifies on-boarding and broadens demographic reach.

Senior-care homes are poised for a 23.5% CAGR, leveraging Ambient Assisted Living platforms to stretch lean staffing budgets and comply with stricter safety regulations. Operators deploy room-level location analytics to predict wandering events and dynamically allocate personnel, delivering measurable productivity savings. Proof-of-concept studies document 25% fewer night-time falls and shortened emergency-response windows, strengthening ROI narratives driving procurement. Hospitals and rehabilitation clinics extend AAL systems to monitor post-acute patients at home, creating hybrid care pathways that blur institutional and residential boundaries, and deepening market opportunity.

By Age Group: 70–79 Dominance Shifts Toward 80+ Growth

Adults aged 70–79 secured 44.20% of 2025 spend, reflecting their blend of technology familiarity and rising health-support needs. This cohort adopts mobile apps and wearables readily, empowering vendors to deliver smartphone-centered subscription models. Market surveys reveal higher willingness to share health data within this age band, accelerating data-driven product refinement cycles.

The 80+ segment, predicted to grow 22.7% CAGR, brings more acute care needs and lower tech affinity, encouraging focus on passive sensing and voice navigation. Robotics that provide physical object retrieval and conversational engagement resonate strongly with this group, reducing caregiver burden. As global life expectancy edges upward and fertility rates fall, the 80+ population will increase by more than 50% before 2030, prompting payers to prioritize preventive home monitoring. Providers designing frictionless interfaces and battery-free sensor grids will gain outsized share in this emergent growth pocket of the Ambient Assisted Living market.

Geography Analysis

Europe commanded 33.65% revenue in 2025, supported by Horizon Europe grants that subsidize pilot deployments and build a pipeline of procurement-ready case studies ec.europa.eu. Mandatory emergency-response regulations in Nordic and DACH markets created predictable demand baselines, while GDPR compliance frameworks cultivated user trust. National health systems are increasingly integrating AAL alerts into electronic health records, smoothing clinician workflows and bolstering medical-device-class certification pathways. Vendors partnering with home-care agencies benefit from publicly funded reimbursement schemes that guarantee payment, anchoring recurring revenue streams.

Asia-Pacific will generate the fastest 23.1% CAGR as governments confront unprecedented aging curves. Japan’s robotics subsidies, China’s smart-senior-care national plan, and South Korea’s 5G-linked chronic-disease monitoring pilots illustrate policy-led market making. Urban density aids installation economics; sensor distribution costs fall when networks can service hundreds of apartments per vertical tower. However, rural digital divide persists, prompting satellite connectivity trials to ensure equitable access. Regional players collaborating with telecom carriers accelerate rollout by embedding AAL-ready firmware on consumer routers, shrinking time-to-market and fueling Ambient Assisted Living market acceleration across the region.

North America maintains a large installed base, propelled by Medicare Advantage reimbursement and private insurer incentives. Hospital systems adopt predictive analytics to trim costly readmissions and meet value-based care targets. Venture funding remains vigorous, with AI-centric start-ups attracting rounds above USD 30 million that finance productization and geographic scaling. The United States is also a leading exporter of software middleware, licensing data-integration stacks to European and Asian device makers. Canada’s single-payer system conducts province-level procurement pilots, and lessons learned are forming national interoperability blueprints that could unlock broader adoption by 2027.

Competitive Landscape

The Ambient Assisted Living market is fragmented; the top five players hold roughly 28% of global revenue. Philips leverages its health-system relationships to bundle connected lighting, sleep diagnostics, and emergency-response subscriptions, while Tunstall focuses on tele-care software embedded into national call-center frameworks. Legrand exploits channel synergies with its electrical-wiring portfolio to position resident-room infrastructure.

Strategic partnerships are the dominant scaling tactic. ASSA ABLOY’s acquisition of 9Solutions added AI-based real-time location services, strengthening its lock-hardware business with predictive safety features. Finland’s Cozify partnered with Vivago to integrate smart-home gateways with medical alarm wearables, delivering a single-invoice solution that resonates with municipal home-care agencies. Start-ups differentiate through edge analytics; Sensi.AI’s Series B funding will finance expansion into the US rehab-chain segment, where its audio-pattern recognition promises early detection of sepsis and urinary-tract infections.

Intellectual-property filings center on low-power radar sensing, emotion-recognition algorithms, and privacy-preserving federated learning. Patent race intensity is highest in Japan and the United States, where public research institutes co-innovate with mid-cap robotics firms. Vendor success increasingly depends on ecosystem orchestration rather than component innovation: platforms that aggregate third-party apps, expose open APIs, and support insurer billing codes accumulate network effects that raise migration costs for institutional buyers. Early-stage disruptors targeting rural and middle-income regions with low-bandwidth adaptive architectures may yet capture under-served markets and upend incumbent share.

Ambient Assisted Living Industry Leaders

Koninklijke Philips N.V.

Tunstall Healthcare Group

Legrand SA

Bosch Security & Safety Systems

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Caring hosted Sompocare to showcase real-time fall-detection algorithms in fully instrumented facilities, illustrating cross-border know-how transfer.

- March 2025: NtelCare allied with Vayyar to commercialize radar-based monitoring that detects bed exits and falls without cameras, enhancing dignity and cultural acceptance.

- January 2025: Panasonic unveiled Umi, an AI wellness assistant integrating voice chat and third-party services, signaling its pivot toward family-centric Ambient Assisted Living bundles.

- January 2025: Kami Vision released an AI fall-detection camera that processes images locally to preserve privacy while reducing response times.

Global Ambient Assisted Living Market Report Scope

The study looks at the current market situation and the most important factors that affect the ambient assisted living (AAL) industry in different parts of the world. The study also looks at the market for ambient assisted living, which includes products and services for accident detection and activity monitoring, emergency alarms, and other connected products that help older people live independently and make better health choices.

The study also looks at how the market works for different kinds of products and countries in terms of their trends, changes, and predictions of demand. The competitive landscape includes profiles of the most important vendors. These profiles include an overview of the vendor's business, changes in segments and regions, product offerings, strategies, and new developments.

The global ambient assisted living (AAL) market is divided by type of solution (hardware, emergency services), geography (North America, Europe, and Asia-Pacific), and market size and forecasts are given in terms of value (USD million) for all of these segments.

| Hardware | Sensors |

| Actuators | |

| Wearable and Smart Devices | |

| Smart Appliances | |

| Software (AI and Analytics Platforms, Middleware and Device Management, Security and Privacy) | |

| Services (Installation and Integration, Managed Services, Emergency Response and Monitoring) |

| Smart Home and Automation |

| Telehealth and Telecare |

| Wearable Devices |

| Social and Companion Robotics |

| Safety and Security |

| Communication and Connectivity |

| Health and Medical Assistive |

| Mobility and Transport |

| Vitality and Wellness |

| Stand-alone Residential Units |

| Assisted Living Facilities |

| Senior Care Homes |

| Hospitals and Clinics |

| 60-69 Years |

| 70-79 Years |

| 80+ Years |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia Pacific | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordics (Sweden, Denmark, Norway, Finland) | ||

| Rest of Europe | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Qatar | ||

| Kuwait | ||

| Bahrain | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Kenya | ||

| Rest of Africa | ||

| By Component | Hardware | Sensors | |

| Actuators | |||

| Wearable and Smart Devices | |||

| Smart Appliances | |||

| Software (AI and Analytics Platforms, Middleware and Device Management, Security and Privacy) | |||

| Services (Installation and Integration, Managed Services, Emergency Response and Monitoring) | |||

| By Technology | Smart Home and Automation | ||

| Telehealth and Telecare | |||

| Wearable Devices | |||

| Social and Companion Robotics | |||

| By System Function | Safety and Security | ||

| Communication and Connectivity | |||

| Health and Medical Assistive | |||

| Mobility and Transport | |||

| Vitality and Wellness | |||

| By Deployment Model | Stand-alone Residential Units | ||

| Assisted Living Facilities | |||

| Senior Care Homes | |||

| Hospitals and Clinics | |||

| By Age Group | 60-69 Years | ||

| 70-79 Years | |||

| 80+ Years | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Australia | |||

| New Zealand | |||

| Rest of Asia Pacific | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Nordics (Sweden, Denmark, Norway, Finland) | |||

| Rest of Europe | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Qatar | |||

| Kuwait | |||

| Bahrain | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Kenya | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the Ambient Assisted Living market?

The market is valued at USD 13.48 billion in 2026 and is projected to reach USD 35.84 billion by 2031.

Which region leads Ambient Assisted Living adoption today?

Europe holds the largest share at 33.65% of 2025 revenue, supported by EU funding and clear regulatory frameworks.

What component segment is growing fastest?

Services are forecast to expand at 23.9% CAGR, driven by managed monitoring and emergency-response subscriptions.

How will robotics influence market growth?

Social and companion robotics are set to grow at 22.85% CAGR as natural-language and haptic technologies humanize interactions and reduce loneliness.

Page last updated on: