Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 7.14 Billion |

| Market Size (2026) | USD 7.30 Billion |

| Market Size (2031) | USD 8.29 Billion |

| Growth Rate (2026 - 2031) | 2.58% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Algeria Oil And Gas Upstream Market Analysis by Mordor Intelligence

The Algeria Oil And Gas Upstream Market size is projected to expand from USD 7.14 billion in 2025 and USD 7.30 billion in 2026 to USD 8.29 billion by 2031, registering a CAGR of 2.58% between 2026 to 2031.

Investment momentum is rebuilding as Sonatrach and its partners channel the bulk of a USD 60 billion five-year budget into brownfield optimization, reserve boosting at Hassi R’Mel and Hassi Messaoud, and new risk-service acreage that appeals to Asian national oil companies. European energy-security concerns are reinforcing a strategic tilt toward natural-gas projects linked to the TransMed and Medgaz pipelines, while LNG back-fill at Skikda and Arzew underpins additional upstream gas spending. Production-maintenance capex, digital drilling tools that cut well times by one-third, and flare-recovery programs that freed up 0.4 billion m³ of gas in 2023 are helping offset maturity-driven declines in crude output. Offshore and unconventional prospects are advancing from a low base, supported by Chevron’s Mediterranean feasibility study and ExxonMobil’s shale-gas talks, but still face longer lead times and higher costs than onshore conventional activity.

Key Report Takeaways

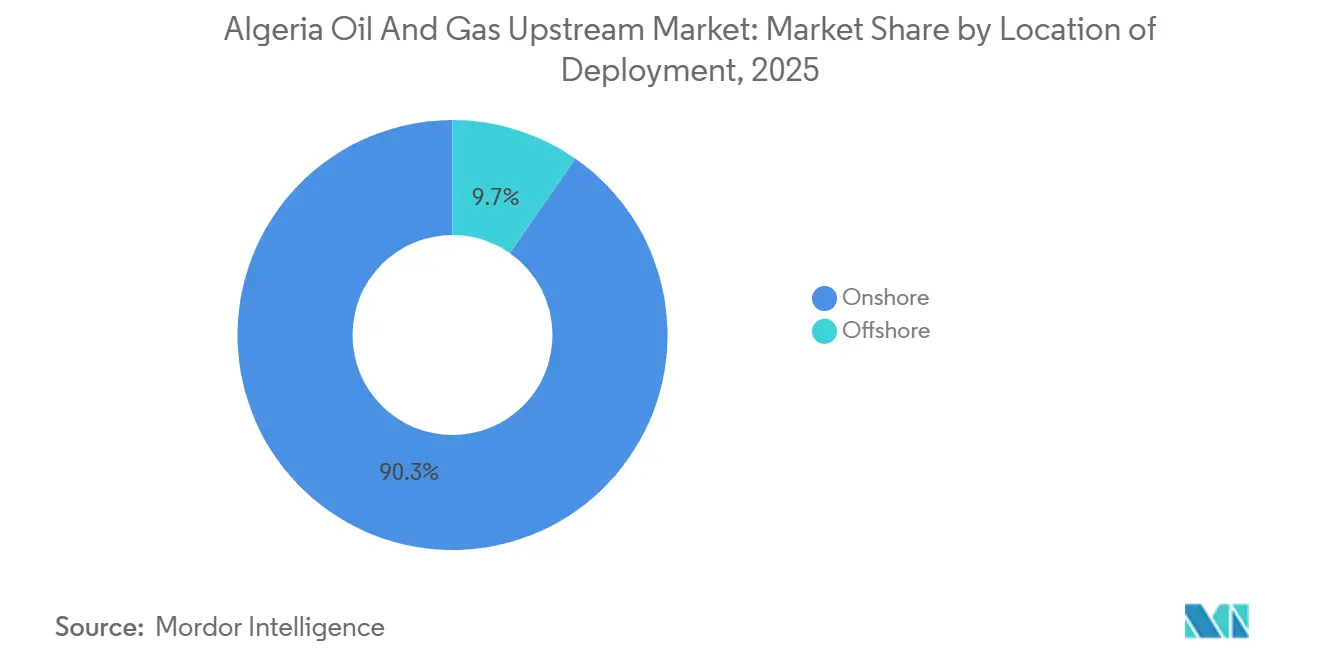

- By location of deployment, onshore operations led with 90.3% share of the Algeria oil and gas upstream market in 2025, while offshore development is projected to expand at a 6.0% CAGR through 2031.

- By resource type, crude oil accounted for 59.8% share of the Algeria oil and gas upstream market size in 2025, and natural gas is expected to advance at a 4.6% CAGR to 2031.

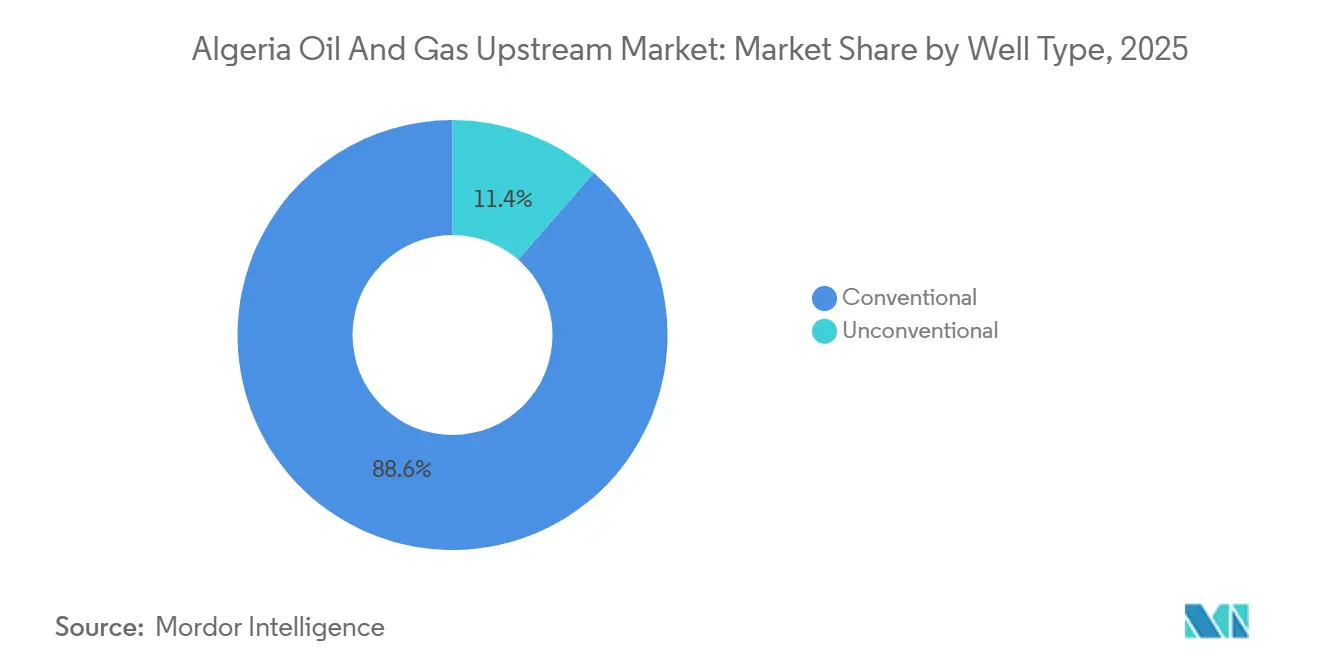

- By well type, conventional drilling dominated with 88.6% of Algeria's oil and gas upstream market share in 2025, whereas unconventional wells are expected to grow at 6.7% CAGR over 2026-2031.

- By service, development and production services held 67.0% of the Algeria oil and gas upstream market size in 2025, and exploration services are expected to grow at 7.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Algeria Oil And Gas Upstream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated post-COVID capex rebound in mature Saharan fields | +0.8% | National, concentrated in Hassi Messaoud, Hassi R'Mel, Berkine, and Illizi basins | Medium term (2-4 years) |

| Entry of Asian NOCs via risk-service contracts | +0.5% | National, with focus on gas-prone southern basins (Ahnet, Gourara, Reggane) | Long term (≥ 4 years) |

| New Hydrocarbon Law (2019) offering improved tax terms | +0.4% | National, applicable to all new exploration and production contracts | Medium term (2-4 years) |

| Surge in European gas demand for Algerian pipeline exports | +0.6% | National upstream, with export infrastructure via TransMed and Medgaz pipelines | Short term (≤ 2 years) |

| LNG back-fill requirements at Skikda & Arzew complexes | +0.3% | Coastal infrastructure linked to Saharan gas fields | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Post-COVID Capex Rebound in Mature Saharan Fields

Sonatrach's 2026-2030 plan channels most of its USD 60 billion budget into sustaining output at legacy fields, with the USD 2.3 billion Hassi R'Mel Phase III Step 2 boosting project exemplifying the focus on brownfield gas recovery.[1]James Cockayne, “Algeria ‘Launches’ $2.3bn HRM Boosting,” MEES, mees.com Hassi Messaoud's research on surfactant adsorption, published in 2025, supports enhanced oil recovery techniques aimed at reversing long-term declines. SLB expanded reservoir-characterization and horizontal-drilling services in early 2024, cutting drilling times by 33% and highlighting the cost-savings potential of digital tools. Re-mobilized capex is skewed to gas-capture and compression, supporting Algeria's pledge to curb routine flaring. The capital surge signals a policy choice favoring incremental gains from known reserves over frontier wildcatting.

Entry of Asian NOCs via Risk-Service Contracts

Sinopec’s USD 850 million Hassi Berkane North deal and ZPEC’s 30-plus-10-year Zerafa II contract typify the willingness of Asian NOCs to absorb exploration risk under Algeria’s risk-service model. ZPEC’s March 2025 national pre-qualification opened the door to all upcoming tenders. Pertamina’s 35-year MLN extension shows long-dated commitments are feasible even under the 51/49 rule.[2]Tom Pepper, “Euromajors, Chinese, Mideast NOCs Take Algeria Blocks,” Energy Intelligence, energyintel.com Asian players prize access to gas for home-market supply or LNG monetization and accept longer paybacks than many Western independents. Their presence intensifies competitive bidding for gas-prone acreage and diversifies Algeria’s partner base.

New Hydrocarbon Law (2019) Offering Improved Tax Terms

Law 19-13 introduced participation, production-sharing, and risk-service contracts, lower royalties, and faster cost-recovery ceilings, yet it still lacks 43 implementing texts, leaving legal uncertainty for bidders. Despite this, the 2024-2025 round attracted 41 firms and awarded five of six blocks, confirming that headline terms offset regulatory inertia. Sliding-scale profit splits improve gas-field economics, and a flaring tax of 12 000 dinars per 1 000 m³ incentivizes gas capture.[3]World Bank GGFR, “Global Gas Flaring Reduction Partnership,” worldbank.org However, multi-agency approvals and foreign-exchange hurdles still prolong deal closure. Operators with established Sonatrach links navigate these frictions more smoothly than newcomers.

Surge in European Gas Demand for Algerian Pipeline Exports

Algeria supplied roughly 15% of EU gas imports in 2024 via TransMed and Medgaz, reshaping upstream portfolios toward gas. Eni-Sonatrach accords in July 2025 target an extra 5.5 billion m³ per year by 2028 through USD 8 billion of joint projects. Germany’s VNG signed the first Algerian pipeline-gas deal in January 2024, routing volumes via Italy to Central Europe. Rising domestic consumption, which absorbed 55% of 2024 gas output, compels Sonatrach to accelerate field boosting and flare-recovery to free exportable supply. Europe’s multi-year offtake contracts de-risk upstream gas investments and tilt capital allocation away from crude projects.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Delay in fiscal reforms implementation bureaucracy | -0.4% | National, affecting all new contract negotiations and approvals across exploration and production segments | Medium term (2-4 years) |

| Water-stress limiting steam & EOR projects | -0.3% | Saharan oil fields, particularly Hassi Messaoud, Berkine Basin, and regions dependent on SASS aquifer system | Long term (≥ 4 years) |

| Persistent security risks in remote Saharan blocks | -0.2% | Remote Saharan exploration blocks, Trans-Saharan corridor, southern basins (Illizi, Ahnet, Gourara) | Long term (≥ 4 years) |

| Growing investor scrutiny on flaring & methane emissions | -0.2% | National, with focus on major producing fields (Hassi Messaoud, Hassi R'Mel, Berkine, Ohanet, Tiguentourine) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Delay in Fiscal-Reforms Implementation Bureaucracy

The absence of 43 implementing decrees slows contract ratification, extending negotiations by 12-18 months for ExxonMobil and Chevron shale-gas talks. Multiple ministry signatures and informal clearances raise pre-sanction costs, while the 51/49 rule complicates financing. Algeria’s non-membership of EITI and a low Resource Governance Index score highlight transparency gaps.[4]Menas Associates, “Bid to resurrect Trans-Saharan Gas Pipeline (TSGP) is likely to fail,” menas.co.uk Investment Law 22-18 promises single-window clearance but remains understaffed. The drag falls hardest on offshore and unconventional schemes with long lead times, reinforcing the dominance of onshore brownfields.

Water-Stress Limiting Steam & EOR Projects

The SASS aquifer runs a 1.5 billion m³ annual deficit, restricting water-intensive steam-injection needed for heavy-oil EOR. Algeria’s USD 5.4 billion desalination drive will supply 60% of drinking water by 2030, but diverts gas-fired power away from exports. Hassi Messaoud’s planned EOR hinges on developing surfactant methods that lower water volumes. Operators pivot to gas-lift and digital optimization instead of steam, slowing crude recovery gains. The constraint accelerates gas-centric activity, aligning upstream portfolios with export demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Location of Deployment: Onshore Dominance Anchors Brownfield Focus

Onshore activity captured 90.3% of Algeria's oil and gas upstream market share in 2025, reflecting decades of infrastructure in Saharan basins. Offshore's current sliver is expanding at a 6.0% CAGR as Chevron evaluates Mediterranean acreage.

Brownfield projects such as Hassi R'Mel Phase III and Zemoul El Kbar dominate near-term spending, offering quicker paybacks and leveraging existing pipelines. Offshore's scale-up depends on seismic confirmation, fiscal clarity, and deepwater service capacity, conditions favoring majors with global deepwater portfolios.

By Resource Type: Gas Gains Ground as Export Commitments Mount

Crude oil held 59.8% of Algeria's oil and gas upstream market size in 2025, yet natural gas is growing faster at 4.6% CAGR to meet EU import needs.

Gas projects such as Illizi Sud and Ahara underpin additional pipeline and LNG feed, while oil investments remain capped by OPEC+ quotas and water-driven EOR limits. Flaring-reduction successes unlock associated gas volumes, supporting Sonatrach's export obligations.

By Well Type: Unconventional Upside Awaits Fiscal Clarity

Conventional wells represented 88.6% of Algeria's oil and gas upstream market in 2025, though unconventional prospects are projected to climb 6.7% CAGR as shale-gas contracts mature.

High water needs and long appraisal cycles lengthen unconventional timelines, but 707 tcf of technically recoverable shale gas offers transformative upside for Algeria once fiscal and water challenges are resolved.

By Service: Exploration Surge Reflects Licensing Revival

Development and production services accounted for 67.0% share of Algeria's oil and gas upstream market size in 2025, whereas exploration services are expanding at 7.2% CAGR on the back of a revived annual bid-round calendar.

Seismic crews, appraisal wells, and feasibility studies for offshore and shale prospects are lifting exploration spend, while digital-field upgrades sustain the larger development-and-production segment.

Geography Analysis

The Hassi R’Mel hub anchors national gas output, with a USD 2.3 billion upgrade sustaining 188 million m³ per day throughput. Berkine Basin gains prominence through Zemoul El Kbar and Reggane II licenses, while Illizi attracts USD 5.4 billion of Midad Energy investment.

Security costs remain elevated in southern blocks, yet February 2025 trilateral agreements revived the Trans-Saharan Gas Pipeline vision, potentially funneling 30 billion m³ per year of Nigerian gas into Hassi R’Mel. Coastal export hubs, Skikda and Arzew, received jetty and storage upgrades to safeguard LNG loadings. Overall, basin-specific priorities converge on gas boosting and brownfield optimization to meet export pledges.

Competitive Landscape

Algeria Oil And Gas Upstream Market is semi consolidated. Sonatrach remains the dominant operator with equity production far above any partner, yet the international tier is fragmenting as Eni, TotalEnergies, Sinopec, ZPEC, and QatarEnergy secure new blocks. Asian NOCs accept high-risk acreage through risk-service terms, European majors focus on export-linked gas, and US majors target long-cycle shale gas. Digital drilling and flare-recovery technologies confer cost and ESG advantages; Corva analytics cut per-well times by 15.9 days, and Sonatrach’s 2023 flare-cut of 0.4 billion m³ ranks as the world’s largest reduction. Regulatory oversight by ALNAFT and ARH shapes partner selection and enforces the no-routine-flaring rule.

Algeria Oil And Gas Upstream Industry Leaders

Sonatrach SPA

Engie SA

Total S.A.

BP PLC

Petroceltic Ain Tsila Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Skikda LNG resumed operations after maintenance, restoring 4.5 million tpa capacity.

- October 2025: Midad Energy and Sonatrach signed a USD 5.4 billion Illizi Sud production-sharing contract.

- July 2025: Eni and Sonatrach sealed a USD 1.35 billion Zemoul El Kbar production deal with a seven-year research phase.

- July 2025: ZPEC inked a 30-plus-10-year Zerafa II production-sharing contract covering 38 697 km² and 109 billion m³ of gas.

Algeria Oil And Gas Upstream Market Report Scope

The oil and gas upstream market encompasses the exploration and production (E&P) segment of the petroleum industry. This includes activities such as locating, drilling, and extracting crude oil and natural gas from underground or underwater reservoirs.

The Algerian oil and gas upstream market is segmented into location of deployment, resource type, well type, and service. By location of deployment, the market is segmented into onshore and offshore. By resource type, the market is divided into crude oil and natural gas. By well type, the market is segmented into conventional and unconventional. By service, the market is divided into exploration, development, production, and decommissioning.

By Location of Deployment

| Onshore |

| Offshore |

By Resource Type

| Crude Oil |

| Natural Gas |

By Well Type

| Conventional |

| Unconventional |

By Service

| Exploration |

| Development and Production |

| Decommissioning |

| By Location of Deployment | Onshore |

| Offshore | |

| By Resource Type | Crude Oil |

| Natural Gas | |

| By Well Type | Conventional |

| Unconventional | |

| By Service | Exploration |

| Development and Production | |

| Decommissioning |

Key Questions Answered in the Report

How large will Algeria's upstream spending be through 2031?

Total market value is projected to reach USD 8.29 billion by 2031, reflecting a 2.58% CAGR from 2026.

Which basin is central to Algeria's future gas exports?

Hassi R-Mel remains pivotal, with a USD 2.3 billion upgrade sustaining 188 million m³ per day throughput.

What contract type attracts Asian NOCs to Algeria?

Risk-service contracts that shift exploration risk to contractors while allowing cost recovery and profit oil.

How fast is offshore activity expected to grow?

Offshore development shows a 6.0% CAGR through 2031 from a low current base.

Why is water scarcity a strategic issue for Algerian oil production?

Steam-injection EOR in mature oil fields needs large water volumes, and the SASS aquifer is already in 1.5 billion m³ annual deficit.

What is the main driver behind gas-focused investment?

European demand for non-Russian pipeline and LNG supplies positions Algerian gas as a preferred alternative.

Page last updated on: