Africa Polyethylene Terephthalate (PET) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

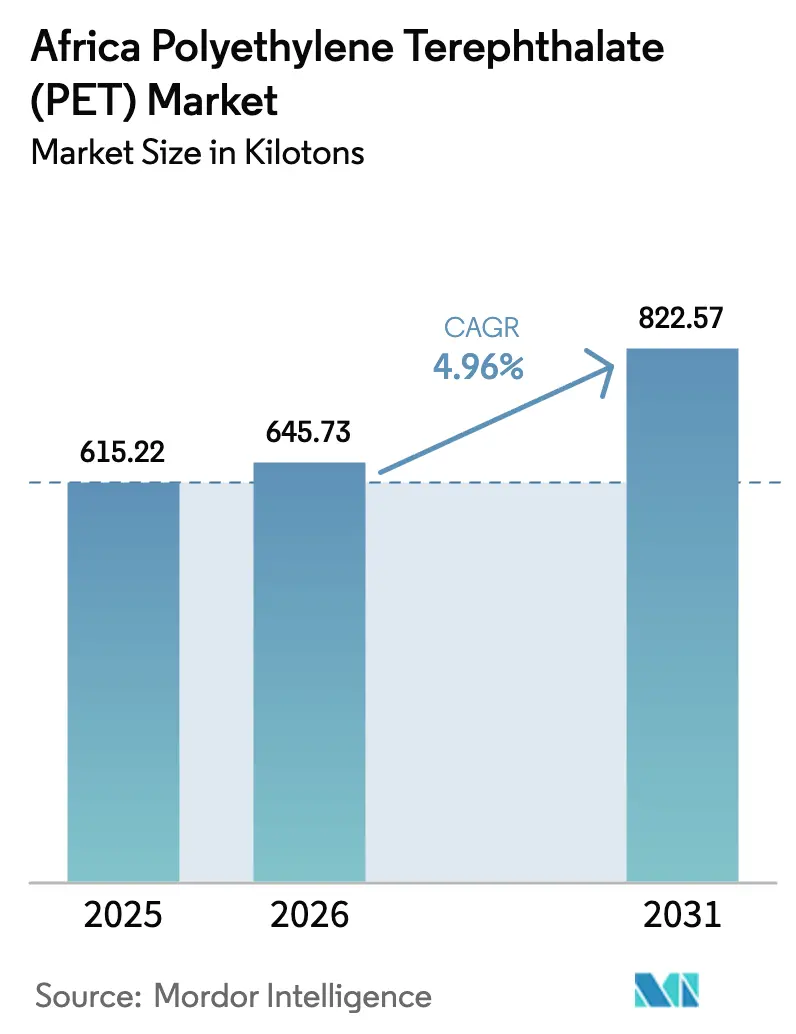

| Base Year Market Size (2025) | 615.22 kilotons |

| Market Volume (2026) | 645.73 kilotons |

| Market Volume (2031) | 822.57 kilotons |

| Growth Rate (2026 - 2031) | 4.96% CAGR |

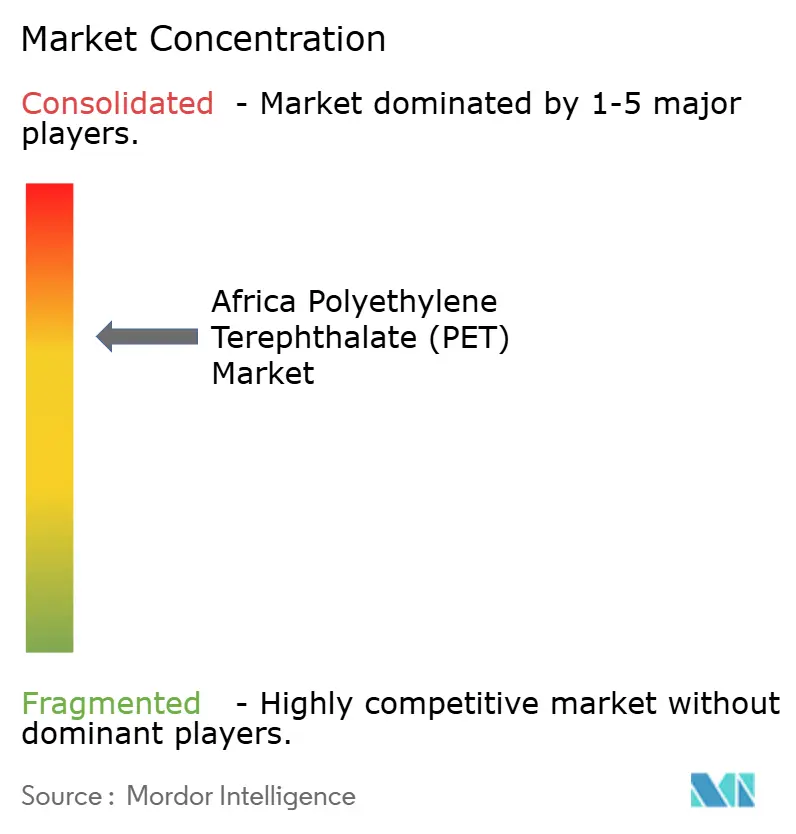

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Polyethylene Terephthalate (PET) Market Analysis by Mordor Intelligence

The Africa Polyethylene Terephthalate Market size is expected to grow from 615.22 kilotons in 2025 to 645.73 kilotons in 2026 and is forecast to reach 822.57 kilotons by 2031 at 4.96% CAGR over 2026-2031. Ongoing beverage bottling, increasing penetration of packaged foods, and a swift adoption of fiber are driving this optimistic outlook. While virgin grades continue to lead, recycled PET (rPET) is rapidly gaining traction, driven by the combination of mandatory extended-producer-responsibility (EPR) regulations, development finance initiatives, and brand commitments. The AfCFTA's tariff liberalization is reducing costs for resin and preforms, and pilot projects in chemical recycling are establishing Africa as a testing ground for closed-loop models. To mitigate energy-supply risks, converters are turning to on-site energy generation and securing long-term power-purchase agreements. Additionally, many are moving upstream into collection processes to ensure consistent feedstock prices.

Key Report Takeaways

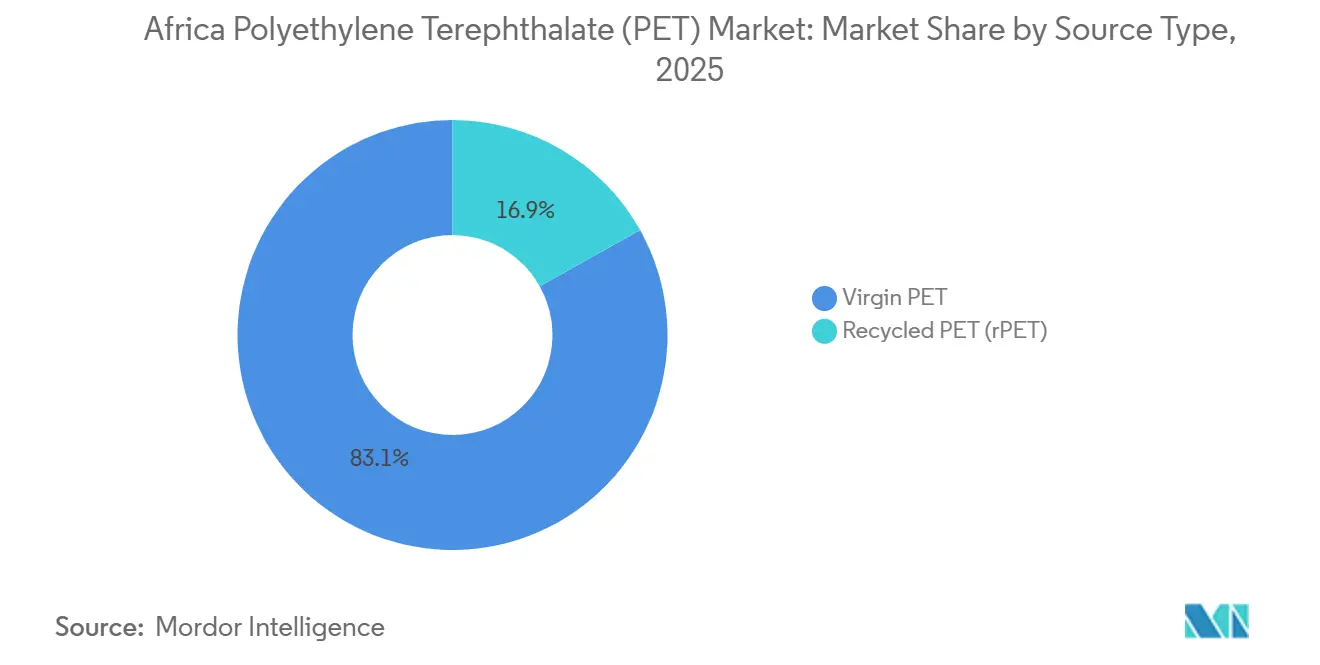

- By source type, virgin PET held an 83.11% share of the African Polyethylene Terephthalate (PET) market in 2025, while recycled PET is expanding at a 7.92% CAGR through 2031.

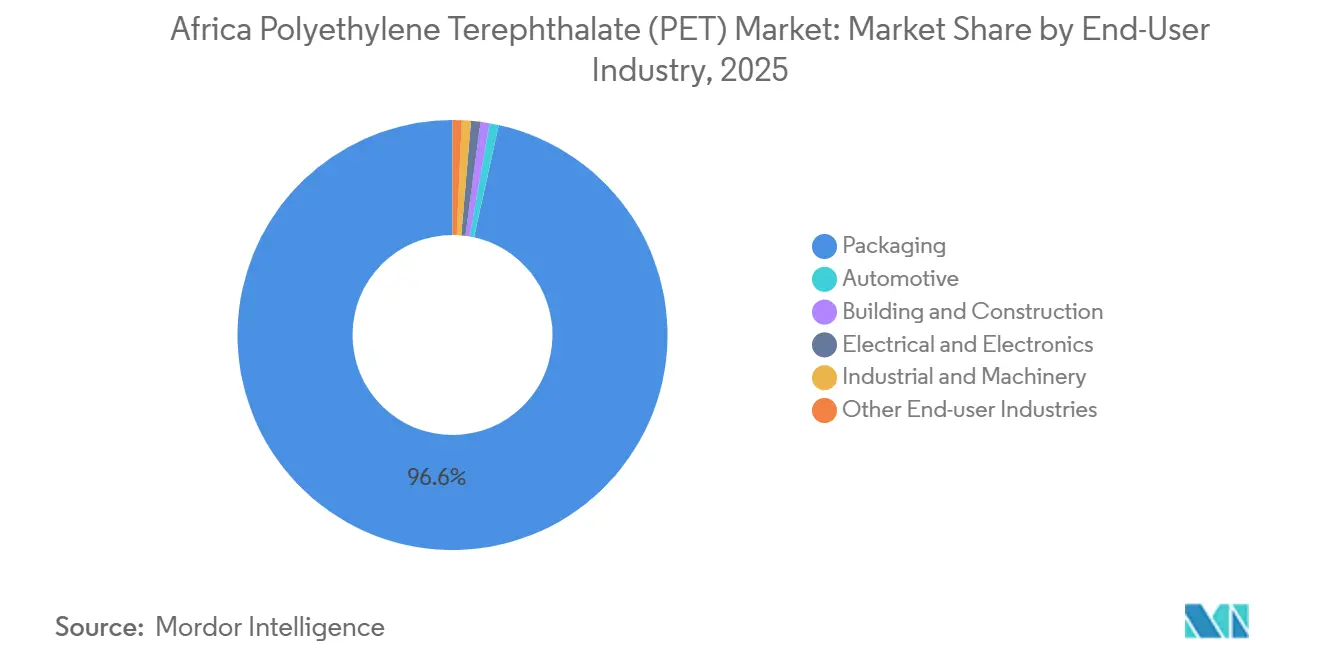

- By end-user industry, packaging commanded 96.56% of the African Polyethylene Terephthalate (PET) market share in 2025; automotive is growing the fastest at 8.11% CAGR to 2031.

- By geography, the Rest of Africa accounted for 63.11% of the Africa Polyethylene Terephthalate (PET) market size in 2025 and is projected to grow at a 5.45% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Polyethylene Terephthalate (PET) Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising beverage consumption by the region's growing middle-class | +1.2% | Global, with highest intensity in Nigeria, Kenya, Ghana, Ethiopia, Tanzania | Medium term (2-4 years) |

| Government targets for recycled-content packaging | +0.9% | South Africa, Kenya, Rwanda; spillover to SADC and EAC blocs | Long term (≥ 4 years) |

| Expansion of local bottling capacity by multinational FMCGs | +1.1% | Nigeria, South Africa, Kenya, Tanzania, Namibia, Ghana | Short term (≤ 2 years) |

| AfCFTA-driven tariff alignment lowering PET import costs | +0.8% | Continental, with early gains in GTI pilot states (Ghana, Kenya, Rwanda, Tanzania, South Africa, Nigeria, Mauritius, Egypt, Cameroon) | Medium term (2-4 years) |

| Emerging DFI/IFC financing for PET recycling infrastructure | +0.7% | Nigeria, Ghana, South Africa, Kenya; potential expansion to Tanzania, Ethiopia, Rwanda | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Beverage Consumption by the Region's Growing Middle-Class

Urbanization and rising disposable incomes are driving a surge in the demand for convenient single-serve formats. Bottled water, carbonated soft drinks, and juices collectively account for nearly half of the global consumption of transparent-bottle recycled PET (rPET). Africa, with its currently low per-capita penetration, presents significant growth potential. By 2035, the implementation of the AfCFTA is projected to elevate millions from moderate poverty, thereby broadening the consumer base for PET bottles. In anticipation of this growth, major multinational bottlers are increasing investments. Coca-Cola plans to enhance line speeds and cold-fill capabilities with investments in Namibia and South Africa during 2024–2025. Volume elasticity means beverage growth alone adds roughly 1.2 percentage points to the Africa polyethylene terephthalate (PET) market CAGR through the medium term.

Government Targets for Recycled-Content Packaging

Across Africa, policies are increasingly favoring the adoption of recycled PET (rPET). In South Africa, the EPR rule, effective from May 2025, mandates brand owners to finance end-of-life management and achieve rising recycled-content targets[1]Onyinyechi L. Uche, “Plastic Waste Regime in Rwanda, Kenya and South Africa,” ajpojournals.org. PETCO is already ensuring compliance for a multitude of companies. In Kenya, Legal Notice 176/2024 has introduced tiered EPR fees and established minimum rPET percentages, driving new investments in wash lines in Nairobi. Rwanda is seeing strengthened regulations, complemented by community initiatives, resulting in plastic recovery through various collection centers in 2025. Furthermore, a draft standard from the continental ARSO seeks to standardize food-contact clearances for rPET, aiming to cut down certification costs. Together, these measures contribute 0.9 percentage points to long-term growth for the Africa polyethylene terephthalate (PET) market.

Expansion of Local Bottling Capacity by Multinational FMCGs

Coca-Cola HBC's acquisition of a majority stake in Coca-Cola Beverages Africa has unified 13 bottling operations, ensuring a steady supply of preforms and rPET flake. In a bid to shorten delivery lead times and mitigate foreign-exchange fluctuations, PepsiCo, Nestlé, and Heineken are either refurbishing or constructing new lines in Kenya, Tanzania, and Namibia. These new lines require high-clarity resin, and contractual offtake agreements secure base loads for emerging rPET producers. This near-term driver adds about 1.1 percentage points to the forecast CAGR.

AfCFTA-Driven Tariff Alignment Lowering PET Import Costs

Starting January 2026, the Category B phase-down will eliminate duties on most tariff lines for non-LDCs over five years. Pilots of the Guided-Trade-Initiative have successfully transported PET preforms through Ghana, Kenya, and Rwanda, demonstrating efficient documentation processes under unified rules of origin. Lower border costs are enhancing converter margins and optimizing hub-and-spoke distribution, particularly from resin plants in Nigeria to the landlocked Sahel markets. Tariff reductions lift volume by 0.8 percentage points over the medium term for the Africa polyethylene terephthalate (PET) market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising consumer shift to bio-based / compostable alternatives | -0.5% | South Africa, Kenya, Rwanda; limited to premium beverage and cosmetics segments | Long term (≥ 4 years) |

| Sub-scale collection networks for rPET feedstock | -0.7% | Continental, acute in francophone West Africa, landlocked Sahel states, and rural regions | Long term (≥ 4 years) |

| Intermittent power supply inflating converter operating costs | -0.6% | South Africa, Nigeria, Ghana, Zimbabwe; episodic in Kenya, Tanzania, Zambia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Sub-Scale Collection Networks for rPET Feedstock

Informal pickers, without deposit-return incentives, continue to lead in bottle recovery. Recyclers, grappling with a shortage of clean flakes, are either turning to imported baled bottles or incurring increased sorting costs. This limitation has shifted their attention primarily to food-grade SSP lines. Furthermore, differing national food-contact approvals necessitate parallel audits for recyclers, which increases compliance expenses. The resulting feedstock bottleneck shaves 0.7 percentage points off the Africa polyethylene terephthalate (PET) market CAGR until harmonized standards and deposit schemes mature.

Intermittent Power Supply Inflating Converter Operating Costs

In recent years, load-shedding in South Africa has significantly curtailed plastics production and increased on-site diesel generation costs for converters. In Nigeria, PET processors report that the unreliability of the grid raises their bottle-blowing costs compared to their Asian counterparts. While several firms have signed solar or wheeling agreements, widespread grid upgrades will take years, exerting a short-term drag of 0.6 percentage points on the Africa polyethylene terephthalate (PET) market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source Type: Virgin Resin Dominates, yet rPET Gains Momentum

In 2025, imports from the Middle-East and Asia bolstered the dominance of virgin resin, capturing an 83.11% share. However, rPET output has surged at a 7.92% CAGR through 2031, that of virgin resin, fueled by newly commissioned facilities in South Africa, Ghana, and Nigeria. Extrupet has boosted its capacity with an added recoSTAR line, elevating its total output. In 2025, ALPLA's Ballito unit also augmented its capacity. Consequently, rPET has steadily increased its stake in Africa's polyethylene terephthalate (PET) market. Mohinani Group, with backing from IFC, is broadening the supply landscape with a plant spanning Ghana and Nigeria. Moreover, pilot projects in chemical recycling, targeting colored bottles, suggest a potential to tap into previously landfilled streams, enhancing rPET's market penetration beyond prior forecasts.

Local resin initiatives are gaining traction. Indorama Ventures has inaugurated an SSP in Port Harcourt, directly serving Nigerian bottlers. At the same time, Wankai is channeling investments into a polymerization unit, a strategic move aimed at reducing West Africa's reliance on imports. Yet, uncertainties in commissioning and challenges with feedstock suggest that virgin imports will continue to dominate, ensuring Africa's polyethylene terephthalate (PET) market remains robust throughout the forecast period of 2026–2031.

By End-User Industry: Packaging Hegemony, Automotive Emergence

Packaging absorbed 96.56% of 2025 demand, reflecting beverage and edible-oil dominance. The African market for polyethylene terephthalate (PET) is projected to grow steadily over the forecast period of 2026–2031, although its market share is expected to experience a slight decline. The automotive sector is establishing a niche, with manufacturers of tire cords and interior trims increasingly adopting recycled PET (rPET) yarns to comply with original equipment manufacturer (OEM) recycled-content mandates. Continental has developed an innovative process that converts bottles into tires, and assemblers in South Africa are considering similar material transitions. Automotive’s faster 8.11% CAGR through 2031 could lift its Africa polyethylene terephthalate (PET) market share from a low base. Although construction applications, such as recycled-plastic bricks and pavers, remain in the experimental phase, they indicate the potential for emerging value chains focused on low-grade flakes. Furthermore, with the expansion of apparel manufacturing clusters driven by African Continental Free Trade Area (AfCFTA) incentives, textiles are expected to become a significant outlet.

Geography Analysis

The rest of Africa accounted for 63.11% of the 2025 volume and is forecast to grow at a 5.45% CAGR to 2031. Indorama, anchoring the virgin supply in Nigeria, operates a running unit, while Wankai plans to establish a new production line. Polysmart is preparing to launch a recycling plant in 2026, which will have the largest capacity in sub-Saharan Africa. Ghana is expected to benefit from Mohinani’s rPET hub, supported by IFC financing, which seamlessly integrates collection with preform molding. In Kenya, a tiered EPR fee is driving investments in washing facilities around Nairobi. Meanwhile, Rwanda's model, supported by levies, effectively transforms community service days into efficient bottle-recovery operations.

Leveraging its robust waste-management framework, South Africa has emerged as the cornerstone of recycling. PETCO's producer funding achieved a commendable collection rate in 2022, and with the implementation of new EPR thresholds in May 2025, this advantage has been further solidified. While energy volatility remains a challenge, companies such as ALPLA, Extrupet, and Mpact have strategically positioned themselves near ports and fiber-optic corridors to mitigate logistics and power-supply issues. Additionally, Safripol's AspireR resin, produced in Durban, is targeting brands that prioritize Life-Cycle-Assessment-verified carbon reductions.

Although North Africa's contribution is modest, its role is crucial, particularly for exports destined for Europe. Sumilon Eco Pet Sarl, based in Tangier, produces EFSA-compliant pellets tailored specifically for EU beverage clients[2]Sumilon Eco Pet Sarl, “Manufacturer & Exporter of PET Food-Grade R-PET Resins,” sumiecopet.com. Furthermore, Egypt's participation in the Guided Trade Initiative not only highlights its strategic importance but also establishes it as a vital link between processors in the Maghreb region and converters in East Africa, especially as AfCFTA certificates of origin have gained routine acceptance.

Competitive Landscape

The Africa polyethylene terephthalate (PET) market is moderately consolidated. Technological differentiation is becoming increasingly evident. South African recyclers are turning to Starlinger recoSTAR and Krones MetaPure lines, while West African startups favor more economical cold-wash systems, adept at producing flakes for fibers and straps. However, bio-based alternatives, exemplified by Fortis X’s plant-bottle line, remain niche, largely due to their steep cost premium. As AfCFTA liberalizes trade, competition heats up with diminishing tariff protections. Major players, equipped with scale, stable power, and traceable feedstock, stand ready to expand their market share. Meanwhile, smaller converters may discover fresh prospects in specialized areas, such as PET-based construction materials.

Africa Polyethylene Terephthalate (PET) Industry Leaders

Indorama Ventures Public Company Limited

Safripol Pty Ltd

ALPLA

Extrupet (Pty) Ltd.

Mpact Group Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: ALPLA has unveiled a state-of-the-art recycling facility in South Africa, backed by an investment of EUR 60 million. Situated in the KwaZulu-Natal province, the plant is projected to produce up to 35,000 tonnes of recycled PET (rPET) annually starting in 2025.

- September 2024: Norfund, the Norwegian investment fund for developing countries, has granted a loan to the Mohinani Group. The investment will enhance the Mohinani Group's rPET production, with facilities operated by Polytanks Ghana Limited and Sonnex Packaging Nigeria Limited, each capable of producing up to 15,000 tons of rPET resin annually.

Africa Polyethylene Terephthalate (PET) Market Report Scope

Polyethylene terephthalate (PET), a member of the polyester family, is a robust, lightweight, transparent, and recyclable thermoplastic polymer resin. Known for its durability, gas-barrier properties, and impact resistance, PET finds applications in plastic bottles (like those for water and soft drinks) and synthetic fibers used in clothing and fabrics.

The Africa polyethylene terephthalate (PET) market is segmented by source type, end-user industry, and geography. By source type, the market is segmented into virgin PET and recycled PET (rPET). By end-user industry, the market is segmented into automotive, building and construction, electrical and electronics, industrial and machinery, packaging, and other end-user industries. By geography, the market is segmented accordingly. The report also covers the market size and forecasts in two countries across the African region. For each segment, the market sizing and forecasts have been done based on volume (Tons).

| Virgin PET |

| Recycled PET (rPET) |

| Automotive |

| Building and Construction |

| Electrical and Electronics |

| Industrial and Machinery |

| Packaging |

| Other End-user Industries |

| Nigeria |

| South Africa |

| Rest of Africa |

| By Source Type | Virgin PET |

| Recycled PET (rPET) | |

| By End-User Industry | Automotive |

| Building and Construction | |

| Electrical and Electronics | |

| Industrial and Machinery | |

| Packaging | |

| Other End-user Industries | |

| By Geography | Nigeria |

| South Africa | |

| Rest of Africa |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Industrial Machinery, Electrical & Electronics, and Others are the end-user industries considered under the polyethylene terephthalate market.

- Resin - Under the scope of the study, virgin polyethylene terephthalate resin in primary forms such as liquid, powder, pellet, etc. are considered.

| Keyword | Definition |

|---|---|

| Acetal | This is a rigid material that has a slippery surface. It can easily withstand wear and tear in abusive work environments. This polymer is used for building applications such as gears, bearings, valve components, etc. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Cast film | A cast film is made by depositing a layer of plastic onto a surface then solidifying and removing the film from that surface. The plastic layer can be in molten form, in a solution, or in dispersion. |

| Colorants & Pigments | Colorants & Pigments are additives used to change the color of the plastic. They can be a powder or a resin/color premix. |

| Composite material | A composite material is a material that is produced from two or more constituent materials. These constituent materials have dissimilar chemical or physical properties and are merged to create a material with properties unlike the individual elements. |

| Degree of Polymerization (DP) | The number of monomeric units in a macromolecule, polymer, or oligomer molecule is referred to as the degree of polymerization or DP. Plastics with useful physical properties often have DPs in the thousands. |

| Dispersion | To create a suspension or solution of material in another substance, fine, agglomerated solid particles of one substance are dispersed in a liquid or another substance to form a dispersion. |

| Fiberglass | Fiberglass-reinforced plastic is a material made up of glass fibers embedded in a resin matrix. These materials have high tensile and impact strength. Handrails and platforms are two examples of lightweight structural applications that use standard fiberglass. |

| Fiber-reinforced polymer (FRP) | Fiber-reinforced polymer is a composite material made of a polymer matrix reinforced with fibers. The fibers are usually glass, carbon, aramid, or basalt. |

| Flake | This is a dry, peeled-off piece, usually with an uneven surface, and is the base of cellulosic plastics. |

| Fluoropolymers | This is a fluorocarbon-based polymer with multiple carbon-fluorine bonds. It is characterized by high resistance to solvents, acids, and bases. These materials are tough yet easy to machine. Some of the popular fluoropolymers are PTFE, ETFE, PVDF, PVF, etc. |

| Kevlar | Kevlar is the commonly referred name for aramid fiber, which was initially a Dupont brand for aramid fiber. Any group of lightweight, heat-resistant, solid, synthetic, aromatic polyamide materials that are fashioned into fibers, filaments, or sheets is called aramid fiber. They are classified into Para-aramid and Meta-aramid. |

| Laminate | A structure or surface composed of sequential layers of material bonded under pressure and heat to build up to the desired shape and width. |

| Nylon | They are synthetic fiber-forming polyamides formed into yarns and monofilaments. These fibers possess excellent tensile strength, durability, and elasticity. They have high melting points and can resist chemicals and various liquids. |

| PET preform | A preform is an intermediate product that is subsequently blown into a polyethylene terephthalate (PET) bottle or a container. |

| Plastic compounding | Compounding consists of preparing plastic formulations by mixing and/or blending polymers and additives in a molten state to achieve the desired characteristics. These blends are automatically dosed with fixed setpoints usually through feeders/hoppers. |

| Plastic pellets | Plastic pellets, also known as pre-production pellets or nurdles, are the building blocks for nearly every product made of plastic. |

| Polymerization | It is a chemical reaction of several monomer molecules to form polymer chains that form stable covalent bonds. |

| Styrene Copolymers | A copolymer is a polymer derived from more than one species of monomer, and a styrene copolymer is a chain of polymers consisting of styrene and acrylate. |

| Thermoplastics | Thermoplastics are defined as polymers that become soft material when it is heated and becomes hard when it is cooled. Thermoplastics have wide-ranging properties and can be remolded and recycled without affecting their physical properties. |

| Virgin Plastic | It is a basic form of plastic that has never been used, processed, or developed. It may be considered more valuable than recycled or already used materials. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms