Size and Share of Advanced Authentication Market In Financial Services Industry

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

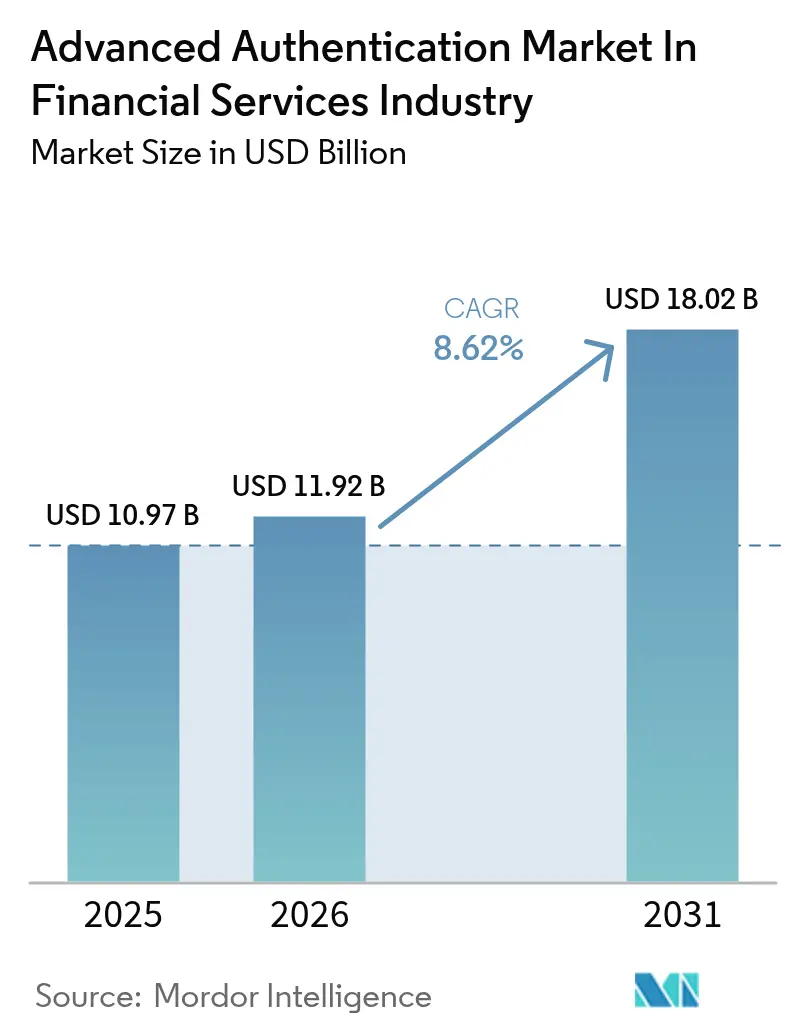

| Market Size (2026) | USD 11.92 Billion |

| Market Size (2031) | USD 18.02 Billion |

| Growth Rate (2026 - 2031) | 8.62% CAGR |

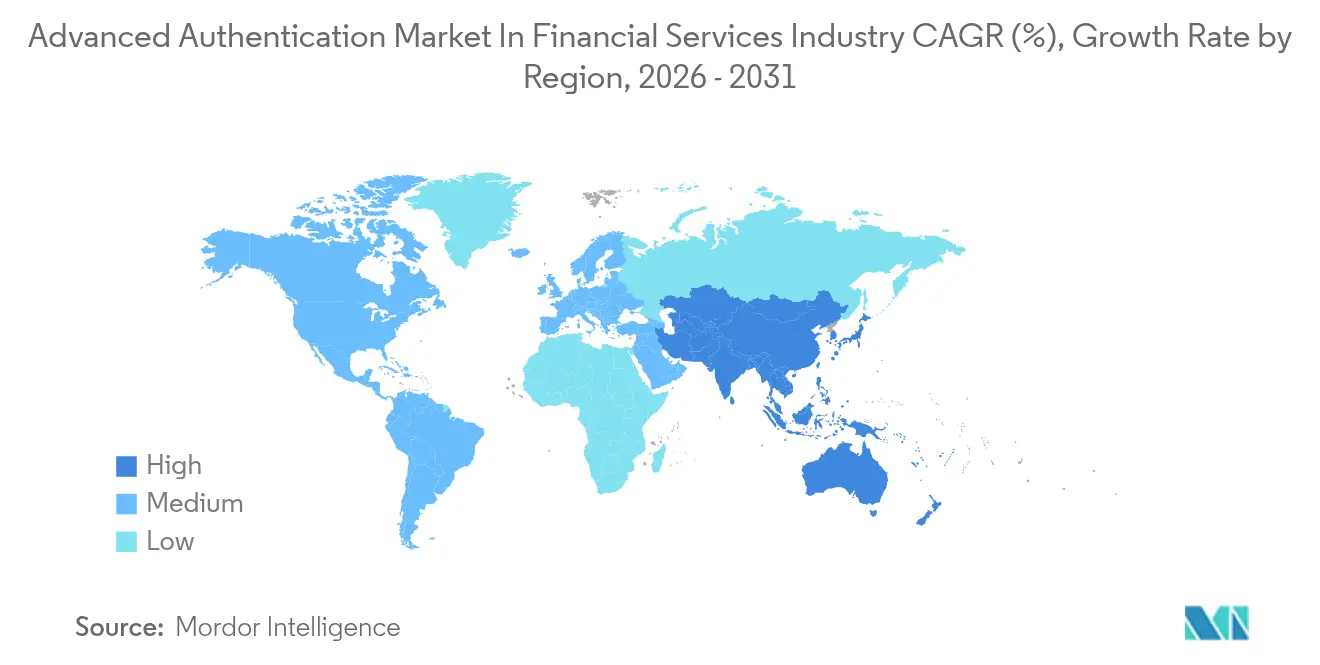

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

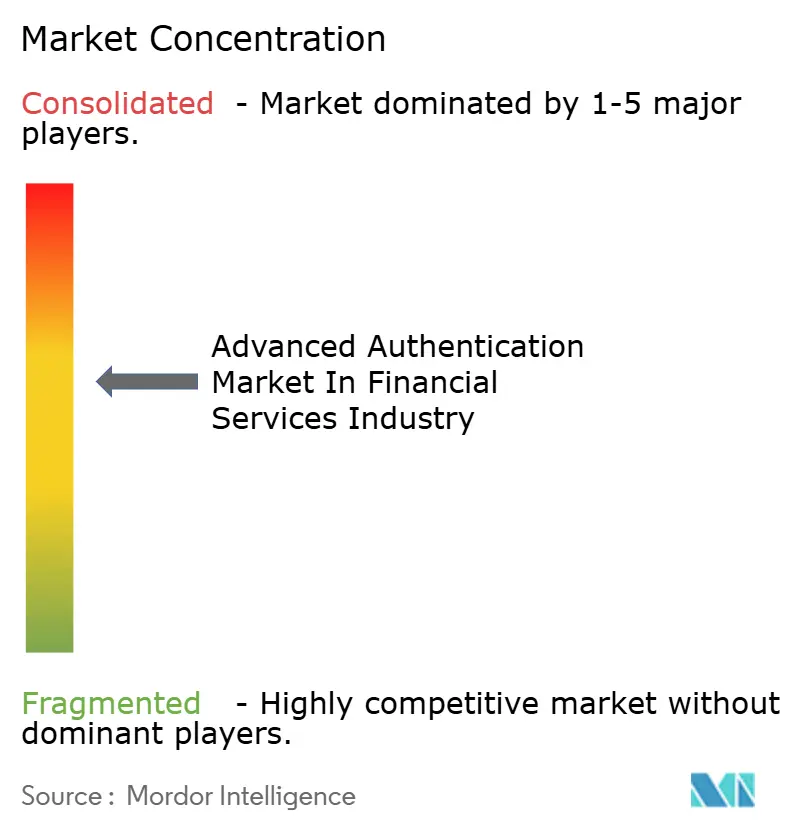

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Analysis of Advanced Authentication Market In Financial Services Industry by Mordor Intelligence

The advanced authentication market size in the financial services industry was valued at USD 10.97 billion in 2025 and estimated to grow from USD 11.92 billion in 2026 to reach USD 18.02 billion by 2031, at a CAGR of 8.62% during the forecast period (2026-2031). Growth rests on four pillars: rapid digitization of retail banking, tighter global security mandates, declining sensor costs, and the expanding use of behavioral analytics that continuously verify identity, rather than at a single log-in. Institutions are reallocating budgets from hardware tokens to cloud-native platforms that orchestrate biometric, device, and behavioral signals in under 200 milliseconds, thereby protecting revenue as mobile services account for over 80% of customer interactions. Competitive differentiation now hinges on algorithm accuracy under real-world conditions, latency of less than 250 milliseconds for real-time payments, and the breadth of pre-built integrations that limit core banking code changes. Vendors able to satisfy these requirements while complying with privacy rules, such as the General Data Protection Regulation Article 9, stand to capture a disproportionate share of the advanced authentication market in the financial services industry.

Key Report Takeaways

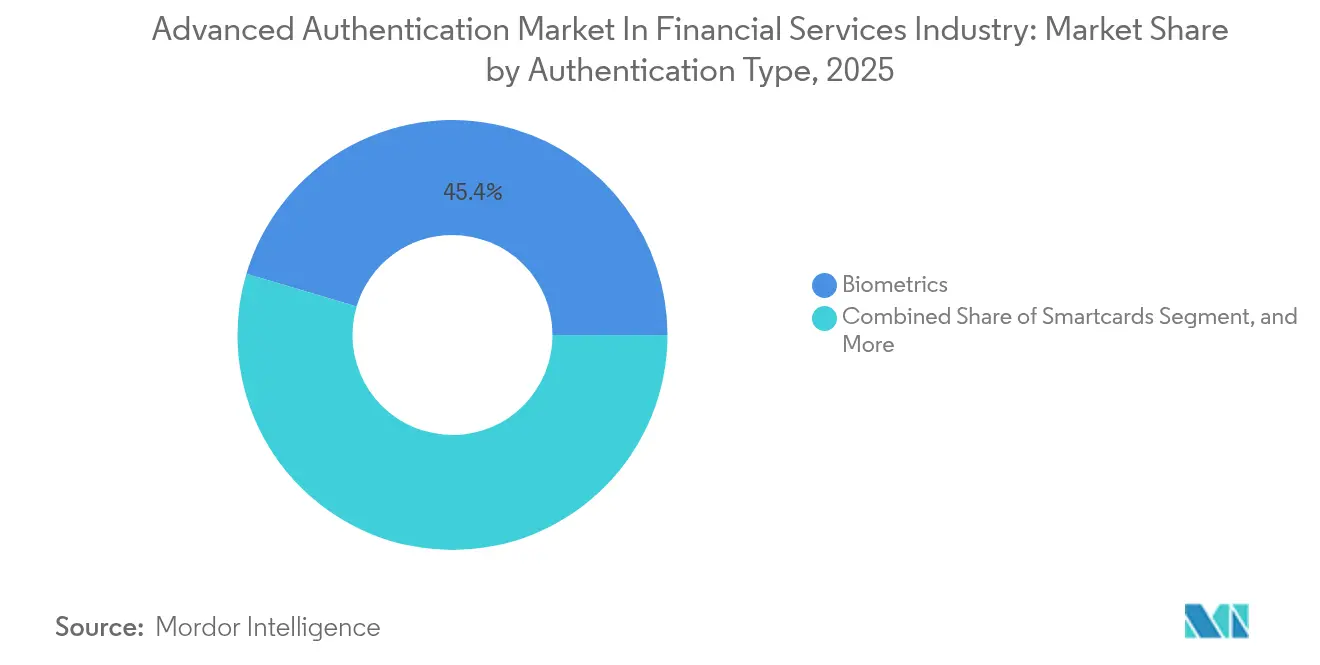

- By authentication type, biometrics led the advanced authentication market in the financial services industry with a 45.41% revenue share in 2025, while behavioral biometrics is forecast to grow at a 11.12% CAGR through 2031.

- By component, hardware contributed 44.35% of the 2025 revenue in the advanced authentication market for the financial services industry; software is projected to rise at a 10.25% CAGR through 2031.

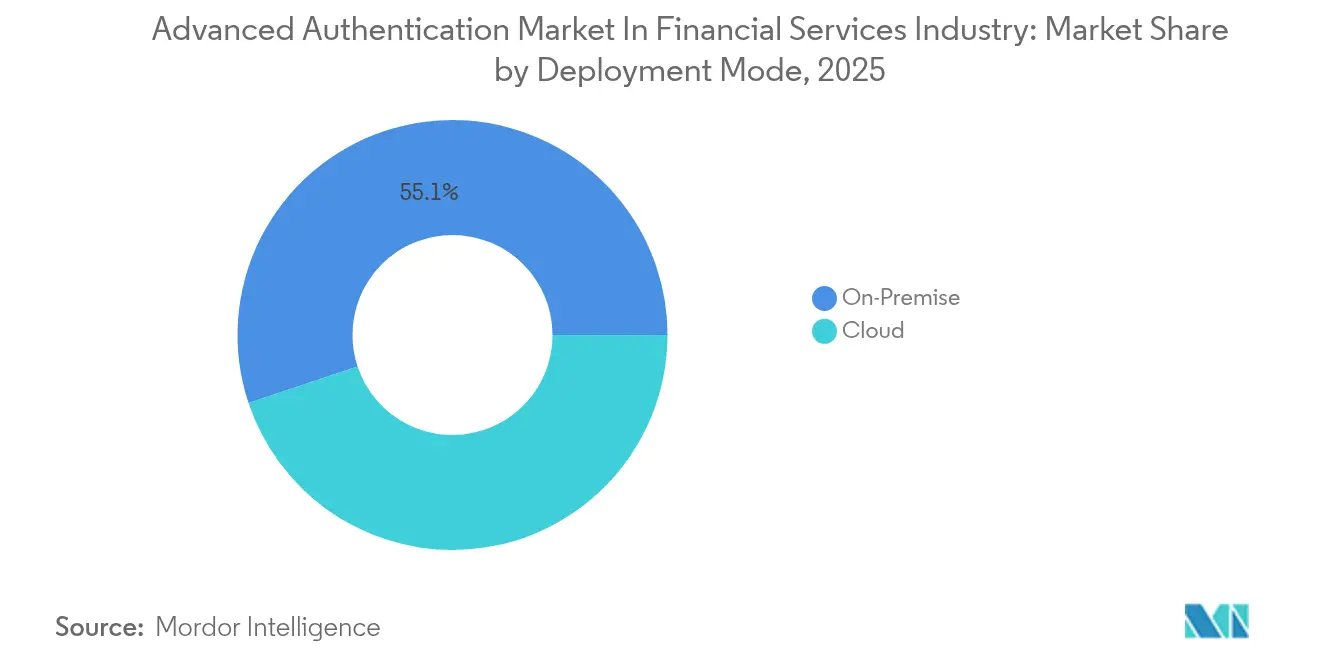

- By deployment mode, on-premise held 55.12% of the revenue in the advanced authentication market for the financial services industry in 2025; however, the cloud is set to record an 10.62% CAGR over the forecast period.

- By end-user application, retail banking accounted for 41.05% of the demand of the advanced authentication market in the financial services industry in 2025, whereas wealth management and fintech platforms are expected to expand at a 11.52% CAGR.

- By geography, North America commanded 36.85% market share of the advanced authentication market in the financial services industry in 2025, while the Asia-Pacific is forecast to post an 11.09% CAGR, the fastest worldwide.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Insights and Trends of Advanced Authentication Market In Financial Services Industry

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of digital banking and mobile transactions | +2.1% | Global, strongest in Asia-Pacific and North America | Short term (≤ 2 years) |

| Surge in regulatory mandates for strong customer authentication | +1.8% | Europe, Asia-Pacific, North America | Medium term (2-4 years) |

| Escalating cybersecurity threats and fraud losses | +1.6% | Global | Short term (≤ 2 years) |

| Growing integration of behavioral biometrics in risk-based platforms | +1.3% | North America, Europe, Asia-Pacific core | Medium term (2-4 years) |

| Adoption of decentralized identity frameworks and self-sovereign wallets | +0.9% | Europe, North America, select Asia-Pacific markets | Long term (≥ 4 years) |

| Rise of passwordless FIDO2 in ATM and branch journeys | +1.1% | North America, Europe, Japan, South Korea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Digital Banking and Mobile Transactions

Mobile penetration is expected to surpass 75% of retail clients in mature markets by 2024, and mobile apps now account for more than 60% of all non-branch transactions in North America and Europe.[1]Federal Reserve, “2024 Payments Study,” federalreserve.gov The surge compels banks to compress decision windows below 200 milliseconds, shifting investment toward biometric and behavioral methods that authenticate silently in the background. U.S. real-time payment volumes advanced 47% year over year in H1-2024, prompting demand for continuous identity assurance throughout multi-step transfers. Liveness detection is being embedded inside mobile software development kits to counter the 300% spike in deepfake attacks that regulators highlighted in 2024 incident reports. At the same time, the Payment Card Industry Data Security Standard version 4.0 requires multi-factor authentication for every card-not-present purchase exceeding USD 30, accelerating the replacement of one-time passwords with biometrics that utilize device-native sensors. Collectively, these factors add more than twenty percentage points of volume to the advanced authentication market in the financial services industry each quarter, fuelling vendor revenue expansion.

Surge in Regulatory Mandates for Strong Customer Authentication

The European Banking Authority expanded low-risk transaction exemptions to EUR 100 in 2024, while simultaneously requiring fraud-detection engines to achieve 99.5% accuracy, prompting the adoption of behavioral analytics that track over 2,000 parameters per session.[2]European Banking Authority, “Incident Reports Under PSD2 2024,” eba.europa.eu In October 2024, the Reserve Bank of India mandated an additional factor for every digital payment above INR 5,000, a rule that eliminates static passwords for 78% of retail transactions in the country. Singapore’s Monetary Authority revised its Technology Risk Management framework in March 2024, introducing risk-adaptive measures for high-value transfers, thereby favoring cloud platforms capable of ingesting threat intelligence feeds. PCI DSS v4.0 now classifies SMS one-time passwords as inadequate for privileged access, prompting U.S. banks to adopt FIDO2 keys. Collectively, these overlapping mandates lift demand for the advanced authentication market in the financial services industry by raising the regulatory floor for identity verification capabilities.

Escalating Cybersecurity Threats and Fraud Losses

Global fraud losses reached USD 485 billion in 2024, with account takeovers accounting for 38% of incidents. Synthetic identities, which combine both real and fabricated data, bypassed legacy knowledge checks in nearly one-quarter of new U.S. accounts, prompting behavioral tools that establish normal interaction baselines during onboarding. The European Central Bank reported a 62% rise in authorized push-payment fraud in 2024, highlighting the gap in systems that verify only who, not why. Ransomware attacks against core banking platforms increased 41%, exploiting weak privileged-access controls, thereby driving interest in hardware security modules that isolate keys from compromised systems. Each headline translates to budget reallocations that raise the five-year revenue trajectory for the advanced authentication market in the financial services industry.

Growing Integration of Behavioral Biometrics in Risk-Based Platforms

Behavioral engines evaluated more than 12 billion user sessions in 2024, detecting anomalies via typing rhythm, mouse velocity, and device orientation that physiological biometrics alone cannot reveal. BioCatch processed authentication checks for 78 financial institutions over four continents and reported false-positive rates under 0.1%. Early adopters reported 34% fewer fraudulent wire transfers after continuous monitoring replaced single-point logins. The European Banking Authority now accepts behavioral scores as a valid inherent factor, provided explainability and auditability are maintained. Although building baseline profiles takes 30–90 days, institutions accept the ramp-up period because long-term savings outweigh near-term integration friction. As a result, behavioral analytics will contribute an additional 11.81% CAGR to the advanced authentication market in the financial services industry through 2030.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High implementation costs and legacy compatibility challenges | -0.8% | Global, acute in North America and Europe | Short term (≤ 2 years) |

| Data-privacy concerns over biometric storage and usage | -0.6% | Europe, North America, select Asia-Pacific markets | Medium term (2-4 years) |

| Transaction-latency sensitivity in high-frequency trading | -0.3% | North America, Europe, Asia-Pacific financial hubs | Short term (≤ 2 years) |

| Vendor lock-in risk from proprietary authentication ecosystems | -0.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Implementation Costs and Legacy Compatibility Challenges

Core systems deployed before 2015 lack native biometric application programming interfaces, which forces the use of middleware layers that can inflate costs by up to 60%. A 2024 survey of 120 community banks found that 67% cited integration complexity as the top barrier, with estimated spending ranging from USD 2 million to USD 8 million per institution. Mainframe connectors introduce latency that conflicts with Federal Financial Institutions Examination Council (FFIEC) uptime rules, which require 99.9% availability. Stranded hardware assets cost USD 12 per user when OTP tokens are decommissioned ahead of schedule. These burdens shave nearly one percentage point off the projected growth of the advanced authentication market in the financial services industry in the near term.

Data-Privacy Concerns over Biometric Storage and Usage

The General Data Protection Regulation (GDPR) Article 9 treats biometric templates as special data, driving security spending 25–35% higher than non-biometric methods. Illinois Biometric Information Privacy Act cases settled for USD 228 million in 2024, highlighting litigation exposure. The California Consumer Privacy Act updates now grant users the right to deletion, which requires institutions to design reversible template architectures, complicating compliance. Banks are testing on-device matching to remove centralized stores, but fragmentation across handset vendors degrades accuracy. These privacy headwinds suppress part of the addressable volume for the advanced authentication market in the financial services industry, although they also motivate innovation in privacy-enhancing technologies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Authentication Type: Behavioral Analytics Redefine Fraud Detection

Biometrics commanded a 45.41% market share in the advanced authentication market in 2025, reflecting the widespread use of fingerprint and facial scans during mobile logins. In contrast, behavioral biometrics is projected to post an 11.12% CAGR, the fastest growth rate within the advanced authentication market in the financial services industry, as it uncovers session anomalies that static templates miss. One-time password tokens remain entrenched in wire-approval flows but are being supplanted as phishing-resistant passkeys proliferate. Mobile smart credentials, anchored in secure elements, are riding the rise of wallets like Apple Pay, which processed more than 45 billion transactions in 2024.

Growth dynamics hinge on multi-modal strategies that combine fingerprint verification at entry with continuous behavioral monitoring throughout the session. Thales shipped 34% more biometric sensors in 2024 amid demand for flexible modality choices. FIDO Alliance data show 6 billion devices already contain embedded authenticators, obviating the need for banks to mail hardware. Together, these factors raise the revenue ceiling for the advanced authentication market in the financial services industry across this segment.

By Component: Software Platforms Displace Token Infrastructure

Hardware supplied 44.35% of revenue in 2025, anchored by smartcard readers, sensors, and OTP generators. Yet, software will grow at a 10.25% CAGR, expanding its revenue share of the advanced authentication market in the financial services industry as cloud microservices enable banks to scale elastically while meeting latency requirements. Integration and consulting services face fee pressure as vendors fold them into subscription models for faster adoption.

Sixty-eight percent of financial institutions now operate hybrid clouds, clearing the path for authentication as a service. Okta processed 1.2 trillion authentication events in fiscal 2024, showing the software’s volume capacity. Hardware security modules persist for root-of-trust functions but play a narrower role as policy engines migrate to software. This shift drives another phase of expansion in the advanced authentication market in the financial services industry.

By Deployment Mode: Cloud Architectures Enable Elastic Scaling

On-premise solutions still accounted for 55.12% of revenue in 2025, particularly among multinational banks managing data sovereignty constraints; however, cloud deployments are forecast to increase by 10.62% per year. Latency improvements of 40% were achieved for a top-10 global bank after migrating to Ping Identity’s cloud service, enabling 2.3 million authentications daily without queuing. European outsourcing guidelines mandate concentration-risk checks, fostering multi-cloud strategies that further broaden the addressable demand for advanced authentication in the financial services industry.

Hybrid approaches are the most popular transition path. Institutions retain biometric templates on premises while outsourcing risk scoring to cloud engines, thereby balancing compliance and flexibility. Over the forecast horizon, cloud-based risk engines are expected to process an ever-larger share of authentications, further solidifying their role in the advanced authentication market within the financial services industry.

By End-User Application: Wealth Platforms Embed Biometric Consent

Retail banking accounted for 41.05% of 2025 revenue as branch activities transitioned online, while wealth management and fintech platforms are expected to grow at a rate of 11.52% annually, the fastest within the advanced authentication market in the financial services industry. Robo-advisors embed biometric consent into the onboarding process, meeting securities suitability rules without requiring paper signatures. Corporate treasury continues to favor hardware tokens for segregation-of-duties compliance, but behavioral checks are gaining traction to flag insider threats.

Super-app ecosystems bundle checking, trading, and insurance products, each with distinct authentication rules. ForgeRock’s platform now supports 1.3 billion identities for financial clients, dynamically matching control rigor to transaction risk. Behavioral analytics also help guard against elder exploitation, a fraud vector that is estimated to cost USD 3.4 billion in 2024. These application-specific needs channel new funds into the advanced authentication market in the financial services industry.

Geography Analysis

North America captured 36.85% of 2025 revenue after the Federal Financial Institutions Examination Council classified SMS codes as insufficient for high-risk actions. The Asia-Pacific is poised for an 11.09% CAGR due to the Reserve Bank of India's rules, which apply an extra factor for payments above INR 5,000, and Singapore's regulations promoting adaptive authentication.

The Asia-Pacific region produced the fastest revenue growth during 2024, driven by mobile-first banking architectures that account for 68% of financial transactions on smartphones, compared with 52% in North America. Reserve Bank of India directives alone will govern more than 1.4 billion mobile subscribers by 2030, expanding the advanced authentication market in the financial services industry as banks integrate device and behavioral signals into unified risk engines. China’s big four banks adopted palm-vein solutions in 2024 pilot branches, boosting regional algorithm diversity.

Europe recorded steady but slower gains as PSD2 compliance programs matured. Yet, the European Banking Authority’s 2024 update, which allows transaction-risk analysis exemptions below EUR 100, encourages the broader use of behavioral biometrics and reduces friction in e-commerce checkouts. Nordic issuers are now testing voice biometrics for telephone banking, adding another inherent factor to their multi-channel strategies.

North America’s growth centers on real-time payments and branch modernization. U.S. credit unions have adopted FIDO2 keys to support cashierless branches, while Canadian banks are embedding hardware attestation in wearable devices. The advanced authentication market size at the regional level is projected to reach USD 6.64 billion by 2031, accounting for 36.85% of global demand, underscoring its strategic significance within the advanced authentication market in the financial services industry.

Competitive Landscape

Competition is moderate, with the top five players holding roughly 42% of 2024 revenue, a level that translates to a concentration score of 6. Thales, NEC, Okta, Yubico, and Ping Identity anchor the field, each extending portfolios by acquiring algorithm specialists or launching multi-modal products. Thales partnered with a top-five European bank to replace OTP tokens across 12 million customers, reducing authentication friction by 68%.[3]Thales Group, “Annual Report 2024,” thalesgroup.com NEC secured a USD 47 million deal with a Southeast Asian central bank to deploy multi-modal biometrics supporting 2 million daily authentications.

The strategic focus has shifted toward vertical integration, which bundles sensors, algorithms, and orchestration layers to create a comprehensive solution. Okta bought Spera Security in 2024 to embed identity-threat detection into its cloud stack, enhancing anomaly scoring for financial clients. Duo Security, under Cisco, has integrated adaptive risk signals into its Secure Access Service Edge (SASE) platform, reducing branch user latency without compromising control depth.[4]Cisco Systems, “Duo Security Integration Announcement 2024,” cisco.com

Niche entrants target gaps in the advanced authentication market year-over-year, such as decentralized passkey wallets from HYPR and post-quantum authenticators under development by startups in Israel and the United States. Patent filings in behavioral biometrics surged 47%year-over-yearr, signaling ongoing innovation despite regulatory complexities.

Leaders of Advanced Authentication Market In Financial Services Industry

Thales Group

NEC Corporation

Broadcom Inc.

Fujitsu Limited

Cisco Systems Inc. (Duo Security LLC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Thales Group partnered with a top-five European bank to deploy mobile biometric authentication across 12 million users, reducing friction by 68% while maintaining a fraud detection rate above 99.7%.

- October 2024: Okta acquired Spera Security to couple authentication anomalies with endpoint signals for proactive credential defense.

- September 2024: NEC won a USD 47 million contract from a Southeast Asian central bank for a nationwide multi-modal biometric payment infrastructure.

- August 2024: Cisco integrated Duo Security’s adaptive engine with its secure-access edge, letting banks modulate controls by device trust and location.

Scope of Report on Advanced Authentication Market In Financial Services Industry

The Advanced Authentication Market in the Financial Services Industry Segments by Authentication Type (Smartcards, Biometrics [fingerprint, facial, iris, voice], Mobile Smart Credentials, One-Time Password Tokens, and Behavioral Biometrics), Component (Hardware, Software, and Services), Deployment Mode (On-Premise and Cloud), End-User Application (Retail Banking, Corporate and Investment Banking, Payment Cards and Digital Payments, Insurance, Wealth Management and FinTech Platforms, and Other End-User Applications), and Geography (North America [United States, Canada, Mexico], South America [Brazil, Argentina, Rest of South America], Europe [Germany, United Kingdom, France, Italy, Spain, Russia, Rest of Europe], Asia-Pacific [China, Japan, India, South Korea, Australia, Rest of Asia-Pacific], and Middle East and Africa [Middle East – Saudi Arabia, United Arab Emirates, Turkey, Rest of Middle East; Africa – South Africa, Nigeria, Egypt, Rest of Africa]). The Market Forecasts are Provided in Value (USD).

| Smartcards |

| Biometrics (fingerprint, facial, iris, voice) |

| Mobile Smart Credentials |

| One-Time Password Tokens |

| Behavioral Biometrics |

| Hardware |

| Software |

| Services |

| On-Premise |

| Cloud |

| Retail Banking |

| Corporate and Investment Banking |

| Payment Cards and Digital Payments |

| Insurance |

| Wealth Management and FinTech Platforms |

| Other End-User Applications |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Authentication Type | Smartcards | ||

| Biometrics (fingerprint, facial, iris, voice) | |||

| Mobile Smart Credentials | |||

| One-Time Password Tokens | |||

| Behavioral Biometrics | |||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| By Deployment Mode | On-Premise | ||

| Cloud | |||

| By End-User Application | Retail Banking | ||

| Corporate and Investment Banking | |||

| Payment Cards and Digital Payments | |||

| Insurance | |||

| Wealth Management and FinTech Platforms | |||

| Other End-User Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the advanced authentication market size in financial services for 2026?

It reached USD 11.92 billion in 2026 and is on course to hit USD 18.02 billion by 2031.

Which authentication type is expanding fastest among banks and fintech firms?

Behavioral biometrics, projected to grow at an 11.12% CAGR as institutions seek continuous, risk-adaptive identity checks.

What share of revenue did North America contribute in 2025?

North America accounted for 36.85% of global revenue, driven by updated FFIEC and PCI DSS mandates.

Why are cloud deployments gaining traction over on-premise models?

Cloud nodes cut mobile-transaction latency by around 40% and let banks scale without buying more hardware, fostering an 10.62% CAGR for cloud deployments.

Which regulations are most shaping authentication investments?

Strong Customer Authentication rules in Europe, Reserve Bank of India extra-factor mandates, and PCI DSS v4.0 requirements for phishing-resistant controls collectively steer budgets toward advanced solutions.

What is the main restraint holding back wider adoption?

High integration costs with legacy core systems, which raise total ownership by up to 60% and delay rollouts, especially among mid-tier banks.

Page last updated on: